ISID Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

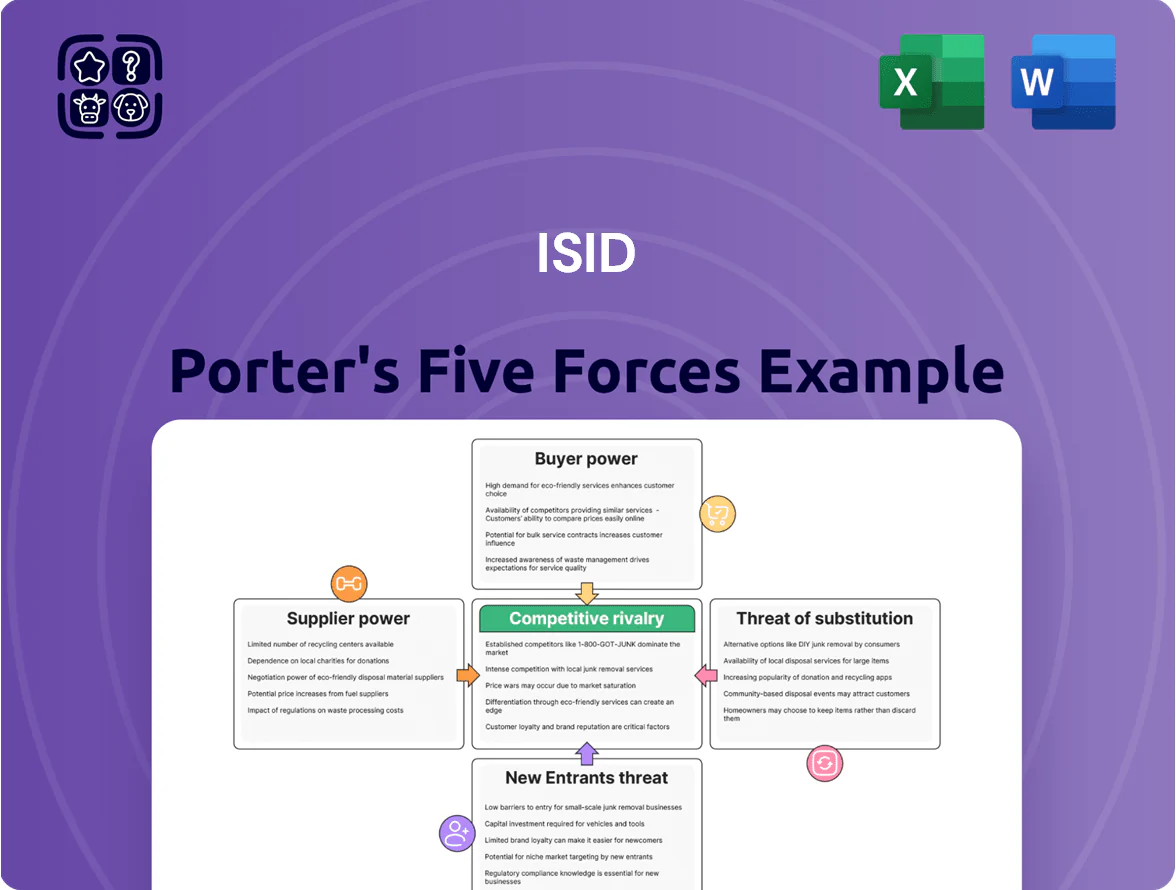

ISID faces moderate supplier leverage and rising buyer sophistication, while substitute threats and regulatory shifts shape its competitive landscape; entry barriers are influenced by tech capital and incumbents’ scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ISID’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Software Vendors

ISID depends on SAP, Oracle, and Microsoft for ERP and cloud infrastructure, and these three held roughly 60% of global enterprise software revenue in 2024, giving them strong leverage.

Their proprietary tech and migration costs—often $1M+ for mid-sized clients—raise switching barriers, so ISID faces limited alternatives.

By end-2025 vendor consolidation reduced supplier competition, shrinking ISID’s ability to win lower licensing or cloud pricing.

Scarcity of Specialized Technical Talent

The Japanese labor market still shows a structural shortfall of AI and cybersecurity specialists, with METI reporting a 2024 shortage of roughly 300,000 IT roles and average software engineer salaries rising about 6.5% YoY in 2024; this scarcity raises suppliers’ (talent and specialist agencies) bargaining power. Since ISID’s core value is human capital, rising wage demands and bidding from global tech firms push ISID to boost retention spending and training—ISID may need to allocate an extra 5–8% of payroll to stay competitive.

Dominance of Hyperscale Cloud Providers

Rising Costs of Specialized Hardware

For edge computing and high-end simulation projects, specialized semiconductors and components are scarce: global advanced chip capacity was tight in 2024 with foundry utilization around 80–90%, letting suppliers set lead times of 12–36 weeks and price premia of 10–30% versus commodity parts.

Geopolitical strain—US export controls and China relations—keeps supply concentrated among a few vendors, so hardware makers can force schedule shifts and cost overruns that threaten fixed-budget deliveries.

What this hides: a single delayed GPU or ASIC can stall multi-month deployments and raise project costs by 5–15%.

- Foundry utilization 80–90% (2024)

- Lead times 12–36 weeks

- Price premia 10–30% for specialized parts

- Project cost risk +5–15% from single-part delays

Intellectual Property and Patent Licensing

Integration of advanced algorithms and third-party IP forces ISID to pay ongoing royalties and meet strict usage terms; global fintech patent licensing fees averaged 5–12% of SaaS revenue in 2024, raising variable costs.

Suppliers of niche patents in fintech and automotive engineering hold high leverage because many standards depend on their IP, so ISID keeps long-term partnerships that often accept less favorable financial terms.

Here’s the quick math: if royalties hit 8% on a $120M contract, ISID pays $9.6M annually, squeezing margins and bargaining flexibility.

- Royalties 5–12% typical (2024)

- Niche patent suppliers = high leverage

- Long-term deals often favor suppliers

- $9.6M = 8% of $120M contract

Supplier dominance fuels rising tech costs: software, hyperscalers, parts & talent squeeze

Suppliers hold strong power: SAP/Oracle/Microsoft ~60% enterprise software revenue (2024), hyperscalers AWS/GCP account for 30–50% of ISID tech spend, foundry utilization 80–90% (2024) with 12–36 week lead times and 10–30% price premia, talent shortfall ~300,000 IT roles (Japan, METI 2024) forcing 5–8% extra payroll, and royalties typically 5–12% (2024) — single GPU delays can add 5–15% to project costs.

| Metric | 2024 Value |

|---|---|

| Top 3 enterprise SW share | ~60% |

| Hyperscaler share of tech spend | 30–50% |

| Foundry utilization | 80–90% |

| Lead times (specialized parts) | 12–36 wks |

| Price premia (special parts) | 10–30% |

| Japan IT role shortfall | ~300,000 |

| Payroll uplift to retain talent | +5–8% |

| Royalty range | 5–12% |

| Project cost risk (single-part delay) | +5–15% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and industry rivalry specific to ISID, highlighting disruptive threats, pricing influence, and strategic levers to protect and grow market share.

Interactive ISID Porter's Five Forces summary that quantifies strategic pressure, lets you toggle scenarios (regulation, entrants) and exports a clean chart for decks—no Excel macros required.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A small set of manufacturing and financial giants accounts for roughly 55% of ISID’s revenue as of FY2024, giving those clients outsized bargaining power since each contract is a high-value account critical to cash flow.

Because renewals can swing quarterly results, these customers press for custom features, faster delivery—often under 90 days—and volume discounts of 10–25% versus standard pricing.

Increased Demand for Measurable ROI

Low Switching Costs for Standardized Services

While core system migrations remain complex, modular cloud platforms and SaaS growth (SaaS revenue hit $214B in 2024) let clients unbundle IT and swap vendors for functions like marketing automation, HR, or analytics.

This cherry-picking lowers relationship stickiness, so ISID faces stronger customer bargaining: expect pricing pressure and service-level competition, with churn risk rising if onboarding exceeds 14 days.

Internal IT Capabilities of Clients

Large Japanese firms built internal digital units; by 2024 about 62% of top 200 firms increased in-house cloud/dev hires, cutting external spend by ~18% year-on-year.

As clients master cloud ops and dev, their bargaining power rises sharply; they can demand lower prices, faster innovation, or shift work in-house if ROI falls below internal thresholds.

- 62% top 200 firms boosted in-house digital hires (2024)

- ~18% average cut in external SI spend (YoY)

- Higher threat of insourcing raises price/innovation pressure

Price Transparency in Global Markets

The global nature of IT consulting and software development gives clients transparent price benchmarks: 2024 offshore rates averaged $25–40/hr in South Asia versus $120–200/hr in North America, so buyers can easily compare domestic integration costs to global consultancies and offshore centers.

This transparency caps ISID’s ability to charge premiums unless it proves localized value—factors like Japan-specific regulation expertise or faster time-to-market that justify 20–40% price gaps.

- Offshore avg $25–40/hr (2024)

- US/NA avg $120–200/hr (2024)

- Premiums need 20–40% local-value gap

High client leverage, ROI demands & in‑house hiring squeeze SI margins

Major clients (55% revenue FY2024) hold strong leverage, forcing 10–25% discounts, 90-day delivery demands, and outcome-tied SLAs (10–30% fees). By late 2025, 74% of buyers insist on measurable ROI; 62% of top 200 firms increased in-house hires (2024), cutting external SI spend ~18% YoY, raising churn risk if onboarding >14 days.

| Metric | Value |

|---|---|

| Revenue concentration | 55% (FY2024) |

| Buyer ROI demand | 74% (late 2025) |

| In-house hires | 62% top 200 (2024) |

| Cut in external spend | ~18% YoY (2024) |

| Offshore rates | $25–40/hr (2024) |

| NA rates | $120–200/hr (2024) |

Full Version Awaits

ISID Porter's Five Forces Analysis

This preview shows the exact ISID Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready to use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

ISID faces moderate supplier leverage and rising buyer sophistication, while substitute threats and regulatory shifts shape its competitive landscape; entry barriers are influenced by tech capital and incumbents’ scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ISID’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global Software Vendors

ISID depends on SAP, Oracle, and Microsoft for ERP and cloud infrastructure, and these three held roughly 60% of global enterprise software revenue in 2024, giving them strong leverage.

Their proprietary tech and migration costs—often $1M+ for mid-sized clients—raise switching barriers, so ISID faces limited alternatives.

By end-2025 vendor consolidation reduced supplier competition, shrinking ISID’s ability to win lower licensing or cloud pricing.

Scarcity of Specialized Technical Talent

The Japanese labor market still shows a structural shortfall of AI and cybersecurity specialists, with METI reporting a 2024 shortage of roughly 300,000 IT roles and average software engineer salaries rising about 6.5% YoY in 2024; this scarcity raises suppliers’ (talent and specialist agencies) bargaining power. Since ISID’s core value is human capital, rising wage demands and bidding from global tech firms push ISID to boost retention spending and training—ISID may need to allocate an extra 5–8% of payroll to stay competitive.

Dominance of Hyperscale Cloud Providers

Rising Costs of Specialized Hardware

For edge computing and high-end simulation projects, specialized semiconductors and components are scarce: global advanced chip capacity was tight in 2024 with foundry utilization around 80–90%, letting suppliers set lead times of 12–36 weeks and price premia of 10–30% versus commodity parts.

Geopolitical strain—US export controls and China relations—keeps supply concentrated among a few vendors, so hardware makers can force schedule shifts and cost overruns that threaten fixed-budget deliveries.

What this hides: a single delayed GPU or ASIC can stall multi-month deployments and raise project costs by 5–15%.

- Foundry utilization 80–90% (2024)

- Lead times 12–36 weeks

- Price premia 10–30% for specialized parts

- Project cost risk +5–15% from single-part delays

Intellectual Property and Patent Licensing

Integration of advanced algorithms and third-party IP forces ISID to pay ongoing royalties and meet strict usage terms; global fintech patent licensing fees averaged 5–12% of SaaS revenue in 2024, raising variable costs.

Suppliers of niche patents in fintech and automotive engineering hold high leverage because many standards depend on their IP, so ISID keeps long-term partnerships that often accept less favorable financial terms.

Here’s the quick math: if royalties hit 8% on a $120M contract, ISID pays $9.6M annually, squeezing margins and bargaining flexibility.

- Royalties 5–12% typical (2024)

- Niche patent suppliers = high leverage

- Long-term deals often favor suppliers

- $9.6M = 8% of $120M contract

Supplier dominance fuels rising tech costs: software, hyperscalers, parts & talent squeeze

Suppliers hold strong power: SAP/Oracle/Microsoft ~60% enterprise software revenue (2024), hyperscalers AWS/GCP account for 30–50% of ISID tech spend, foundry utilization 80–90% (2024) with 12–36 week lead times and 10–30% price premia, talent shortfall ~300,000 IT roles (Japan, METI 2024) forcing 5–8% extra payroll, and royalties typically 5–12% (2024) — single GPU delays can add 5–15% to project costs.

| Metric | 2024 Value |

|---|---|

| Top 3 enterprise SW share | ~60% |

| Hyperscaler share of tech spend | 30–50% |

| Foundry utilization | 80–90% |

| Lead times (specialized parts) | 12–36 wks |

| Price premia (special parts) | 10–30% |

| Japan IT role shortfall | ~300,000 |

| Payroll uplift to retain talent | +5–8% |

| Royalty range | 5–12% |

| Project cost risk (single-part delay) | +5–15% |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and industry rivalry specific to ISID, highlighting disruptive threats, pricing influence, and strategic levers to protect and grow market share.

Interactive ISID Porter's Five Forces summary that quantifies strategic pressure, lets you toggle scenarios (regulation, entrants) and exports a clean chart for decks—no Excel macros required.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A small set of manufacturing and financial giants accounts for roughly 55% of ISID’s revenue as of FY2024, giving those clients outsized bargaining power since each contract is a high-value account critical to cash flow.

Because renewals can swing quarterly results, these customers press for custom features, faster delivery—often under 90 days—and volume discounts of 10–25% versus standard pricing.

Increased Demand for Measurable ROI

Low Switching Costs for Standardized Services

While core system migrations remain complex, modular cloud platforms and SaaS growth (SaaS revenue hit $214B in 2024) let clients unbundle IT and swap vendors for functions like marketing automation, HR, or analytics.

This cherry-picking lowers relationship stickiness, so ISID faces stronger customer bargaining: expect pricing pressure and service-level competition, with churn risk rising if onboarding exceeds 14 days.

Internal IT Capabilities of Clients

Large Japanese firms built internal digital units; by 2024 about 62% of top 200 firms increased in-house cloud/dev hires, cutting external spend by ~18% year-on-year.

As clients master cloud ops and dev, their bargaining power rises sharply; they can demand lower prices, faster innovation, or shift work in-house if ROI falls below internal thresholds.

- 62% top 200 firms boosted in-house digital hires (2024)

- ~18% average cut in external SI spend (YoY)

- Higher threat of insourcing raises price/innovation pressure

Price Transparency in Global Markets

The global nature of IT consulting and software development gives clients transparent price benchmarks: 2024 offshore rates averaged $25–40/hr in South Asia versus $120–200/hr in North America, so buyers can easily compare domestic integration costs to global consultancies and offshore centers.

This transparency caps ISID’s ability to charge premiums unless it proves localized value—factors like Japan-specific regulation expertise or faster time-to-market that justify 20–40% price gaps.

- Offshore avg $25–40/hr (2024)

- US/NA avg $120–200/hr (2024)

- Premiums need 20–40% local-value gap

High client leverage, ROI demands & in‑house hiring squeeze SI margins

Major clients (55% revenue FY2024) hold strong leverage, forcing 10–25% discounts, 90-day delivery demands, and outcome-tied SLAs (10–30% fees). By late 2025, 74% of buyers insist on measurable ROI; 62% of top 200 firms increased in-house hires (2024), cutting external SI spend ~18% YoY, raising churn risk if onboarding >14 days.

| Metric | Value |

|---|---|

| Revenue concentration | 55% (FY2024) |

| Buyer ROI demand | 74% (late 2025) |

| In-house hires | 62% top 200 (2024) |

| Cut in external spend | ~18% YoY (2024) |

| Offshore rates | $25–40/hr (2024) |

| NA rates | $120–200/hr (2024) |

Full Version Awaits

ISID Porter's Five Forces Analysis

This preview shows the exact ISID Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready to use with no placeholders or mockups.