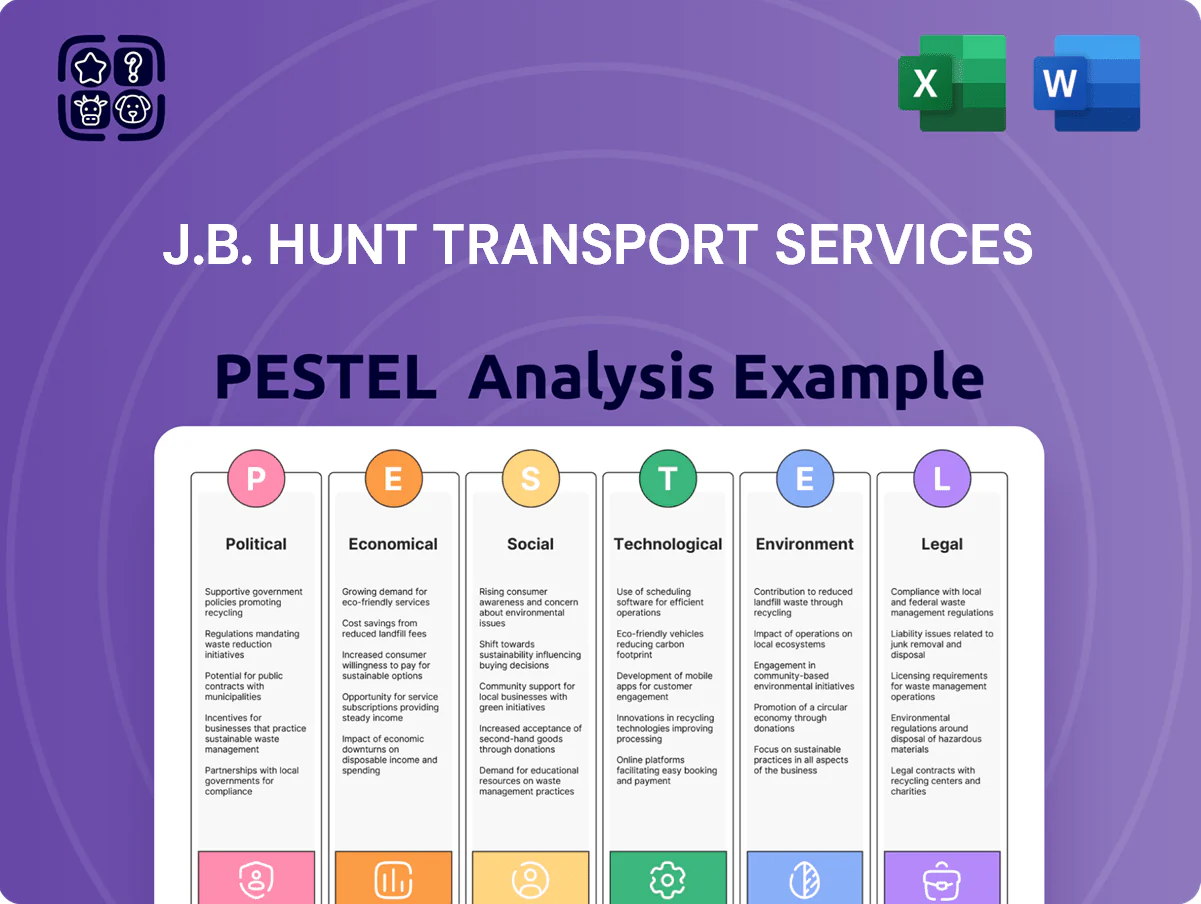

J.B. Hunt Transport Services PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of J.B. Hunt Transport Services reveals how regulatory shifts, fuel price volatility, labor dynamics, technological disruption, and sustainability pressures converge to reshape logistics margins and growth prospects—insights that can sharpen your investment or strategic playbook. Purchase the full report to access detailed drivers, quantified risks, and ready-to-use strategic recommendations for immediate impact.

Political factors

Trade Policy and Tariffs

Trade relations among the US, Mexico and Canada drive J.B. Hunt’s cross-border volumes—USMCA-linked trade totaled about $1.7 trillion in 2023, and roughly 20% of J.B. Hunt’s revenue in 2024 was exposed to cross-border freight lanes.

Protectionist measures or changes to USMCA rules could shift manufacturing and reroute supply chains, altering demand for intermodal and truckload services.

Analysts track tariff risks and geopolitical developments closely because a 10% decline in cross-border trade could materially compress J.B. Hunt’s border lane utilization and margins.

Infrastructure Spending Legislation

Federal infrastructure bills allocating roughly 200 billion USD for highways and rail over 2022–2026 and recent USD 17 billion in port grants directly boost J.B. Hunt’s efficiency by improving highway maintenance and intermodal rail hubs used in its 2025 network; better roads reduce vehicle wear and detention.

Taxation and Fiscal Policy

Corporate tax rate changes and investment tax credits for fleet renewal directly affect J.B. Hunt’s capex plans and net margin: a 1% change in US federal rate can alter cash taxes materially for a company reporting $4.9 billion revenue in 2024, while accelerated depreciation/EV credits reduce effective costs of replacing tractors. Fiscal shifts like higher federal/state fuel taxes or a $50/ton carbon price would raise operating costs, forcing pricing or efficiency adjustments to protect margins. Management must track divergent state incentives—e.g., Washington, California grants for zero-emission trucks—to optimize site-level investment and capture rebates that lower total cost of ownership.

Labor Union Regulations

Political shifts on collective bargaining and worker classification can raise J.B. Hunt's operating costs; for example, a 2024 NLRB review and state bills could affect ~40% of industry capacity driven by independent contractors.

J.B. Hunt's mix of independent contractors and company drivers means federal labor rulings change competitive dynamics and labor expense forecasts.

Ongoing legislative efforts to reclassify workers require continuous legal monitoring to protect margins—driver W-2 conversion scenarios could add 10–20% to labor-related costs.

- Labor rulings affect cost structure and capacity (~40% contractor-driven)

- Federal/state bills influence competitive landscape and margins

- W-2 conversion could increase labor costs by 10–20%

- Continuous legal/operational monitoring required

International Relations and Security

Global geopolitical tensions drive oil volatility—Brent averaged about 86 USD/barrel in 2024, pressuring J.B. Hunt's diesel costs and squeezing retail/manufacturing demand that account for a large portion of its revenue.

Border and port security requirements from agencies like CBP and TSA add dwell-time and compliance costs, raising per-shipment expenses and reducing throughput.

Instability in manufacturing hubs (e.g., occasional 2024 disruptions in Red Sea shipping lanes) causes supply-chain reroutes that create short-term spikes and dips in domestic freight volumes for J.B. Hunt.

- Brent ~86 USD/barrel (2024) increases fuel expense.

- Enhanced border/port security raises dwell-time and costs.

- Red Sea/other hub disruptions in 2024 led to volatile domestic freight demand.

J.B. Hunt: Trade exposure, infrastructure tailwinds, fuel & labor cost risks

Political factors affecting J.B. Hunt include USMCA trade exposure (~20% of 2024 revenue), federal infrastructure funding (~$200B 2022–26 + $17B port grants), Brent oil ~86 USD/bbl (2024) impacting diesel costs, labor rule risks (W-2 conversion could raise labor costs 10–20%), and regulatory compliance/dwell-time from border/port security.

| Metric | Value |

|---|---|

| Cross-border revenue exposure | ~20% (2024) |

| Infrastructure funding | ~$200B (2022–26) |

| Brent (avg) | $86/bbl (2024) |

| W-2 cost impact | +10–20% |

What is included in the product

Explores how external macro-environmental factors uniquely affect J.B. Hunt Transport Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a concise, visually segmented PESTLE summary for J.B. Hunt that’s easy to drop into presentations or share across teams, helping align stakeholders quickly on external risks and market positioning.

Economic factors

GDP Growth and Consumer Spending

Demand for freight services closely tracks North American GDP and retail sales; US GDP grew 2.4% in 2024 and retail sales rose 4.1% year-over-year, supporting volumes for carriers like J.B. Hunt.

As a primary carrier for major retailers, J.B. Hunt’s 2024 revenue of $14.6 billion reflected sensitivity to consumer purchasing power and inventory restocking cycles.

Economic expansions boost Intermodal and Final Mile demand—J.B. Hunt reported Intermodal revenue up 6% and Final Mile volumes increasing in 2024 as e-commerce sales continued to expand.

Fuel Price Volatility

Fluctuations in U.S. diesel prices—averaging about 4.05 USD/gal in 2024 and volatile month-to-month—represent a sizable variable cost that can erode J.B. Hunt's operating margin if not fully offset by fuel surcharges.

J.B. Hunt deploys dynamic surcharge programs and fuel hedges to mitigate risk, yet rapid spikes (e.g., 2022–2023 peaks) can cause short-term pressure on operating income and cash flow.

Long-term trends—U.S. crude production growth, renewables adoption, and potential biofuel mandates—affect total cost of ownership across J.B. Hunt's ~30,000-vehicle fleet and capital planning.

Interest Rates and Cost of Capital

The late-2025 rise in U.S. policy rates (Fed funds target ~5.25–5.50%) increased J.B. Hunt’s cost of capital, raising borrowing costs for equipment and terminal expansion; higher rates contributed to 2025 interest expense pressures after net interest-bearing debt of $1.8B reported in FY2024. Elevated rates can slow fleet modernization and acquisitions, and investors monitor Fed moves closely given logistics’ capital intensity.

Labor Market Tightness

Shortages of qualified truck drivers drive wage inflation and higher recruitment costs; trucking industry average turnover was 82% in 2024, pushing median driver pay up about 12% year-over-year and increasing J.B. Hunt’s labor expense pressure.

J.B. Hunt’s ability to attract and retain drivers and warehouse staff—critical to its intermodal and dedicated fleet capacity—depends on competitive pay, benefits, and training amid a 2024 US unemployment rate of ~3.7% that tightens labor supply.

- Driver shortage → industry turnover 82% (2024)

- Median driver pay +12% YoY (2024)

- US unemployment ~3.7% (2024) → tighter labor pool

- Recruitment & retention key to J.B. Hunt operational capacity

E-commerce Market Penetration

The ongoing shift to online shopping—U.S. e-commerce sales reached about 15.3% of total retail sales in 2024 (~$1.1 trillion)—boosts demand for specialized delivery and final-mile services, benefiting J.B. Hunt’s Final Mile segment.

Meeting this requires investment in diverse fleet assets and localized distribution centers; J.B. Hunt reported expanding final-mile capacity in 2024, adding routes and partnerships to capture rising volume.

E-commerce growth represents a durable tailwind for revenue mix and utilization in Final Mile Services, supporting long-term margin and network scale gains.

- U.S. e-commerce ~15.3% of retail in 2024 (~$1.1T)

- J.B. Hunt expanded final-mile capacity, 2024 route/partner growth

- Higher demand necessitates varied equipment and local hubs

- Long-term tailwind for Final Mile revenue and utilization

J.B. Hunt Grows to $14.6B in 2024 as Costs, Driver Turnover and Rates Squeeze Margins

Economic growth, with US GDP +2.4% and retail sales +4.1% in 2024, supported J.B. Hunt’s $14.6B revenue; intermodal +6% and Final Mile volumes rose. Diesel averaged $4.05/gal in 2024, pressuring margins despite surcharges; net debt $1.8B (FY2024) and Fed rates ~5.25–5.50% raised cost of capital. Driver turnover 82% and median pay +12% (2024) tightened capacity; e-commerce =15.3% of retail (~$1.1T).

| Metric | 2024 |

|---|---|

| Revenue | $14.6B |

| Intermodal rev | +6% |

| Diesel | $4.05/gal |

| Net debt | $1.8B |

| Driver turnover | 82% |

Preview Before You Purchase

J.B. Hunt Transport Services PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This J.B. Hunt Transport Services PESTLE analysis covers political, economic, social, technological, legal, and environmental factors affecting the company, with concise insights and implications for strategy. No placeholders or teasers—what you see is the final, downloadable file. Ready for immediate use after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of J.B. Hunt Transport Services reveals how regulatory shifts, fuel price volatility, labor dynamics, technological disruption, and sustainability pressures converge to reshape logistics margins and growth prospects—insights that can sharpen your investment or strategic playbook. Purchase the full report to access detailed drivers, quantified risks, and ready-to-use strategic recommendations for immediate impact.

Political factors

Trade Policy and Tariffs

Trade relations among the US, Mexico and Canada drive J.B. Hunt’s cross-border volumes—USMCA-linked trade totaled about $1.7 trillion in 2023, and roughly 20% of J.B. Hunt’s revenue in 2024 was exposed to cross-border freight lanes.

Protectionist measures or changes to USMCA rules could shift manufacturing and reroute supply chains, altering demand for intermodal and truckload services.

Analysts track tariff risks and geopolitical developments closely because a 10% decline in cross-border trade could materially compress J.B. Hunt’s border lane utilization and margins.

Infrastructure Spending Legislation

Federal infrastructure bills allocating roughly 200 billion USD for highways and rail over 2022–2026 and recent USD 17 billion in port grants directly boost J.B. Hunt’s efficiency by improving highway maintenance and intermodal rail hubs used in its 2025 network; better roads reduce vehicle wear and detention.

Taxation and Fiscal Policy

Corporate tax rate changes and investment tax credits for fleet renewal directly affect J.B. Hunt’s capex plans and net margin: a 1% change in US federal rate can alter cash taxes materially for a company reporting $4.9 billion revenue in 2024, while accelerated depreciation/EV credits reduce effective costs of replacing tractors. Fiscal shifts like higher federal/state fuel taxes or a $50/ton carbon price would raise operating costs, forcing pricing or efficiency adjustments to protect margins. Management must track divergent state incentives—e.g., Washington, California grants for zero-emission trucks—to optimize site-level investment and capture rebates that lower total cost of ownership.

Labor Union Regulations

Political shifts on collective bargaining and worker classification can raise J.B. Hunt's operating costs; for example, a 2024 NLRB review and state bills could affect ~40% of industry capacity driven by independent contractors.

J.B. Hunt's mix of independent contractors and company drivers means federal labor rulings change competitive dynamics and labor expense forecasts.

Ongoing legislative efforts to reclassify workers require continuous legal monitoring to protect margins—driver W-2 conversion scenarios could add 10–20% to labor-related costs.

- Labor rulings affect cost structure and capacity (~40% contractor-driven)

- Federal/state bills influence competitive landscape and margins

- W-2 conversion could increase labor costs by 10–20%

- Continuous legal/operational monitoring required

International Relations and Security

Global geopolitical tensions drive oil volatility—Brent averaged about 86 USD/barrel in 2024, pressuring J.B. Hunt's diesel costs and squeezing retail/manufacturing demand that account for a large portion of its revenue.

Border and port security requirements from agencies like CBP and TSA add dwell-time and compliance costs, raising per-shipment expenses and reducing throughput.

Instability in manufacturing hubs (e.g., occasional 2024 disruptions in Red Sea shipping lanes) causes supply-chain reroutes that create short-term spikes and dips in domestic freight volumes for J.B. Hunt.

- Brent ~86 USD/barrel (2024) increases fuel expense.

- Enhanced border/port security raises dwell-time and costs.

- Red Sea/other hub disruptions in 2024 led to volatile domestic freight demand.

J.B. Hunt: Trade exposure, infrastructure tailwinds, fuel & labor cost risks

Political factors affecting J.B. Hunt include USMCA trade exposure (~20% of 2024 revenue), federal infrastructure funding (~$200B 2022–26 + $17B port grants), Brent oil ~86 USD/bbl (2024) impacting diesel costs, labor rule risks (W-2 conversion could raise labor costs 10–20%), and regulatory compliance/dwell-time from border/port security.

| Metric | Value |

|---|---|

| Cross-border revenue exposure | ~20% (2024) |

| Infrastructure funding | ~$200B (2022–26) |

| Brent (avg) | $86/bbl (2024) |

| W-2 cost impact | +10–20% |

What is included in the product

Explores how external macro-environmental factors uniquely affect J.B. Hunt Transport Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a concise, visually segmented PESTLE summary for J.B. Hunt that’s easy to drop into presentations or share across teams, helping align stakeholders quickly on external risks and market positioning.

Economic factors

GDP Growth and Consumer Spending

Demand for freight services closely tracks North American GDP and retail sales; US GDP grew 2.4% in 2024 and retail sales rose 4.1% year-over-year, supporting volumes for carriers like J.B. Hunt.

As a primary carrier for major retailers, J.B. Hunt’s 2024 revenue of $14.6 billion reflected sensitivity to consumer purchasing power and inventory restocking cycles.

Economic expansions boost Intermodal and Final Mile demand—J.B. Hunt reported Intermodal revenue up 6% and Final Mile volumes increasing in 2024 as e-commerce sales continued to expand.

Fuel Price Volatility

Fluctuations in U.S. diesel prices—averaging about 4.05 USD/gal in 2024 and volatile month-to-month—represent a sizable variable cost that can erode J.B. Hunt's operating margin if not fully offset by fuel surcharges.

J.B. Hunt deploys dynamic surcharge programs and fuel hedges to mitigate risk, yet rapid spikes (e.g., 2022–2023 peaks) can cause short-term pressure on operating income and cash flow.

Long-term trends—U.S. crude production growth, renewables adoption, and potential biofuel mandates—affect total cost of ownership across J.B. Hunt's ~30,000-vehicle fleet and capital planning.

Interest Rates and Cost of Capital

The late-2025 rise in U.S. policy rates (Fed funds target ~5.25–5.50%) increased J.B. Hunt’s cost of capital, raising borrowing costs for equipment and terminal expansion; higher rates contributed to 2025 interest expense pressures after net interest-bearing debt of $1.8B reported in FY2024. Elevated rates can slow fleet modernization and acquisitions, and investors monitor Fed moves closely given logistics’ capital intensity.

Labor Market Tightness

Shortages of qualified truck drivers drive wage inflation and higher recruitment costs; trucking industry average turnover was 82% in 2024, pushing median driver pay up about 12% year-over-year and increasing J.B. Hunt’s labor expense pressure.

J.B. Hunt’s ability to attract and retain drivers and warehouse staff—critical to its intermodal and dedicated fleet capacity—depends on competitive pay, benefits, and training amid a 2024 US unemployment rate of ~3.7% that tightens labor supply.

- Driver shortage → industry turnover 82% (2024)

- Median driver pay +12% YoY (2024)

- US unemployment ~3.7% (2024) → tighter labor pool

- Recruitment & retention key to J.B. Hunt operational capacity

E-commerce Market Penetration

The ongoing shift to online shopping—U.S. e-commerce sales reached about 15.3% of total retail sales in 2024 (~$1.1 trillion)—boosts demand for specialized delivery and final-mile services, benefiting J.B. Hunt’s Final Mile segment.

Meeting this requires investment in diverse fleet assets and localized distribution centers; J.B. Hunt reported expanding final-mile capacity in 2024, adding routes and partnerships to capture rising volume.

E-commerce growth represents a durable tailwind for revenue mix and utilization in Final Mile Services, supporting long-term margin and network scale gains.

- U.S. e-commerce ~15.3% of retail in 2024 (~$1.1T)

- J.B. Hunt expanded final-mile capacity, 2024 route/partner growth

- Higher demand necessitates varied equipment and local hubs

- Long-term tailwind for Final Mile revenue and utilization

J.B. Hunt Grows to $14.6B in 2024 as Costs, Driver Turnover and Rates Squeeze Margins

Economic growth, with US GDP +2.4% and retail sales +4.1% in 2024, supported J.B. Hunt’s $14.6B revenue; intermodal +6% and Final Mile volumes rose. Diesel averaged $4.05/gal in 2024, pressuring margins despite surcharges; net debt $1.8B (FY2024) and Fed rates ~5.25–5.50% raised cost of capital. Driver turnover 82% and median pay +12% (2024) tightened capacity; e-commerce =15.3% of retail (~$1.1T).

| Metric | 2024 |

|---|---|

| Revenue | $14.6B |

| Intermodal rev | +6% |

| Diesel | $4.05/gal |

| Net debt | $1.8B |

| Driver turnover | 82% |

Preview Before You Purchase

J.B. Hunt Transport Services PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This J.B. Hunt Transport Services PESTLE analysis covers political, economic, social, technological, legal, and environmental factors affecting the company, with concise insights and implications for strategy. No placeholders or teasers—what you see is the final, downloadable file. Ready for immediate use after checkout.