Isbank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

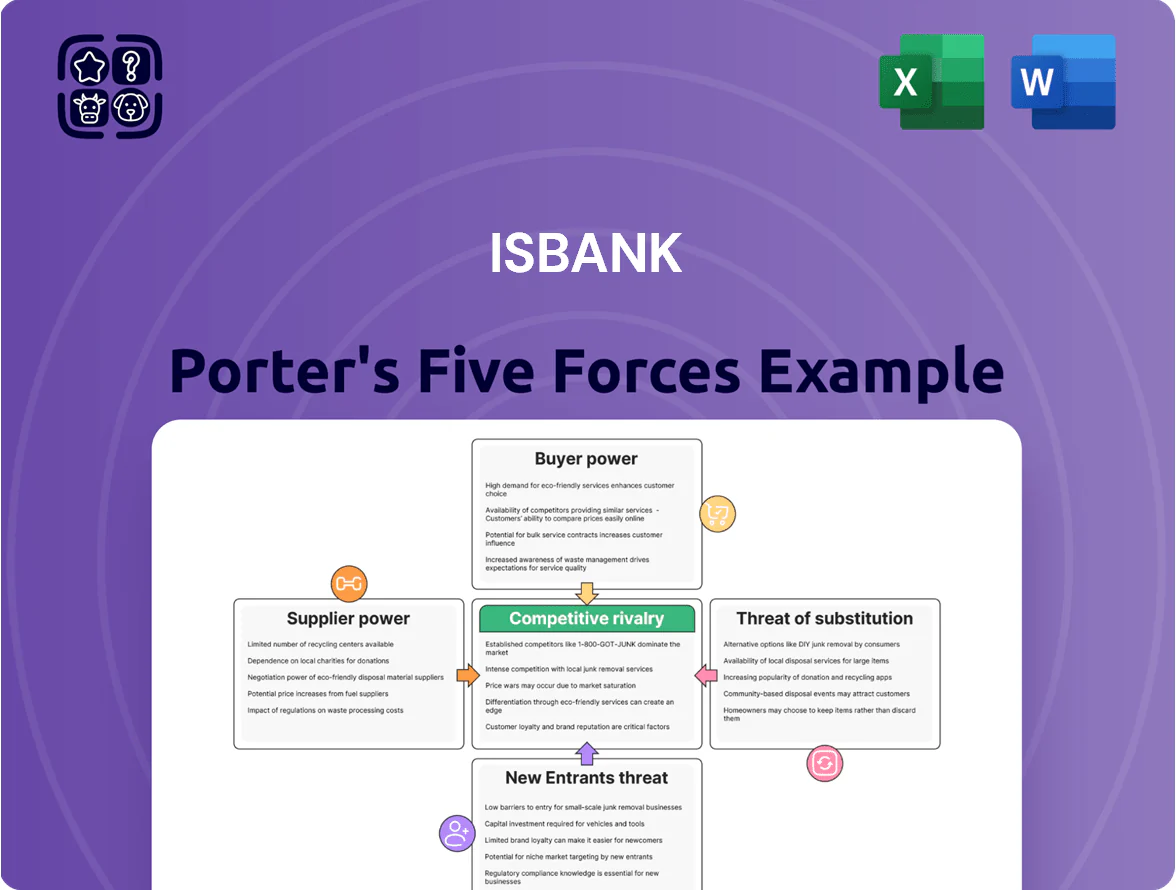

Isbank faces moderate buyer power, concentrated regulation, and rising fintech substitution that together reshape its competitive landscape; supplier leverage and entry barriers remain mixed due to scale advantages but evolving digital threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Isbank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank Policy and Liquidity

The Central Bank of the Republic of Türkiye (CBRT) is the primary supplier of capital and regulatory liquidity, so its policy sets Isbank’s funding cost via the policy rate (24% in Dec 2025) and reserve requirement ratios (8–12% depending on deposit type). Tight 2025 monetary policy compressed net interest margins across Turkish banks, leaving CBRT with outsized leverage over Isbank’s profitability and loan growth.

Global Capital Markets Access

Isbank depends on international lenders for syndicated loans and securitizations to fund FX operations; in 2024 foreign currency short-term funding comprised about 18% of its liabilities. Lenders' bargaining power tracks Türkiye’s sovereign rating (as of Dec 2025 Moody’s B1/S&P BB‑) and Isbank’s standalone risk metrics—higher CDS spreads (Turkey 5y CDS ~580 bps in Dec 2025) raise costs. Rising global rates or EM outflows push up margins and shorten tenor, increasing funding expense and rollover risk.

Technology and Infrastructure Providers

Isbank relies on specialized global vendors for core banking, cloud and cyber defenses; switching costs are very high—enterprise core migrations can exceed $200m and take 18–36 months—giving suppliers like Microsoft, Oracle and IBM strong leverage.

Isbank boosts resilience with internal R&D and a 2024 IT spend near 1.1bn TRY, but still depends on external hardware, firmware and security patches, keeping supplier power materially high.

Human Capital and Specialized Talent

Limited supply of senior fintech, data-science, and risk-management talent in Turkey raises suppliers’ bargaining power; a 2024 LinkedIn report showed 18% year-on-year shortage in data roles in Türkiye.

Competition from local banks, startups, and remote global employers paying 20–40% higher total comp boosts turnover risk.

Isbank needs market-leading pay, equity, and training—else brain drain to global tech firms will accelerate.

- 2024: 18% data-role shortage in Türkiye

- Global remote pay premium: 20–40%

- Retention levers: pay, equity, upskilling

Deposit Base Fragmentation

Retail and corporate depositors supply Isbank with raw capital, but the base is split across millions, so individual bargaining power is negligible.

Still, Turkey's 2025 annual inflation near 48% and lira deposits falling 7% YoY (Q4 2024) pushed banks to raise rates and promote FX products, showing collective depositor moves can force pricing shifts.

- Millions of depositors → low individual leverage

- 2025 inflation ~48% drives rate hikes

- Q4 2024 lira deposits down 7% YoY

- Collective shifts to FX/high-yield products raise funding costs

High supplier power: soaring funding costs, costly core migration & IT/talent shortages

Suppliers exert high bargaining power: CBRT policy (policy rate 24% Dec 2025; RR 8–12%) and international lenders (FX funding ~18% liabilities in 2024; Turkey 5y CDS ~580bps Dec 2025) drive funding cost and tenor; core-vendor switching costs (> $200m; 18–36 months) plus 2024 IT spend 1.1bn TRY and 18% data-role shortage raise input costs and talent risk.

| Metric | Value |

|---|---|

| Policy rate (Dec 2025) | 24% |

| FX funding share (2024) | 18% |

| Turkey 5y CDS (Dec 2025) | ~580bps |

| Core migration cost/time | >$200m / 18–36m |

| IT spend (2024) | 1.1bn TRY |

| Data-role shortage (2024) | 18% |

What is included in the product

Tailored Porter's Five Forces analysis for Isbank that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic and investment decisions.

One-sheet Isbank Porter's Five Forces summary—quickly spot competitive pressures and inform strategic or investment decisions.

Customers Bargaining Power

High Price Sensitivity in Lending

Retail and SME customers in Türkiye show high price sensitivity to interest rate spreads for mortgages and commercial loans, with online comparison sites reporting average mortgage shopping times under 10 days in 2024 and churn rising 12% year-on-year. With over 60% of loan inquiries starting digitally and rival banks offering rates as much as 150–200 bps lower, customers easily switch for better terms. This forces Türkiye Isbank (Isbank) to keep lending rates competitive to defend its ~9% share of total bank loans and prevent margin erosion.

Low Switching Costs for Retail Banking

Digital banking and Türkiye’s Open Banking rollout (PSD2-like updates 2023–2024) cut switching costs: 62% of Turkish retail customers used mobile apps to move funds in 2024, and fintech account aggregation grew 45% YoY, letting users manage multiple accounts and shift deposits quickly.

This low-friction environment raises pressure on İşbank to invest in UX and loyalty: İşbank’s mobile active base (9.8M in 2024) must see better rewards and service to prevent churn, given industry average annual retail deposit switching near 8–10%.

Corporate Client Negotiation Leverage

Large conglomerates supply over 30% of İşbank’s corporate deposit and loan volumes and routinely benchmark offers across 3–5 domestic and international banks, giving them strong negotiation leverage.

These clients win bespoke rates—often 25–75 bps below standard corporate pricing—plus reduced FX and transaction fees by contracting scale and multi-product deals.

To retain them, İşbank bundles trade finance, cash management and advisory; in 2024 trade finance revenue rose 12%, showing the importance of value-added services.

Impact of Digital Comparison Tools

- 42% of retail users used comparison sites in 2024

- Isbank must match market APRs and card rewards

- Transparency reduces information asymmetry

Regulatory Consumer Protection

Turkish banking rules cap fees for basic transactions and account maintenance, limiting ISBANK's (Türkiye İş Bankası A.Ş.) ability to extract customer value; the Banking Regulation and Supervision Agency (BDDK) and Consumer Protection Law enforce these limits.

This regulatory ceiling functions like customer bargaining power: banks reported average retail account fees falling 8% y/y in 2024, and fee income made up ~6% of sector revenue in 2024, constraining price flexibility.

- BDDK/Consumer Law cap fees

- Fee income ≈6% of sector revenue (2024)

- Retail fees down 8% y/y (2024)

İşbank under customer pressure: digital switching, quick mortgages & squeezed fees

Customers hold strong bargaining power vs İşbank: digital comparison use (42% in 2024), short mortgage shopping (<10 days) and 60% digital loan starts enable rapid switching; large corporates (30%+ volumes) secure 25–75 bps concessions; regulation caps fees (fee income ~6% sector revenue, retail fees -8% y/y 2024), forcing competitive pricing and increased UX/loyalty spend.

| Metric | 2024 |

|---|---|

| Comparison site use | 42% |

| Mortgage shopping time | <10 days |

| Digital loan starts | 60% |

| Corp volume share | 30%+ |

| Fee income | ~6% rev |

Preview the Actual Deliverable

Isbank Porter's Five Forces Analysis

This preview shows the exact İŞBANK Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is complete, professionally formatted, and ready for download.

You're looking at the actual document: instant access to this same, fully written analysis is granted upon payment, suitable for presentation, research, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Isbank faces moderate buyer power, concentrated regulation, and rising fintech substitution that together reshape its competitive landscape; supplier leverage and entry barriers remain mixed due to scale advantages but evolving digital threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Isbank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank Policy and Liquidity

The Central Bank of the Republic of Türkiye (CBRT) is the primary supplier of capital and regulatory liquidity, so its policy sets Isbank’s funding cost via the policy rate (24% in Dec 2025) and reserve requirement ratios (8–12% depending on deposit type). Tight 2025 monetary policy compressed net interest margins across Turkish banks, leaving CBRT with outsized leverage over Isbank’s profitability and loan growth.

Global Capital Markets Access

Isbank depends on international lenders for syndicated loans and securitizations to fund FX operations; in 2024 foreign currency short-term funding comprised about 18% of its liabilities. Lenders' bargaining power tracks Türkiye’s sovereign rating (as of Dec 2025 Moody’s B1/S&P BB‑) and Isbank’s standalone risk metrics—higher CDS spreads (Turkey 5y CDS ~580 bps in Dec 2025) raise costs. Rising global rates or EM outflows push up margins and shorten tenor, increasing funding expense and rollover risk.

Technology and Infrastructure Providers

Isbank relies on specialized global vendors for core banking, cloud and cyber defenses; switching costs are very high—enterprise core migrations can exceed $200m and take 18–36 months—giving suppliers like Microsoft, Oracle and IBM strong leverage.

Isbank boosts resilience with internal R&D and a 2024 IT spend near 1.1bn TRY, but still depends on external hardware, firmware and security patches, keeping supplier power materially high.

Human Capital and Specialized Talent

Limited supply of senior fintech, data-science, and risk-management talent in Turkey raises suppliers’ bargaining power; a 2024 LinkedIn report showed 18% year-on-year shortage in data roles in Türkiye.

Competition from local banks, startups, and remote global employers paying 20–40% higher total comp boosts turnover risk.

Isbank needs market-leading pay, equity, and training—else brain drain to global tech firms will accelerate.

- 2024: 18% data-role shortage in Türkiye

- Global remote pay premium: 20–40%

- Retention levers: pay, equity, upskilling

Deposit Base Fragmentation

Retail and corporate depositors supply Isbank with raw capital, but the base is split across millions, so individual bargaining power is negligible.

Still, Turkey's 2025 annual inflation near 48% and lira deposits falling 7% YoY (Q4 2024) pushed banks to raise rates and promote FX products, showing collective depositor moves can force pricing shifts.

- Millions of depositors → low individual leverage

- 2025 inflation ~48% drives rate hikes

- Q4 2024 lira deposits down 7% YoY

- Collective shifts to FX/high-yield products raise funding costs

High supplier power: soaring funding costs, costly core migration & IT/talent shortages

Suppliers exert high bargaining power: CBRT policy (policy rate 24% Dec 2025; RR 8–12%) and international lenders (FX funding ~18% liabilities in 2024; Turkey 5y CDS ~580bps Dec 2025) drive funding cost and tenor; core-vendor switching costs (> $200m; 18–36 months) plus 2024 IT spend 1.1bn TRY and 18% data-role shortage raise input costs and talent risk.

| Metric | Value |

|---|---|

| Policy rate (Dec 2025) | 24% |

| FX funding share (2024) | 18% |

| Turkey 5y CDS (Dec 2025) | ~580bps |

| Core migration cost/time | >$200m / 18–36m |

| IT spend (2024) | 1.1bn TRY |

| Data-role shortage (2024) | 18% |

What is included in the product

Tailored Porter's Five Forces analysis for Isbank that uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic and investment decisions.

One-sheet Isbank Porter's Five Forces summary—quickly spot competitive pressures and inform strategic or investment decisions.

Customers Bargaining Power

High Price Sensitivity in Lending

Retail and SME customers in Türkiye show high price sensitivity to interest rate spreads for mortgages and commercial loans, with online comparison sites reporting average mortgage shopping times under 10 days in 2024 and churn rising 12% year-on-year. With over 60% of loan inquiries starting digitally and rival banks offering rates as much as 150–200 bps lower, customers easily switch for better terms. This forces Türkiye Isbank (Isbank) to keep lending rates competitive to defend its ~9% share of total bank loans and prevent margin erosion.

Low Switching Costs for Retail Banking

Digital banking and Türkiye’s Open Banking rollout (PSD2-like updates 2023–2024) cut switching costs: 62% of Turkish retail customers used mobile apps to move funds in 2024, and fintech account aggregation grew 45% YoY, letting users manage multiple accounts and shift deposits quickly.

This low-friction environment raises pressure on İşbank to invest in UX and loyalty: İşbank’s mobile active base (9.8M in 2024) must see better rewards and service to prevent churn, given industry average annual retail deposit switching near 8–10%.

Corporate Client Negotiation Leverage

Large conglomerates supply over 30% of İşbank’s corporate deposit and loan volumes and routinely benchmark offers across 3–5 domestic and international banks, giving them strong negotiation leverage.

These clients win bespoke rates—often 25–75 bps below standard corporate pricing—plus reduced FX and transaction fees by contracting scale and multi-product deals.

To retain them, İşbank bundles trade finance, cash management and advisory; in 2024 trade finance revenue rose 12%, showing the importance of value-added services.

Impact of Digital Comparison Tools

- 42% of retail users used comparison sites in 2024

- Isbank must match market APRs and card rewards

- Transparency reduces information asymmetry

Regulatory Consumer Protection

Turkish banking rules cap fees for basic transactions and account maintenance, limiting ISBANK's (Türkiye İş Bankası A.Ş.) ability to extract customer value; the Banking Regulation and Supervision Agency (BDDK) and Consumer Protection Law enforce these limits.

This regulatory ceiling functions like customer bargaining power: banks reported average retail account fees falling 8% y/y in 2024, and fee income made up ~6% of sector revenue in 2024, constraining price flexibility.

- BDDK/Consumer Law cap fees

- Fee income ≈6% of sector revenue (2024)

- Retail fees down 8% y/y (2024)

İşbank under customer pressure: digital switching, quick mortgages & squeezed fees

Customers hold strong bargaining power vs İşbank: digital comparison use (42% in 2024), short mortgage shopping (<10 days) and 60% digital loan starts enable rapid switching; large corporates (30%+ volumes) secure 25–75 bps concessions; regulation caps fees (fee income ~6% sector revenue, retail fees -8% y/y 2024), forcing competitive pricing and increased UX/loyalty spend.

| Metric | 2024 |

|---|---|

| Comparison site use | 42% |

| Mortgage shopping time | <10 days |

| Digital loan starts | 60% |

| Corp volume share | 30%+ |

| Fee income | ~6% rev |

Preview the Actual Deliverable

Isbank Porter's Five Forces Analysis

This preview shows the exact İŞBANK Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is complete, professionally formatted, and ready for download.

You're looking at the actual document: instant access to this same, fully written analysis is granted upon payment, suitable for presentation, research, or strategic planning.