Isagro Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Isagro operates in a niche agrochemical segment where supplier concentration, regulatory pressure, and shifting farmer preferences shape competitive intensity; this snapshot highlights key pressures but omits granular metrics and visuals.

Want the full picture—force-by-force ratings, market data, and strategic implications—to assess Isagro’s risks and opportunities? Unlock the complete Porter's Five Forces Analysis for a consultant-grade, ready-to-use report.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The production of Isagro proprietary agrochemicals relies on niche chemical precursors from a few global suppliers; in 2025, the top five upstream specialty chemical firms control roughly 55–60% of supply for key intermediates, boosting supplier leverage.

Industry consolidation since 2020 pushed average spot prices for certain active-ingredient precursors up 12–18% by 2024–25, so Isagro needs diversified sourcing, longer contracts, and regional stockpiles to limit cost shocks and delivery risk.

Energy Price Volatility in Manufacturing

The synthesis of fungicides and insecticides is highly energy intensive, making Isagro vulnerable to 2025 natural gas and electricity volatility; EU industrial gas prices averaged €56/MWh in 2024 vs €28/MWh pre-2021, squeezing chemical margins.

Utility suppliers therefore hold substantial bargaining power over European manufacturers’ margins, so Isagro must invest in efficiency or lock long-term contracts—example: a 5-year fixed gas deal can cap fuel cost exposure and protect EBITDA.

Access to Specialized Research Talent

The supply of molecular biology and sustainable chemistry experts is a strategic input for Isagro; global biotech hiring grew 12% in 2024, pushing average senior researcher pay in Europe to ~€85k–€110k, so competition from firms and startups raises costs. With green-agriculture R&D funding up 18% in 2023–24, specialized labs and talent command stronger partnership terms and equity-like compensation, increasing their bargaining power over Isagro.

Regulatory Compliance Costs for Inputs

Suppliers face tighter environmental rules like REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), narrowing compliant vendors and raising costs which are passed to Isagro; in 2024 EU REACH-related compliance increased specialty-chemical input prices by an estimated 6–9% industry-wide.

With few certified suppliers for certain active ingredients, Isagro has limited bargaining power and cannot fully absorb price hikes—this compresses margins unless the company raises prices or cuts costs elsewhere.

- REACH narrows supplier pool

- Industry input costs +6–9% (2024)

- Limited supplier negotiation power

- Margin pressure unless price/cost adjustments

Logistical and Transportation Dependencies

Isagro’s global distribution makes shipping providers critical; by late 2025 carriers held higher bargaining power after geopolitical bottlenecks and fleet decarbonization pushed freight rates up ~18% YoY, raising landed costs and margin pressure.

Higher rates and port congestion force tighter coordination to meet seasonal planting windows; missed windows can cut sales by double digits for key crop cycles.

- Global freight +18% YoY (late 2025)

Isagro margin squeeze: supplier dominance, higher costs—urgent contracts, energy fixes

Suppliers hold high bargaining power: top 5 specialty-chemical firms control ~55–60% of key precursors (2025), REACH added ~6–9% input cost (2024), EU industrial gas ~€56/MWh (2024) vs €28/MWh pre-2021, biotech hiring +12% (2024) raising senior pay €85–110k, freight +18% YoY (late 2025); Isagro needs long contracts, regional stockpiles, and energy fixes to protect margins.

| Metric | Value |

|---|---|

| Top-5 supplier share | 55–60% |

| REACH cost impact (2024) | +6–9% |

| EU industrial gas (2024) | €56/MWh |

| Biotech hiring (2024) | +12% |

| Freight (late 2025) | +18% YoY |

What is included in the product

Tailored Porter's Five Forces analysis of Isagro that uncovers competitive pressures, supplier and buyer influence, entry barriers, substitutes, and disruptive threats—designed for inclusion in investor materials, strategy decks, or academic work and fully editable for customization.

Isagro Porter's Five Forces in one sheet—rapidly spot strengths and vulnerabilities to guide strategic moves and investor decisions.

Customers Bargaining Power

Consolidation of Agricultural Distributors

The global agri-distribution sector has concentrated: the top 10 distributors now control ~55% of global crop protection volumes (2024 IHS Markit), creating a few buyers with massive leverage over manufacturers like Isagro.

These large groups push for double-digit rebates and extended payment terms—buyers extracting 8–15% average discounts in 2023–24—squeezing Isagro’s gross margins on high-volume products.

As a result, Isagro’s pricing power weakens; losing 5 percentage points of margin on core SKUs would cut annual EBITDA by roughly €10–20m given 2024 revenue of €400m.

Low Switching Costs for Generic Products

Influence of Agricultural Cooperatives

In Italy and EU markets, agricultural cooperatives—representing over 40% of EU farm output per Eurostat 2023—buy collectively, giving them strong price leverage over Isagro and peers. Their pooled procurement from thousands of smallholders can push down margins; in 2024 distributor-negotiated discounts reached 8–12% in Southern Europe. Isagro must use targeted contracts, volume rebates, and service bundling to retain cooperative business. Coordinated marketing and crop-specific formulations reduce churn risk.

Demand for Sustainable and Bio-based Solutions

Buyers now demand low-residue and bio-based inputs; surveys show 62% of EU consumers prioritize sustainability in food purchases (2024), pushing retailers and farmers to prefer biostimulants and organic-certified crop inputs.

This trend raises buyer leverage as they steer suppliers toward greener portfolios; Isagro risks share loss unless it shifts R&D and product mix toward certified bio-solutions.

- 62% EU consumers prioritise sustainability (2024)

- Global biostimulant market grew ~10% CAGR to $4.5bn in 2024

- Retailers demand residue limits, raising switching pressure

Information Symmetry and Digital Platforms

By end-2025, digital agronomy platforms (e.g., Climate FieldView, xarvio) pushed price and efficacy transparency: global platform users rose ~35% YoY to ~9.8M farmers in 2024–25, enabling live comparisons of cost-benefit and efficacy metrics.

This shifts leverage to buyers: farmers use data to negotiate prices, switch brands, and demand bundling, reducing dependence on local reps and raising customer bargaining power vs Isagro.

- ~9.8M platform users by 2025

- 35% YoY user growth (2024–25)

- Real-time price/efficacy comparisons increase switching

Distributor rebates squeeze Isagro as generics & platforms boost buyer power

Large distributors (top 10 ≈55% global volume, 2024 IHS) and EU cooperatives (cover >40% EU output, Eurostat 2023) extract 8–15% rebates, cutting Isagro margins; 2024 revenue €400m, R&D 6.1% rev. Generic share ~40% (2024) and biostimulant market $4.5bn (2024) raise switching; digital platforms (9.8M users, 35% YoY) increase price transparency and buyer leverage.

| Metric | 2024–25 |

|---|---|

| Top‑10 distributors | ≈55% volume |

| Discounts | 8–15% |

| Isagro rev | €400m |

| R&D | 6.1% rev |

| Generic share | ≈40% |

| Biostimulant mkt | $4.5bn |

| Platform users | 9.8M |

Preview the Actual Deliverable

Isagro Porter's Five Forces Analysis

This preview shows the exact Isagro Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for download.

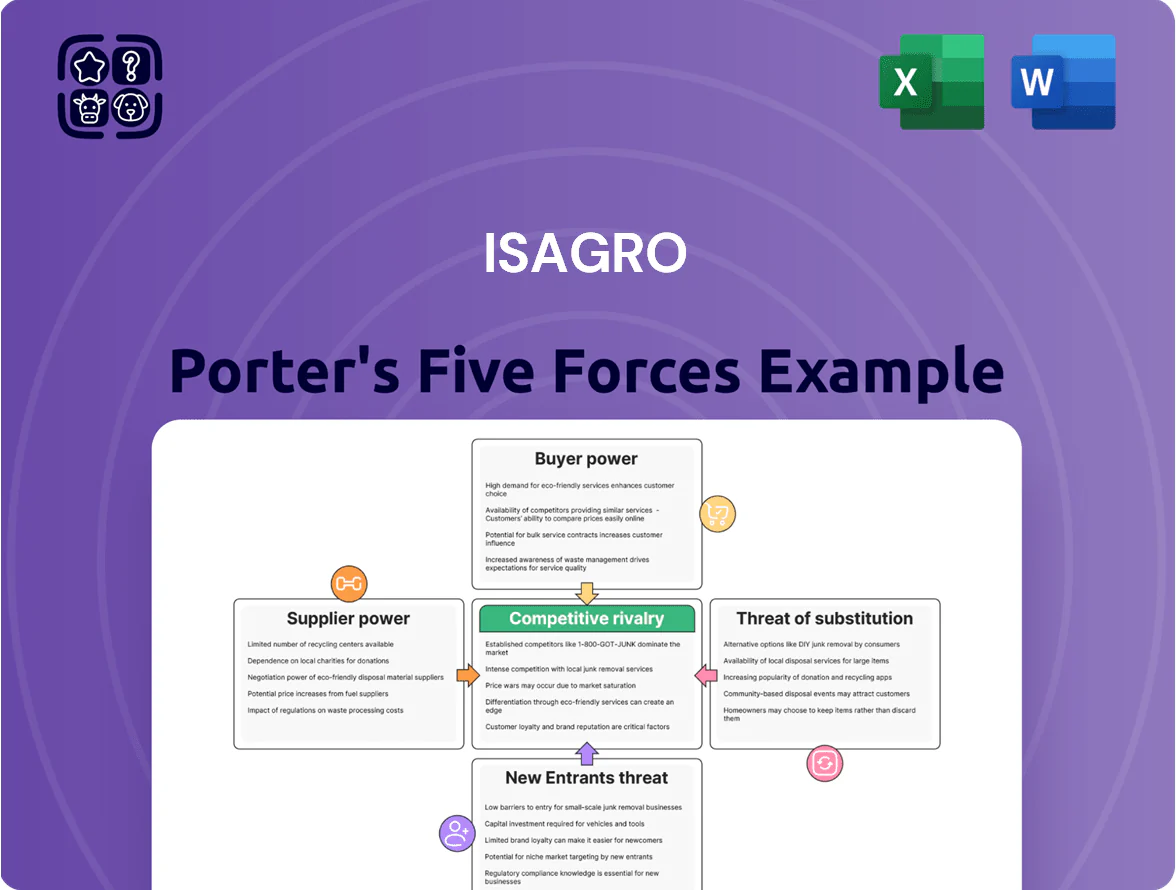

The document is the final deliverable, containing a complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Isagro operates in a niche agrochemical segment where supplier concentration, regulatory pressure, and shifting farmer preferences shape competitive intensity; this snapshot highlights key pressures but omits granular metrics and visuals.

Want the full picture—force-by-force ratings, market data, and strategic implications—to assess Isagro’s risks and opportunities? Unlock the complete Porter's Five Forces Analysis for a consultant-grade, ready-to-use report.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The production of Isagro proprietary agrochemicals relies on niche chemical precursors from a few global suppliers; in 2025, the top five upstream specialty chemical firms control roughly 55–60% of supply for key intermediates, boosting supplier leverage.

Industry consolidation since 2020 pushed average spot prices for certain active-ingredient precursors up 12–18% by 2024–25, so Isagro needs diversified sourcing, longer contracts, and regional stockpiles to limit cost shocks and delivery risk.

Energy Price Volatility in Manufacturing

The synthesis of fungicides and insecticides is highly energy intensive, making Isagro vulnerable to 2025 natural gas and electricity volatility; EU industrial gas prices averaged €56/MWh in 2024 vs €28/MWh pre-2021, squeezing chemical margins.

Utility suppliers therefore hold substantial bargaining power over European manufacturers’ margins, so Isagro must invest in efficiency or lock long-term contracts—example: a 5-year fixed gas deal can cap fuel cost exposure and protect EBITDA.

Access to Specialized Research Talent

The supply of molecular biology and sustainable chemistry experts is a strategic input for Isagro; global biotech hiring grew 12% in 2024, pushing average senior researcher pay in Europe to ~€85k–€110k, so competition from firms and startups raises costs. With green-agriculture R&D funding up 18% in 2023–24, specialized labs and talent command stronger partnership terms and equity-like compensation, increasing their bargaining power over Isagro.

Regulatory Compliance Costs for Inputs

Suppliers face tighter environmental rules like REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), narrowing compliant vendors and raising costs which are passed to Isagro; in 2024 EU REACH-related compliance increased specialty-chemical input prices by an estimated 6–9% industry-wide.

With few certified suppliers for certain active ingredients, Isagro has limited bargaining power and cannot fully absorb price hikes—this compresses margins unless the company raises prices or cuts costs elsewhere.

- REACH narrows supplier pool

- Industry input costs +6–9% (2024)

- Limited supplier negotiation power

- Margin pressure unless price/cost adjustments

Logistical and Transportation Dependencies

Isagro’s global distribution makes shipping providers critical; by late 2025 carriers held higher bargaining power after geopolitical bottlenecks and fleet decarbonization pushed freight rates up ~18% YoY, raising landed costs and margin pressure.

Higher rates and port congestion force tighter coordination to meet seasonal planting windows; missed windows can cut sales by double digits for key crop cycles.

- Global freight +18% YoY (late 2025)

Isagro margin squeeze: supplier dominance, higher costs—urgent contracts, energy fixes

Suppliers hold high bargaining power: top 5 specialty-chemical firms control ~55–60% of key precursors (2025), REACH added ~6–9% input cost (2024), EU industrial gas ~€56/MWh (2024) vs €28/MWh pre-2021, biotech hiring +12% (2024) raising senior pay €85–110k, freight +18% YoY (late 2025); Isagro needs long contracts, regional stockpiles, and energy fixes to protect margins.

| Metric | Value |

|---|---|

| Top-5 supplier share | 55–60% |

| REACH cost impact (2024) | +6–9% |

| EU industrial gas (2024) | €56/MWh |

| Biotech hiring (2024) | +12% |

| Freight (late 2025) | +18% YoY |

What is included in the product

Tailored Porter's Five Forces analysis of Isagro that uncovers competitive pressures, supplier and buyer influence, entry barriers, substitutes, and disruptive threats—designed for inclusion in investor materials, strategy decks, or academic work and fully editable for customization.

Isagro Porter's Five Forces in one sheet—rapidly spot strengths and vulnerabilities to guide strategic moves and investor decisions.

Customers Bargaining Power

Consolidation of Agricultural Distributors

The global agri-distribution sector has concentrated: the top 10 distributors now control ~55% of global crop protection volumes (2024 IHS Markit), creating a few buyers with massive leverage over manufacturers like Isagro.

These large groups push for double-digit rebates and extended payment terms—buyers extracting 8–15% average discounts in 2023–24—squeezing Isagro’s gross margins on high-volume products.

As a result, Isagro’s pricing power weakens; losing 5 percentage points of margin on core SKUs would cut annual EBITDA by roughly €10–20m given 2024 revenue of €400m.

Low Switching Costs for Generic Products

Influence of Agricultural Cooperatives

In Italy and EU markets, agricultural cooperatives—representing over 40% of EU farm output per Eurostat 2023—buy collectively, giving them strong price leverage over Isagro and peers. Their pooled procurement from thousands of smallholders can push down margins; in 2024 distributor-negotiated discounts reached 8–12% in Southern Europe. Isagro must use targeted contracts, volume rebates, and service bundling to retain cooperative business. Coordinated marketing and crop-specific formulations reduce churn risk.

Demand for Sustainable and Bio-based Solutions

Buyers now demand low-residue and bio-based inputs; surveys show 62% of EU consumers prioritize sustainability in food purchases (2024), pushing retailers and farmers to prefer biostimulants and organic-certified crop inputs.

This trend raises buyer leverage as they steer suppliers toward greener portfolios; Isagro risks share loss unless it shifts R&D and product mix toward certified bio-solutions.

- 62% EU consumers prioritise sustainability (2024)

- Global biostimulant market grew ~10% CAGR to $4.5bn in 2024

- Retailers demand residue limits, raising switching pressure

Information Symmetry and Digital Platforms

By end-2025, digital agronomy platforms (e.g., Climate FieldView, xarvio) pushed price and efficacy transparency: global platform users rose ~35% YoY to ~9.8M farmers in 2024–25, enabling live comparisons of cost-benefit and efficacy metrics.

This shifts leverage to buyers: farmers use data to negotiate prices, switch brands, and demand bundling, reducing dependence on local reps and raising customer bargaining power vs Isagro.

- ~9.8M platform users by 2025

- 35% YoY user growth (2024–25)

- Real-time price/efficacy comparisons increase switching

Distributor rebates squeeze Isagro as generics & platforms boost buyer power

Large distributors (top 10 ≈55% global volume, 2024 IHS) and EU cooperatives (cover >40% EU output, Eurostat 2023) extract 8–15% rebates, cutting Isagro margins; 2024 revenue €400m, R&D 6.1% rev. Generic share ~40% (2024) and biostimulant market $4.5bn (2024) raise switching; digital platforms (9.8M users, 35% YoY) increase price transparency and buyer leverage.

| Metric | 2024–25 |

|---|---|

| Top‑10 distributors | ≈55% volume |

| Discounts | 8–15% |

| Isagro rev | €400m |

| R&D | 6.1% rev |

| Generic share | ≈40% |

| Biostimulant mkt | $4.5bn |

| Platform users | 9.8M |

Preview the Actual Deliverable

Isagro Porter's Five Forces Analysis

This preview shows the exact Isagro Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for download.

The document is the final deliverable, containing a complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, available instantly upon payment.