ITV PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic pressures, and fast-moving tech trends are shaping ITV’s strategic outlook in our concise PESTLE snapshot—designed to help investors and strategists act with confidence; buy the full analysis to access the complete, editable report and actionable insights instantly.

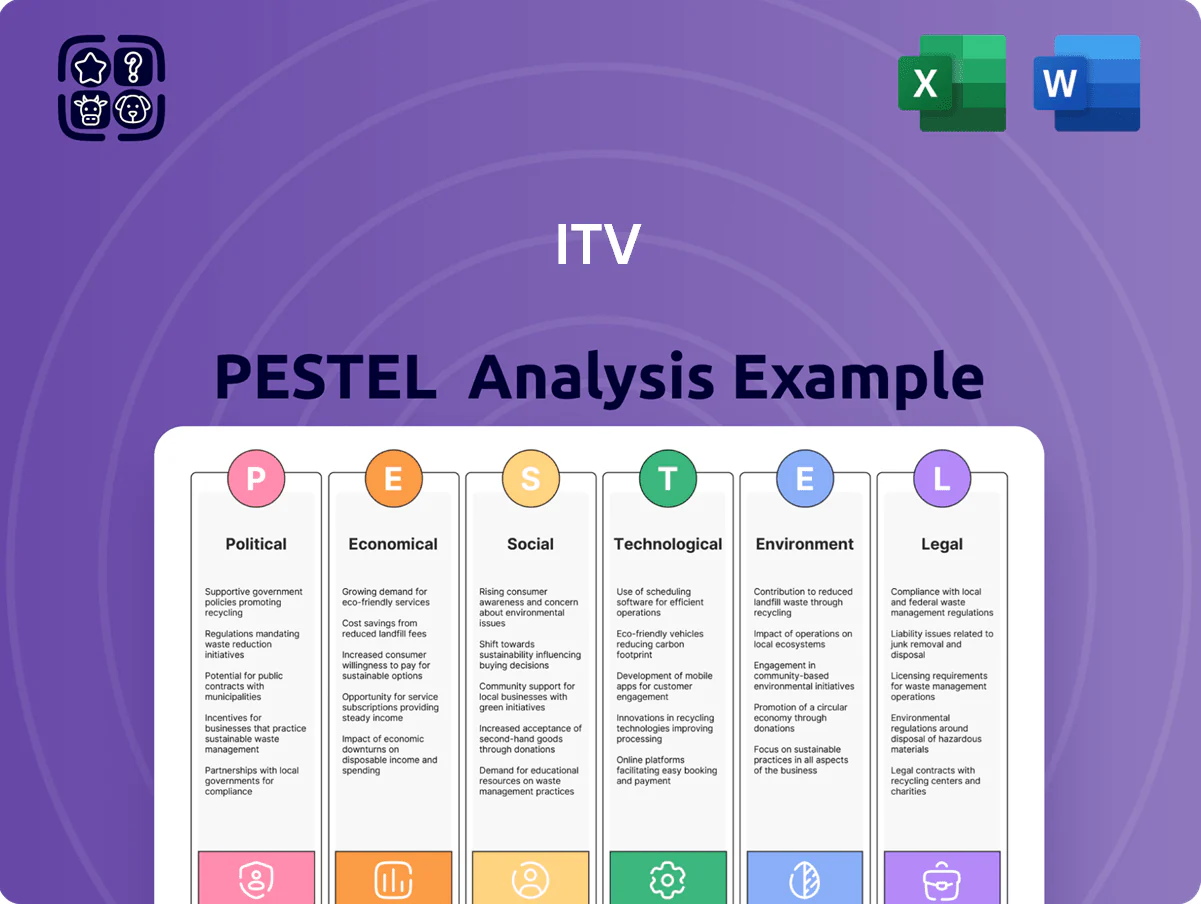

Political factors

Ofcom Media Bill Implementation

The 2024 Media Act reached full implementation by late 2025, legally guaranteeing ITV and other PSBs prominence on smart-TV home screens and platform guides, increasing discoverability for ITVX which reported 42 million monthly active users in 2025. This political intervention helps shield ITV’s streaming apps from algorithmic burying by global tech platforms, supporting a 7% uplift in UK streaming share for PSBs versus 2023. The regulatory framework reallocates catalogue visibility and advertising inventory to better balance competition with US tech giants, affecting ad revenues—ITV reported UK streaming ad revenue of £370m in H1 2025, up 12% year-on-year.

Post-Election Fiscal Policy

Following the 2024 general election, the 2025 fiscal roadmap preserved the UK’s creative tax reliefs, with film and high-end TV reliefs reducing marginal production costs by an estimated 12–15% for studios; corporate tax remained at 25% after the 2023 rise, affecting ITV Studios’ after-tax margins. Political stability in 2025 unlocked £500m+ in public support commitments for screen production hubs, while executives monitor Treasury signals on R&D and creative incentives that could shift capex and commissioning strategies.

BBC Charter and Funding Debates

Ongoing political debates over the BBC charter and potential license fee changes—parliamentary reviews in 2024 considered reductions up to 20% in BBC funding—reshape ITV’s competitive landscape by potentially shifting audience share and increasing bidding for talent.

Trade Relations and Global Distribution

Political stability in UK-EU and UK-US trade agreements affects ITV Studios’ ability to export content; post-Brexit arrangements and the UK-US trade dialogue shape tariffs, quotas, and market access for TV rights.

By late 2025 harmonization of IP protections and cross-border data flow rules remains a priority—affecting licensing, streaming, and rights enforcement across jurisdictions.

Geopolitical friction (e.g., sanctions, trade disputes) can interrupt a pipeline that contributes roughly 30–40% of ITV’s non-advertising revenue, increasing distribution risk and contract renegotiation costs.

- Trade stability shapes export costs and market access

- IP/data harmonization critical for streaming/licensing

- International sales ~30–40% of non-advertising revenue

- Geopolitical shocks raise distribution and legal risks

Advertising Regulation on Public Health

Government moves to restrict HFSS advertising threaten ITV’s linear ad revenue, with Ofcom and UK government consultations in 2024 targeting watershed rules that could affect ~25% of food and drink ad spend on TV; ITV must diversify digital and non-HFSS advertisers to protect revenue.

Political pressure requires intensified lobbying and compliance costs—ITV reported regulatory and compliance expenses of £42m in FY2024—and ongoing adaptation to shifting rules on family viewing hours is essential to safeguard peak-time inventory value.

- HFSS rules risk ~25% of TV food/drink ad revenue

- FY2024 regulatory/compliance costs £42m for ITV

- Need to diversify advertiser mix toward non-HFSS and digital

- Continuous lobbying required as watershed policies evolve

ITV: 42m ITVX MAUs, £370m streaming ads; costs cut 12–15%, HFSS ads risk ~25%

Political support for PSB prominence (Media Act) boosted ITVX discoverability; ITVX 2025 MAUs 42m and H1 2025 UK streaming ad revenue £370m (+12% YoY). Creative tax reliefs cut production costs ~12–15%; corporate tax 25%. International sales ~30–40% of non-ad revenue; FY2024 regulatory costs £42m. HFSS ad curbs risk ~25% of food/drink TV ad spend.

| Metric | Value |

|---|---|

| ITVX MAUs (2025) | 42m |

| H1 2025 streaming ads | £370m (+12%) |

| Prod cost reduction | 12–15% |

| Intl share of non-ad rev | 30–40% |

| FY2024 reg costs | £42m |

| HFSS ad risk | ~25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact ITV, using current data and trends to highlight risks and opportunities for broadcasters and streaming services.

A concise, visually segmented ITV PESTLE summary that can be dropped into presentations or shared across teams for fast alignment, with editable notes for regional or business-line specifics.

Economic factors

Cyclical Advertising Market Volatility

As of late 2025 the UK ad market fell 3.2% YoY in H1 2025 amid weak GDP growth and consumer confidence, exposing ITV’s linear ad reliance; linear TV ad revenue declined c.8% in 2024–25 while digital ad revenue grew ~12%. Economic downturns prompt immediate brand budget cuts, pushing ITV to lean on Studios, which contributed ~30% of group adjusted EBITDA in FY2024. ITV is accelerating digital ad and addressable offerings to reduce cyclicality.

Cost of Content Production Inflation

The global surge in demand for premium scripted content has pushed average production budgets up to 30-50% since 2019, with top-tier UK drama episodes often costing over 1m GBP each, raising talent, crew and studio expenses for ITV Studios.

ITV faces margin pressure as commissioning fees compress in competitive bids; ITV Studios reported studio operating margins around mid-single digits in 2023, highlighting sensitivity to input-cost inflation.

Controlling talent and facility spend, leveraging co-productions and tax incentives (UK tax reliefs saving up to 25% of qualifying spend) is essential for preserving profitability as the production arm scales globally.

Consumer Discretionary Spending Trends

ITVX Premium's uptake and paid add-ons are closely tied to household disposable income; UK real wages remained 0.2% below pre-COVID levels in 2024, limiting pay-TV spend. With US/UK consumers subscribing to a median of 4–5 streaming services in 2024, willingness to pay is saturated, capping TAM for ITVX Premium. In weak growth scenarios subscription fatigue shifts growth to ITV's ad-funded tier, which delivered 2024 digital ad revenue growth of ~8% y/y.

Interest Rates and Debt Servicing

Rising UK Bank Rate (5.25% as of Dec 2023, little changed through 2025) has increased ITV’s average borrowing costs, tightening capacity for large M&A at ITV Studios and elevating 2024 net finance costs (ITV reported £82m net finance costs in FY 2023 into higher 2024 estimates).

Higher rates force ITV to prioritise servicing c.£1.2bn net debt (FY 2023) while allocating capex to digital transformation and content spend to defend advertising and streaming revenues.

- UK Bank Rate ~5.25% (Dec 2023–2025)

- ITV net debt ~£1.2bn (FY 2023)

- FY 2023 net finance costs ~£82m

- Higher rates constrain ITV Studios M&A pace and increase trade-off vs content/digital investment

Currency Exchange Rate Fluctuations

ITV Studios faces material FX risk with 2024 revenue ~45% generated overseas; a 5% GBP weakness vs USD/Euro can boost translated earnings materially, while a 5% strengthening would reverse that effect.

In FY2024 ITV reported net debt £1.1bn; hedging reduced currency volatility impact—formal hedges covered ~60% of projected 12-month USD/EUR cashflows as of Dec 2024.

- ~45% revenue from US/Europe in 2024

- 5% GBP move materially alters translated earnings

- Net debt £1.1bn (FY2024) increases FX sensitivity

- Hedges covered ~60% of 12-month FX exposure (Dec 2024)

UK ad slump and costly studios squeeze margins as debt, rates and FX risk rise

UK ad market weakness (H1 2025 -3.2% YoY) and tepid wage growth compress linear ad revenue (-c.8% 2024–25) while digital ads grew ~10–12%; Studios (~30% group EBITDA FY2024) face rising production costs (+30–50% since 2019) and margin pressure (mid-single digit studio margins 2023). Net debt ~£1.1–1.2bn (FY2023–24), UK Bank Rate ~5.25% (2023–25) and FX exposure (~45% revenue overseas) heighten financial sensitivity.

| Metric | Value |

|---|---|

| UK ad market H1 2025 | -3.2% YoY |

| Linear ad rev change 2024–25 | -c.8% |

| Digital ad growth | ~10–12% |

| Studios EBITDA share FY2024 | ~30% |

| Studio margins (2023) | Mid-single digits |

| Net debt FY2024 | ~£1.1–1.2bn |

| UK Bank Rate | ~5.25% |

| Overseas revenue | ~45% |

Same Document Delivered

ITV PESTLE Analysis

The preview shown here is the exact ITV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file you’re seeing, not a teaser or placeholder, so the content, layout, and headings match the downloadable product exactly. After checkout you’ll instantly get this same finished document for immediate use in research, presentations, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic pressures, and fast-moving tech trends are shaping ITV’s strategic outlook in our concise PESTLE snapshot—designed to help investors and strategists act with confidence; buy the full analysis to access the complete, editable report and actionable insights instantly.

Political factors

Ofcom Media Bill Implementation

The 2024 Media Act reached full implementation by late 2025, legally guaranteeing ITV and other PSBs prominence on smart-TV home screens and platform guides, increasing discoverability for ITVX which reported 42 million monthly active users in 2025. This political intervention helps shield ITV’s streaming apps from algorithmic burying by global tech platforms, supporting a 7% uplift in UK streaming share for PSBs versus 2023. The regulatory framework reallocates catalogue visibility and advertising inventory to better balance competition with US tech giants, affecting ad revenues—ITV reported UK streaming ad revenue of £370m in H1 2025, up 12% year-on-year.

Post-Election Fiscal Policy

Following the 2024 general election, the 2025 fiscal roadmap preserved the UK’s creative tax reliefs, with film and high-end TV reliefs reducing marginal production costs by an estimated 12–15% for studios; corporate tax remained at 25% after the 2023 rise, affecting ITV Studios’ after-tax margins. Political stability in 2025 unlocked £500m+ in public support commitments for screen production hubs, while executives monitor Treasury signals on R&D and creative incentives that could shift capex and commissioning strategies.

BBC Charter and Funding Debates

Ongoing political debates over the BBC charter and potential license fee changes—parliamentary reviews in 2024 considered reductions up to 20% in BBC funding—reshape ITV’s competitive landscape by potentially shifting audience share and increasing bidding for talent.

Trade Relations and Global Distribution

Political stability in UK-EU and UK-US trade agreements affects ITV Studios’ ability to export content; post-Brexit arrangements and the UK-US trade dialogue shape tariffs, quotas, and market access for TV rights.

By late 2025 harmonization of IP protections and cross-border data flow rules remains a priority—affecting licensing, streaming, and rights enforcement across jurisdictions.

Geopolitical friction (e.g., sanctions, trade disputes) can interrupt a pipeline that contributes roughly 30–40% of ITV’s non-advertising revenue, increasing distribution risk and contract renegotiation costs.

- Trade stability shapes export costs and market access

- IP/data harmonization critical for streaming/licensing

- International sales ~30–40% of non-advertising revenue

- Geopolitical shocks raise distribution and legal risks

Advertising Regulation on Public Health

Government moves to restrict HFSS advertising threaten ITV’s linear ad revenue, with Ofcom and UK government consultations in 2024 targeting watershed rules that could affect ~25% of food and drink ad spend on TV; ITV must diversify digital and non-HFSS advertisers to protect revenue.

Political pressure requires intensified lobbying and compliance costs—ITV reported regulatory and compliance expenses of £42m in FY2024—and ongoing adaptation to shifting rules on family viewing hours is essential to safeguard peak-time inventory value.

- HFSS rules risk ~25% of TV food/drink ad revenue

- FY2024 regulatory/compliance costs £42m for ITV

- Need to diversify advertiser mix toward non-HFSS and digital

- Continuous lobbying required as watershed policies evolve

ITV: 42m ITVX MAUs, £370m streaming ads; costs cut 12–15%, HFSS ads risk ~25%

Political support for PSB prominence (Media Act) boosted ITVX discoverability; ITVX 2025 MAUs 42m and H1 2025 UK streaming ad revenue £370m (+12% YoY). Creative tax reliefs cut production costs ~12–15%; corporate tax 25%. International sales ~30–40% of non-ad revenue; FY2024 regulatory costs £42m. HFSS ad curbs risk ~25% of food/drink TV ad spend.

| Metric | Value |

|---|---|

| ITVX MAUs (2025) | 42m |

| H1 2025 streaming ads | £370m (+12%) |

| Prod cost reduction | 12–15% |

| Intl share of non-ad rev | 30–40% |

| FY2024 reg costs | £42m |

| HFSS ad risk | ~25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact ITV, using current data and trends to highlight risks and opportunities for broadcasters and streaming services.

A concise, visually segmented ITV PESTLE summary that can be dropped into presentations or shared across teams for fast alignment, with editable notes for regional or business-line specifics.

Economic factors

Cyclical Advertising Market Volatility

As of late 2025 the UK ad market fell 3.2% YoY in H1 2025 amid weak GDP growth and consumer confidence, exposing ITV’s linear ad reliance; linear TV ad revenue declined c.8% in 2024–25 while digital ad revenue grew ~12%. Economic downturns prompt immediate brand budget cuts, pushing ITV to lean on Studios, which contributed ~30% of group adjusted EBITDA in FY2024. ITV is accelerating digital ad and addressable offerings to reduce cyclicality.

Cost of Content Production Inflation

The global surge in demand for premium scripted content has pushed average production budgets up to 30-50% since 2019, with top-tier UK drama episodes often costing over 1m GBP each, raising talent, crew and studio expenses for ITV Studios.

ITV faces margin pressure as commissioning fees compress in competitive bids; ITV Studios reported studio operating margins around mid-single digits in 2023, highlighting sensitivity to input-cost inflation.

Controlling talent and facility spend, leveraging co-productions and tax incentives (UK tax reliefs saving up to 25% of qualifying spend) is essential for preserving profitability as the production arm scales globally.

Consumer Discretionary Spending Trends

ITVX Premium's uptake and paid add-ons are closely tied to household disposable income; UK real wages remained 0.2% below pre-COVID levels in 2024, limiting pay-TV spend. With US/UK consumers subscribing to a median of 4–5 streaming services in 2024, willingness to pay is saturated, capping TAM for ITVX Premium. In weak growth scenarios subscription fatigue shifts growth to ITV's ad-funded tier, which delivered 2024 digital ad revenue growth of ~8% y/y.

Interest Rates and Debt Servicing

Rising UK Bank Rate (5.25% as of Dec 2023, little changed through 2025) has increased ITV’s average borrowing costs, tightening capacity for large M&A at ITV Studios and elevating 2024 net finance costs (ITV reported £82m net finance costs in FY 2023 into higher 2024 estimates).

Higher rates force ITV to prioritise servicing c.£1.2bn net debt (FY 2023) while allocating capex to digital transformation and content spend to defend advertising and streaming revenues.

- UK Bank Rate ~5.25% (Dec 2023–2025)

- ITV net debt ~£1.2bn (FY 2023)

- FY 2023 net finance costs ~£82m

- Higher rates constrain ITV Studios M&A pace and increase trade-off vs content/digital investment

Currency Exchange Rate Fluctuations

ITV Studios faces material FX risk with 2024 revenue ~45% generated overseas; a 5% GBP weakness vs USD/Euro can boost translated earnings materially, while a 5% strengthening would reverse that effect.

In FY2024 ITV reported net debt £1.1bn; hedging reduced currency volatility impact—formal hedges covered ~60% of projected 12-month USD/EUR cashflows as of Dec 2024.

- ~45% revenue from US/Europe in 2024

- 5% GBP move materially alters translated earnings

- Net debt £1.1bn (FY2024) increases FX sensitivity

- Hedges covered ~60% of 12-month FX exposure (Dec 2024)

UK ad slump and costly studios squeeze margins as debt, rates and FX risk rise

UK ad market weakness (H1 2025 -3.2% YoY) and tepid wage growth compress linear ad revenue (-c.8% 2024–25) while digital ads grew ~10–12%; Studios (~30% group EBITDA FY2024) face rising production costs (+30–50% since 2019) and margin pressure (mid-single digit studio margins 2023). Net debt ~£1.1–1.2bn (FY2023–24), UK Bank Rate ~5.25% (2023–25) and FX exposure (~45% revenue overseas) heighten financial sensitivity.

| Metric | Value |

|---|---|

| UK ad market H1 2025 | -3.2% YoY |

| Linear ad rev change 2024–25 | -c.8% |

| Digital ad growth | ~10–12% |

| Studios EBITDA share FY2024 | ~30% |

| Studio margins (2023) | Mid-single digits |

| Net debt FY2024 | ~£1.1–1.2bn |

| UK Bank Rate | ~5.25% |

| Overseas revenue | ~45% |

Same Document Delivered

ITV PESTLE Analysis

The preview shown here is the exact ITV PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file you’re seeing, not a teaser or placeholder, so the content, layout, and headings match the downloadable product exactly. After checkout you’ll instantly get this same finished document for immediate use in research, presentations, or strategic planning.