Isuzu Motors PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Isuzu Motors faces shifting regulatory, economic, and technological currents that will redefine commercial-vehicle demand and supply chains; our PESTLE highlights risks from emissions rules, trade policy, and EV transition while identifying growth in emerging markets and logistics digitization. Purchase the full PESTLE for a ready-to-use, deeply researched roadmap to inform investment decisions and strategic planning.

Political factors

Geopolitical Trade Tensions

Ongoing trade disputes—notably US-China tariffs and ASEAN-EU negotiations—are reshaping Isuzu’s supply chain and export routes; in 2024 Isuzu reported 38% of global truck exports tied to Southeast Asia, making tariff shifts material. A 5–10% tariff increase on commercial vehicles or engine parts could raise unit production costs by an estimated $500–$1,200, squeezing margins. Maintaining market share in ASEAN and emerging markets requires active diplomatic risk management and supply diversification.

Government Infrastructure Spending

National infrastructure budgets directly boost demand for Isuzu’s heavy trucks and construction gear; for example, India’s 2025-26 capital expenditure rose 11% to Rs 10.4 trillion, and ASEAN public investment grew ~4.2% in 2024, expanding procurement opportunities. As urbanization and logistics upgrades in developing markets continue, Isuzu gains larger fleet and OEM contracts; however, austerity or policy shifts toward digital infrastructure could reduce physical-asset orders and slow revenue growth.

Subsidies for Green Transition

Political subsidies for EVs and hydrogen trucks shape Isuzu’s R&D, with Japan’s 2024 subsidy program offering up to ¥3.6m (~$25k) per EV truck and Thailand’s EV tax breaks reducing purchase costs by ~30%, prompting Isuzu to accelerate low-emission powertrain development.

Regulatory Stability in Emerging Markets

Isuzu’s heavy exposure to Thailand and India—which accounted for about 35% of global sales and 28% of revenues in 2024—makes it vulnerable to political instability and abrupt policy shifts that can disrupt production and capex plans.

Sudden leadership changes or industrial-policy revisions have previously delayed plant expansions; a single-year tariff hike of 5–10% could materially raise unit costs and squeeze margins.

Maintaining strong local political ties and lobbying helped Isuzu secure incentives worth roughly $120m across ASEAN in 2023–24, mitigating risks from protectionist measures.

- 35% sales exposure to Thailand/India (2024)

- 28% revenue dependence (2024)

- $120m incentives secured (2023–24)

- Potential 5–10% tariff shocks raise unit costs

Global Security and Supply Routes

Political instability along key shipping corridors—Red Sea, Strait of Hormuz, and South China Sea—threatens Isuzu’s timely delivery of vehicles and parts; 2024 attacks and insurance premium spikes raised container rates by ~25% in some lanes, straining margins.

Rising maritime security incidents and regional conflicts increase logistics complexity and costs, pushing rerouting and longer transit times that inflate supply-chain expenses.

Isuzu must monitor hotspots to protect its just-in-time production: delays of even 7–14 days can halt assembly lines and impact FY2024 revenue streams.

- Shipping disruptions up 2024: ~25% rate increase on affected routes

- Critical chokepoints: Red Sea, Strait of Hormuz, South China Sea

- Delay impact: 7–14 days can stop JIT lines

Isuzu at Risk: 35% Exposure to Thailand/India — Tariffs + Shipping Shocks Threaten Margins

Political risks—trade tariffs, subsidies, and regional instability—directly affect Isuzu’s costs, demand, and operations; 2024: 35% sales exposure to Thailand/India, 28% revenue, $120m incentives secured. Tariff shocks of 5–10% could add $500–$1,200/unit; Red Sea/Strait/South China Sea disruptions raised some container rates ~25% in 2024, causing 7–14 day delays that can halt JIT lines.

| Metric | 2024/2023–24 |

|---|---|

| Sales exposure (Thailand/India) | 35% |

| Revenue dependence | 28% |

| Incentives secured | $120m |

| Tariff shock impact | $500–$1,200/unit |

| Shipping rate spike (affected lanes) | ~25% |

| Delay impact | 7–14 days |

What is included in the product

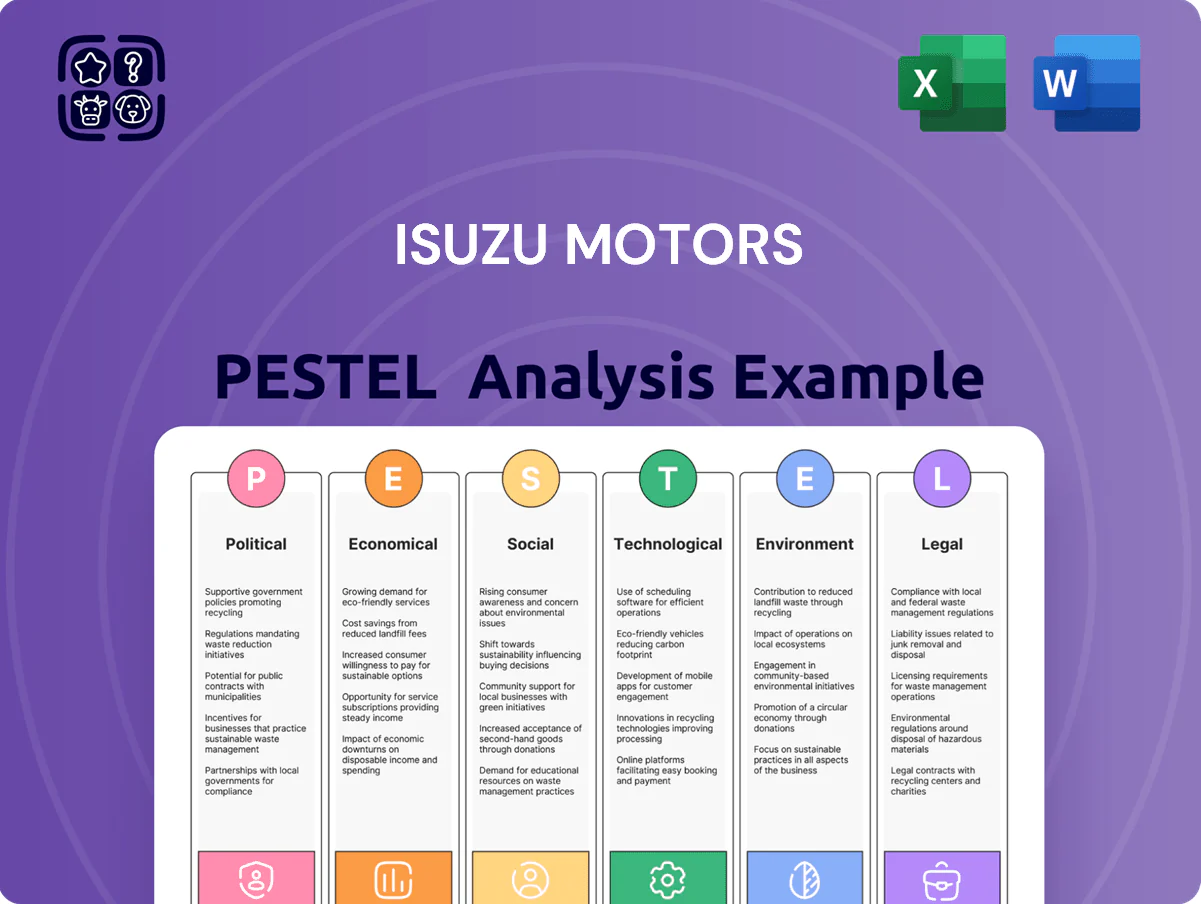

Explores how external macro-environmental factors uniquely affect Isuzu Motors across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Isuzu Motors PESTLE snapshot that relieves planning pain by summarizing key external risks and opportunities for quick insertion into presentations, collaborative sessions, or client reports.

Economic factors

Fluctuations in Global Interest Rates

High global interest rates raise financing costs for commercial vehicle buyers; OECD data shows corporate lending rates rose to ~6.1% in 2024, increasing likelihood of deferred fleet upgrades. Isuzu’s volumes depend on affordable SME credit—SMEs contribute about 40–50% of light/medium truck purchases in key markets like ASEAN. With central banks tightening to curb 2023–24 inflation, Isuzu must expand captive finance, longer tenors, and leasing to sustain demand.

Currency Exchange Rate Volatility

As a Japan-headquartered exporter, Isuzu is sensitive to JPY/USD and JPY/EUR moves; JPY strengthened ~9% vs USD in 2024 H2, which can raise export prices overseas and compress volumes.

A weaker yen in 2025 YTD (≈6% decline vs USD through Jan 2026) can boost reported export margins but raises costs for imported steel/parts, which accounted for ~28% of COGS in FY2024.

Active hedging—forward contracts and natural hedges—remains vital: Isuzu reported FX hedges covering roughly 40% of anticipated net exposures as of FY2024.

Commodity Price Inflation

The 2024 average steel price rose ~18% YoY to $820/ton and aluminum climbed 12% to $2,350/ton, while rare-earth oxide basket prices surged ~35% in 2023–24, directly increasing Isuzu’s material costs for engines and chassis; sustained input inflation pressures gross margins unless offset.

Isuzu must boost operational efficiency—2023 global automotive input cost inflation averaged ~9%—or pass costs to buyers; delayed pass-through risks volume decline in price-sensitive commercial vehicle segments.

Rising energy costs from 2022–24 raised manufacturing overheads ~6–9% across Japan, Thailand and Brazil plants, further squeezing margins and pushing capital allocation toward energy efficiency and supply-chain hedging.

Economic Growth in Southeast Asia

- ASEAN GDP ~4.6% (2024)

- Thailand GDP ~3.3% (2024)

- Isuzu Thailand market share ≈30% (2024)

- Higher trade/logistics = ↑ LCV demand

Labor Cost Trends

- Wage growth 4–6% (2024–25)

- Manufacturing wages ~$4–6/hr in key hubs

- Robot density target 300→450/10,000 by 2025

- Capex needed to automate vs. relocate production

Isuzu margins squeezed by rates, steel and FX as ASEAN demand and automation reshape costs

| Item | Value |

|---|---|

| OECD lending rate (2024) | ~6.1% |

| Steel (2024) | $820/t |

| ASEAN GDP (2024) | 4.6% |

| Thailand GDP (2024) | 3.3% |

| Isuzu Thailand share (2024) | ~30% |

| Wage growth (2024–25) | 4–6% |

Full Version Awaits

Isuzu Motors PESTLE Analysis

The preview shown here is the exact Isuzu Motors PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content and structure visible are the same file you’ll download immediately after payment, with no placeholders or teasers. This is the real, finished product—professionally structured and ready for analysis and presentation. Everything displayed here is part of the final deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Isuzu Motors faces shifting regulatory, economic, and technological currents that will redefine commercial-vehicle demand and supply chains; our PESTLE highlights risks from emissions rules, trade policy, and EV transition while identifying growth in emerging markets and logistics digitization. Purchase the full PESTLE for a ready-to-use, deeply researched roadmap to inform investment decisions and strategic planning.

Political factors

Geopolitical Trade Tensions

Ongoing trade disputes—notably US-China tariffs and ASEAN-EU negotiations—are reshaping Isuzu’s supply chain and export routes; in 2024 Isuzu reported 38% of global truck exports tied to Southeast Asia, making tariff shifts material. A 5–10% tariff increase on commercial vehicles or engine parts could raise unit production costs by an estimated $500–$1,200, squeezing margins. Maintaining market share in ASEAN and emerging markets requires active diplomatic risk management and supply diversification.

Government Infrastructure Spending

National infrastructure budgets directly boost demand for Isuzu’s heavy trucks and construction gear; for example, India’s 2025-26 capital expenditure rose 11% to Rs 10.4 trillion, and ASEAN public investment grew ~4.2% in 2024, expanding procurement opportunities. As urbanization and logistics upgrades in developing markets continue, Isuzu gains larger fleet and OEM contracts; however, austerity or policy shifts toward digital infrastructure could reduce physical-asset orders and slow revenue growth.

Subsidies for Green Transition

Political subsidies for EVs and hydrogen trucks shape Isuzu’s R&D, with Japan’s 2024 subsidy program offering up to ¥3.6m (~$25k) per EV truck and Thailand’s EV tax breaks reducing purchase costs by ~30%, prompting Isuzu to accelerate low-emission powertrain development.

Regulatory Stability in Emerging Markets

Isuzu’s heavy exposure to Thailand and India—which accounted for about 35% of global sales and 28% of revenues in 2024—makes it vulnerable to political instability and abrupt policy shifts that can disrupt production and capex plans.

Sudden leadership changes or industrial-policy revisions have previously delayed plant expansions; a single-year tariff hike of 5–10% could materially raise unit costs and squeeze margins.

Maintaining strong local political ties and lobbying helped Isuzu secure incentives worth roughly $120m across ASEAN in 2023–24, mitigating risks from protectionist measures.

- 35% sales exposure to Thailand/India (2024)

- 28% revenue dependence (2024)

- $120m incentives secured (2023–24)

- Potential 5–10% tariff shocks raise unit costs

Global Security and Supply Routes

Political instability along key shipping corridors—Red Sea, Strait of Hormuz, and South China Sea—threatens Isuzu’s timely delivery of vehicles and parts; 2024 attacks and insurance premium spikes raised container rates by ~25% in some lanes, straining margins.

Rising maritime security incidents and regional conflicts increase logistics complexity and costs, pushing rerouting and longer transit times that inflate supply-chain expenses.

Isuzu must monitor hotspots to protect its just-in-time production: delays of even 7–14 days can halt assembly lines and impact FY2024 revenue streams.

- Shipping disruptions up 2024: ~25% rate increase on affected routes

- Critical chokepoints: Red Sea, Strait of Hormuz, South China Sea

- Delay impact: 7–14 days can stop JIT lines

Isuzu at Risk: 35% Exposure to Thailand/India — Tariffs + Shipping Shocks Threaten Margins

Political risks—trade tariffs, subsidies, and regional instability—directly affect Isuzu’s costs, demand, and operations; 2024: 35% sales exposure to Thailand/India, 28% revenue, $120m incentives secured. Tariff shocks of 5–10% could add $500–$1,200/unit; Red Sea/Strait/South China Sea disruptions raised some container rates ~25% in 2024, causing 7–14 day delays that can halt JIT lines.

| Metric | 2024/2023–24 |

|---|---|

| Sales exposure (Thailand/India) | 35% |

| Revenue dependence | 28% |

| Incentives secured | $120m |

| Tariff shock impact | $500–$1,200/unit |

| Shipping rate spike (affected lanes) | ~25% |

| Delay impact | 7–14 days |

What is included in the product

Explores how external macro-environmental factors uniquely affect Isuzu Motors across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific regulatory context to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Isuzu Motors PESTLE snapshot that relieves planning pain by summarizing key external risks and opportunities for quick insertion into presentations, collaborative sessions, or client reports.

Economic factors

Fluctuations in Global Interest Rates

High global interest rates raise financing costs for commercial vehicle buyers; OECD data shows corporate lending rates rose to ~6.1% in 2024, increasing likelihood of deferred fleet upgrades. Isuzu’s volumes depend on affordable SME credit—SMEs contribute about 40–50% of light/medium truck purchases in key markets like ASEAN. With central banks tightening to curb 2023–24 inflation, Isuzu must expand captive finance, longer tenors, and leasing to sustain demand.

Currency Exchange Rate Volatility

As a Japan-headquartered exporter, Isuzu is sensitive to JPY/USD and JPY/EUR moves; JPY strengthened ~9% vs USD in 2024 H2, which can raise export prices overseas and compress volumes.

A weaker yen in 2025 YTD (≈6% decline vs USD through Jan 2026) can boost reported export margins but raises costs for imported steel/parts, which accounted for ~28% of COGS in FY2024.

Active hedging—forward contracts and natural hedges—remains vital: Isuzu reported FX hedges covering roughly 40% of anticipated net exposures as of FY2024.

Commodity Price Inflation

The 2024 average steel price rose ~18% YoY to $820/ton and aluminum climbed 12% to $2,350/ton, while rare-earth oxide basket prices surged ~35% in 2023–24, directly increasing Isuzu’s material costs for engines and chassis; sustained input inflation pressures gross margins unless offset.

Isuzu must boost operational efficiency—2023 global automotive input cost inflation averaged ~9%—or pass costs to buyers; delayed pass-through risks volume decline in price-sensitive commercial vehicle segments.

Rising energy costs from 2022–24 raised manufacturing overheads ~6–9% across Japan, Thailand and Brazil plants, further squeezing margins and pushing capital allocation toward energy efficiency and supply-chain hedging.

Economic Growth in Southeast Asia

- ASEAN GDP ~4.6% (2024)

- Thailand GDP ~3.3% (2024)

- Isuzu Thailand market share ≈30% (2024)

- Higher trade/logistics = ↑ LCV demand

Labor Cost Trends

- Wage growth 4–6% (2024–25)

- Manufacturing wages ~$4–6/hr in key hubs

- Robot density target 300→450/10,000 by 2025

- Capex needed to automate vs. relocate production

Isuzu margins squeezed by rates, steel and FX as ASEAN demand and automation reshape costs

| Item | Value |

|---|---|

| OECD lending rate (2024) | ~6.1% |

| Steel (2024) | $820/t |

| ASEAN GDP (2024) | 4.6% |

| Thailand GDP (2024) | 3.3% |

| Isuzu Thailand share (2024) | ~30% |

| Wage growth (2024–25) | 4–6% |

Full Version Awaits

Isuzu Motors PESTLE Analysis

The preview shown here is the exact Isuzu Motors PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content and structure visible are the same file you’ll download immediately after payment, with no placeholders or teasers. This is the real, finished product—professionally structured and ready for analysis and presentation. Everything displayed here is part of the final deliverable.