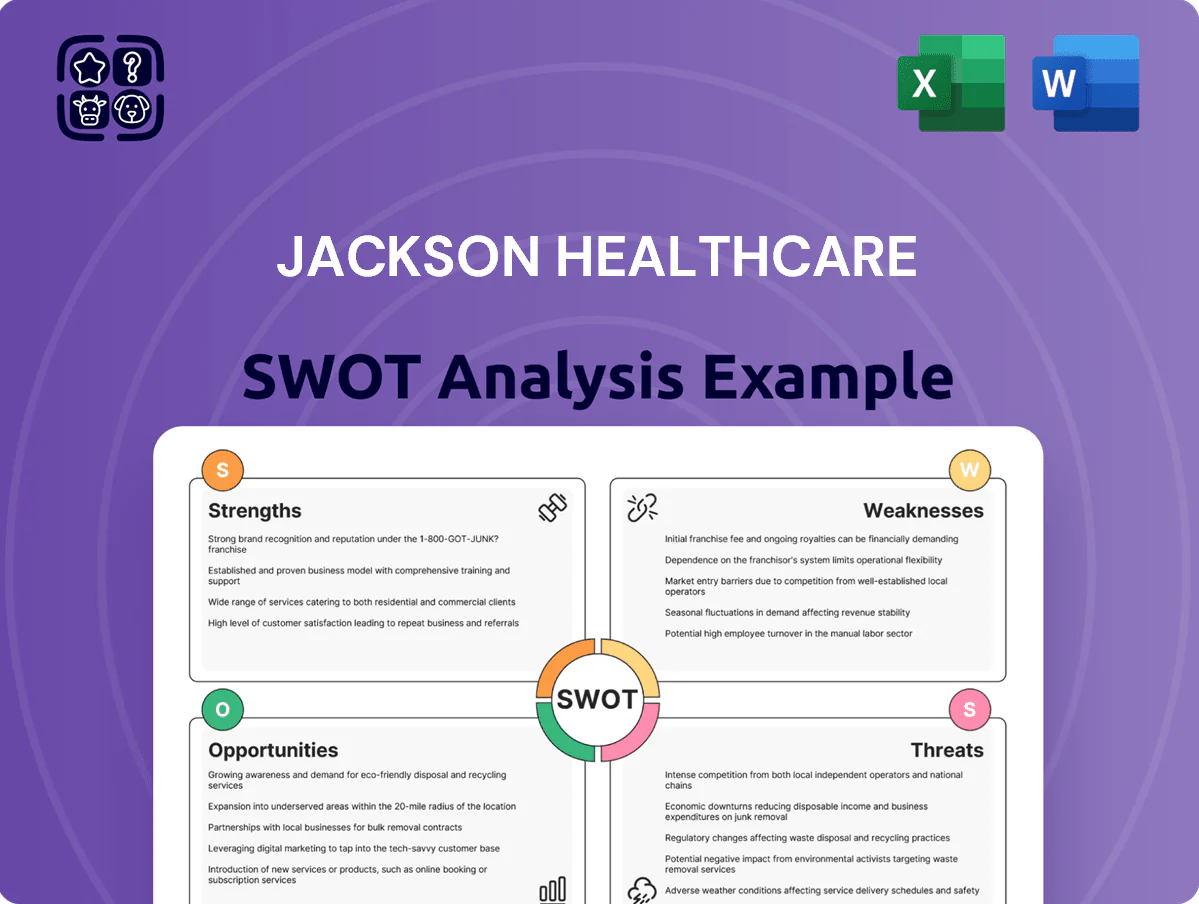

Jackson Healthcare SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Jackson Healthcare’s strong niche in staffing and technology positions it well amid healthcare labor shortages, but reimbursement pressures and regulatory complexity pose clear risks; our full SWOT digs into competitive advantages, operational vulnerabilities, and strategic opportunities for expansion. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel files that support investment decisions, strategic planning, and presentations.

Strengths

Specialized Brand Portfolio

Jackson Healthcare runs a portfolio of specialist brands—LocumTenens.com, Jackson Nurse Professionals, and others—that reported combined 2024 revenue around $1.2 billion, letting each unit focus on niches like locum tenens and nursing.

This brand structure uses shared corporate services to cut SG&A and scale tech; Jackson reported 2024 adjusted EBITDA margin near 18%, improving margins across affiliates.

Market Leadership in Locum Tenens

Jackson Healthcare dominates the US locum tenens market, supplying temporary physicians to hospitals and clinics and capturing an estimated ~25% market share in 2024, enabling lower unit costs through scale.

Scale supports a database of 60,000+ qualified clinicians (2024), faster fills, and higher fill rates—reported fill-time averages near 7 days versus industry 14 days.

Their reputation makes them a go-to for large health systems; in 2024 top-50 health systems accounted for roughly 40% of locum revenue.

Award-Winning Corporate Culture

Jackson Healthcare, repeatedly listed on Glassdoor and Forbes Best Places to Work through 2024, keeps voluntary turnover below industry average (estimated ~15% vs. 20–25% peers), boosting recruiter continuity and candidate pipeline strength.

The positive culture cuts hiring time and raises fill-rate quality, helping Jackson report higher gross margin per placement and stronger client NPS; this edge fuels growth in a staffing market valued at ~$150B in 2024.

Integrated Healthcare Technology

- Proprietary scheduling and credentialing

- ~20% faster time-to-fill (2024)

- Improved retention vs manual peers

- ~10% revenue growth in tech services (2024)

Private Ownership Stability

- Private ownership: enables long-term planning

- 2024 revenue ~1.8B supports investments

- Patient capital for tech, M&A, expansion

- Stable leadership, values-driven growth

Jackson Healthcare: $1.8B scale, 25% locum share, 7-day fills, 18% adj. EBITDA

Jackson Healthcare’s scale and specialist brands drove ~2024 revenue $1.8B and adjusted EBITDA ~18%, ~25% share of US locum market, 60,000+ clinicians, ~7-day average fill vs 14 industry, ~20% faster time-to-fill from proprietary tech, ~10% tech-line revenue growth, and ~15% voluntary turnover—enabling higher margins, faster fills, and repeat business.

| Metric | 2024 |

|---|---|

| Revenue | $1.8B |

| Adj. EBITDA | ~18% |

| Locum share | ~25% |

| Clinicians | 60,000+ |

| Avg fill time | ~7 days |

| Time-to-fill improvement | ~20% |

| Tech rev growth | ~10% |

| Voluntary turnover | ~15% |

What is included in the product

Delivers a strategic overview of Jackson Healthcare’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Delivers a concise SWOT matrix tailored to Jackson Healthcare for rapid strategy alignment and stakeholder briefings.

Weaknesses

Geographic Concentration

Jackson Healthcare operates primarily in the United States, with over 90% of 2024 revenue tied to domestic staffing and workforce solutions, exposing it to U.S. economic cycles and Medicare/Medicaid policy shifts.

Limited international presence prevents Jackson from capturing global staffing shortages—WHO estimates a 15 million health worker shortfall by 2030—reducing diversification and growth upside.

This U.S. focus creates dependency: slowing U.S. healthcare spending growth (projected 5.4% CAGR 2024–2028) would materially hit Jackson’s top line and margins.

High Operational Complexity

Managing Jackson Healthcare’s 40+ specialized subsidiaries creates operational complexity and risks silos that raised SG&A margin to about 28% in 2024, above peer average of ~22%. Ensuring uniform service quality and brand messaging across ops requires heavy oversight—estimated $25–40M annual central coordination spend in similar roll-ups—otherwise inefficiencies surface and cross-sell capture (currently ~12% of revenue) can remain below potential.

Limited Public Financial Transparency

As a private company, Jackson Healthcare provides far less public financial transparency than public rivals, limiting analysts' access to audited revenue and margin trends; for context, private staffing peers report median gross margins near 25% publicly while Jackson's exact margins are undisclosed. This opacity makes it harder for external analysts and potential partners to assess solvency or valuation—private healthcare staffing deals in 2024 averaged EBITDA multiples of 8–12x, a benchmark Jackson's stakeholders cannot confirm openly. While privacy shields strategic data, it also constrains direct access to large capital markets—US IPO and follow-on equity raised $260 billion in 2024, funding scale Jackson cannot tap without going public or taking on costly alternatives.

Talent Acquisition Costs

The rising cost of recruiting and retaining clinical talent squeezes Jackson Healthcare’s margins: industry data show U.S. clinician turnover raises hiring spend ~20–30% and specialty locum costs rose 18% in 2024, forcing higher marketing and compensation outlays.

Competition for nurses and physicians, especially in specialties with <10% vacancy buffers, pushes acquisition costs higher and increases reliance on premium contracts and agency placements.

- Hiring spend up ~20–30% (turnover-driven)

- Specialty locum costs +18% in 2024

- Vacancy buffers <10% in key specialties

- Higher marketing and premium pay reduce margins

Dependency on Specific Clinical Segments

Jackson Healthcare relies heavily on high-demand segments like emergency medicine and nursing, where burnout rates exceed 40% in some studies and turnover can hit 20% annually, raising revenue volatility if supply drops or demand shifts.

Diversifying the provider mix is hard amid a 2024 U.S. clinician shortage estimated at 37,800 physicians and 1.1M nurses by 2030, so sector-specific shocks could disproportionately cut placements and fees.

- High burnout: >40% in emergency medicine

- Turnover: ~20% annually in nursing

- Projected shortages: 37,800 physicians by 2030

- Diversification remains operationally difficult

High U.S. Concentration, Rising Clinician Costs & Complex Structure Threaten Margins

Heavy U.S. concentration (90%+ revenue), limited international diversification, and exposure to Medicare/Medicaid shifts; complex 40+ subsidiary structure inflating SG&A (~28% vs peers ~22%) and reducing cross-sell (~12%); rising recruiting costs (turnover adds 20–30% hiring spend; specialty locum +18% in 2024) and clinician shortages (37,800 physicians, 1.1M nurses by 2030) raise margin and revenue volatility.

| Metric | Value |

|---|---|

| US revenue share | 90%+ |

| SG&A 2024 | ~28% |

| Cross-sell | ~12% |

| Locum cost change 2024 | +18% |

| Physician shortfall by 2030 | 37,800 |

Preview the Actual Deliverable

Jackson Healthcare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete, editable file. You’re viewing a live preview of the exact analysis; the full, detailed version becomes available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Jackson Healthcare’s strong niche in staffing and technology positions it well amid healthcare labor shortages, but reimbursement pressures and regulatory complexity pose clear risks; our full SWOT digs into competitive advantages, operational vulnerabilities, and strategic opportunities for expansion. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel files that support investment decisions, strategic planning, and presentations.

Strengths

Specialized Brand Portfolio

Jackson Healthcare runs a portfolio of specialist brands—LocumTenens.com, Jackson Nurse Professionals, and others—that reported combined 2024 revenue around $1.2 billion, letting each unit focus on niches like locum tenens and nursing.

This brand structure uses shared corporate services to cut SG&A and scale tech; Jackson reported 2024 adjusted EBITDA margin near 18%, improving margins across affiliates.

Market Leadership in Locum Tenens

Jackson Healthcare dominates the US locum tenens market, supplying temporary physicians to hospitals and clinics and capturing an estimated ~25% market share in 2024, enabling lower unit costs through scale.

Scale supports a database of 60,000+ qualified clinicians (2024), faster fills, and higher fill rates—reported fill-time averages near 7 days versus industry 14 days.

Their reputation makes them a go-to for large health systems; in 2024 top-50 health systems accounted for roughly 40% of locum revenue.

Award-Winning Corporate Culture

Jackson Healthcare, repeatedly listed on Glassdoor and Forbes Best Places to Work through 2024, keeps voluntary turnover below industry average (estimated ~15% vs. 20–25% peers), boosting recruiter continuity and candidate pipeline strength.

The positive culture cuts hiring time and raises fill-rate quality, helping Jackson report higher gross margin per placement and stronger client NPS; this edge fuels growth in a staffing market valued at ~$150B in 2024.

Integrated Healthcare Technology

- Proprietary scheduling and credentialing

- ~20% faster time-to-fill (2024)

- Improved retention vs manual peers

- ~10% revenue growth in tech services (2024)

Private Ownership Stability

- Private ownership: enables long-term planning

- 2024 revenue ~1.8B supports investments

- Patient capital for tech, M&A, expansion

- Stable leadership, values-driven growth

Jackson Healthcare: $1.8B scale, 25% locum share, 7-day fills, 18% adj. EBITDA

Jackson Healthcare’s scale and specialist brands drove ~2024 revenue $1.8B and adjusted EBITDA ~18%, ~25% share of US locum market, 60,000+ clinicians, ~7-day average fill vs 14 industry, ~20% faster time-to-fill from proprietary tech, ~10% tech-line revenue growth, and ~15% voluntary turnover—enabling higher margins, faster fills, and repeat business.

| Metric | 2024 |

|---|---|

| Revenue | $1.8B |

| Adj. EBITDA | ~18% |

| Locum share | ~25% |

| Clinicians | 60,000+ |

| Avg fill time | ~7 days |

| Time-to-fill improvement | ~20% |

| Tech rev growth | ~10% |

| Voluntary turnover | ~15% |

What is included in the product

Delivers a strategic overview of Jackson Healthcare’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Delivers a concise SWOT matrix tailored to Jackson Healthcare for rapid strategy alignment and stakeholder briefings.

Weaknesses

Geographic Concentration

Jackson Healthcare operates primarily in the United States, with over 90% of 2024 revenue tied to domestic staffing and workforce solutions, exposing it to U.S. economic cycles and Medicare/Medicaid policy shifts.

Limited international presence prevents Jackson from capturing global staffing shortages—WHO estimates a 15 million health worker shortfall by 2030—reducing diversification and growth upside.

This U.S. focus creates dependency: slowing U.S. healthcare spending growth (projected 5.4% CAGR 2024–2028) would materially hit Jackson’s top line and margins.

High Operational Complexity

Managing Jackson Healthcare’s 40+ specialized subsidiaries creates operational complexity and risks silos that raised SG&A margin to about 28% in 2024, above peer average of ~22%. Ensuring uniform service quality and brand messaging across ops requires heavy oversight—estimated $25–40M annual central coordination spend in similar roll-ups—otherwise inefficiencies surface and cross-sell capture (currently ~12% of revenue) can remain below potential.

Limited Public Financial Transparency

As a private company, Jackson Healthcare provides far less public financial transparency than public rivals, limiting analysts' access to audited revenue and margin trends; for context, private staffing peers report median gross margins near 25% publicly while Jackson's exact margins are undisclosed. This opacity makes it harder for external analysts and potential partners to assess solvency or valuation—private healthcare staffing deals in 2024 averaged EBITDA multiples of 8–12x, a benchmark Jackson's stakeholders cannot confirm openly. While privacy shields strategic data, it also constrains direct access to large capital markets—US IPO and follow-on equity raised $260 billion in 2024, funding scale Jackson cannot tap without going public or taking on costly alternatives.

Talent Acquisition Costs

The rising cost of recruiting and retaining clinical talent squeezes Jackson Healthcare’s margins: industry data show U.S. clinician turnover raises hiring spend ~20–30% and specialty locum costs rose 18% in 2024, forcing higher marketing and compensation outlays.

Competition for nurses and physicians, especially in specialties with <10% vacancy buffers, pushes acquisition costs higher and increases reliance on premium contracts and agency placements.

- Hiring spend up ~20–30% (turnover-driven)

- Specialty locum costs +18% in 2024

- Vacancy buffers <10% in key specialties

- Higher marketing and premium pay reduce margins

Dependency on Specific Clinical Segments

Jackson Healthcare relies heavily on high-demand segments like emergency medicine and nursing, where burnout rates exceed 40% in some studies and turnover can hit 20% annually, raising revenue volatility if supply drops or demand shifts.

Diversifying the provider mix is hard amid a 2024 U.S. clinician shortage estimated at 37,800 physicians and 1.1M nurses by 2030, so sector-specific shocks could disproportionately cut placements and fees.

- High burnout: >40% in emergency medicine

- Turnover: ~20% annually in nursing

- Projected shortages: 37,800 physicians by 2030

- Diversification remains operationally difficult

High U.S. Concentration, Rising Clinician Costs & Complex Structure Threaten Margins

Heavy U.S. concentration (90%+ revenue), limited international diversification, and exposure to Medicare/Medicaid shifts; complex 40+ subsidiary structure inflating SG&A (~28% vs peers ~22%) and reducing cross-sell (~12%); rising recruiting costs (turnover adds 20–30% hiring spend; specialty locum +18% in 2024) and clinician shortages (37,800 physicians, 1.1M nurses by 2030) raise margin and revenue volatility.

| Metric | Value |

|---|---|

| US revenue share | 90%+ |

| SG&A 2024 | ~28% |

| Cross-sell | ~12% |

| Locum cost change 2024 | +18% |

| Physician shortfall by 2030 | 37,800 |

Preview the Actual Deliverable

Jackson Healthcare SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete, editable file. You’re viewing a live preview of the exact analysis; the full, detailed version becomes available immediately after checkout.