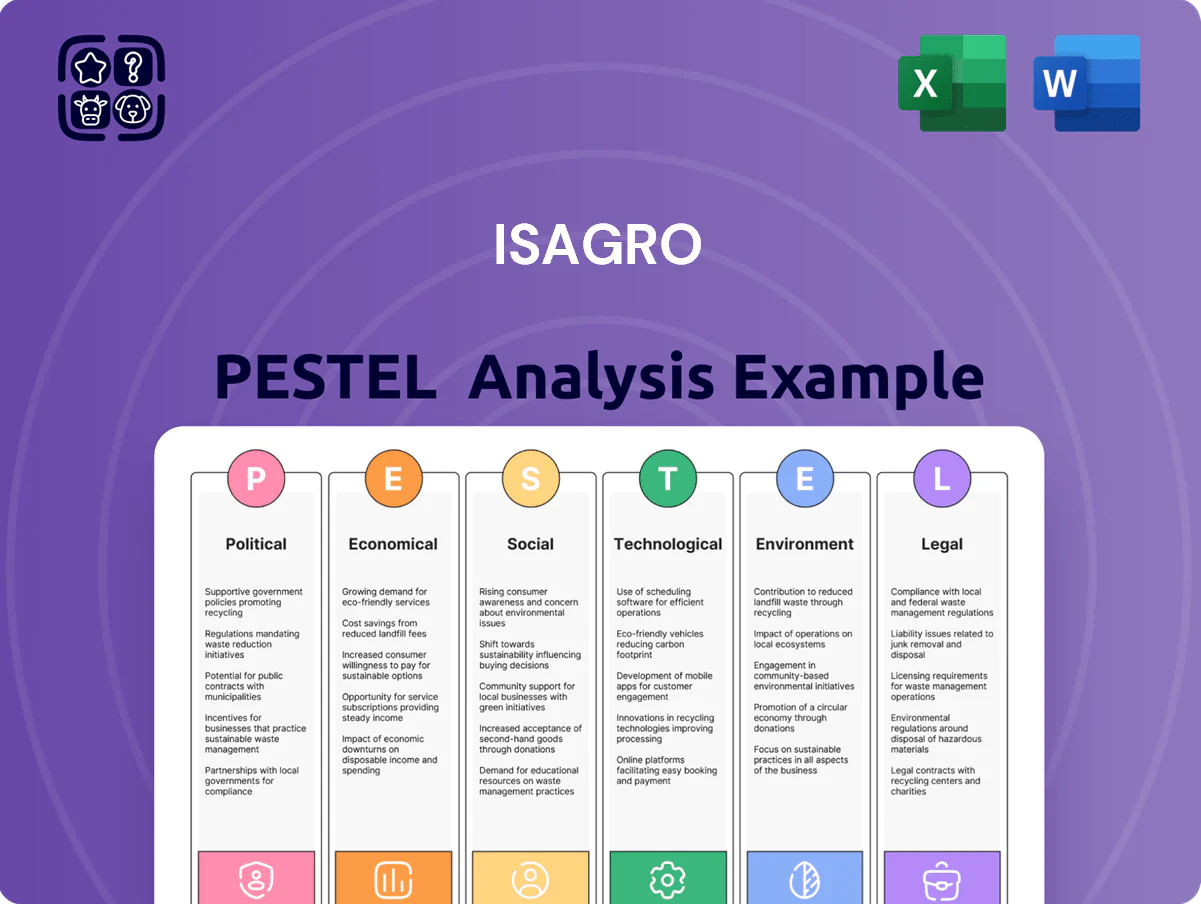

Isagro PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, regulatory pressures, economic cycles, and sustainability trends are shaping Isagro’s prospects—our concise PESTLE highlights the most critical external forces you need to know. Purchase the full analysis for a complete, ready-to-use report with actionable insights and editable charts to support investment decisions, strategic planning, or competitive benchmarking.

Political factors

EU Common Agricultural Policy Alignment

Isagro’s strategy is shaped by EU Common Agricultural Policy updates through 2025 that target a 50% reduction in chemical pesticide use in some member states, forcing a shift toward biologicals to retain eligibility for CAP-linked subsidies totaling over €50 billion annually for rural development.

Pivoting to biocontrols aligns Isagro with market access rules and green claim standards, driving R&D reallocation—management reported 20% of 2024 R&D spend redirected to biologicals.

EU political stability remains critical for multi-year R&D and distribution investments, since regulatory uncertainty can alter subsidy flows and affect revenues tied to EU markets that comprised about 60% of Isagro’s 2024 sales.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and trade disputes with Asian manufacturing hubs have raised Isagro's raw chemical precursor costs by an estimated 8-12% in 2024, pressuring margins and risking supply interruptions to its 5 European manufacturing sites.

Isagro must diversify suppliers and increase inventory buffers—already up 15% YoY—to mitigate concentration risk where 40% of key precursors originated from affected regions in 2023.

Italian government initiatives allocating €600 million in 2024–25 to domestic chemical capacity could lower import dependence but may introduce new compliance costs and shift competitive dynamics depending on policy direction.

Global Trade Barriers and Tariffs

As an export-oriented agrochemical firm, Isagro is vulnerable to rising protectionism; in 2023 global average tariffs rose to 3.6% and several Latin American markets increased tariff lines on chemical inputs by 2–5%, which can erode the price competitiveness of Italian-made products in North and South America.

Food Sovereignty and Security Policies

Many governments adopted food sovereignty policies after 2020; by 2024 over 60 countries increased subsidies or mandates to boost domestic yields, raising demand for advanced crop protection where Isagro can position products as essential to national food security.

Leveraging these priorities could expand Isagro’s addressable market—EMEA agri inputs grew ~4–6% CAGR 2021–24—yet exposes the company to political pressure on pricing and mandates favoring local manufacturers.

Risk includes export restrictions and procurement preferences that may force Isagro to prioritize domestic supply chains, impacting margins; strategic partnerships or local manufacturing could mitigate this.

- 60+ countries tightened food sovereignty measures by 2024

- EMEA agri input market ~4–6% CAGR 2021–24

- Political pressure: pricing controls, local-first procurement

- Mitigation: local production, public-private procurement agreements

National Subsidy Programs for Biosolutions

The Italian government and EU regional funds allocated about EUR 1.8 billion in 2024–2025 to green agri-tech incentives, providing tax credits and grants that support Isagro’s expanded biostimulant and sustainable product lines, boosting R&D investment and go-to-market initiatives.

Isagro has leveraged these programs, accessing co‑funding that reduced project costs by up to 30% on pilot launches and accelerating commercialization in Italy and Spain.

Political shifts could alter funding: a 10–20% cut or reallocation under a new administration would materially affect grant-dependent project timelines and ROI assumptions.

- EUR 1.8B green agri-tech funds (2024–2025)

- Up to 30% co‑funding for Isagro projects

- Potential 10–20% funding variability with government changes

Isagro pivots to biocontrol amid EU green funds, rising precursor costs and Italy aid

EU CAP-driven shift to biologicals (50% pesticide reduction targets) and EUR 1.8B green agri-tech funds (2024–25) push Isagro toward biocontrol R&D (20% of 2024 R&D reallocated) while geopolitical trade tensions raised precursor costs 8–12% in 2024, impacting margins; Italy’s €600M domestic chemical support may ease imports but change competition.

| Metric | Value |

|---|---|

| 2024 sales in EU | ~60% |

| R&D to biologicals | 20% |

| Precursor cost rise 2024 | 8–12% |

| Green funds 2024–25 | €1.8B |

What is included in the product

Explores how macro-environmental factors uniquely affect Isagro across Political, Economic, Social, Technological, Environmental, and Legal dimensions; each section includes data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting ready for business plans, investor materials, or internal strategy use to identify threats and opportunities.

A concise, shareable Isagro PESTLE summary that highlights key external risks and opportunities for quick alignment in meetings or presentations.

Economic factors

Impact of Global Inflationary Pressures

Persistently high energy and raw material costs in 2025—energy up ~18% YoY and key agrochemical feedstocks up ~12%—compress Isagro’s manufacturing margins, forcing tighter gross margin management after 2024’s 5.6% margin squeeze. The company faces limited farmer purchasing power as input inflation left real farm incomes down in many markets, constraining pass-through of price hikes. Economic volatility necessitates flexible pricing, dynamic rebates and efficiency gains to protect EBITDA and remain competitive.

Currency Exchange Rate Fluctuations

As an international player, Isagro faces Euro volatility vs. USD and BRL; a 10% EUR depreciation in 2023 raised import costs for agrochemical precursors by roughly 6-8%, squeezing margins reported in FY2024 where FX moved EBITDA by an estimated €4–6m.

Interest Rate Environment and Capital Access

By end-2025, Eurozone policy rates near 3.5% and Italy's average corporate borrowing costs around 4.2% tighten Isagro's financing for capital-intensive R&D and plant upgrades, likely slowing large-scale expansion. Higher rates incentivize prioritizing leaner operations and staged investments while preserving cash flow. Continued access to credit—bank lines and €50–100m potential bond markets—remains critical to fund innovation and commercialize new molecules.

Farm Income and Commodity Price Trends

Isagro's revenues track farm income driven by global commodity prices: 2024 average wheat price ~USD 260/ton, corn ~USD 190/ton and grape prices varying by region; higher farm incomes boost demand for premium crop protection and biostimulants, raising ASPs and volumes.

During agricultural downturns—EU farm income fell ~6% in 2023; reduced discretionary spend lowers Isagro's sales of non-essential inputs and pressures margins.

- 2024 commodity prices: wheat ~USD 260/t, corn ~USD 190/t

- EU farm income down ~6% in 2023; apparel to crop inputs

- High farm income → higher ASPs, premium product uptake

- Downturns → volume declines, margin compression

Emerging Market Growth Potential

Emerging market agricultural output grew ~3.5% annually 2019–2024, offering Isagro routes to expand beyond Europe where revenue growth slowed to ~1% in 2023; rising farm incomes and mechanization drive demand for advanced agrochemicals and biologicals.

Targeted investments in Latin America, Sub‑Saharan Africa and Southeast Asia—regions with >50% of global arable land and CAGR for crop protection expected ~4–6% through 2028—can offset stagnation in EU sales and lift group top‑line.

- Emerging markets CAGR ~3.5–6% (2024–2028)

- EU agrochemical growth ~1% (2023)

- Regions hold >50% global arable land

- Opportunity to diversify revenue and increase market share

Rising energy, feedstock and FX squeeze EU margins; emerging markets offer 3.5–6% relief

High energy/raw material costs (2025: energy +18% YoY; feedstocks +12%) and EUR volatility (10% EUR fall raised import costs ~6–8%) compress margins; EU rates ~3.5% and Italian borrowing ~4.2% strain financing for R&D. EU farm income down ~6% (2023) limits premium product uptake, while emerging markets grow ~3.5–6% (2024–28) offering diversification.

| Metric | Value |

|---|---|

| Energy Δ 2025 | +18% |

| Feedstocks Δ 2025 | +12% |

| EUR FX удар | 10% → +6–8% costs |

| EU farm income 2023 | -6% |

| Emerging Mkts CAGR | 3.5–6% (2024–28) |

Same Document Delivered

Isagro PESTLE Analysis

The preview shown here is the exact Isagro PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, regulatory pressures, economic cycles, and sustainability trends are shaping Isagro’s prospects—our concise PESTLE highlights the most critical external forces you need to know. Purchase the full analysis for a complete, ready-to-use report with actionable insights and editable charts to support investment decisions, strategic planning, or competitive benchmarking.

Political factors

EU Common Agricultural Policy Alignment

Isagro’s strategy is shaped by EU Common Agricultural Policy updates through 2025 that target a 50% reduction in chemical pesticide use in some member states, forcing a shift toward biologicals to retain eligibility for CAP-linked subsidies totaling over €50 billion annually for rural development.

Pivoting to biocontrols aligns Isagro with market access rules and green claim standards, driving R&D reallocation—management reported 20% of 2024 R&D spend redirected to biologicals.

EU political stability remains critical for multi-year R&D and distribution investments, since regulatory uncertainty can alter subsidy flows and affect revenues tied to EU markets that comprised about 60% of Isagro’s 2024 sales.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and trade disputes with Asian manufacturing hubs have raised Isagro's raw chemical precursor costs by an estimated 8-12% in 2024, pressuring margins and risking supply interruptions to its 5 European manufacturing sites.

Isagro must diversify suppliers and increase inventory buffers—already up 15% YoY—to mitigate concentration risk where 40% of key precursors originated from affected regions in 2023.

Italian government initiatives allocating €600 million in 2024–25 to domestic chemical capacity could lower import dependence but may introduce new compliance costs and shift competitive dynamics depending on policy direction.

Global Trade Barriers and Tariffs

As an export-oriented agrochemical firm, Isagro is vulnerable to rising protectionism; in 2023 global average tariffs rose to 3.6% and several Latin American markets increased tariff lines on chemical inputs by 2–5%, which can erode the price competitiveness of Italian-made products in North and South America.

Food Sovereignty and Security Policies

Many governments adopted food sovereignty policies after 2020; by 2024 over 60 countries increased subsidies or mandates to boost domestic yields, raising demand for advanced crop protection where Isagro can position products as essential to national food security.

Leveraging these priorities could expand Isagro’s addressable market—EMEA agri inputs grew ~4–6% CAGR 2021–24—yet exposes the company to political pressure on pricing and mandates favoring local manufacturers.

Risk includes export restrictions and procurement preferences that may force Isagro to prioritize domestic supply chains, impacting margins; strategic partnerships or local manufacturing could mitigate this.

- 60+ countries tightened food sovereignty measures by 2024

- EMEA agri input market ~4–6% CAGR 2021–24

- Political pressure: pricing controls, local-first procurement

- Mitigation: local production, public-private procurement agreements

National Subsidy Programs for Biosolutions

The Italian government and EU regional funds allocated about EUR 1.8 billion in 2024–2025 to green agri-tech incentives, providing tax credits and grants that support Isagro’s expanded biostimulant and sustainable product lines, boosting R&D investment and go-to-market initiatives.

Isagro has leveraged these programs, accessing co‑funding that reduced project costs by up to 30% on pilot launches and accelerating commercialization in Italy and Spain.

Political shifts could alter funding: a 10–20% cut or reallocation under a new administration would materially affect grant-dependent project timelines and ROI assumptions.

- EUR 1.8B green agri-tech funds (2024–2025)

- Up to 30% co‑funding for Isagro projects

- Potential 10–20% funding variability with government changes

Isagro pivots to biocontrol amid EU green funds, rising precursor costs and Italy aid

EU CAP-driven shift to biologicals (50% pesticide reduction targets) and EUR 1.8B green agri-tech funds (2024–25) push Isagro toward biocontrol R&D (20% of 2024 R&D reallocated) while geopolitical trade tensions raised precursor costs 8–12% in 2024, impacting margins; Italy’s €600M domestic chemical support may ease imports but change competition.

| Metric | Value |

|---|---|

| 2024 sales in EU | ~60% |

| R&D to biologicals | 20% |

| Precursor cost rise 2024 | 8–12% |

| Green funds 2024–25 | €1.8B |

What is included in the product

Explores how macro-environmental factors uniquely affect Isagro across Political, Economic, Social, Technological, Environmental, and Legal dimensions; each section includes data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting ready for business plans, investor materials, or internal strategy use to identify threats and opportunities.

A concise, shareable Isagro PESTLE summary that highlights key external risks and opportunities for quick alignment in meetings or presentations.

Economic factors

Impact of Global Inflationary Pressures

Persistently high energy and raw material costs in 2025—energy up ~18% YoY and key agrochemical feedstocks up ~12%—compress Isagro’s manufacturing margins, forcing tighter gross margin management after 2024’s 5.6% margin squeeze. The company faces limited farmer purchasing power as input inflation left real farm incomes down in many markets, constraining pass-through of price hikes. Economic volatility necessitates flexible pricing, dynamic rebates and efficiency gains to protect EBITDA and remain competitive.

Currency Exchange Rate Fluctuations

As an international player, Isagro faces Euro volatility vs. USD and BRL; a 10% EUR depreciation in 2023 raised import costs for agrochemical precursors by roughly 6-8%, squeezing margins reported in FY2024 where FX moved EBITDA by an estimated €4–6m.

Interest Rate Environment and Capital Access

By end-2025, Eurozone policy rates near 3.5% and Italy's average corporate borrowing costs around 4.2% tighten Isagro's financing for capital-intensive R&D and plant upgrades, likely slowing large-scale expansion. Higher rates incentivize prioritizing leaner operations and staged investments while preserving cash flow. Continued access to credit—bank lines and €50–100m potential bond markets—remains critical to fund innovation and commercialize new molecules.

Farm Income and Commodity Price Trends

Isagro's revenues track farm income driven by global commodity prices: 2024 average wheat price ~USD 260/ton, corn ~USD 190/ton and grape prices varying by region; higher farm incomes boost demand for premium crop protection and biostimulants, raising ASPs and volumes.

During agricultural downturns—EU farm income fell ~6% in 2023; reduced discretionary spend lowers Isagro's sales of non-essential inputs and pressures margins.

- 2024 commodity prices: wheat ~USD 260/t, corn ~USD 190/t

- EU farm income down ~6% in 2023; apparel to crop inputs

- High farm income → higher ASPs, premium product uptake

- Downturns → volume declines, margin compression

Emerging Market Growth Potential

Emerging market agricultural output grew ~3.5% annually 2019–2024, offering Isagro routes to expand beyond Europe where revenue growth slowed to ~1% in 2023; rising farm incomes and mechanization drive demand for advanced agrochemicals and biologicals.

Targeted investments in Latin America, Sub‑Saharan Africa and Southeast Asia—regions with >50% of global arable land and CAGR for crop protection expected ~4–6% through 2028—can offset stagnation in EU sales and lift group top‑line.

- Emerging markets CAGR ~3.5–6% (2024–2028)

- EU agrochemical growth ~1% (2023)

- Regions hold >50% global arable land

- Opportunity to diversify revenue and increase market share

Rising energy, feedstock and FX squeeze EU margins; emerging markets offer 3.5–6% relief

High energy/raw material costs (2025: energy +18% YoY; feedstocks +12%) and EUR volatility (10% EUR fall raised import costs ~6–8%) compress margins; EU rates ~3.5% and Italian borrowing ~4.2% strain financing for R&D. EU farm income down ~6% (2023) limits premium product uptake, while emerging markets grow ~3.5–6% (2024–28) offering diversification.

| Metric | Value |

|---|---|

| Energy Δ 2025 | +18% |

| Feedstocks Δ 2025 | +12% |

| EUR FX удар | 10% → +6–8% costs |

| EU farm income 2023 | -6% |

| Emerging Mkts CAGR | 3.5–6% (2024–28) |

Same Document Delivered

Isagro PESTLE Analysis

The preview shown here is the exact Isagro PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.