IRT Business Model Canvas

Download IRT’s Complete Business Model Canvas—Turn Strategic Insight into Action

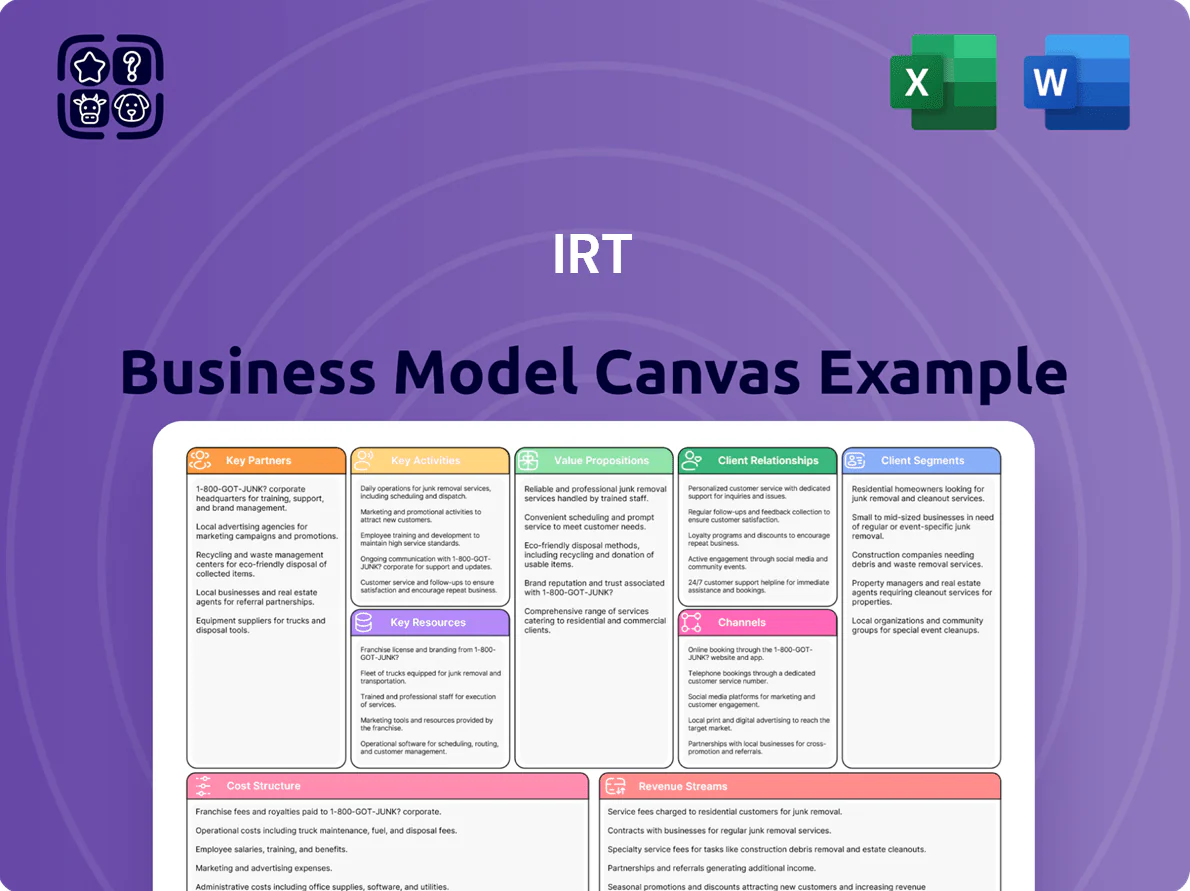

Unlock IRT’s full strategic blueprint with our complete Business Model Canvas—detailing value propositions, customer segments, key partners, revenue streams, and cost drivers to reveal how the company scales and sustains advantage. Ideal for entrepreneurs, investors, and consultants, this ready-to-use Word/Excel file accelerates benchmarking, strategic planning, and investor presentations—purchase the full canvas to turn insight into action.

Partnerships

Financial Institutions and Lenders

IRT keeps strategic ties with major banks and credit agencies to secure debt for large acquisitions, including $1.2–1.5 billion in revolving credit lines and $800 million+ in term loans committed as of Q4 2025; these facilities support liquidity and capital-structure flexibility. By end-2025, these partners are essential for navigating ~5–6% prevailing corporate borrowing rates and refinancing roughly $600–900 million of maturing debt at competitive terms.

Local Maintenance and Service Contractors

IRT partners with local vendors and contractors for specialized maintenance, landscaping, and emergency repairs across its 12,400+ apartment units, cutting fixed overhead by an estimated 18% while preserving property values and boosting resident retention rates—management reports a 6–9% lower turnover where local partners are used. This network lets IRT scale into growth markets quickly, avoiding full-time specialist payrolls and saving roughly $2,000–$4,500 per unit annually in outsourced service efficiency.

Technology and PropTech Providers

Real Estate Brokerage Firms

Renovation and Construction Firms

Strategic partnerships with renovation and construction firms enable IRT’s value-add program to upgrade units and common areas, driving rent premiums—US multifamily renovations raised rents by ~12% on average in 2023, a useful benchmark for IRT.

Long-term contractor agreements help IRT lock unit renovation costs (typical per-unit scope: $8k–$18k in 2024 markets) and meet timelines across regions, reducing variance in ROI and vacancy days.

- Average rent uplift target ~10–15%

- Per-unit renovation cost range $8,000–$18,000

- Standard project timeline 2–6 weeks/unit

- Long-term contracts cut cost variance by ~15%

IRT partners drive liquidity, ops efficiency and 10–15% rent uplifts via strategic alliances

IRT’s key partners—banks (providing $1.2–1.5B revolvers, $800M+ term loans as of Q4 2025), PropTech vendors, regional brokers (35% of 2024 deals), and long‑term contractors—support liquidity, ops efficiency, and 10–15% rent uplift from $8k–$18k/unit renovations.

| Partner | 2024–25 metric | Impact |

|---|---|---|

| Banks/credit | $1.2–1.5B revolver; $800M+ term | Refinance $600–900M; 5–6% rates |

| Brokers | 35% acquisitions; $420M recycled | Off‑market deals, faster dispositions |

| PropTech | +18% digital leases; −30% response | Improve occupancy, revenue +6% |

| Contractors | $8k–$18k/unit; 2–6 wks | Rent uplift 10–15%; −15% cost variance |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to the company’s strategy, covering customer segments, channels, value propositions and revenue streams with detailed narratives and insights to support presentations and funding discussions.

Streamlines strategy mapping into an editable one-page canvas, saving hours of setup and enabling teams to quickly compare, adapt, and collaborate on business models for fast decision-making.

Activities

Portfolio Optimization and Acquisition

IRT actively acquires well-located apartment communities in metros with strong job and population growth, targeting secondary markets such as Austin-Round Rock, Phoenix-Mesa, and Columbus where rent growth averaged 6–9% in 2024 and population rose 1.2–2.3% annually.

Each deal undergoes rigorous due diligence and financial modeling—IRR and NPV stress tests, cap rate compression analysis—to meet a 12–15% target equity return and preserve risk-adjusted yields; through 2025 emphasis stays on supply-constrained, high-demand secondary markets.

Value-Add Renovation Programs

A core activity is systematic interior and exterior upgrades—modern appliances, LVP flooring, fresh kitchens and added on-site amenities—targeting middle-market renters to raise rents by 8–15% and drive 12–18% faster lease-up, based on 2024 US multifamily value-add benchmarks.

Property Management and Leasing

IRT uses hands-on property management to keep occupancy above 95% and push average rent growth around 3–5% annually; in 2024 their communities reported median occupancy of 96.2% and NOI (net operating income) gains near 4% year-over-year.

Capital Allocation and Financial Reporting

Management directs capital allocation—dividends, debt paydown, and reinvestment—balancing a target payout ratio (typically 90%+ for REITs) with debt-to-equity goals; for example, many US REITs kept net leverage near 40–50% through 2024 to preserve ratings.

As a REIT, IRT must meet IRS and SEC rules on income distribution and transparency, filing Form 10-K/10-Q and proxy statements and routinely updating investors to sustain market credibility and dividend trust.

- Target payout: 90%+ of taxable income

- Typical net leverage: ~40–50% (2024)

- Required filings: Form 10-K, Form 10-Q, proxy

- Regular shareholder communication: quarterly/annual updates

Resident Retention and Community Engagement

Resident retention drives value: by hosting regular community events, acting on resident feedback, and resolving maintenance requests within 48 hours, IRT cuts turnover and raises resident lifetime value—industry data shows a 5–7% lift in renewals for high-engagement programs, saving roughly A$1,200–A$2,500 per unit per renewal in reduced acquisition and vacancy costs (2024 Australian senior housing benchmarks).

- Events + feedback = higher renewals

- 48-hour maintenance SLA

- 5–7% renewal lift (2024)

- A$1,200–A$2,500 saved per renewal

High‑yield value-add apartments: 12–15% equity returns, 96% occupancy, 8–15% rent lift

IRT sources value-add apartments in fast-growing secondary metros, performs IRR/NPV stress tests to hit 12–15% equity returns, renovates units to lift rents 8–15% and speed lease-up 12–18%, maintains 95%+ occupancy (96.2% median in 2024), targets 90%+ payout with 40–50% net leverage, and boosts renewals 5–7% saving A$1,200–A$2,500 per renewal.

| Metric | 2024/Target |

|---|---|

| Occupancy | 96.2% |

| Equity return | 12–15% |

| Rent lift | 8–15% |

| Renewal lift | 5–7% |

| Net leverage | 40–50% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual IRT Business Model Canvas—not a mockup or sample—and it reflects the exact layout and content you will receive after purchase.

When you complete your order, you’ll get this same professional, ready-to-edit file in Word and Excel formats, with all sections and pages included—no surprises, no fillers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download IRT’s Complete Business Model Canvas—Turn Strategic Insight into Action

Unlock IRT’s full strategic blueprint with our complete Business Model Canvas—detailing value propositions, customer segments, key partners, revenue streams, and cost drivers to reveal how the company scales and sustains advantage. Ideal for entrepreneurs, investors, and consultants, this ready-to-use Word/Excel file accelerates benchmarking, strategic planning, and investor presentations—purchase the full canvas to turn insight into action.

Partnerships

Financial Institutions and Lenders

IRT keeps strategic ties with major banks and credit agencies to secure debt for large acquisitions, including $1.2–1.5 billion in revolving credit lines and $800 million+ in term loans committed as of Q4 2025; these facilities support liquidity and capital-structure flexibility. By end-2025, these partners are essential for navigating ~5–6% prevailing corporate borrowing rates and refinancing roughly $600–900 million of maturing debt at competitive terms.

Local Maintenance and Service Contractors

IRT partners with local vendors and contractors for specialized maintenance, landscaping, and emergency repairs across its 12,400+ apartment units, cutting fixed overhead by an estimated 18% while preserving property values and boosting resident retention rates—management reports a 6–9% lower turnover where local partners are used. This network lets IRT scale into growth markets quickly, avoiding full-time specialist payrolls and saving roughly $2,000–$4,500 per unit annually in outsourced service efficiency.

Technology and PropTech Providers

Real Estate Brokerage Firms

Renovation and Construction Firms

Strategic partnerships with renovation and construction firms enable IRT’s value-add program to upgrade units and common areas, driving rent premiums—US multifamily renovations raised rents by ~12% on average in 2023, a useful benchmark for IRT.

Long-term contractor agreements help IRT lock unit renovation costs (typical per-unit scope: $8k–$18k in 2024 markets) and meet timelines across regions, reducing variance in ROI and vacancy days.

- Average rent uplift target ~10–15%

- Per-unit renovation cost range $8,000–$18,000

- Standard project timeline 2–6 weeks/unit

- Long-term contracts cut cost variance by ~15%

IRT partners drive liquidity, ops efficiency and 10–15% rent uplifts via strategic alliances

IRT’s key partners—banks (providing $1.2–1.5B revolvers, $800M+ term loans as of Q4 2025), PropTech vendors, regional brokers (35% of 2024 deals), and long‑term contractors—support liquidity, ops efficiency, and 10–15% rent uplift from $8k–$18k/unit renovations.

| Partner | 2024–25 metric | Impact |

|---|---|---|

| Banks/credit | $1.2–1.5B revolver; $800M+ term | Refinance $600–900M; 5–6% rates |

| Brokers | 35% acquisitions; $420M recycled | Off‑market deals, faster dispositions |

| PropTech | +18% digital leases; −30% response | Improve occupancy, revenue +6% |

| Contractors | $8k–$18k/unit; 2–6 wks | Rent uplift 10–15%; −15% cost variance |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to the company’s strategy, covering customer segments, channels, value propositions and revenue streams with detailed narratives and insights to support presentations and funding discussions.

Streamlines strategy mapping into an editable one-page canvas, saving hours of setup and enabling teams to quickly compare, adapt, and collaborate on business models for fast decision-making.

Activities

Portfolio Optimization and Acquisition

IRT actively acquires well-located apartment communities in metros with strong job and population growth, targeting secondary markets such as Austin-Round Rock, Phoenix-Mesa, and Columbus where rent growth averaged 6–9% in 2024 and population rose 1.2–2.3% annually.

Each deal undergoes rigorous due diligence and financial modeling—IRR and NPV stress tests, cap rate compression analysis—to meet a 12–15% target equity return and preserve risk-adjusted yields; through 2025 emphasis stays on supply-constrained, high-demand secondary markets.

Value-Add Renovation Programs

A core activity is systematic interior and exterior upgrades—modern appliances, LVP flooring, fresh kitchens and added on-site amenities—targeting middle-market renters to raise rents by 8–15% and drive 12–18% faster lease-up, based on 2024 US multifamily value-add benchmarks.

Property Management and Leasing

IRT uses hands-on property management to keep occupancy above 95% and push average rent growth around 3–5% annually; in 2024 their communities reported median occupancy of 96.2% and NOI (net operating income) gains near 4% year-over-year.

Capital Allocation and Financial Reporting

Management directs capital allocation—dividends, debt paydown, and reinvestment—balancing a target payout ratio (typically 90%+ for REITs) with debt-to-equity goals; for example, many US REITs kept net leverage near 40–50% through 2024 to preserve ratings.

As a REIT, IRT must meet IRS and SEC rules on income distribution and transparency, filing Form 10-K/10-Q and proxy statements and routinely updating investors to sustain market credibility and dividend trust.

- Target payout: 90%+ of taxable income

- Typical net leverage: ~40–50% (2024)

- Required filings: Form 10-K, Form 10-Q, proxy

- Regular shareholder communication: quarterly/annual updates

Resident Retention and Community Engagement

Resident retention drives value: by hosting regular community events, acting on resident feedback, and resolving maintenance requests within 48 hours, IRT cuts turnover and raises resident lifetime value—industry data shows a 5–7% lift in renewals for high-engagement programs, saving roughly A$1,200–A$2,500 per unit per renewal in reduced acquisition and vacancy costs (2024 Australian senior housing benchmarks).

- Events + feedback = higher renewals

- 48-hour maintenance SLA

- 5–7% renewal lift (2024)

- A$1,200–A$2,500 saved per renewal

High‑yield value-add apartments: 12–15% equity returns, 96% occupancy, 8–15% rent lift

IRT sources value-add apartments in fast-growing secondary metros, performs IRR/NPV stress tests to hit 12–15% equity returns, renovates units to lift rents 8–15% and speed lease-up 12–18%, maintains 95%+ occupancy (96.2% median in 2024), targets 90%+ payout with 40–50% net leverage, and boosts renewals 5–7% saving A$1,200–A$2,500 per renewal.

| Metric | 2024/Target |

|---|---|

| Occupancy | 96.2% |

| Equity return | 12–15% |

| Rent lift | 8–15% |

| Renewal lift | 5–7% |

| Net leverage | 40–50% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual IRT Business Model Canvas—not a mockup or sample—and it reflects the exact layout and content you will receive after purchase.

When you complete your order, you’ll get this same professional, ready-to-edit file in Word and Excel formats, with all sections and pages included—no surprises, no fillers.