ISG plc PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

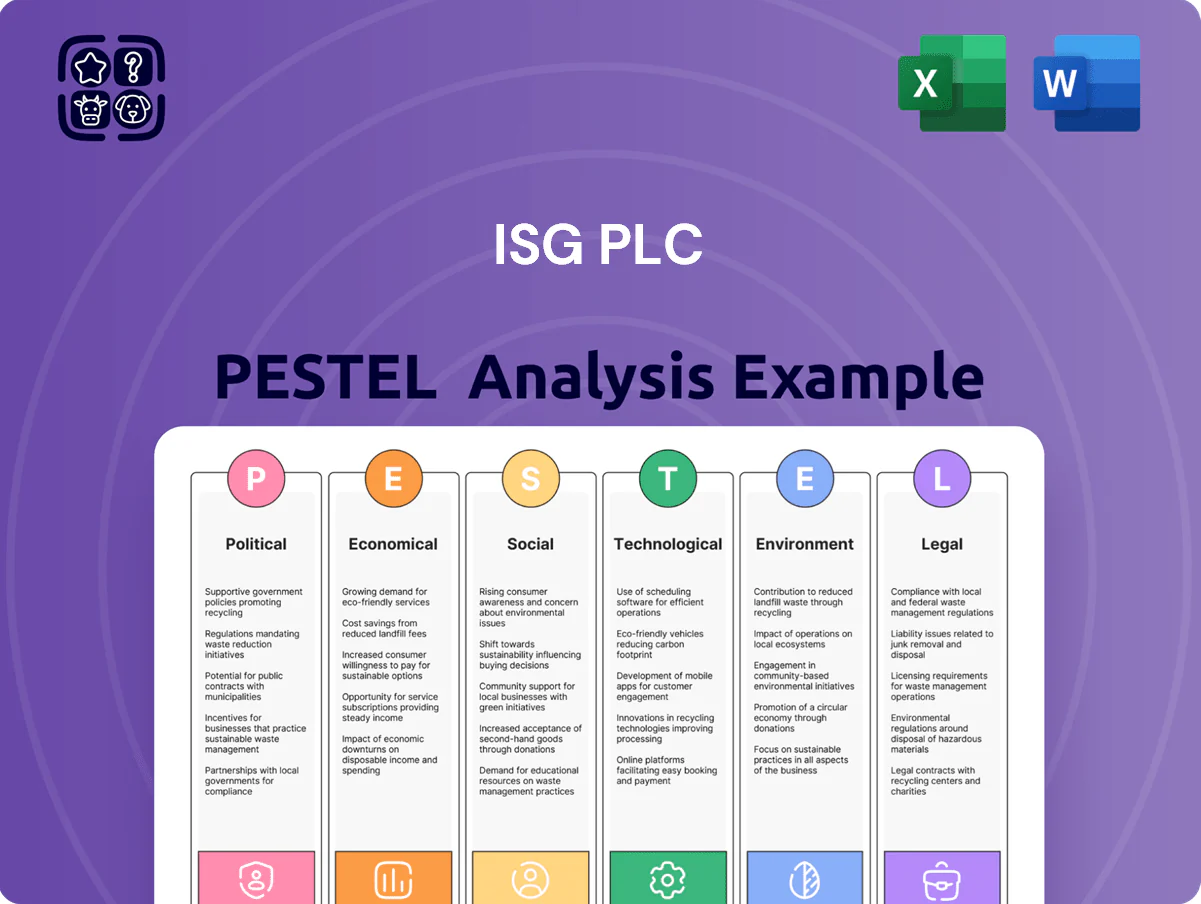

Discover how political shifts, economic cycles, and technological change are reshaping ISG plc’s prospects—our concise PESTLE highlights the external risks and opportunities you need to know; buy the full analysis to access the complete, actionable report for investment decisions, strategy sessions, or competitive benchmarking.

Political factors

Government infrastructure investment

UK and EU governments plan over 100 billion GBP/EUR in infrastructure spending through 2025 to boost growth; ISG’s revenue mix—with around 45% from public sector frameworks in education and healthcare—makes it highly sensitive to political budget allocations and policy shifts. Remaining aligned with regional development targets is critical to secure long-term pipelines amid competition for limited public contracts.

Post-Brexit trade relations

Post-Brexit trade adjustments continue to disrupt ISG plc operations: UK-EU border frictions increased average delivery times for construction materials by 12% in 2024, while visa and certification changes reduced specialist labour mobility, raising labour sourcing costs by about 7% year-on-year.

Political decisions on customs, tariffs and divergent certification standards drove input cost inflation—ISM sector materials saw a 6–9% tariff-equivalent rise impacting project margins and pushing some fit-out project lead times beyond contractual SLAs in 2025.

Managing these geopolitical shifts—including new UK-EU SPS and rules-of-origin checks implemented in 2024—is critical for ISG to control FY2025 cost structures and preserve competitiveness across its European portfolio.

Public procurement policy changes

New UK public procurement rules now weight social value up to 20% in many tenders; ISG must embed local economic impact metrics and community employment targets to remain competitive for the £12–15bn NHS capital pipeline and MoJ estates programmes.

Aligning bids with government priorities—net-zero, apprenticeships, SME supply‑chain share—boosts ISG’s chance at high-value healthcare and justice contracts; failure to show such alignment risks losing deals where social criteria decide winners.

Geopolitical supply chain stability

Global political tensions in manufacturing hubs like Taiwan, South Korea and Xinjiang have raised risk: semiconductors and specialty metals disruptions could add 6–12% to component lead times and push procurement costs up by an estimated 3–5% for engineering firms in 2024–25.

Political instability in supplier regions forces ISG plc to diversify routes and maintain buffer inventories; a 20–30% increase in dual-sourcing contracts and logistics redundancies is prudent given recent supply shocks.

Continuous monitoring of international relations is essential to protect project continuity and cost predictability—risk-adjusted contract clauses and hedging reduced project margin volatility by ~1.5 percentage points in recent industry cases.

- 6–12% longer lead times; 3–5% higher procurement costs (2024–25 estimates)

- 20–30% rise in dual-sourcing/logistics redundancies recommended

- Risk management reduced margin volatility by ~1.5 pp in comparable projects

Urban regeneration initiatives

Political emphasis on urban renewal and brownfield repurposing fuels demand for large-scale construction and refurbishment, with UK brownfield sites accounting for over 80% of development land in 2023.

Government incentives—such as the £1.3bn Levelling Up Fund (2023–24) and tax reliefs for high street conversions—create steady work for fit-out specialists like ISG.

ISG is positioned to capture state-led metropolitan revitalization projects, supporting local economic growth and recurring contract pipelines.

- UK brownfield: ~80% of development land (2023)

- Levelling Up Fund: £1.3bn (2023–24)

- Increased retrofit/fit-out demand: rising share of ISG revenue from refurbishment projects (2024)

ISG risks: 45% public revenue, higher costs/delays; social-value procures reshape bids

Political shifts (UK/EU infrastructure spending £100bn+ to 2025) make ISG highly dependent on public budgets (~45% revenue); post-Brexit trade frictions raised material delivery times ~12% and labour costs ~7% (2024); procurement rules now weight social value up to 20% affecting bid success for NHS (£12–15bn) and MoJ pipelines; supply‑chain geopolitical risks add 3–5% procurement cost and warrant 20–30% more dual‑sourcing.

| Metric | Value (2023–25) |

|---|---|

| Public spend pipeline | £100bn+ |

| ISG public revenue | ~45% |

| Material delays | +12% |

| Labour cost rise | +7% |

| Procurement social value | up to 20% |

| Procurement cost risk | +3–5% |

| Dual‑sourcing uplift recommended | +20–30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ISG plc across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored to the construction and professional services sector.

Condensed ISG plc PESTLE insights tailored for swift reference in meetings or presentations, highlighting external risks and opportunities that relieve strategic planning friction.

Economic factors

Interest rate fluctuations

The cost of borrowing remains critical for ISG plc as UK base rates rose to 5.25% in 2024 before stabilizing, influencing private developers and corporate clients funding large-scale construction and fit-out schemes.

While rates showed signs of stabilizing by late 2025, volatility persists and directly affects feasibility and IRR thresholds for capital-intensive projects, often shifting NPV outcomes by several percentage points.

ISG must monitor Bank of England policy and global central bank moves to anticipate demand swings in commercial real estate and accelerating data center builds, where financing needs can exceed hundreds of millions.

Construction material inflation

Labor market shortages

Persistent shortages of skilled tradespeople and project managers have pushed ISG plc’s direct labor costs up; UK construction pay growth ran at 6.1% year‑on‑year in 2024, squeezing margins on lower‑margin projects.

Fierce sector competition raised recruitment and retention spend—ISG reported rising staff costs representing about 8–10% of operating expenses in recent 2024/25 filings—driving investment in training and benefits to secure expertise.

These labor shortages complicate scheduling and increase overheads, with temporary staffing and subcontractor premiums adding an estimated 3–5% to project budgets in 2024, pressuring profitability on fixed‑price contracts.

Commercial real estate demand

The shift to hybrid work cut global office occupancy to about 55–65% in 2024, shrinking demand for large floorplates and boosting spend on tech-enabled fit-outs; corporate average fit-out budgets rose ~8–12% as firms prioritized quality over square footage.

ISG must pivot to specialized, sustainable interiors—demand for green-certified refurbishments grew 18% in 2024—and offer modular, tech-integrated solutions to capture this evolving market.

- Office occupancy 55–65% (2024)

- Fit-out budgets +8–12% (2024)

- Green refurb demand +18% (2024)

Currency exchange volatility

As a multinational, ISG plc faces currency exchange volatility that can swing reported EBITDA by several percent; for example, a 5% GBP weakness against the euro in 2024 would have amplified project revenues in continental Europe while squeezing UK-costed margins.

Managing multi-currency revenue and costs requires hedging—forward contracts and natural hedges—to guard against sudden devaluations in key markets; ISG’s 2024 disclosure noted foreign-exchange translation impacted profit before tax variability by mid-single digits.

Economic instability in major regions creates financial reporting challenges that can reduce consolidated returns and increase balance sheet FX exposure, elevating the need for dynamic treasury policies and scenario stress-testing.

- FX swings can move EBITDA by mid-single digits (2024 observed)

- Hedging and natural hedges used to mitigate translation risk

- Regional instability raises reporting volatility and balance-sheet exposure

Rising rates, inflation squeeze margins; ISG saves £25–30m as fit‑outs and green refurb surge

Rising UK rates (BoE 5.25% 2024) and material inflation (steel +18% vs 2019; timber +12% y/y H2 2025) squeezed margins; ISG secured c.£25–30m procurement savings in 2024. Labour cost growth ~6.1% (2024) and staff costs ~8–10% of Opex raised project overheads. Office occupancy 55–65% (2024) shifted demand to higher‑value fit-outs (+8–12%) and green refurb (+18%). FX volatility moved EBITDA by mid‑single digits (2024).

| Metric | Value |

|---|---|

| BoE rate (2024) | 5.25% |

| Steel vs 2019 | +18% |

| Lumber y/y H2 2025 | +12% |

| Labour pay growth (2024) | 6.1% |

| Procurement savings (2024) | £25–30m |

Full Version Awaits

ISG plc PESTLE Analysis

The preview shown here is the exact ISG plc PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological change are reshaping ISG plc’s prospects—our concise PESTLE highlights the external risks and opportunities you need to know; buy the full analysis to access the complete, actionable report for investment decisions, strategy sessions, or competitive benchmarking.

Political factors

Government infrastructure investment

UK and EU governments plan over 100 billion GBP/EUR in infrastructure spending through 2025 to boost growth; ISG’s revenue mix—with around 45% from public sector frameworks in education and healthcare—makes it highly sensitive to political budget allocations and policy shifts. Remaining aligned with regional development targets is critical to secure long-term pipelines amid competition for limited public contracts.

Post-Brexit trade relations

Post-Brexit trade adjustments continue to disrupt ISG plc operations: UK-EU border frictions increased average delivery times for construction materials by 12% in 2024, while visa and certification changes reduced specialist labour mobility, raising labour sourcing costs by about 7% year-on-year.

Political decisions on customs, tariffs and divergent certification standards drove input cost inflation—ISM sector materials saw a 6–9% tariff-equivalent rise impacting project margins and pushing some fit-out project lead times beyond contractual SLAs in 2025.

Managing these geopolitical shifts—including new UK-EU SPS and rules-of-origin checks implemented in 2024—is critical for ISG to control FY2025 cost structures and preserve competitiveness across its European portfolio.

Public procurement policy changes

New UK public procurement rules now weight social value up to 20% in many tenders; ISG must embed local economic impact metrics and community employment targets to remain competitive for the £12–15bn NHS capital pipeline and MoJ estates programmes.

Aligning bids with government priorities—net-zero, apprenticeships, SME supply‑chain share—boosts ISG’s chance at high-value healthcare and justice contracts; failure to show such alignment risks losing deals where social criteria decide winners.

Geopolitical supply chain stability

Global political tensions in manufacturing hubs like Taiwan, South Korea and Xinjiang have raised risk: semiconductors and specialty metals disruptions could add 6–12% to component lead times and push procurement costs up by an estimated 3–5% for engineering firms in 2024–25.

Political instability in supplier regions forces ISG plc to diversify routes and maintain buffer inventories; a 20–30% increase in dual-sourcing contracts and logistics redundancies is prudent given recent supply shocks.

Continuous monitoring of international relations is essential to protect project continuity and cost predictability—risk-adjusted contract clauses and hedging reduced project margin volatility by ~1.5 percentage points in recent industry cases.

- 6–12% longer lead times; 3–5% higher procurement costs (2024–25 estimates)

- 20–30% rise in dual-sourcing/logistics redundancies recommended

- Risk management reduced margin volatility by ~1.5 pp in comparable projects

Urban regeneration initiatives

Political emphasis on urban renewal and brownfield repurposing fuels demand for large-scale construction and refurbishment, with UK brownfield sites accounting for over 80% of development land in 2023.

Government incentives—such as the £1.3bn Levelling Up Fund (2023–24) and tax reliefs for high street conversions—create steady work for fit-out specialists like ISG.

ISG is positioned to capture state-led metropolitan revitalization projects, supporting local economic growth and recurring contract pipelines.

- UK brownfield: ~80% of development land (2023)

- Levelling Up Fund: £1.3bn (2023–24)

- Increased retrofit/fit-out demand: rising share of ISG revenue from refurbishment projects (2024)

ISG risks: 45% public revenue, higher costs/delays; social-value procures reshape bids

Political shifts (UK/EU infrastructure spending £100bn+ to 2025) make ISG highly dependent on public budgets (~45% revenue); post-Brexit trade frictions raised material delivery times ~12% and labour costs ~7% (2024); procurement rules now weight social value up to 20% affecting bid success for NHS (£12–15bn) and MoJ pipelines; supply‑chain geopolitical risks add 3–5% procurement cost and warrant 20–30% more dual‑sourcing.

| Metric | Value (2023–25) |

|---|---|

| Public spend pipeline | £100bn+ |

| ISG public revenue | ~45% |

| Material delays | +12% |

| Labour cost rise | +7% |

| Procurement social value | up to 20% |

| Procurement cost risk | +3–5% |

| Dual‑sourcing uplift recommended | +20–30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ISG plc across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored to the construction and professional services sector.

Condensed ISG plc PESTLE insights tailored for swift reference in meetings or presentations, highlighting external risks and opportunities that relieve strategic planning friction.

Economic factors

Interest rate fluctuations

The cost of borrowing remains critical for ISG plc as UK base rates rose to 5.25% in 2024 before stabilizing, influencing private developers and corporate clients funding large-scale construction and fit-out schemes.

While rates showed signs of stabilizing by late 2025, volatility persists and directly affects feasibility and IRR thresholds for capital-intensive projects, often shifting NPV outcomes by several percentage points.

ISG must monitor Bank of England policy and global central bank moves to anticipate demand swings in commercial real estate and accelerating data center builds, where financing needs can exceed hundreds of millions.

Construction material inflation

Labor market shortages

Persistent shortages of skilled tradespeople and project managers have pushed ISG plc’s direct labor costs up; UK construction pay growth ran at 6.1% year‑on‑year in 2024, squeezing margins on lower‑margin projects.

Fierce sector competition raised recruitment and retention spend—ISG reported rising staff costs representing about 8–10% of operating expenses in recent 2024/25 filings—driving investment in training and benefits to secure expertise.

These labor shortages complicate scheduling and increase overheads, with temporary staffing and subcontractor premiums adding an estimated 3–5% to project budgets in 2024, pressuring profitability on fixed‑price contracts.

Commercial real estate demand

The shift to hybrid work cut global office occupancy to about 55–65% in 2024, shrinking demand for large floorplates and boosting spend on tech-enabled fit-outs; corporate average fit-out budgets rose ~8–12% as firms prioritized quality over square footage.

ISG must pivot to specialized, sustainable interiors—demand for green-certified refurbishments grew 18% in 2024—and offer modular, tech-integrated solutions to capture this evolving market.

- Office occupancy 55–65% (2024)

- Fit-out budgets +8–12% (2024)

- Green refurb demand +18% (2024)

Currency exchange volatility

As a multinational, ISG plc faces currency exchange volatility that can swing reported EBITDA by several percent; for example, a 5% GBP weakness against the euro in 2024 would have amplified project revenues in continental Europe while squeezing UK-costed margins.

Managing multi-currency revenue and costs requires hedging—forward contracts and natural hedges—to guard against sudden devaluations in key markets; ISG’s 2024 disclosure noted foreign-exchange translation impacted profit before tax variability by mid-single digits.

Economic instability in major regions creates financial reporting challenges that can reduce consolidated returns and increase balance sheet FX exposure, elevating the need for dynamic treasury policies and scenario stress-testing.

- FX swings can move EBITDA by mid-single digits (2024 observed)

- Hedging and natural hedges used to mitigate translation risk

- Regional instability raises reporting volatility and balance-sheet exposure

Rising rates, inflation squeeze margins; ISG saves £25–30m as fit‑outs and green refurb surge

Rising UK rates (BoE 5.25% 2024) and material inflation (steel +18% vs 2019; timber +12% y/y H2 2025) squeezed margins; ISG secured c.£25–30m procurement savings in 2024. Labour cost growth ~6.1% (2024) and staff costs ~8–10% of Opex raised project overheads. Office occupancy 55–65% (2024) shifted demand to higher‑value fit-outs (+8–12%) and green refurb (+18%). FX volatility moved EBITDA by mid‑single digits (2024).

| Metric | Value |

|---|---|

| BoE rate (2024) | 5.25% |

| Steel vs 2019 | +18% |

| Lumber y/y H2 2025 | +12% |

| Labour pay growth (2024) | 6.1% |

| Procurement savings (2024) | £25–30m |

Full Version Awaits

ISG plc PESTLE Analysis

The preview shown here is the exact ISG plc PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.