J. C. Penney Company PESTLE Analysis

Your Competitive Advantage Starts with This Report

J. C. Penney faces shifting retail dynamics—from regulatory pressures and economic headwinds to rising e-commerce competition and sustainability expectations—that are reshaping its strategy and risk profile; our concise PESTLE highlights these forces and their implications for operations and growth. Purchase the full PESTLE to access detailed, actionable insights and ready-to-use analysis for investment, strategy, or competitive planning.

Political factors

International Trade Policy and Tariffs

Changes in trade agreements and tariffs on imported textiles materially affect J. C. Penney’s cost base; in 2024 roughly 60–70% of apparel inventory remained sourced from China and Southeast Asia, so tariff hikes of 10–25% can raise COGS significantly. Escalating trade tensions through 2023–2025 pushed input costs and contributed to a mid-single-digit rise in retail prices industrywide. JCP must monitor geopolitical shifts and diversify suppliers to Vietnam, Bangladesh, and Mexico to mitigate sudden duty increases and protect gross margin.

Minimum Wage Legislation

Ongoing federal and state minimum wage debates directly raise labor costs for J. C. Penney, which employed about 60,000 staff pre-2024 and reported $8.1 billion revenue in FY2023; a $1 rise in hourly wages across that workforce could add hundreds of millions in annual payroll. As a mid-scale department store, Penney must adjust compensation to comply and stay competitive, pressuring margins that averaged low single-digit operating income in recent years. Without offsets from higher same-store sales—U.S. comparable sales were down mid-single digits in 2023—or efficiency gains, mandated wage hikes risk materially compressing profits.

Corporate Taxation Policies

The US federal corporate tax rate reset to 21% after 2017 reforms, and J. C. Penney reported a 2024 adjusted operating loss, limiting reinvestment capacity; lower effective tax burdens can boost free cash flow for store modernizations.

Consumer Protection Regulations

Government oversight of consumer credit impacts J. C. Penney’s private-label card business; CFPB actions and state usury caps can constrain interest rates and fees that generated about 8-12% of retail revenue pre-2024 for U.S. retailers' card programs.

Stricter rate/fee limits would compress card-related margins—already pressured after 2023 credit-market shifts—reducing a key loyalty driver tied to repeat purchases and higher AOVs.

J. C. Penney must ensure compliance with evolving federal/state rules while preserving rewards, promotions, and merchant-funded benefits to retain cardholder value.

- Card revenue ≈ 8–12% of retail sales (industry range)

- CFPB/state caps can cut finance income, lowering margins

- Compliance investment needed to sustain card benefits and loyalty

Geopolitical Stability in Sourcing Regions

Political instability in key manufacturing hubs—notably Vietnam, Bangladesh and parts of China—has raised supply-chain risk; 2024 UN trade disruption indexes showed a 12% increase in transport delays from these regions, risking inventory shortages for J. C. Penney’s apparel and home goods lines.

Events like civil unrest or diplomatic disputes require contingency planning; in 2023 J. C. Penney reported inventory turnover slowing to 3.8x, highlighting vulnerability to sourcing shocks.

Maintaining a flexible sourcing strategy—diversifying suppliers and nearshoring—helps prevent stock-outs that could push customers to competitors.

- 12% increase in transport delays (2024 UN index)

- Inventory turnover 3.8x (2023)

- Priority: supplier diversification and nearshoring

Political risks could swell JCP’s costs, cut card income and slow inventory turnover

Political factors raise JCP’s cost and operational risk: tariffs on China/SE Asia sourcing (60–70% of apparel) can add 10–25% to COGS; wage hikes across ~60,000 employees materially lift payroll; CFPB/state caps threaten private‑label card income (~8–12% of retail sales); geopolitical/supply disruptions increased transport delays ~12% (2024 UN index), slowing inventory turnover to 3.8x (2023).

| Metric | Value |

|---|---|

| Apparel sourced from China/SE Asia | 60–70% |

| Tariff impact range | +10–25% COGS |

| Employees (pre‑2024) | ~60,000 |

| Card revenue (industry) | 8–12% of sales |

| Transport delays (UN index 2024) | +12% |

| Inventory turnover (2023) | 3.8x |

What is included in the product

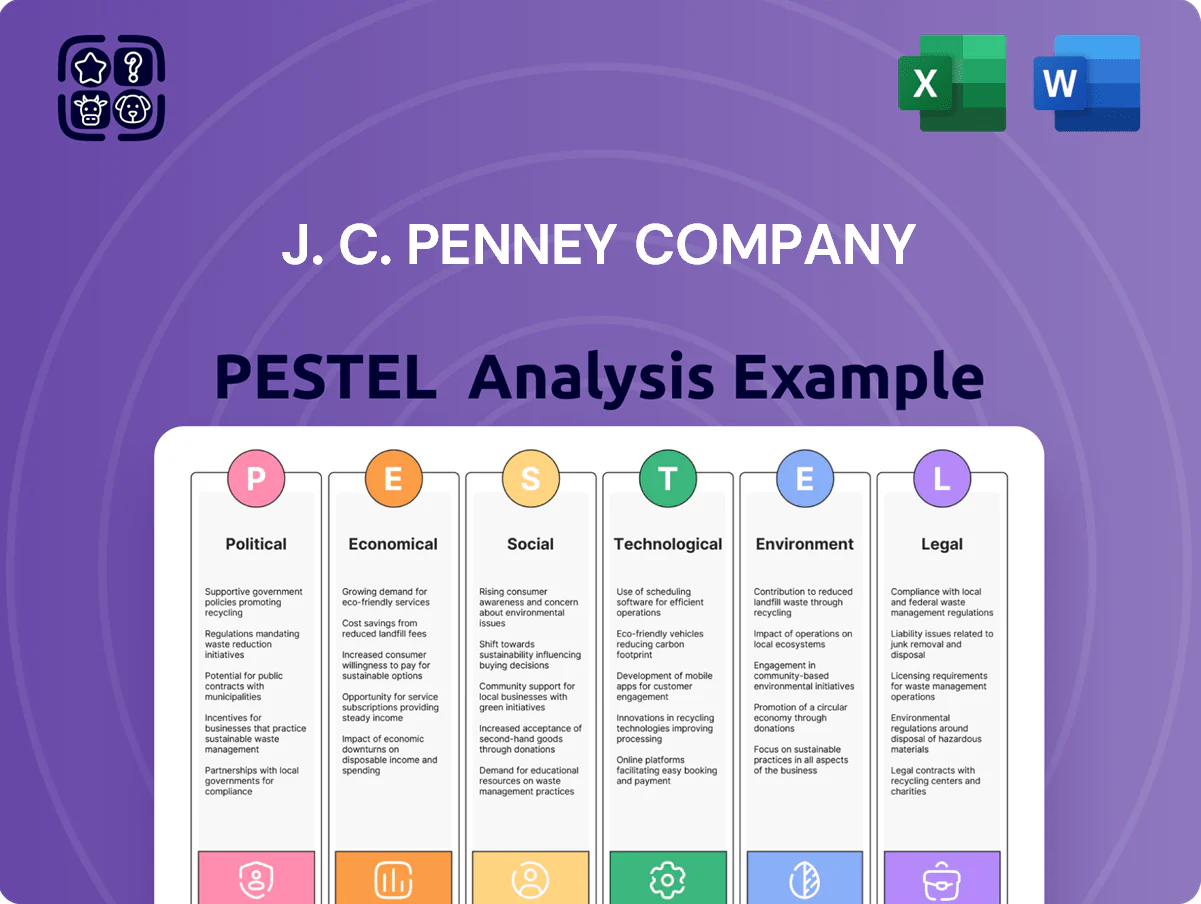

Explores how external macro-environmental factors uniquely affect the J. C. Penney Company across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise PESTLE snapshot of J.C. Penney, organized by Political, Economic, Social, Technological, Legal, and Environmental factors, provides a ready-to-use summary for meetings, easy slide insertion, and quick team alignment on external risks and market positioning.

Economic factors

Inflation and Consumer Spending Power

Persistent inflation erodes discretionary income for J. C. Penney’s core middle‑class shoppers; US CPI rose 3.4% in 2024 after 2023’s 3.1%, pressuring spending on non‑essentials like jewelry and home furnishings.

As food and shelter costs consumed larger budget shares—housing costs up ~5% YoY in 2024—customers shifted to value options, forcing Penney to lean on targeted promotions, competitive pricing and private‑label expansion to retain traffic.

Interest Rate Environment

Rising U.S. benchmark rates—the Federal Reserve funds rate at 5.25–5.50% in 2024—raises J. C. Penney’s borrowing costs, increasing interest expense on its credit facilities and making store renovation projects more expensive to finance.

Higher consumer borrowing costs are shown by average credit card APRs near 22% in 2024, which can suppress discretionary spending and big-ticket purchases at J. C. Penney.

Elevated rates may reduce use of store credit programs, lowering transaction frequency and compressing same-store sales growth unless offset by promotions or financing incentives.

Competition from Off-Price Retailers

The rise of off-price chains like TJX and Ross, which grew net sales to about $52.5 billion and $24.4 billion respectively in FY2024, draws budget-conscious shoppers away from traditional department stores such as J. C. Penney. Discount competitors offering branded goods at lower price points captured market share, pressuring J. C. Penney’s comparable-store sales—down mid-single digits in 2024—while compressing margins. To stay viable, J. C. Penney must expand exclusive private labels and boost in-store services to differentiate its assortment and drive higher customer loyalty and spend.

Labor Market Dynamics

A tight US labor market drove retail average hourly earnings up 4.4% year-over-year in 2024, pressuring J. C. Penney’s recruitment and retention costs for store and warehouse staff.

Penney competes with retailers, gig platforms and logistics firms—Amazon’s U.S. warehousing workforce grew ~10% in 2023—raising wage benchmarks.

Investment in benefits and training is essential to maintain service quality but will increase operating expenses and labor margin pressure.

- Retail hourly wages +4.4% YoY (2024)

- Competition from gig/logistics firms; Amazon workforce +10% (2023)

- Higher benefits/training raise operating costs, squeezing margins

Real Estate and Mall Traffic Trends

The economic health of U.S. malls directly impacts J. C. Penney foot traffic and sales; national mall occupancy fell to about 88% in 2024 from 92% in 2019, pressuring store revenues.

With declining mall tenancy, JCP may renegotiate leases or relocate to off-mall strip centers; average mall rent concessions rose ~15% in 2023–24, improving relocation feasibility.

The 2026 strategy targets optimizing store footprint toward top MSAs—focusing on high-performing geographies that delivered ~70% of in-store sales in 2024.

- Declining mall occupancy: 88% (2024)

- Lease concessions up ~15% (2023–24)

- 70% of in-store sales from top MSAs (2024)

High rates and inflation shift shoppers to off‑price rivals, squeezing mall retailers

Inflation and high rates in 2024 cut discretionary spending (CPI +3.4%; Fed funds 5.25–5.50%), boosting demand for value channels; off‑price peers grew sales (TJX $52.5B, Ross $24.4B) eroding JCP comps (mid‑single‑digit declines). Wage inflation (+4.4% retail hourly pay) and mall occupancy declines (88% in 2024) squeeze margins and force footprint optimization.

| Metric | 2024 |

|---|---|

| US CPI | +3.4% |

| Fed funds | 5.25–5.50% |

| TJX net sales | $52.5B |

| Ross net sales | $24.4B |

| Retail wages | +4.4% YoY |

| Mall occupancy | 88% |

Same Document Delivered

J. C. Penney Company PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of J. C. Penney covers political, economic, social, technological, legal, and environmental factors with concise insights and actionable implications. No placeholders or teasers—what you see is the final, professionally structured file available for immediate download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

J. C. Penney faces shifting retail dynamics—from regulatory pressures and economic headwinds to rising e-commerce competition and sustainability expectations—that are reshaping its strategy and risk profile; our concise PESTLE highlights these forces and their implications for operations and growth. Purchase the full PESTLE to access detailed, actionable insights and ready-to-use analysis for investment, strategy, or competitive planning.

Political factors

International Trade Policy and Tariffs

Changes in trade agreements and tariffs on imported textiles materially affect J. C. Penney’s cost base; in 2024 roughly 60–70% of apparel inventory remained sourced from China and Southeast Asia, so tariff hikes of 10–25% can raise COGS significantly. Escalating trade tensions through 2023–2025 pushed input costs and contributed to a mid-single-digit rise in retail prices industrywide. JCP must monitor geopolitical shifts and diversify suppliers to Vietnam, Bangladesh, and Mexico to mitigate sudden duty increases and protect gross margin.

Minimum Wage Legislation

Ongoing federal and state minimum wage debates directly raise labor costs for J. C. Penney, which employed about 60,000 staff pre-2024 and reported $8.1 billion revenue in FY2023; a $1 rise in hourly wages across that workforce could add hundreds of millions in annual payroll. As a mid-scale department store, Penney must adjust compensation to comply and stay competitive, pressuring margins that averaged low single-digit operating income in recent years. Without offsets from higher same-store sales—U.S. comparable sales were down mid-single digits in 2023—or efficiency gains, mandated wage hikes risk materially compressing profits.

Corporate Taxation Policies

The US federal corporate tax rate reset to 21% after 2017 reforms, and J. C. Penney reported a 2024 adjusted operating loss, limiting reinvestment capacity; lower effective tax burdens can boost free cash flow for store modernizations.

Consumer Protection Regulations

Government oversight of consumer credit impacts J. C. Penney’s private-label card business; CFPB actions and state usury caps can constrain interest rates and fees that generated about 8-12% of retail revenue pre-2024 for U.S. retailers' card programs.

Stricter rate/fee limits would compress card-related margins—already pressured after 2023 credit-market shifts—reducing a key loyalty driver tied to repeat purchases and higher AOVs.

J. C. Penney must ensure compliance with evolving federal/state rules while preserving rewards, promotions, and merchant-funded benefits to retain cardholder value.

- Card revenue ≈ 8–12% of retail sales (industry range)

- CFPB/state caps can cut finance income, lowering margins

- Compliance investment needed to sustain card benefits and loyalty

Geopolitical Stability in Sourcing Regions

Political instability in key manufacturing hubs—notably Vietnam, Bangladesh and parts of China—has raised supply-chain risk; 2024 UN trade disruption indexes showed a 12% increase in transport delays from these regions, risking inventory shortages for J. C. Penney’s apparel and home goods lines.

Events like civil unrest or diplomatic disputes require contingency planning; in 2023 J. C. Penney reported inventory turnover slowing to 3.8x, highlighting vulnerability to sourcing shocks.

Maintaining a flexible sourcing strategy—diversifying suppliers and nearshoring—helps prevent stock-outs that could push customers to competitors.

- 12% increase in transport delays (2024 UN index)

- Inventory turnover 3.8x (2023)

- Priority: supplier diversification and nearshoring

Political risks could swell JCP’s costs, cut card income and slow inventory turnover

Political factors raise JCP’s cost and operational risk: tariffs on China/SE Asia sourcing (60–70% of apparel) can add 10–25% to COGS; wage hikes across ~60,000 employees materially lift payroll; CFPB/state caps threaten private‑label card income (~8–12% of retail sales); geopolitical/supply disruptions increased transport delays ~12% (2024 UN index), slowing inventory turnover to 3.8x (2023).

| Metric | Value |

|---|---|

| Apparel sourced from China/SE Asia | 60–70% |

| Tariff impact range | +10–25% COGS |

| Employees (pre‑2024) | ~60,000 |

| Card revenue (industry) | 8–12% of sales |

| Transport delays (UN index 2024) | +12% |

| Inventory turnover (2023) | 3.8x |

What is included in the product

Explores how external macro-environmental factors uniquely affect the J. C. Penney Company across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise PESTLE snapshot of J.C. Penney, organized by Political, Economic, Social, Technological, Legal, and Environmental factors, provides a ready-to-use summary for meetings, easy slide insertion, and quick team alignment on external risks and market positioning.

Economic factors

Inflation and Consumer Spending Power

Persistent inflation erodes discretionary income for J. C. Penney’s core middle‑class shoppers; US CPI rose 3.4% in 2024 after 2023’s 3.1%, pressuring spending on non‑essentials like jewelry and home furnishings.

As food and shelter costs consumed larger budget shares—housing costs up ~5% YoY in 2024—customers shifted to value options, forcing Penney to lean on targeted promotions, competitive pricing and private‑label expansion to retain traffic.

Interest Rate Environment

Rising U.S. benchmark rates—the Federal Reserve funds rate at 5.25–5.50% in 2024—raises J. C. Penney’s borrowing costs, increasing interest expense on its credit facilities and making store renovation projects more expensive to finance.

Higher consumer borrowing costs are shown by average credit card APRs near 22% in 2024, which can suppress discretionary spending and big-ticket purchases at J. C. Penney.

Elevated rates may reduce use of store credit programs, lowering transaction frequency and compressing same-store sales growth unless offset by promotions or financing incentives.

Competition from Off-Price Retailers

The rise of off-price chains like TJX and Ross, which grew net sales to about $52.5 billion and $24.4 billion respectively in FY2024, draws budget-conscious shoppers away from traditional department stores such as J. C. Penney. Discount competitors offering branded goods at lower price points captured market share, pressuring J. C. Penney’s comparable-store sales—down mid-single digits in 2024—while compressing margins. To stay viable, J. C. Penney must expand exclusive private labels and boost in-store services to differentiate its assortment and drive higher customer loyalty and spend.

Labor Market Dynamics

A tight US labor market drove retail average hourly earnings up 4.4% year-over-year in 2024, pressuring J. C. Penney’s recruitment and retention costs for store and warehouse staff.

Penney competes with retailers, gig platforms and logistics firms—Amazon’s U.S. warehousing workforce grew ~10% in 2023—raising wage benchmarks.

Investment in benefits and training is essential to maintain service quality but will increase operating expenses and labor margin pressure.

- Retail hourly wages +4.4% YoY (2024)

- Competition from gig/logistics firms; Amazon workforce +10% (2023)

- Higher benefits/training raise operating costs, squeezing margins

Real Estate and Mall Traffic Trends

The economic health of U.S. malls directly impacts J. C. Penney foot traffic and sales; national mall occupancy fell to about 88% in 2024 from 92% in 2019, pressuring store revenues.

With declining mall tenancy, JCP may renegotiate leases or relocate to off-mall strip centers; average mall rent concessions rose ~15% in 2023–24, improving relocation feasibility.

The 2026 strategy targets optimizing store footprint toward top MSAs—focusing on high-performing geographies that delivered ~70% of in-store sales in 2024.

- Declining mall occupancy: 88% (2024)

- Lease concessions up ~15% (2023–24)

- 70% of in-store sales from top MSAs (2024)

High rates and inflation shift shoppers to off‑price rivals, squeezing mall retailers

Inflation and high rates in 2024 cut discretionary spending (CPI +3.4%; Fed funds 5.25–5.50%), boosting demand for value channels; off‑price peers grew sales (TJX $52.5B, Ross $24.4B) eroding JCP comps (mid‑single‑digit declines). Wage inflation (+4.4% retail hourly pay) and mall occupancy declines (88% in 2024) squeeze margins and force footprint optimization.

| Metric | 2024 |

|---|---|

| US CPI | +3.4% |

| Fed funds | 5.25–5.50% |

| TJX net sales | $52.5B |

| Ross net sales | $24.4B |

| Retail wages | +4.4% YoY |

| Mall occupancy | 88% |

Same Document Delivered

J. C. Penney Company PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This PESTLE analysis of J. C. Penney covers political, economic, social, technological, legal, and environmental factors with concise insights and actionable implications. No placeholders or teasers—what you see is the final, professionally structured file available for immediate download.