Jana Bank Business Model Canvas

Jana Bank Business Model Canvas: Quick Strategic Playbook for Investors & Founders

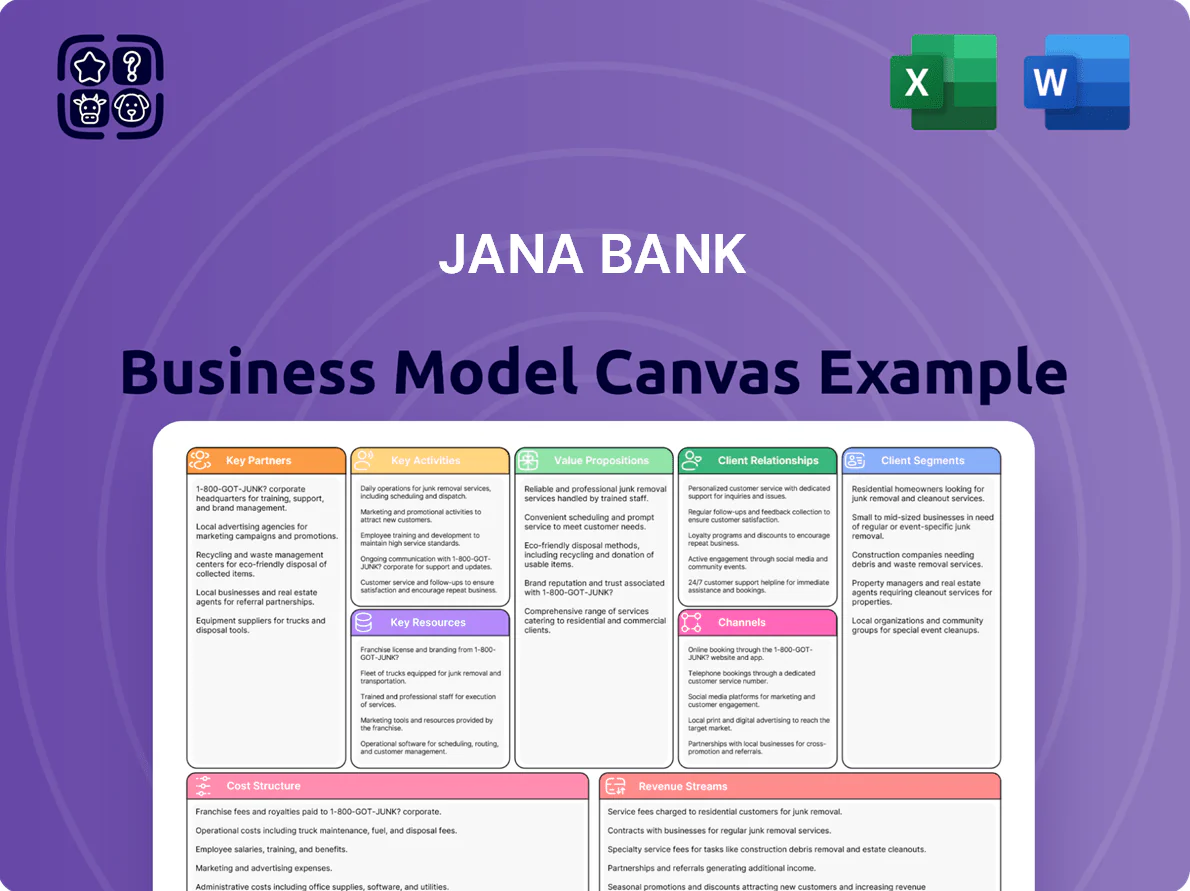

Unlock Jana Bank’s strategic playbook with our concise Business Model Canvas—see how its value propositions, channels, and revenue streams align to drive growth and competitive edge; perfect for investors, consultants, and founders who need a practical, ready-to-use framework. Purchase the full Canvas to get the complete nine-block breakdown, editable Word/Excel files, and actionable insights to benchmark or adapt the model to your strategy.

Partnerships

Strategic Banking Correspondents

Jana Small Finance Bank uses ~100,000 banking correspondents across India to reach rural and semi-urban customers, enabling ~60% of its new accounts in FY2024-25 via BC channels and reducing branch capex by an estimated 40%.

These local entrepreneurs and retail outlets perform KYC, account openings, deposits and withdrawals, handling over 25 million transactions monthly and extending the bank’s footprint without heavy physical investment.

Insurance and Third Party Providers

Jana Bank partners with top insurers and mutual fund houses—covering 12 insurers and 18 AMCs as of Dec 2025—to distribute microinsurance and SIP products, earning commission income (approx 18% of non-interest revenue in FY2024-25). These alliances give low-income customers access to risk protection and investment tools within one ecosystem, boosting cross-sell: partner products contributed 22% of new customer wallet share in 2025.

Technology and Fintech Collaborators

Jana Bank partners with fintechs and tech vendors for core banking, UPI rails, and mobile banking, enabling 99.9% uptime and sub-100ms payment latency; such ties cut time-to-market for features by ~40% and supported 12 million digital transactions/month in 2025.

Regulatory and Government Bodies

Maintaining strong ties with the Reserve Bank of India and other regulators ensures compliance and operational stability; Jana Bank met 100% of CRR/SLR requirements in 2025 and reported zero major compliance breaches to RBI in FY2024–25.

The bank partners with PMJDY and Ujjwala-linked schemes, directing 34% of new rural accounts to financial inclusion programs and claiming priority sector lending support worth ₹2.1 billion in FY2024–25.

- 100% CRR/SLR compliance (2025)

- 0 major RBI breaches reported (FY2024–25)

- 34% new rural accounts in inclusion schemes

- ₹2.1 billion priority sector support (FY2024–25)

Credit Bureaus and Data Analytics Firms

Collaborations with credit bureaus and data analytics firms let Jana Bank score first-time borrowers using alternative data; pilots in 2024 cut default rates by 18% for MSME loans versus traditional models.

Using device, payment, and utility data plus machine learning helps Jana reduce non-performing assets and protect microfinance portfolios; a 2025 internal model shows a projected NPA fall from 6.5% to 4.3%.

- 18% lower defaults in 2024 pilots

- NPA projection: 6.5% → 4.3% (2025 model)

- Alternative-data coverage: +35% of thin-file applicants

Jana Bank: 100K BCs, 60% new accounts, 18% partner revenue; NPA cut 6.5%→4.3%

Jana Bank leverages ~100,000 banking correspondents, 12 insurers, 18 AMCs, fintech vendors and credit bureaus to scale reach, drive 60% of new accounts via BCs (FY2024-25), earn ~18% of non-interest income from partner sales, and cut pilot loan defaults 18% (2024), projecting NPA drop 6.5%→4.3% (2025 model).

| Metric | Value |

|---|---|

| BCs | 100,000 |

| New accounts via BCs | 60% |

| Partner revenue | 18% |

| Default cut (pilot) | 18% |

| NPA projection | 6.5%→4.3% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Jana Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and governance—organized into 9 classic BMC blocks with competitive analysis, SWOT-linked insights, and polished narrative ideal for presentations, investor discussions, and strategic decision-making.

Clean, one-page Business Model Canvas that condenses Jana Bank’s strategy into an editable, shareable format—perfect for fast executive reviews, team collaboration, and saving hours on structuring internal or investor-facing deliverables.

Activities

Credit Underwriting and Loan Disbursement

Deposit Mobilization and Liability Management

Jana Bank mobilizes low-cost funding via savings, current, and fixed deposits—these accounted for 68% of liabilities in FY2024 (₹3,400bn of total deposits ₹5,000bn). Targeted marketing and relationship teams offer competitive rates (savings 3.5%–4.0%, 1-year FDs 6.5% in 2025) to retail and institutional savers.

Liability management focuses on maintaining LCR 135% (Q4 2024) and CASA 40% to ensure liquidity and sustainably fund a 12% loan book CAGR (2022–2024); stress tests guide tenor and repricing decisions.

Digital Transformation and Platform Maintenance

Jana Bank invests ~12% of annual IT spend (≈$18M in 2025) to keep mobile and internet channels live 24/7, cutting downtime to <0.5% and improving transaction throughput by 40% year-on-year; continuous software updates boost UX and security while training 3,200 staff and 45,000 rural customers in 2025 to drive cashless transactions in remote regions.

Financial Literacy and Community Outreach

Jana runs monthly financial-literacy workshops reaching ~12,000 underserved adults in 2025, teaching savings, budgeting, and credit basics to boost formal-account uptake by 18% year-over-year and cut new-loan default rates from 6.8% to 4.9%.

These programs build trust and loyalty, easing transitions from informal to formal finance and creating a more resilient local financial ecosystem.

- 12,000 people reached (2025)

- +18% formal-account uptake YoY

- Default rate drop 6.8% → 4.9%

- Monthly workshops and community events

Regulatory Compliance and Risk Management

The bank complies with Reserve Bank of India rules, keeping CRR at 4.0% and SLR at 18.0% as of Dec 2025, while internal audits and continuous risk assessments limit credit, market, and ops exposure to target NPL ratio under 2.5%.

High corporate governance standards, quarterly board oversight, and IFRS-aligned reporting sustain depositor and investor trust, supporting CET1-equivalent capital ratio near 12.5%.

- CRR 4.0% (Dec 2025)

- SLR 18.0% (Dec 2025)

- Target NPL <2.5%

- CET1-equivalent ~12.5%

- Quarterly audits & board oversight

Jana Bank: Fast 48h credit approvals, 24h disbursals, 3.8% default, strong liquidity

Jana Bank runs credit assessments (field + analytics) with 48h approvals, 3.8% default (2025); disburses in 24h via wallets/agents/transfers. Deposits = 68% liabilities (FY2024 ₹3,400bn of ₹5,000bn); CASA 40%, LCR 135% (Q4 2024). IT spend ≈$18M (2025), uptime >99.5%; outreach 12,000 adults (2025), +18% formal accounts YoY; CRR 4.0%, SLR 18.0% (Dec 2025), CET1 ~12.5%.

| Metric | Value |

|---|---|

| Approval time | ≤48h |

| Median disburse | 24h |

| Default rate (2025) | 3.8% |

| Deposits (FY2024) | ₹3,400bn (68%) |

| CASA | 40% |

| LCR (Q4 2024) | 135% |

| IT spend (2025) | $18M |

| Outreach (2025) | 12,000 people |

| Formal-account uplift | +18% YoY |

| CRR / SLR (Dec 2025) | 4.0% / 18.0% |

| CET1-equivalent | ~12.5% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Jana Bank Business Model Canvas you’ll receive—no mockups or samples. When you complete your purchase, you’ll get this exact, fully editable file ready for presentation, analysis, or customization in Word and Excel formats. What you see here reflects the final structure, content, and layout with no hidden pages or altered sections.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Jana Bank Business Model Canvas: Quick Strategic Playbook for Investors & Founders

Unlock Jana Bank’s strategic playbook with our concise Business Model Canvas—see how its value propositions, channels, and revenue streams align to drive growth and competitive edge; perfect for investors, consultants, and founders who need a practical, ready-to-use framework. Purchase the full Canvas to get the complete nine-block breakdown, editable Word/Excel files, and actionable insights to benchmark or adapt the model to your strategy.

Partnerships

Strategic Banking Correspondents

Jana Small Finance Bank uses ~100,000 banking correspondents across India to reach rural and semi-urban customers, enabling ~60% of its new accounts in FY2024-25 via BC channels and reducing branch capex by an estimated 40%.

These local entrepreneurs and retail outlets perform KYC, account openings, deposits and withdrawals, handling over 25 million transactions monthly and extending the bank’s footprint without heavy physical investment.

Insurance and Third Party Providers

Jana Bank partners with top insurers and mutual fund houses—covering 12 insurers and 18 AMCs as of Dec 2025—to distribute microinsurance and SIP products, earning commission income (approx 18% of non-interest revenue in FY2024-25). These alliances give low-income customers access to risk protection and investment tools within one ecosystem, boosting cross-sell: partner products contributed 22% of new customer wallet share in 2025.

Technology and Fintech Collaborators

Jana Bank partners with fintechs and tech vendors for core banking, UPI rails, and mobile banking, enabling 99.9% uptime and sub-100ms payment latency; such ties cut time-to-market for features by ~40% and supported 12 million digital transactions/month in 2025.

Regulatory and Government Bodies

Maintaining strong ties with the Reserve Bank of India and other regulators ensures compliance and operational stability; Jana Bank met 100% of CRR/SLR requirements in 2025 and reported zero major compliance breaches to RBI in FY2024–25.

The bank partners with PMJDY and Ujjwala-linked schemes, directing 34% of new rural accounts to financial inclusion programs and claiming priority sector lending support worth ₹2.1 billion in FY2024–25.

- 100% CRR/SLR compliance (2025)

- 0 major RBI breaches reported (FY2024–25)

- 34% new rural accounts in inclusion schemes

- ₹2.1 billion priority sector support (FY2024–25)

Credit Bureaus and Data Analytics Firms

Collaborations with credit bureaus and data analytics firms let Jana Bank score first-time borrowers using alternative data; pilots in 2024 cut default rates by 18% for MSME loans versus traditional models.

Using device, payment, and utility data plus machine learning helps Jana reduce non-performing assets and protect microfinance portfolios; a 2025 internal model shows a projected NPA fall from 6.5% to 4.3%.

- 18% lower defaults in 2024 pilots

- NPA projection: 6.5% → 4.3% (2025 model)

- Alternative-data coverage: +35% of thin-file applicants

Jana Bank: 100K BCs, 60% new accounts, 18% partner revenue; NPA cut 6.5%→4.3%

Jana Bank leverages ~100,000 banking correspondents, 12 insurers, 18 AMCs, fintech vendors and credit bureaus to scale reach, drive 60% of new accounts via BCs (FY2024-25), earn ~18% of non-interest income from partner sales, and cut pilot loan defaults 18% (2024), projecting NPA drop 6.5%→4.3% (2025 model).

| Metric | Value |

|---|---|

| BCs | 100,000 |

| New accounts via BCs | 60% |

| Partner revenue | 18% |

| Default cut (pilot) | 18% |

| NPA projection | 6.5%→4.3% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Jana Bank detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and governance—organized into 9 classic BMC blocks with competitive analysis, SWOT-linked insights, and polished narrative ideal for presentations, investor discussions, and strategic decision-making.

Clean, one-page Business Model Canvas that condenses Jana Bank’s strategy into an editable, shareable format—perfect for fast executive reviews, team collaboration, and saving hours on structuring internal or investor-facing deliverables.

Activities

Credit Underwriting and Loan Disbursement

Deposit Mobilization and Liability Management

Jana Bank mobilizes low-cost funding via savings, current, and fixed deposits—these accounted for 68% of liabilities in FY2024 (₹3,400bn of total deposits ₹5,000bn). Targeted marketing and relationship teams offer competitive rates (savings 3.5%–4.0%, 1-year FDs 6.5% in 2025) to retail and institutional savers.

Liability management focuses on maintaining LCR 135% (Q4 2024) and CASA 40% to ensure liquidity and sustainably fund a 12% loan book CAGR (2022–2024); stress tests guide tenor and repricing decisions.

Digital Transformation and Platform Maintenance

Jana Bank invests ~12% of annual IT spend (≈$18M in 2025) to keep mobile and internet channels live 24/7, cutting downtime to <0.5% and improving transaction throughput by 40% year-on-year; continuous software updates boost UX and security while training 3,200 staff and 45,000 rural customers in 2025 to drive cashless transactions in remote regions.

Financial Literacy and Community Outreach

Jana runs monthly financial-literacy workshops reaching ~12,000 underserved adults in 2025, teaching savings, budgeting, and credit basics to boost formal-account uptake by 18% year-over-year and cut new-loan default rates from 6.8% to 4.9%.

These programs build trust and loyalty, easing transitions from informal to formal finance and creating a more resilient local financial ecosystem.

- 12,000 people reached (2025)

- +18% formal-account uptake YoY

- Default rate drop 6.8% → 4.9%

- Monthly workshops and community events

Regulatory Compliance and Risk Management

The bank complies with Reserve Bank of India rules, keeping CRR at 4.0% and SLR at 18.0% as of Dec 2025, while internal audits and continuous risk assessments limit credit, market, and ops exposure to target NPL ratio under 2.5%.

High corporate governance standards, quarterly board oversight, and IFRS-aligned reporting sustain depositor and investor trust, supporting CET1-equivalent capital ratio near 12.5%.

- CRR 4.0% (Dec 2025)

- SLR 18.0% (Dec 2025)

- Target NPL <2.5%

- CET1-equivalent ~12.5%

- Quarterly audits & board oversight

Jana Bank: Fast 48h credit approvals, 24h disbursals, 3.8% default, strong liquidity

Jana Bank runs credit assessments (field + analytics) with 48h approvals, 3.8% default (2025); disburses in 24h via wallets/agents/transfers. Deposits = 68% liabilities (FY2024 ₹3,400bn of ₹5,000bn); CASA 40%, LCR 135% (Q4 2024). IT spend ≈$18M (2025), uptime >99.5%; outreach 12,000 adults (2025), +18% formal accounts YoY; CRR 4.0%, SLR 18.0% (Dec 2025), CET1 ~12.5%.

| Metric | Value |

|---|---|

| Approval time | ≤48h |

| Median disburse | 24h |

| Default rate (2025) | 3.8% |

| Deposits (FY2024) | ₹3,400bn (68%) |

| CASA | 40% |

| LCR (Q4 2024) | 135% |

| IT spend (2025) | $18M |

| Outreach (2025) | 12,000 people |

| Formal-account uplift | +18% YoY |

| CRR / SLR (Dec 2025) | 4.0% / 18.0% |

| CET1-equivalent | ~12.5% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Jana Bank Business Model Canvas you’ll receive—no mockups or samples. When you complete your purchase, you’ll get this exact, fully editable file ready for presentation, analysis, or customization in Word and Excel formats. What you see here reflects the final structure, content, and layout with no hidden pages or altered sections.