ISS Schweiz SWOT Analysis

Make Insightful Decisions Backed by Expert Research

ISS Schweiz stands at the intersection of strong service capabilities and a shifting European facilities market, presenting clear operational strengths but exposure to labor costs and regulatory complexity; our full SWOT unpacks these dynamics with actionable strategies and financial context. Purchase the complete SWOT analysis to receive a professional, editable Word and Excel package—ready for investor decks, strategic planning, and due diligence.

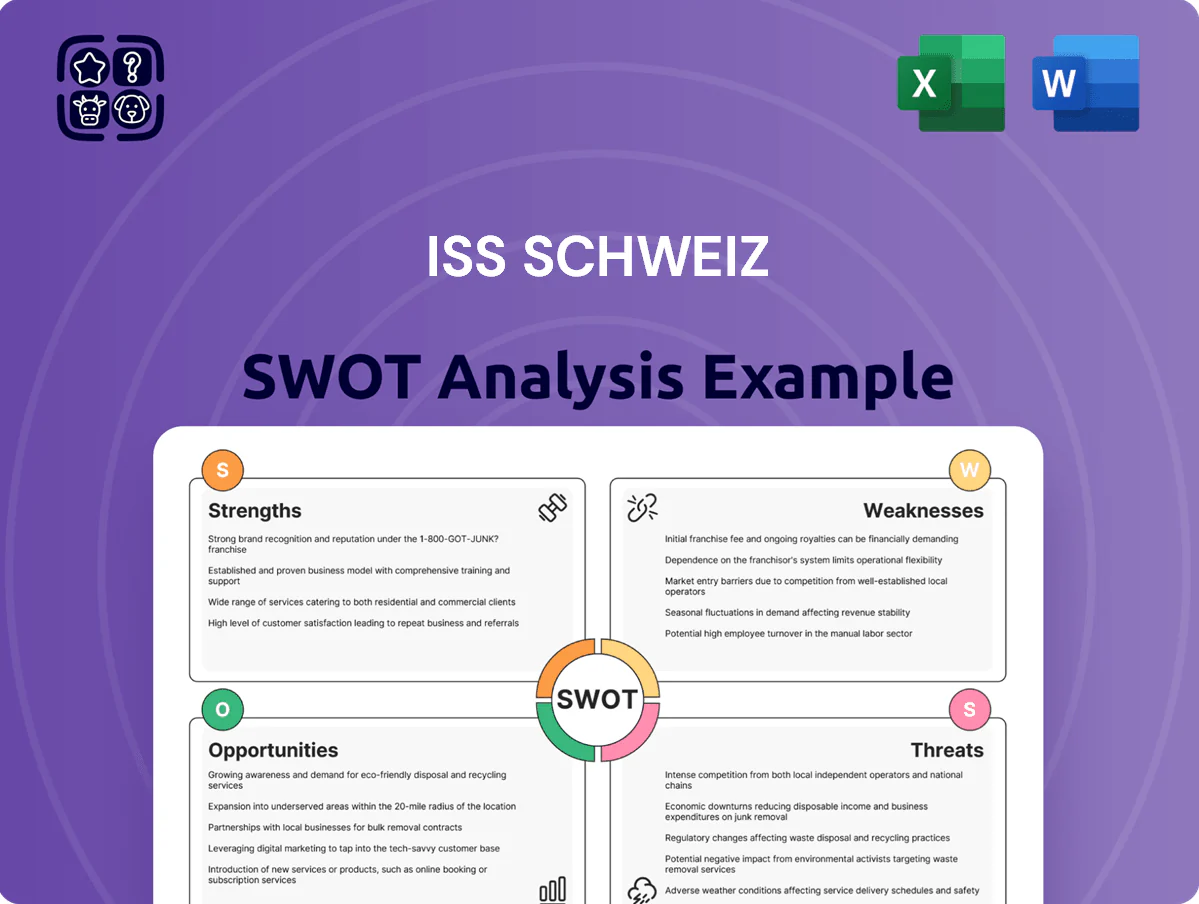

Strengths

Market Leadership and Scale

ISS Schweiz is among the top facility management providers in Switzerland, with estimated 2024 revenues around CHF 1.1bn and operations in all 26 cantons, giving strong national scale. This size creates economies of scope—bulk procurement and shared services—reducing supplier costs by an estimated 6–10% versus local firms. The broad footprint supports consistent service to 2,000+ multi-site clients and high operational reliability.

Integrated Facility Services Model

ISS Schweiz offers a single-source model combining cleaning, catering, technical services, and security, cutting client vendor management and raising switching costs—contracts averaged CHF 4.2m in 2024, up 6% YoY.

Integrated delivery supports multi-year contracts (median 4.5 years) and stable revenue—2024 service-retention exceeded 88%—protecting margins in tight markets.

Managing multiple lines lets ISS Schweiz reallocate 3–7% of labor hours monthly, improving building efficiency and reducing overtime by 12% in 2024.

Strong Brand and Global Expertise

As part of global ISS A/S, ISS Schweiz taps into group-wide best practices and tech frameworks used across 60+ countries, enabling scale and consistency; the ISS brand—contributing to ISS A/S €10.4bn revenue in 2024—signals reliability prized in Swiss corporate procurement. Clients access global innovation labs and standardized processes, a competitive edge over many local providers, and benefit from group investments of ~€120m/year in tech and sustainability R&D.

Diversified High-Value Client Base

ISS Schweiz serves blue-chip clients in pharma, finance, and public sectors, including contracts with firms representing over CHF 3.5bn in combined Swiss revenue, which cushions revenue during sector downturns.

The mix delivers recurring income from essential services—cleanroom and banking facility management—contributing to a stable 2024 Swiss division margin near 8.5%.

Their cleanroom and secure-site expertise is a clear competitive edge, reducing client churn and enabling premium pricing.

- Diversified client mix: pharma, finance, public

- CHF 3.5bn estimated client revenue exposure

- 2024 Swiss margin ≈ 8.5%

- Specialized cleanroom/banking expertise

Commitment to Quality Standards

ISS Schweiz: CHF1.1bn leader—92% retention, 4.5yr contracts, premium margins

ISS Schweiz is a national leader with ~CHF 1.1bn 2024 revenue, operations in all 26 cantons, 2,000+ multi-site clients and 88–92% retention; integrated services (cleaning, technical, security, catering) yield 4.5-year median contracts and ~8.5% Swiss margin. Group backing (ISS A/S €10.4bn 2024) supplies €120m/year tech R&D and lets ISS charge ~15% contract premium for cleanroom/banking expertise.

| Metric | 2024 |

|---|---|

| Swiss revenue | CHF 1.1bn |

| Client retention | 92% |

| Median contract length | 4.5 yrs |

| Swiss margin | ≈8.5% |

| Contract premium vs peers | ~15% |

What is included in the product

Provides a concise SWOT overview of ISS Schweiz, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decision-making.

Delivers a compact SWOT matrix tailored to ISS Schweiz for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Pressure on Operating Margins

ISS Schweiz operates in low-margin, labor-heavy services—cleaning and security—where global FM median EBIT margins are ~4–6% and Swiss labor costs are among highest: average employer cost per employee CHF 111,000 in 2024 (SECO).

High Swiss wage inflation (2.9% in 2024) and energy upswings squeeze margins; failure to pass ~3–5% annual cost rises to clients can cut operating profit immediately.

High Dependency on Labor

A large share of ISS Schweiz’s services depends on manual labor, leaving it exposed to Swiss labor market shifts; Switzerland’s unemployment was 2.1% in 2024, tightening supply and lifting wages by about 3–4% year-on-year in facilities sectors.

Recruiting certified cleaners and technicians in a low-unemployment market raises hiring costs; ISS reported Swiss personnel expenses rose ~6% in 2023, reflecting higher recruitment and wages.

Entry-level turnover—often 25–35% annually in cleaning roles—raises training spend and risks uneven service quality, increasing supervision and rework costs.

Complex Organizational Structure

Being part of ISS A/S (global revenue €12.6bn in 2024) creates layers of approval that can slow Swiss-site decisions, adding 2–6 weeks to rollouts versus local rivals. Aligning with global directives often clashes with Swiss market needs—ISS Schweiz missed a 2023 bid opportunity cited by local sources due to central constraints. This complexity reduces speed against niche Swiss competitors growing ~4–7% annually.

Limited Growth in Traditional Segments

The Swiss facility management market is mature; basic cleaning growth is near-stagnant and ISS Schweiz faces capped organic revenue—Swiss FM revenue grew only 0.5% in 2024, per Branchenverband Gebäude- und Raumdienste (BGR), signaling saturation.

To sustain margins ISS Schweiz must pivot to technical and digital services, yet that shift needs heavy upfront capex—ISS Group invested EUR 200m in tech in 2023 as indication of scale required.

Failure to innovate risks revenue decline as price competition intensifies and low-margin contracts persist.

- Swiss FM growth ~0.5% (2024, BGR)

- Basic cleaning commoditized; low margins

- Shift to tech/digital needs large capex (e.g., EUR 200m ISS Group 2023)

- Market saturation caps organic growth

Vulnerability to Client Consolidation

ISS Schweiz risks contract downsizing as Swiss firms cut office space or adopt permanent hybrid work; Swiss office vacancy hit 11.2% in Q4 2024, raising demand risk for facility services.

Large clients in banking and insurance account for an estimated 20–30% of revenue; a 25% portfolio reduction by top clients could trim overall revenue by ~5–7%.

The firm’s earnings closely track physical occupancy and maintenance needs, so sustained lower occupancy would pressure margins and renegotiation leverage.

- Q4 2024 Swiss office vacancy 11.2%

- Top-client concentration ~20–30% of revenue

- 25% large-client cut → ~5–7% revenue hit

- Direct linkage: occupancy → service demand → margins

Swiss FM under squeeze: high labor costs, thin margins, turnover and client risk

High Swiss labor costs and low FM margins (median 4–6%) compress profits; employer cost/employee CHF 111,000 (2024, SECO). Wage inflation 2.9% (2024) and energy swings force 3–5% price pass-through or margin loss. High turnover (25–35%) and 6%+ personnel cost rise (ISS 2023) raise training and supervision spend. Market saturation (Swiss FM growth 0.5% 2024) and client concentration (20–30% revenue) heighten revenue risk.

| Metric | Value |

|---|---|

| Employer cost/employee | CHF 111,000 (2024, SECO) |

| Wage inflation | 2.9% (2024) |

| FM median EBIT | 4–6% |

| Turnover (cleaning) | 25–35% |

| Swiss FM growth | 0.5% (2024, BGR) |

| Top-client share | 20–30% |

Same Document Delivered

ISS Schweiz SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the content shown is a real excerpt of the editable file. Purchase unlocks the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

ISS Schweiz stands at the intersection of strong service capabilities and a shifting European facilities market, presenting clear operational strengths but exposure to labor costs and regulatory complexity; our full SWOT unpacks these dynamics with actionable strategies and financial context. Purchase the complete SWOT analysis to receive a professional, editable Word and Excel package—ready for investor decks, strategic planning, and due diligence.

Strengths

Market Leadership and Scale

ISS Schweiz is among the top facility management providers in Switzerland, with estimated 2024 revenues around CHF 1.1bn and operations in all 26 cantons, giving strong national scale. This size creates economies of scope—bulk procurement and shared services—reducing supplier costs by an estimated 6–10% versus local firms. The broad footprint supports consistent service to 2,000+ multi-site clients and high operational reliability.

Integrated Facility Services Model

ISS Schweiz offers a single-source model combining cleaning, catering, technical services, and security, cutting client vendor management and raising switching costs—contracts averaged CHF 4.2m in 2024, up 6% YoY.

Integrated delivery supports multi-year contracts (median 4.5 years) and stable revenue—2024 service-retention exceeded 88%—protecting margins in tight markets.

Managing multiple lines lets ISS Schweiz reallocate 3–7% of labor hours monthly, improving building efficiency and reducing overtime by 12% in 2024.

Strong Brand and Global Expertise

As part of global ISS A/S, ISS Schweiz taps into group-wide best practices and tech frameworks used across 60+ countries, enabling scale and consistency; the ISS brand—contributing to ISS A/S €10.4bn revenue in 2024—signals reliability prized in Swiss corporate procurement. Clients access global innovation labs and standardized processes, a competitive edge over many local providers, and benefit from group investments of ~€120m/year in tech and sustainability R&D.

Diversified High-Value Client Base

ISS Schweiz serves blue-chip clients in pharma, finance, and public sectors, including contracts with firms representing over CHF 3.5bn in combined Swiss revenue, which cushions revenue during sector downturns.

The mix delivers recurring income from essential services—cleanroom and banking facility management—contributing to a stable 2024 Swiss division margin near 8.5%.

Their cleanroom and secure-site expertise is a clear competitive edge, reducing client churn and enabling premium pricing.

- Diversified client mix: pharma, finance, public

- CHF 3.5bn estimated client revenue exposure

- 2024 Swiss margin ≈ 8.5%

- Specialized cleanroom/banking expertise

Commitment to Quality Standards

ISS Schweiz: CHF1.1bn leader—92% retention, 4.5yr contracts, premium margins

ISS Schweiz is a national leader with ~CHF 1.1bn 2024 revenue, operations in all 26 cantons, 2,000+ multi-site clients and 88–92% retention; integrated services (cleaning, technical, security, catering) yield 4.5-year median contracts and ~8.5% Swiss margin. Group backing (ISS A/S €10.4bn 2024) supplies €120m/year tech R&D and lets ISS charge ~15% contract premium for cleanroom/banking expertise.

| Metric | 2024 |

|---|---|

| Swiss revenue | CHF 1.1bn |

| Client retention | 92% |

| Median contract length | 4.5 yrs |

| Swiss margin | ≈8.5% |

| Contract premium vs peers | ~15% |

What is included in the product

Provides a concise SWOT overview of ISS Schweiz, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decision-making.

Delivers a compact SWOT matrix tailored to ISS Schweiz for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

Pressure on Operating Margins

ISS Schweiz operates in low-margin, labor-heavy services—cleaning and security—where global FM median EBIT margins are ~4–6% and Swiss labor costs are among highest: average employer cost per employee CHF 111,000 in 2024 (SECO).

High Swiss wage inflation (2.9% in 2024) and energy upswings squeeze margins; failure to pass ~3–5% annual cost rises to clients can cut operating profit immediately.

High Dependency on Labor

A large share of ISS Schweiz’s services depends on manual labor, leaving it exposed to Swiss labor market shifts; Switzerland’s unemployment was 2.1% in 2024, tightening supply and lifting wages by about 3–4% year-on-year in facilities sectors.

Recruiting certified cleaners and technicians in a low-unemployment market raises hiring costs; ISS reported Swiss personnel expenses rose ~6% in 2023, reflecting higher recruitment and wages.

Entry-level turnover—often 25–35% annually in cleaning roles—raises training spend and risks uneven service quality, increasing supervision and rework costs.

Complex Organizational Structure

Being part of ISS A/S (global revenue €12.6bn in 2024) creates layers of approval that can slow Swiss-site decisions, adding 2–6 weeks to rollouts versus local rivals. Aligning with global directives often clashes with Swiss market needs—ISS Schweiz missed a 2023 bid opportunity cited by local sources due to central constraints. This complexity reduces speed against niche Swiss competitors growing ~4–7% annually.

Limited Growth in Traditional Segments

The Swiss facility management market is mature; basic cleaning growth is near-stagnant and ISS Schweiz faces capped organic revenue—Swiss FM revenue grew only 0.5% in 2024, per Branchenverband Gebäude- und Raumdienste (BGR), signaling saturation.

To sustain margins ISS Schweiz must pivot to technical and digital services, yet that shift needs heavy upfront capex—ISS Group invested EUR 200m in tech in 2023 as indication of scale required.

Failure to innovate risks revenue decline as price competition intensifies and low-margin contracts persist.

- Swiss FM growth ~0.5% (2024, BGR)

- Basic cleaning commoditized; low margins

- Shift to tech/digital needs large capex (e.g., EUR 200m ISS Group 2023)

- Market saturation caps organic growth

Vulnerability to Client Consolidation

ISS Schweiz risks contract downsizing as Swiss firms cut office space or adopt permanent hybrid work; Swiss office vacancy hit 11.2% in Q4 2024, raising demand risk for facility services.

Large clients in banking and insurance account for an estimated 20–30% of revenue; a 25% portfolio reduction by top clients could trim overall revenue by ~5–7%.

The firm’s earnings closely track physical occupancy and maintenance needs, so sustained lower occupancy would pressure margins and renegotiation leverage.

- Q4 2024 Swiss office vacancy 11.2%

- Top-client concentration ~20–30% of revenue

- 25% large-client cut → ~5–7% revenue hit

- Direct linkage: occupancy → service demand → margins

Swiss FM under squeeze: high labor costs, thin margins, turnover and client risk

High Swiss labor costs and low FM margins (median 4–6%) compress profits; employer cost/employee CHF 111,000 (2024, SECO). Wage inflation 2.9% (2024) and energy swings force 3–5% price pass-through or margin loss. High turnover (25–35%) and 6%+ personnel cost rise (ISS 2023) raise training and supervision spend. Market saturation (Swiss FM growth 0.5% 2024) and client concentration (20–30% revenue) heighten revenue risk.

| Metric | Value |

|---|---|

| Employer cost/employee | CHF 111,000 (2024, SECO) |

| Wage inflation | 2.9% (2024) |

| FM median EBIT | 4–6% |

| Turnover (cleaning) | 25–35% |

| Swiss FM growth | 0.5% (2024, BGR) |

| Top-client share | 20–30% |

Same Document Delivered

ISS Schweiz SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the content shown is a real excerpt of the editable file. Purchase unlocks the complete, detailed version immediately after checkout.