JBS PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for JBS maps the political, economic, social, technological, legal, and environmental forces shaping its global meat-business strategy—highlighting regulatory risks, supply-chain pressures, and sustainability trends investors need to watch. Use this concise intelligence to anticipate disruption, identify growth levers, and fortify competitive plans. Purchase the full, fully editable report for the complete, actionable breakdown and instant download.

Political factors

Global Trade Protectionism and Tariffs

Rising protectionism in the US and China has forced JBS to re-route exports, with US beef tariffs rising to 8% in 2024 and China maintaining seasonal tariff-rate quotas; Brazilian beef exports to China fell 12% YoY in 2024, pressuring JBS’s margins. Changes to pork tariffs—US retaliatory duties at 5–10% in 2025—shift competitiveness toward Brazilian plants where production costs are ~15% lower. Management must adjust footprint and logistics to mitigate tariff-driven cost swings and currency exposure.

Brazilian Agricultural Policy Stability

As a Brazilian-headquartered multinational, JBS is heavily exposed to government agricultural policy: 2024 EMBRAPA/Ministry of Agriculture data show rural credit reached R$225 billion, and changes to subsidized rates or credit ceilings directly affect cattle rancher liquidity and JBS raw material costs.

Legislative shifts on land use and deforestation controls—Brazil reduced Amazon deforestation monitoring funding by 18% in 2023—can alter supply chain access and compliance costs for JBS.

Political stability matters for investor confidence; Brazil’s sovereign risk (5-year CDS ~160 bps in Jan 2025) influences JBS borrowing spreads and long-term strategic planning.

US Farm Bill and Regulatory Oversight

With JBS USA accounting for roughly 40% of US beef packing capacity and contributing over $50bn annual revenue globally, amendments to the US Farm Bill that shift subsidies or price supports for livestock could compress margins across its US operations.

Provisions enhancing USDA oversight or antitrust enforcement—following DOJ probes that led to $1bn+ industry settlements in recent years—could increase compliance costs and limit pricing power.

Heightened political emphasis on domestic food security has raised scrutiny of foreign-owned firms like JBS, evidenced by expanded CFIUS reviews and congressional inquiries, potentially affecting investment approvals and supply-chain decisions.

Geopolitical Instability in Supply Chains

Ongoing tensions in Eastern Europe and the Middle East have tightened global grain supplies, pushing corn and soybean meal prices up by ~18–25% during 2024–2025 and increasing JBS feed costs materially.

Price volatility has led JBS to expand hedging and risk-management, with commodity derivative positions reported at multi-hundred-million-dollar notional exposure to stabilize margins.

Unrest in key transit corridors prompted investment in diversified logistics, raising transport and storage CAPEX to secure supply continuity.

- Grain price rise 18–25% (2024–2025)

- Commodity hedges: multi-hundred-million-dollar notional

- Increased CAPEX for logistics diversification

Governmental Support for Sustainable Transition

Governments are increasing incentives and mandates for green agriculture; in 2024 the EU allocated €270 billion to its Farm to Fork and Green Deal-related programs, pressuring JBS to accelerate emissions cuts and sustainable feed sourcing.

JBS must align lobbying and strategy with global initiatives such as the 2021 Global Methane Pledge; methane reductions are material—enteric and manure account for roughly 40% of livestock emissions.

Failure to secure favorable rules for international carbon credit markets risks disadvantaging JBS versus local competitors who capture national credits; voluntary carbon market flows to agribusiness reached about $1.2 billion in 2023.

- EU green funding €270B (2024)

- Livestock ~40% of ag emissions (methane)

- Voluntary ag carbon markets ~$1.2B (2023)

- Alignment needed with Global Methane Pledge

Rising tariffs, grain shocks and green costs reshape agri risk and finance

Political risks—tariffs (US 8% beef 2024; US pork duties 5–10% 2025), Brazil sovereign CDS ~160bps (Jan 2025), and reduced Amazon monitoring funding −18% (2023)—raise input costs, compliance and financing spreads; grain price inflation +18–25% (2024–25) and multi-hundred-million-dollar commodity hedges broaden risk management; EU green funds €270B (2024) and ~$1.2B ag carbon markets (2023) drive sustainability costs and lobbying needs.

| Metric | Value |

|---|---|

| US beef tariff | 8% (2024) |

| US pork duties | 5–10% (2025) |

| Brazil 5y CDS | ~160 bps (Jan 2025) |

| Amazon monitoring funding | −18% (2023) |

| Grain price rise | +18–25% (2024–25) |

| EU green funding | €270B (2024) |

| Ag carbon market | $1.2B (2023) |

What is included in the product

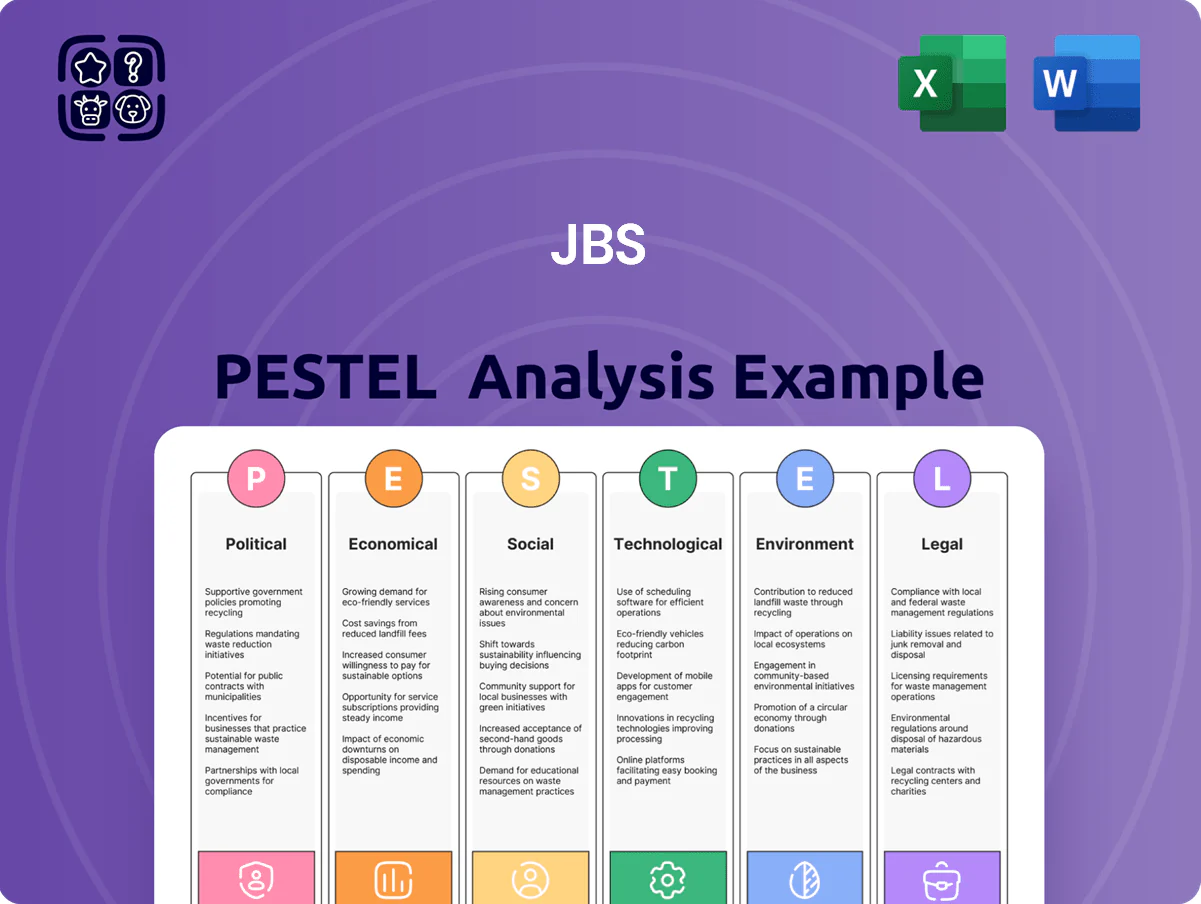

Explores how external macro-environmental factors uniquely affect JBS across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of JBS that’s visually segmented for quick interpretation, ideal for slide decks, team alignment, or consultant reports to streamline external risk and market-positioning discussions.

Economic factors

Currency Exchange Rate Volatility

JBS operates across multiple currencies, making it highly exposed to BRL/USD swings; a 2023–2025 average BRL depreciation of roughly 18% vs the dollar boosted local-margin competitiveness but increased dollar-denominated debt servicing—JBS reported net debt of about $14.5bn in 2024, amplifying FX risk. Financial teams use hedging and natural offsets to manage conversion volatility and protect reported EBITDA for global investors.

Global Inflation and Consumer Purchasing Power

Interest Rate Environments and Debt Servicing

The high-interest-rate environment of 2024–2025 pushed global benchmark rates up, with the US Fed Funds peak near 5.5% and Brazil SELIC at 13.75% in 2024, raising JBS’s cost of capital for its capital-intensive operations and imports. Managing JBS’s sizable net debt—about $12.6 billion net debt reported end-2024—requires disciplined cash flow allocation and targeted refinancing to avoid liquidity strain. Elevated rates constrain JBS’s appetite for large M&A, increasing hurdle rates and deal financing costs in the near term.

Volatility in Commodity Feed Costs

Corn and soybean prices, up 18% and 22% year-over-year in 2024 respectively, remain a key cost driver for JBS’s poultry and pork operations, directly affecting margins in prepared foods.

Weather-driven supply shocks and rising global feed demand have increased volatility, making commodity swings a principal determinant of quarterly profitability for the segment.

JBS leverages vertical integration, on-farm supply contracts and hedging; in 2024 the company reported procurement-led cost savings that mitigated roughly 40% of feed-price impact on prepared foods margins.

- 2024 Y/Y: corn +18%, soybeans +22%

- Feed volatility materially affects prepared foods margins

- Vertical integration and hedging offset ~40% of feed-price shocks

Emerging Market Growth and Protein Demand

Emerging market expansion in Southeast Asia and Africa—GDP growth forecasts of ~4.5–5.5% annually (IMF 2025) and rising middle classes—drives stronger demand for animal protein; per-capita meat consumption is projected to rise by 15–25% through 2030 in key markets.

To capture exports, JBS needs targeted investments in local distribution and cold chain: estimated capex per country for refrigerated logistics ranges $50–200M depending on scale, enabling market-share gains.

- GDP growth: ~4.5–5.5% (2025 IMF)

- Per-capita meat rise: +15–25% by 2030

- Estimated cold-chain capex: $50–200M/country

- Strategy: local distribution + refrigerated logistics

BRL depreciation lifts debt pain but boosts meat competitiveness as costs bite

FX exposure (BRL/USD avg depreciation ~18% 2023–25) raises dollar debt servicing on ~$14.5bn net debt (2024) while boosting local competitiveness; food CPI +6.2% YoY (2024) shifts demand to cheaper proteins; corn +18% and soy +22% YoY (2024) drive feed costs—vertical integration/hedging offset ~40% of impact; emerging markets GDP ~4.5–5.5% (2025 IMF) support +15–25% per‑capita meat growth to 2030.

| Metric | 2024/2025 Value |

|---|---|

| Net debt | $14.5bn (2024) |

| BRL/USD move | ~18% depreciation (2023–25) |

| Food CPI | +6.2% YoY (2024) |

| Corn / Soy | +18% / +22% YoY (2024) |

| Hedging impact | ~40% feed cost offset (2024) |

| Emerging GDP | 4.5–5.5% (2025 IMF) |

Full Version Awaits

JBS PESTLE Analysis

The preview shown here is the exact JBS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for JBS maps the political, economic, social, technological, legal, and environmental forces shaping its global meat-business strategy—highlighting regulatory risks, supply-chain pressures, and sustainability trends investors need to watch. Use this concise intelligence to anticipate disruption, identify growth levers, and fortify competitive plans. Purchase the full, fully editable report for the complete, actionable breakdown and instant download.

Political factors

Global Trade Protectionism and Tariffs

Rising protectionism in the US and China has forced JBS to re-route exports, with US beef tariffs rising to 8% in 2024 and China maintaining seasonal tariff-rate quotas; Brazilian beef exports to China fell 12% YoY in 2024, pressuring JBS’s margins. Changes to pork tariffs—US retaliatory duties at 5–10% in 2025—shift competitiveness toward Brazilian plants where production costs are ~15% lower. Management must adjust footprint and logistics to mitigate tariff-driven cost swings and currency exposure.

Brazilian Agricultural Policy Stability

As a Brazilian-headquartered multinational, JBS is heavily exposed to government agricultural policy: 2024 EMBRAPA/Ministry of Agriculture data show rural credit reached R$225 billion, and changes to subsidized rates or credit ceilings directly affect cattle rancher liquidity and JBS raw material costs.

Legislative shifts on land use and deforestation controls—Brazil reduced Amazon deforestation monitoring funding by 18% in 2023—can alter supply chain access and compliance costs for JBS.

Political stability matters for investor confidence; Brazil’s sovereign risk (5-year CDS ~160 bps in Jan 2025) influences JBS borrowing spreads and long-term strategic planning.

US Farm Bill and Regulatory Oversight

With JBS USA accounting for roughly 40% of US beef packing capacity and contributing over $50bn annual revenue globally, amendments to the US Farm Bill that shift subsidies or price supports for livestock could compress margins across its US operations.

Provisions enhancing USDA oversight or antitrust enforcement—following DOJ probes that led to $1bn+ industry settlements in recent years—could increase compliance costs and limit pricing power.

Heightened political emphasis on domestic food security has raised scrutiny of foreign-owned firms like JBS, evidenced by expanded CFIUS reviews and congressional inquiries, potentially affecting investment approvals and supply-chain decisions.

Geopolitical Instability in Supply Chains

Ongoing tensions in Eastern Europe and the Middle East have tightened global grain supplies, pushing corn and soybean meal prices up by ~18–25% during 2024–2025 and increasing JBS feed costs materially.

Price volatility has led JBS to expand hedging and risk-management, with commodity derivative positions reported at multi-hundred-million-dollar notional exposure to stabilize margins.

Unrest in key transit corridors prompted investment in diversified logistics, raising transport and storage CAPEX to secure supply continuity.

- Grain price rise 18–25% (2024–2025)

- Commodity hedges: multi-hundred-million-dollar notional

- Increased CAPEX for logistics diversification

Governmental Support for Sustainable Transition

Governments are increasing incentives and mandates for green agriculture; in 2024 the EU allocated €270 billion to its Farm to Fork and Green Deal-related programs, pressuring JBS to accelerate emissions cuts and sustainable feed sourcing.

JBS must align lobbying and strategy with global initiatives such as the 2021 Global Methane Pledge; methane reductions are material—enteric and manure account for roughly 40% of livestock emissions.

Failure to secure favorable rules for international carbon credit markets risks disadvantaging JBS versus local competitors who capture national credits; voluntary carbon market flows to agribusiness reached about $1.2 billion in 2023.

- EU green funding €270B (2024)

- Livestock ~40% of ag emissions (methane)

- Voluntary ag carbon markets ~$1.2B (2023)

- Alignment needed with Global Methane Pledge

Rising tariffs, grain shocks and green costs reshape agri risk and finance

Political risks—tariffs (US 8% beef 2024; US pork duties 5–10% 2025), Brazil sovereign CDS ~160bps (Jan 2025), and reduced Amazon monitoring funding −18% (2023)—raise input costs, compliance and financing spreads; grain price inflation +18–25% (2024–25) and multi-hundred-million-dollar commodity hedges broaden risk management; EU green funds €270B (2024) and ~$1.2B ag carbon markets (2023) drive sustainability costs and lobbying needs.

| Metric | Value |

|---|---|

| US beef tariff | 8% (2024) |

| US pork duties | 5–10% (2025) |

| Brazil 5y CDS | ~160 bps (Jan 2025) |

| Amazon monitoring funding | −18% (2023) |

| Grain price rise | +18–25% (2024–25) |

| EU green funding | €270B (2024) |

| Ag carbon market | $1.2B (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect JBS across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary of JBS that’s visually segmented for quick interpretation, ideal for slide decks, team alignment, or consultant reports to streamline external risk and market-positioning discussions.

Economic factors

Currency Exchange Rate Volatility

JBS operates across multiple currencies, making it highly exposed to BRL/USD swings; a 2023–2025 average BRL depreciation of roughly 18% vs the dollar boosted local-margin competitiveness but increased dollar-denominated debt servicing—JBS reported net debt of about $14.5bn in 2024, amplifying FX risk. Financial teams use hedging and natural offsets to manage conversion volatility and protect reported EBITDA for global investors.

Global Inflation and Consumer Purchasing Power

Interest Rate Environments and Debt Servicing

The high-interest-rate environment of 2024–2025 pushed global benchmark rates up, with the US Fed Funds peak near 5.5% and Brazil SELIC at 13.75% in 2024, raising JBS’s cost of capital for its capital-intensive operations and imports. Managing JBS’s sizable net debt—about $12.6 billion net debt reported end-2024—requires disciplined cash flow allocation and targeted refinancing to avoid liquidity strain. Elevated rates constrain JBS’s appetite for large M&A, increasing hurdle rates and deal financing costs in the near term.

Volatility in Commodity Feed Costs

Corn and soybean prices, up 18% and 22% year-over-year in 2024 respectively, remain a key cost driver for JBS’s poultry and pork operations, directly affecting margins in prepared foods.

Weather-driven supply shocks and rising global feed demand have increased volatility, making commodity swings a principal determinant of quarterly profitability for the segment.

JBS leverages vertical integration, on-farm supply contracts and hedging; in 2024 the company reported procurement-led cost savings that mitigated roughly 40% of feed-price impact on prepared foods margins.

- 2024 Y/Y: corn +18%, soybeans +22%

- Feed volatility materially affects prepared foods margins

- Vertical integration and hedging offset ~40% of feed-price shocks

Emerging Market Growth and Protein Demand

Emerging market expansion in Southeast Asia and Africa—GDP growth forecasts of ~4.5–5.5% annually (IMF 2025) and rising middle classes—drives stronger demand for animal protein; per-capita meat consumption is projected to rise by 15–25% through 2030 in key markets.

To capture exports, JBS needs targeted investments in local distribution and cold chain: estimated capex per country for refrigerated logistics ranges $50–200M depending on scale, enabling market-share gains.

- GDP growth: ~4.5–5.5% (2025 IMF)

- Per-capita meat rise: +15–25% by 2030

- Estimated cold-chain capex: $50–200M/country

- Strategy: local distribution + refrigerated logistics

BRL depreciation lifts debt pain but boosts meat competitiveness as costs bite

FX exposure (BRL/USD avg depreciation ~18% 2023–25) raises dollar debt servicing on ~$14.5bn net debt (2024) while boosting local competitiveness; food CPI +6.2% YoY (2024) shifts demand to cheaper proteins; corn +18% and soy +22% YoY (2024) drive feed costs—vertical integration/hedging offset ~40% of impact; emerging markets GDP ~4.5–5.5% (2025 IMF) support +15–25% per‑capita meat growth to 2030.

| Metric | 2024/2025 Value |

|---|---|

| Net debt | $14.5bn (2024) |

| BRL/USD move | ~18% depreciation (2023–25) |

| Food CPI | +6.2% YoY (2024) |

| Corn / Soy | +18% / +22% YoY (2024) |

| Hedging impact | ~40% feed cost offset (2024) |

| Emerging GDP | 4.5–5.5% (2025 IMF) |

Full Version Awaits

JBS PESTLE Analysis

The preview shown here is the exact JBS PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.