JCET Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our focused PESTLE Analysis of JCET Group—spot regulatory, economic, and technological forces shaping its outlook and turn those insights into strategic advantage; buy the full report for a complete, downloadable breakdown you can use in investment pitches or strategy sessions.

Political factors

Geopolitical semiconductor tensions

Ongoing US-China trade friction hits JCET Group, a leading Chinese OSAT, as US export controls on high-end lithography and packaging tools have tightened since 2020, contributing to a 15% rise in regional compliance costs for Chinese chip suppliers in 2024.

Restrictions on advanced packaging tech force JCET to reroute orders and invest in localized tooling, with capex rising to RMB 2.1 billion in 2024 to secure alternative equipment and IP-safe processes.

JCET mitigates risk through operations in Singapore and South Korea, which accounted for 18% of revenue in 2024, balancing market access amid growing regional protectionism and supply-chain reshoring pressures.

Governmental industrial subsidies

China’s National Integrated Circuit Industry Investment Fund has channeled over CNY 200 billion since 2014 into semiconductor firms, bolstering JCET’s access to subsidies and tax incentives that supported its 2023 R&D spend of RMB 1.2 billion and expansion of domestic capacity by 18% year‑on‑year; such state backing accelerates technology scaling but increases exposure to international scrutiny and potential trade remedies over alleged unfair competition.

Supply chain sovereignty initiatives

Many governments adopting China Plus One have driven 2024 semiconductor reshoring: EU and US subsidies exceeded $85bn combined by end-2024, prompting firms to diversify suppliers; JCET must leverage its 8+ international manufacturing sites (2025 capacity growth plans ~15%) to stay a preferred global partner. Political pressure to localize assembly/testing in Europe/North America risks eroding JCET’s regional share, where local providers received >$10bn in investment in 2024.

Regulatory oversight on cross-border M&A

Political barriers limit Chinese semiconductor acquisitions abroad; national security reviews blocked several deals and CFIUS reviews rose 30% in 2023, constraining JCET’s ability to buy foreign IP-rich targets.

JCET faces tight U.S. and EU scrutiny—CFIUS interventions cost deals or led to divestitures—pushing the company toward organic growth and R&D, where it increased capex 22% to RMB 3.6 billion in 2024.

- CFIUS reviews +30% (2023)

- JCET capex +22% to RMB 3.6bn (2024)

- Higher political risk → shift to organic R&D

Diplomatic stability in SE Asia

JCET’s major Singapore facilities mean Southeast Asian diplomatic stability is critical; Singapore accounted for about 12% of JCET’s 2024 revenue, so disruptions risk meaningful operational impact.

Tense China-ASEAN ties affect cross-border logistics and labor mobility—China-Southeast Asia trade was roughly $1.3 trillion in 2024, influencing supply-chain flow for JCET.

Escalation in maritime/territorial disputes could disrupt specialized semiconductor distribution routes, raising freight delays and insurance costs that would hit margins.

- Singapore = ~12% of 2024 revenue

- China-ASEAN trade ~ $1.3T (2024)

- Maritime disputes → higher logistics delays/insurance

JCET hikes capex for compliance as geopolitical shifts drive diversification, subsidy race

Geopolitical tensions (US export controls, CFIUS +30% 2023) raised JCET compliance/capex (capex +22% to RMB 3.6bn 2024; RMB 2.1bn localized tooling 2024), diversified revenue (Singapore ~12%, international sites 18% 2024) amid $85bn+ EU/US subsidies (end-2024); China-ASEAN trade $1.3T (2024) heightens logistics risk.

| Metric | Value (2024) |

|---|---|

| Capex | RMB 3.6bn (+22%) |

| Tooling/localize spend | RMB 2.1bn |

| Singapore rev | ~12% |

| Intl sites rev | 18% |

| EU/US subsidies | $85bn+ |

| China-ASEAN trade | $1.3T |

What is included in the product

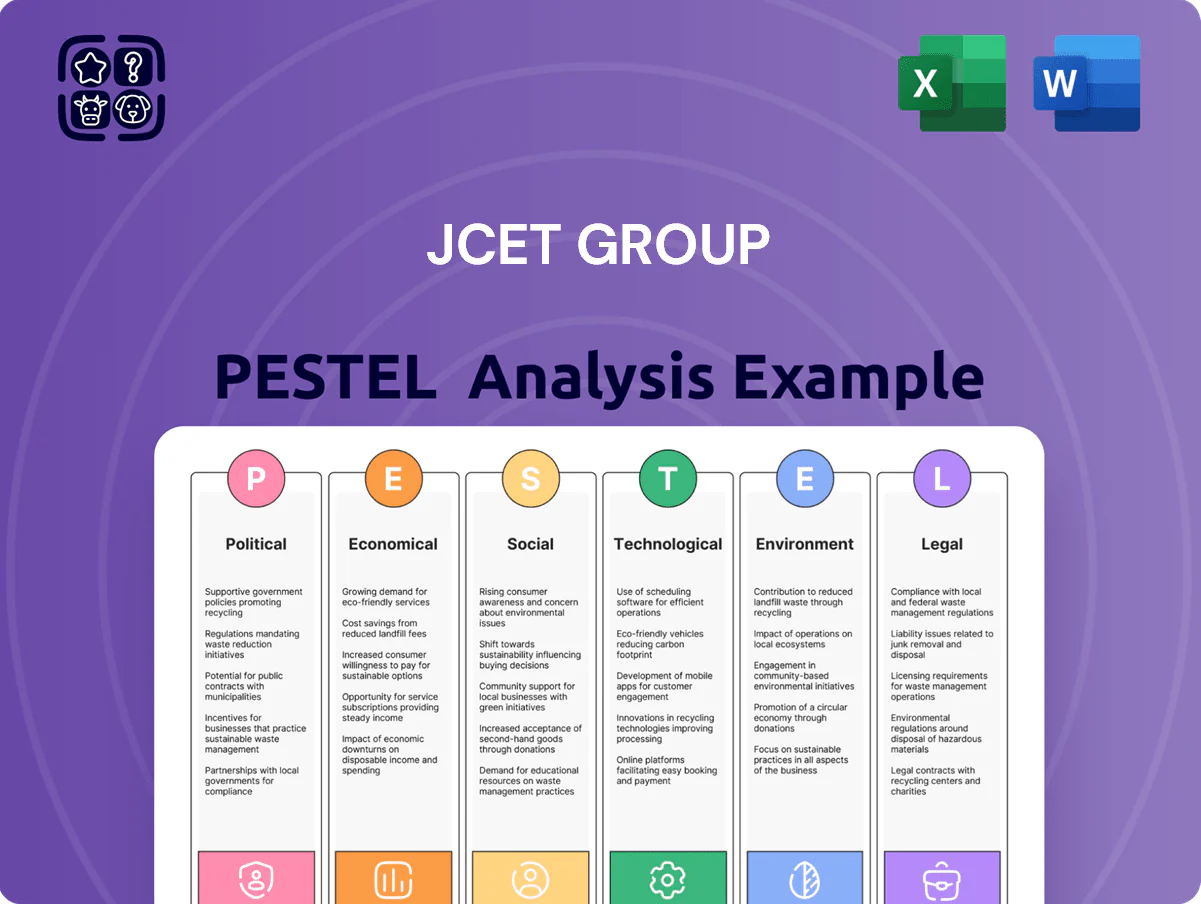

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact JCET Group, using current market and regulatory dynamics to identify risks and opportunities.

A concise JCET Group PESTLE summary that’s visually segmented for quick meetings, easily dropped into slides, and editable for regional or business-line notes to streamline risk discussions and client reports.

Economic factors

Global semiconductor market cycles

The demand for JCET’s packaging and testing services is highly cyclical, linked to electronics and automotive end-markets; late 2025 recovery in smartphones and a surge in AI server demand helped JCET report a 38% year-on-year revenue increase in 9M2025 and lifted gross margin to ~18.5%. Inventory corrections or consumer-electronics downturns remain the main downside risk, as past semiconductor cycles have seen revenues fall 20–30% during downturns.

Currency exchange rate volatility

As JCET reports in RMB while ~45% of revenues are USD-linked, a 10% RMB appreciation vs USD in 2025 would have cut RMB-reported revenue by roughly 4.5%, materially squeezing margins given FY2024 gross margin of ~18.2%.

Inflationary pressure on manufacturing costs

Rising raw material costs—gold up ~35% and copper ~20% in 2024 vs 2022, plus specialty resins up ~18%—have compressed JCET’s reported gross margins; materials represent a significant portion of BOM for advanced packaging. Energy price volatility (electricity up ~12% in APAC 2024) increases operating costs for climate-controlled test labs. To preserve margins JCET must either pass costs to customers or boost automation-driven efficiency; automation capex rose ~10% industry-wide in 2024.

Interest rate environment and capital expenditure

JCET operates in a capital-intensive semiconductor packaging/testing sector that requires continual investment in advanced lithography and bonding equipment; industry CAPEX often runs into billions—global semiconductor equipment spending reached about $95.4bn in 2023 and was projected near $115bn for 2024–25.

Elevated global interest rates (Fed funds ~5.25–5.50% in 2024) raise JCET’s cost of debt for capacity expansion, stressing debt servicing and project IRRs, making disciplined debt-to-equity management critical.

- 2023–25 industry equipment spend ~95–115bn

- US policy rate ~5.25–5.50% (2024)

- Multi-billion-dollar CAPEX requires balanced debt/equity to protect margins

Labor cost trends in Asia

- China wages +6.5% YoY (2024)

- Engineer salary premiums 10–20% in tech hubs

- ASEAN assembly wages 40–60% below China

- Strategic focus: automation, productivity, selective relocation

JCET: AI-driven 9M25 surge vs cyclicality, input inflation and FX risks

Demand cyclicality ties JCET revenue to smartphones/automotive; late-2025 AI/server upswing drove 9M2025 revenue +38% YoY and gross margin ~18.5%, but past downturns cut revenues 20–30%. Currency risk: 45% USD-linked sales—10% RMB appreciation would lower RMB revenue ~4.5%. Input inflation (gold +35%, copper +20%, resins +18% vs 2022) and China wages +6.5% (2024) squeeze margins; CAPEX needs (industry spend $95–115bn 2023–25) plus Fed rates ~5.25–5.50% raise funding costs.

| Metric | Value |

|---|---|

| 9M2025 rev growth | +38% YoY |

| Gross margin | ~18.5% |

| Industry capex (2023–25) | $95–115bn |

| Gold/copper/resins (vs 2022) | +35%/+20%/+18% |

| China wages (2024) | +6.5% YoY |

| Policy rate (2024) | ~5.25–5.50% |

What You See Is What You Get

JCET Group PESTLE Analysis

The preview shown here is the exact JCET Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with no placeholders or teasers, and the layout, content, and structure visible now are exactly what you’ll download. You’ll get the complete, professionally structured document immediately after checkout. What you see is what you’ll be working with.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our focused PESTLE Analysis of JCET Group—spot regulatory, economic, and technological forces shaping its outlook and turn those insights into strategic advantage; buy the full report for a complete, downloadable breakdown you can use in investment pitches or strategy sessions.

Political factors

Geopolitical semiconductor tensions

Ongoing US-China trade friction hits JCET Group, a leading Chinese OSAT, as US export controls on high-end lithography and packaging tools have tightened since 2020, contributing to a 15% rise in regional compliance costs for Chinese chip suppliers in 2024.

Restrictions on advanced packaging tech force JCET to reroute orders and invest in localized tooling, with capex rising to RMB 2.1 billion in 2024 to secure alternative equipment and IP-safe processes.

JCET mitigates risk through operations in Singapore and South Korea, which accounted for 18% of revenue in 2024, balancing market access amid growing regional protectionism and supply-chain reshoring pressures.

Governmental industrial subsidies

China’s National Integrated Circuit Industry Investment Fund has channeled over CNY 200 billion since 2014 into semiconductor firms, bolstering JCET’s access to subsidies and tax incentives that supported its 2023 R&D spend of RMB 1.2 billion and expansion of domestic capacity by 18% year‑on‑year; such state backing accelerates technology scaling but increases exposure to international scrutiny and potential trade remedies over alleged unfair competition.

Supply chain sovereignty initiatives

Many governments adopting China Plus One have driven 2024 semiconductor reshoring: EU and US subsidies exceeded $85bn combined by end-2024, prompting firms to diversify suppliers; JCET must leverage its 8+ international manufacturing sites (2025 capacity growth plans ~15%) to stay a preferred global partner. Political pressure to localize assembly/testing in Europe/North America risks eroding JCET’s regional share, where local providers received >$10bn in investment in 2024.

Regulatory oversight on cross-border M&A

Political barriers limit Chinese semiconductor acquisitions abroad; national security reviews blocked several deals and CFIUS reviews rose 30% in 2023, constraining JCET’s ability to buy foreign IP-rich targets.

JCET faces tight U.S. and EU scrutiny—CFIUS interventions cost deals or led to divestitures—pushing the company toward organic growth and R&D, where it increased capex 22% to RMB 3.6 billion in 2024.

- CFIUS reviews +30% (2023)

- JCET capex +22% to RMB 3.6bn (2024)

- Higher political risk → shift to organic R&D

Diplomatic stability in SE Asia

JCET’s major Singapore facilities mean Southeast Asian diplomatic stability is critical; Singapore accounted for about 12% of JCET’s 2024 revenue, so disruptions risk meaningful operational impact.

Tense China-ASEAN ties affect cross-border logistics and labor mobility—China-Southeast Asia trade was roughly $1.3 trillion in 2024, influencing supply-chain flow for JCET.

Escalation in maritime/territorial disputes could disrupt specialized semiconductor distribution routes, raising freight delays and insurance costs that would hit margins.

- Singapore = ~12% of 2024 revenue

- China-ASEAN trade ~ $1.3T (2024)

- Maritime disputes → higher logistics delays/insurance

JCET hikes capex for compliance as geopolitical shifts drive diversification, subsidy race

Geopolitical tensions (US export controls, CFIUS +30% 2023) raised JCET compliance/capex (capex +22% to RMB 3.6bn 2024; RMB 2.1bn localized tooling 2024), diversified revenue (Singapore ~12%, international sites 18% 2024) amid $85bn+ EU/US subsidies (end-2024); China-ASEAN trade $1.3T (2024) heightens logistics risk.

| Metric | Value (2024) |

|---|---|

| Capex | RMB 3.6bn (+22%) |

| Tooling/localize spend | RMB 2.1bn |

| Singapore rev | ~12% |

| Intl sites rev | 18% |

| EU/US subsidies | $85bn+ |

| China-ASEAN trade | $1.3T |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact JCET Group, using current market and regulatory dynamics to identify risks and opportunities.

A concise JCET Group PESTLE summary that’s visually segmented for quick meetings, easily dropped into slides, and editable for regional or business-line notes to streamline risk discussions and client reports.

Economic factors

Global semiconductor market cycles

The demand for JCET’s packaging and testing services is highly cyclical, linked to electronics and automotive end-markets; late 2025 recovery in smartphones and a surge in AI server demand helped JCET report a 38% year-on-year revenue increase in 9M2025 and lifted gross margin to ~18.5%. Inventory corrections or consumer-electronics downturns remain the main downside risk, as past semiconductor cycles have seen revenues fall 20–30% during downturns.

Currency exchange rate volatility

As JCET reports in RMB while ~45% of revenues are USD-linked, a 10% RMB appreciation vs USD in 2025 would have cut RMB-reported revenue by roughly 4.5%, materially squeezing margins given FY2024 gross margin of ~18.2%.

Inflationary pressure on manufacturing costs

Rising raw material costs—gold up ~35% and copper ~20% in 2024 vs 2022, plus specialty resins up ~18%—have compressed JCET’s reported gross margins; materials represent a significant portion of BOM for advanced packaging. Energy price volatility (electricity up ~12% in APAC 2024) increases operating costs for climate-controlled test labs. To preserve margins JCET must either pass costs to customers or boost automation-driven efficiency; automation capex rose ~10% industry-wide in 2024.

Interest rate environment and capital expenditure

JCET operates in a capital-intensive semiconductor packaging/testing sector that requires continual investment in advanced lithography and bonding equipment; industry CAPEX often runs into billions—global semiconductor equipment spending reached about $95.4bn in 2023 and was projected near $115bn for 2024–25.

Elevated global interest rates (Fed funds ~5.25–5.50% in 2024) raise JCET’s cost of debt for capacity expansion, stressing debt servicing and project IRRs, making disciplined debt-to-equity management critical.

- 2023–25 industry equipment spend ~95–115bn

- US policy rate ~5.25–5.50% (2024)

- Multi-billion-dollar CAPEX requires balanced debt/equity to protect margins

Labor cost trends in Asia

- China wages +6.5% YoY (2024)

- Engineer salary premiums 10–20% in tech hubs

- ASEAN assembly wages 40–60% below China

- Strategic focus: automation, productivity, selective relocation

JCET: AI-driven 9M25 surge vs cyclicality, input inflation and FX risks

Demand cyclicality ties JCET revenue to smartphones/automotive; late-2025 AI/server upswing drove 9M2025 revenue +38% YoY and gross margin ~18.5%, but past downturns cut revenues 20–30%. Currency risk: 45% USD-linked sales—10% RMB appreciation would lower RMB revenue ~4.5%. Input inflation (gold +35%, copper +20%, resins +18% vs 2022) and China wages +6.5% (2024) squeeze margins; CAPEX needs (industry spend $95–115bn 2023–25) plus Fed rates ~5.25–5.50% raise funding costs.

| Metric | Value |

|---|---|

| 9M2025 rev growth | +38% YoY |

| Gross margin | ~18.5% |

| Industry capex (2023–25) | $95–115bn |

| Gold/copper/resins (vs 2022) | +35%/+20%/+18% |

| China wages (2024) | +6.5% YoY |

| Policy rate (2024) | ~5.25–5.50% |

What You See Is What You Get

JCET Group PESTLE Analysis

The preview shown here is the exact JCET Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with no placeholders or teasers, and the layout, content, and structure visible now are exactly what you’ll download. You’ll get the complete, professionally structured document immediately after checkout. What you see is what you’ll be working with.