J.B. Hunt Transport Services Porter's Five Forces Analysis

From Overview to Strategy Blueprint

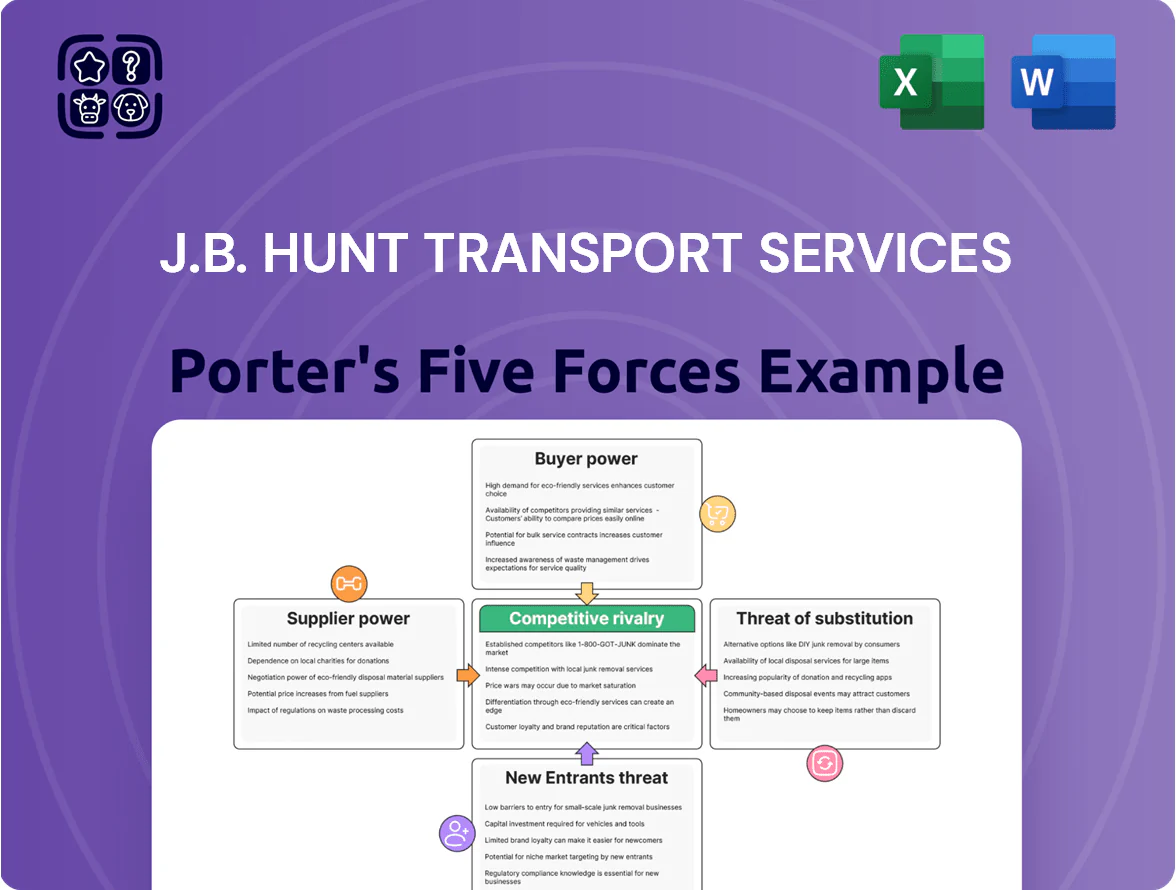

J.B. Hunt faces moderate supplier power, intense rivalry among large carriers, and rising buyer demands for integrated logistics—while asset-light entrants and tech-enabled substitutes inch into the market, pressuring margins and innovation cycles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore J.B. Hunt Transport Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Class I Railroads

J.B. Hunt depends heavily on Class I railroads—notably BNSF and Norfolk Southern—for Intermodal operations, with these carriers controlling pricing due to just seven U.S. Class I railroads and high fixed infrastructure costs.

In 2024 intermodal revenue represented ~36% of J.B. Hunt’s $14.8B total revenue, so a 5% rail rate hike could raise costs by ~0.9% of revenue, squeezing margins.

Service disruptions—like the 2022 national rail strike threats that briefly cut network capacity—directly harm reliability and can force short-term truck substitution at higher cost.

Equipment and Vehicle Manufacturers

J.B. Hunt depends on a few global makers for tractors, trailers and containers, so supplier disruptions or raw-material inflation (steel up ~20% in 2021–23) can raise fleet capex; company disclosed $1.9bn in capex for 2024 guidance toward equipment renewal.

Energy and Fuel Providers

Fluctuations in diesel—up 38% from 2020 to 2022 and averaging about $3.60/gal in 2024—pose major operational risk largely set by global oil markets; J.B. Hunt offsets this with fuel surcharge programs but remains exposed to supplier pricing moves.

Adopting electric and alternative-fuel trucks (J.B. Hunt ordered 5,000 EVs in 2023) shifts dependence to battery, charging, and hydrogen infrastructure providers, creating new supplier concentration and technology risk.

Labor Market and Driver Supply

The tight U.S. market for qualified commercial drivers drives wage inflation and higher recruitment costs; ATA data showed 2024 driver turnover averaged ~80% for for-hire carriers, pushing average pay up 8–12% year-over-year.

Professional drivers have leverage, forcing J.B. Hunt to boost pay and benefits—J.B. Hunt reported 2024 driver-related labor expense growth of about mid-teens percent, squeezing margins.

J.B. Hunt leans on Dedicated Contract Services to offer predictable schedules and higher retention; DCS yields lower turnover (reported ~30–40% vs. industry 80%), reducing per-driver hiring costs and stabilizing capacity.

- Driver turnover: industry ~80% (2024)

- J.B. Hunt DCS turnover: ~30–40%

- Driver pay growth: 8–12% (2024)

- Driver labor expense: mid-teens % growth for J.B. Hunt (2024)

Technology and Software Vendors

As J.B. Hunt shifts freight management onto J.B. Hunt 360, reliance on telematics, cloud, and AI vendors rises; third-party software now underpins routing and visibility, creating exposure to subscription hikes and outages.

In 2025 J.B. Hunt reported technology and digital revenue investments growing ~12% year-over-year, so keeping more proprietary capabilities or multi-vendor contracts is key to limit cost and operational risk.

- Dependency: third-party vendors power J.B. Hunt 360

- Risk: subscription inflation and outages affect ops

- Mitigation: build proprietary tech, diversify vendors

- 2025 signal: tech spending up ~12% YoY

Suppliers Hold the Levers: Intermodal 36%, $1.9B Capex, Rising Fuel/Steel & EV Vendor Risk

Suppliers wield significant power: seven Class I railroads control intermodal pricing (36% of 2024 revenue), diesel averaged ~$3.60/gal (2024), steel rose ~20% (2021–23), and driver turnover hit ~80% industry (2024) vs J.B. Hunt DCS 30–40%; 2024 capex guidance $1.9bn; EV orders 5,000 (2023) shift dependence to battery/charging vendors.

| Metric | Value |

|---|---|

| Intermodal share | 36% (2024) |

| Diesel | $3.60/gal (2024) |

| Capex | $1.9bn (2024) |

What is included in the product

Tailored exclusively for J.B. Hunt Transport Services, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitute threats, and emergent disruptors shaping its pricing power and profitability.

Concise Porter's Five Forces snapshot for J.B. Hunt—quickly spot carrier bargaining shifts, modal substitution risks, and regulatory pressure to inform routing and pricing decisions.

Customers Bargaining Power

Concentration of Large Retail Clients

A large share of J.B. Hunt Transport Services revenue comes from big shippers—Walmart and other Fortune 500 retailers—giving customers strong bargaining power; in 2024 shippers accounted for roughly 40–50% of contract freight revenue, enabling steep rate pressure and strict SLAs. Losing one major account could cut annual revenue materially—J.B. Hunt reported $14.2 billion revenue in 2024, so a single large contract loss could swing hundreds of millions.

Availability of Competitive Bidding

The rise of digital freight brokerages lets shippers compare rates from dozens of carriers in seconds, and in 2024 digital tender acceptance rose to ~35% of U.S. truckload volumes, increasing price transparency.

Large shippers run annual competitive bids that compressed average contracted TL rates by ~4–6% YoY in 2023–24, putting downward pressure on J.B. Hunt’s margins.

J.B. Hunt must show superior reliability and tech—like its 2024 TMC and J.B. Hunt 360 platform, which handled >1.2M loads in 2024—to keep customers from switching to lower-cost providers.

Low Switching Costs in Truckload

Low switching costs in J.B. Hunt's truckload and brokerage segments mean customers can move providers easily, keeping price as a key battleground; commodity truckload rates fell ~3% YoY in 2024, pressuring margins. Integrated logistics like Integrated Capacity Solutions add stickiness—J.B. Hunt reported 2024 revenue of $14.5B with Final Mile and Dedicated Contract Services growing double digits, which the company pushes to raise customer integration and reduce churn.

Demand for Integrated Supply Chain Solutions

Sophisticated shippers now favor end-to-end logistics over point-to-point moves, boosting demand for J.B. Hunt’s intermodal, dedicated, final-mile, and 3PL services; J.B. Hunt reported 2025 contract logistics revenue of $3.2 billion, showing strength in integrated offerings.

This gives J.B. Hunt an edge through cross-service margins and client stickiness, but it raises performance expectations—missed SLAs or inventory errors risk losing an entire account to full-service rivals like XPO or DHL Supply Chain.

- 2025 contract logistics revenue $3.2B

- Integrated services increase switching cost

- Poor performance risks full-account loss

- Competitors: XPO, DHL, Kuehne+Nagel

Economic Sensitivity of Shippers

During downturns shippers cut volumes and push for lower rates; in 2023 US truckload demand fell ~3.5% and spot rates dropped ~22% year-over-year, raising customer leverage.

Excess capacity—US for-hire truck capacity grew ~4% in 2024—lets large shippers dictate terms; J.B. Hunt offsets this by spreading revenue across retail, auto, food, and e-commerce, with 2024 intermodal and dedicated segments contributing ~60% of total revenue.

- Shipper price sensitivity rises in recessions

- Excess capacity increases buyer leverage

- J.B. Hunt diversification: intermodal, dedicated, 60% revenue

- 2023–24: spot rates down ~22%, capacity +4%

Large shippers squeeze rates as digital tenders rise; $14.2B firm faces contract risk

Large shippers (Walmart, Fortune 500) drive strong bargaining power—2024 revenue $14.2B; losing one major account could swing hundreds of millions. Digital brokers raised price transparency (digital tenders ~35% of truckload 2024). Low switching costs compress TL rates (~4–6% contracted decline in 2023–24); integrated services (2025 contract logistics $3.2B) add some stickiness but raise performance risk.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.2B |

| Contract logistics 2025 | $3.2B |

| Digital tenders 2024 | ~35% |

| Contract rate change 2023–24 | -4–6% |

Same Document Delivered

J.B. Hunt Transport Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of J.B. Hunt Transport Services you'll receive immediately after purchase—no placeholders or mockups; the complete, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

J.B. Hunt faces moderate supplier power, intense rivalry among large carriers, and rising buyer demands for integrated logistics—while asset-light entrants and tech-enabled substitutes inch into the market, pressuring margins and innovation cycles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore J.B. Hunt Transport Services’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Class I Railroads

J.B. Hunt depends heavily on Class I railroads—notably BNSF and Norfolk Southern—for Intermodal operations, with these carriers controlling pricing due to just seven U.S. Class I railroads and high fixed infrastructure costs.

In 2024 intermodal revenue represented ~36% of J.B. Hunt’s $14.8B total revenue, so a 5% rail rate hike could raise costs by ~0.9% of revenue, squeezing margins.

Service disruptions—like the 2022 national rail strike threats that briefly cut network capacity—directly harm reliability and can force short-term truck substitution at higher cost.

Equipment and Vehicle Manufacturers

J.B. Hunt depends on a few global makers for tractors, trailers and containers, so supplier disruptions or raw-material inflation (steel up ~20% in 2021–23) can raise fleet capex; company disclosed $1.9bn in capex for 2024 guidance toward equipment renewal.

Energy and Fuel Providers

Fluctuations in diesel—up 38% from 2020 to 2022 and averaging about $3.60/gal in 2024—pose major operational risk largely set by global oil markets; J.B. Hunt offsets this with fuel surcharge programs but remains exposed to supplier pricing moves.

Adopting electric and alternative-fuel trucks (J.B. Hunt ordered 5,000 EVs in 2023) shifts dependence to battery, charging, and hydrogen infrastructure providers, creating new supplier concentration and technology risk.

Labor Market and Driver Supply

The tight U.S. market for qualified commercial drivers drives wage inflation and higher recruitment costs; ATA data showed 2024 driver turnover averaged ~80% for for-hire carriers, pushing average pay up 8–12% year-over-year.

Professional drivers have leverage, forcing J.B. Hunt to boost pay and benefits—J.B. Hunt reported 2024 driver-related labor expense growth of about mid-teens percent, squeezing margins.

J.B. Hunt leans on Dedicated Contract Services to offer predictable schedules and higher retention; DCS yields lower turnover (reported ~30–40% vs. industry 80%), reducing per-driver hiring costs and stabilizing capacity.

- Driver turnover: industry ~80% (2024)

- J.B. Hunt DCS turnover: ~30–40%

- Driver pay growth: 8–12% (2024)

- Driver labor expense: mid-teens % growth for J.B. Hunt (2024)

Technology and Software Vendors

As J.B. Hunt shifts freight management onto J.B. Hunt 360, reliance on telematics, cloud, and AI vendors rises; third-party software now underpins routing and visibility, creating exposure to subscription hikes and outages.

In 2025 J.B. Hunt reported technology and digital revenue investments growing ~12% year-over-year, so keeping more proprietary capabilities or multi-vendor contracts is key to limit cost and operational risk.

- Dependency: third-party vendors power J.B. Hunt 360

- Risk: subscription inflation and outages affect ops

- Mitigation: build proprietary tech, diversify vendors

- 2025 signal: tech spending up ~12% YoY

Suppliers Hold the Levers: Intermodal 36%, $1.9B Capex, Rising Fuel/Steel & EV Vendor Risk

Suppliers wield significant power: seven Class I railroads control intermodal pricing (36% of 2024 revenue), diesel averaged ~$3.60/gal (2024), steel rose ~20% (2021–23), and driver turnover hit ~80% industry (2024) vs J.B. Hunt DCS 30–40%; 2024 capex guidance $1.9bn; EV orders 5,000 (2023) shift dependence to battery/charging vendors.

| Metric | Value |

|---|---|

| Intermodal share | 36% (2024) |

| Diesel | $3.60/gal (2024) |

| Capex | $1.9bn (2024) |

What is included in the product

Tailored exclusively for J.B. Hunt Transport Services, this Porter’s Five Forces overview uncovers competitive drivers, buyer and supplier influence, entry barriers, substitute threats, and emergent disruptors shaping its pricing power and profitability.

Concise Porter's Five Forces snapshot for J.B. Hunt—quickly spot carrier bargaining shifts, modal substitution risks, and regulatory pressure to inform routing and pricing decisions.

Customers Bargaining Power

Concentration of Large Retail Clients

A large share of J.B. Hunt Transport Services revenue comes from big shippers—Walmart and other Fortune 500 retailers—giving customers strong bargaining power; in 2024 shippers accounted for roughly 40–50% of contract freight revenue, enabling steep rate pressure and strict SLAs. Losing one major account could cut annual revenue materially—J.B. Hunt reported $14.2 billion revenue in 2024, so a single large contract loss could swing hundreds of millions.

Availability of Competitive Bidding

The rise of digital freight brokerages lets shippers compare rates from dozens of carriers in seconds, and in 2024 digital tender acceptance rose to ~35% of U.S. truckload volumes, increasing price transparency.

Large shippers run annual competitive bids that compressed average contracted TL rates by ~4–6% YoY in 2023–24, putting downward pressure on J.B. Hunt’s margins.

J.B. Hunt must show superior reliability and tech—like its 2024 TMC and J.B. Hunt 360 platform, which handled >1.2M loads in 2024—to keep customers from switching to lower-cost providers.

Low Switching Costs in Truckload

Low switching costs in J.B. Hunt's truckload and brokerage segments mean customers can move providers easily, keeping price as a key battleground; commodity truckload rates fell ~3% YoY in 2024, pressuring margins. Integrated logistics like Integrated Capacity Solutions add stickiness—J.B. Hunt reported 2024 revenue of $14.5B with Final Mile and Dedicated Contract Services growing double digits, which the company pushes to raise customer integration and reduce churn.

Demand for Integrated Supply Chain Solutions

Sophisticated shippers now favor end-to-end logistics over point-to-point moves, boosting demand for J.B. Hunt’s intermodal, dedicated, final-mile, and 3PL services; J.B. Hunt reported 2025 contract logistics revenue of $3.2 billion, showing strength in integrated offerings.

This gives J.B. Hunt an edge through cross-service margins and client stickiness, but it raises performance expectations—missed SLAs or inventory errors risk losing an entire account to full-service rivals like XPO or DHL Supply Chain.

- 2025 contract logistics revenue $3.2B

- Integrated services increase switching cost

- Poor performance risks full-account loss

- Competitors: XPO, DHL, Kuehne+Nagel

Economic Sensitivity of Shippers

During downturns shippers cut volumes and push for lower rates; in 2023 US truckload demand fell ~3.5% and spot rates dropped ~22% year-over-year, raising customer leverage.

Excess capacity—US for-hire truck capacity grew ~4% in 2024—lets large shippers dictate terms; J.B. Hunt offsets this by spreading revenue across retail, auto, food, and e-commerce, with 2024 intermodal and dedicated segments contributing ~60% of total revenue.

- Shipper price sensitivity rises in recessions

- Excess capacity increases buyer leverage

- J.B. Hunt diversification: intermodal, dedicated, 60% revenue

- 2023–24: spot rates down ~22%, capacity +4%

Large shippers squeeze rates as digital tenders rise; $14.2B firm faces contract risk

Large shippers (Walmart, Fortune 500) drive strong bargaining power—2024 revenue $14.2B; losing one major account could swing hundreds of millions. Digital brokers raised price transparency (digital tenders ~35% of truckload 2024). Low switching costs compress TL rates (~4–6% contracted decline in 2023–24); integrated services (2025 contract logistics $3.2B) add some stickiness but raise performance risk.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.2B |

| Contract logistics 2025 | $3.2B |

| Digital tenders 2024 | ~35% |

| Contract rate change 2023–24 | -4–6% |

Same Document Delivered

J.B. Hunt Transport Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of J.B. Hunt Transport Services you'll receive immediately after purchase—no placeholders or mockups; the complete, professionally formatted document is ready for download and use the moment you buy.