JD.com Porter's Five Forces Analysis

From Overview to Strategy Blueprint

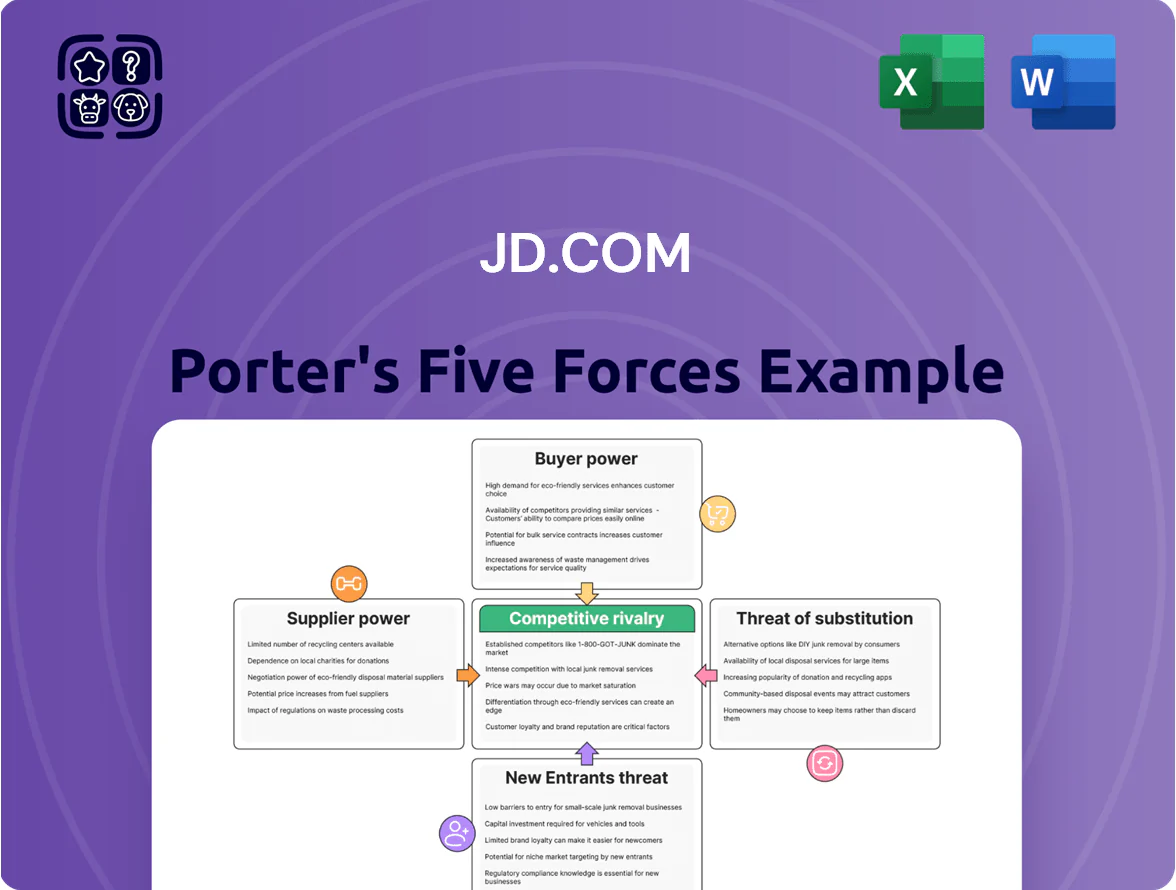

JD.com operates in a high-volume, low-margin e‑commerce landscape where supplier scale and logistics control limit supplier power, buyer bargaining is moderate due to strong brand and service, and intense rivalry plus high tech-driven switching raise competitive pressure.

Suppliers Bargaining Power

Dominance of Large Global Brands

Major electronics and luxury brands wield strong bargaining power at JD.com because offering Apple, Samsung, LVMH and similar names is key to JD’s premium image; in 2024 JD’s electronics GMV topped ¥500 billion, so these suppliers can demand prime placement and lower commission rates—often 1–3 percentage points below marketplace averages. JD must carefully balance concessions and purchase guarantees to secure authentic, high-demand stock and protect its brand reputation.

Fragmentation of Third-Party Merchants

The thousands of small and medium merchants on JD’s marketplace hold limited bargaining power; as of 2024 JD Retail hosted over 1.2 million active merchants, most single-digit sellers by GMV. These suppliers depend on JD’s 600+ million annual active users and its nationwide logistics network (over 1,400 warehouses in 2024), so JD can enforce strict service-level agreements and fee schedules. As a result, JD imposes platform fees and fulfillment terms with little risk of mass defection, since individual sellers account for small shares of total GMV.

Vertical Integration via JD Logistics

By running JD Logistics, JD.com cut reliance on third-party carriers—JD operated over 1,600 warehouses and 1,330 delivery stations by end-2024, handling ~60% of its last-mile orders in 2024, so supplier leverage fell sharply.

This vertical integration lets JD set terms for smaller regional carriers and partners, often dictating rates and service standards tied to platform volume.

Controlling fulfillment reduces exposure to supplier-driven price hikes: JD Logistics reported a 3.8% decline in per-order delivery cost in 2024 versus 2023, insulating margins.

Expansion into Private Label Products

JD.com has scaled private labels to 7% of GMV in 2024, using in-house brands to cut suppliers' leverage by offering comparable quality at lower prices.

Private labels let JD pressure branded suppliers to trim wholesale margins while JD captures higher retail margins and passes savings to customers, improving competitiveness.

Strict Quality Control and Authentication Standards

JD’s zero-tolerance counterfeit policy gives it leverage to force suppliers into strict quality and authentication standards, cutting platform fraud rates to 0.03% in 2024 per JD’s safety reports and reducing dispute costs by ~18% year-over-year.

Suppliers face vetting, on-site audits, and GS1/ISO product-traceability requirements to join JD, letting JD set operational norms and reject noncompliant vendors quickly.

- 0.03% counterfeit incidence (2024).

- ~18% lower dispute costs YoY (2023–2024).

- Mandatory GS1/ISO traceability and audits.

JD’s supplier power split: mega-brands dominate, mass merchants weakened by scale

Suppliers' power is mixed: top brands (Apple, Samsung, LVMH) exert strong leverage—electronics GMV >¥500bn (2024)—demanding favorable placement and lower commissions, while 1.2M+ small merchants (2024) have low leverage due to JD’s 600M+ users and 1,600+ warehouses. Vertical integration (JD Logistics handled ~60% last-mile, 2024) + 7% GMV private labels and 0.03% counterfeit rate (2024) reduce supplier bargaining power.

| Metric | 2024 |

|---|---|

| Electronics GMV | ¥500bn+ |

| Active merchants | 1.2M+ |

| Active users | 600M+ |

| JD warehouses | 1,600+ |

| Last-mile share | ~60% |

| Private labels | 7% GMV |

| Counterfeit rate | 0.03% |

What is included in the product

Tailored exclusively for JD.com, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping JD.com's pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for JD.com—swiftly highlights supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs across Platforms

Chinese shoppers face near-zero switching costs between JD.com, Alibaba (Taobao/Tmall), and Pinduoduo, so JD must continuously innovate and price competitively to retain users; in 2024 JD reported 587 million annual active users, yet lost market share to rivals.

High Price Sensitivity in Lower-Tier Cities

As JD.com pushes into smaller Chinese cities and rural areas, consumers show high price sensitivity—McKinsey estimated in 2024 that 60% of lower-tier shoppers compare prices across three or more apps before buying, giving them collective bargaining power.

JD must sustain subsidies and discount schemes: in FY2024 JD Group reported 233 billion RMB in promotions and logistics discounts, reflecting price-driven retention strategy in these segments.

Demand for Premium Logistics and Speed

JD’s customers expect same-day or next-day delivery as standard, and in 2024 JD Logistics handled over 70% of orders within 24 hours, cementing speed as a must-have.

That expectation gives customers bargaining power: a single delivery miss can drive them to Alibaba or Pinduoduo, shrinking JD’s active buyers—JD reported 580 million annual active customers in 2024.

JD must keep high logistics capex to meet demand; JD invested RMB 46.7 billion (≈ USD 6.8 billion) in logistics and fulfillment in 2024 to expand warehouses and last-mile networks.

Influence of Social Media and Reviews

Social media and JD’s review system make customer feedback highly visible, empowering users to shape JD.com’s reputation; in 2024, JD reported 580 million annual active customers, amplifying reach when reviews go viral.

A single viral negative post can hit sales fast in China’s digital market—Kantar found 63% of Chinese shoppers avoid brands after one bad social post—so JD must act quickly.

This collective power pushes JD to prioritize customer service and product quality, reflected in its 2024 net promoter improvements and lower return rates after faster dispute resolutions.

- 580M active customers (2024)

- 63% avoid brands after bad social post (Kantar, 2023)

- Faster dispute resolution cut returns in 2024

Availability of Comprehensive Product Information

With comparison tools and live-stream demos, customers entering JD.com are highly informed, cutting JD’s pricing power; a 2024 McKinsey survey found 62% of Chinese e-shoppers use comparison apps before buying, reducing brand-based premiums.

Information symmetry lets buyers demand lower prices and clearer specs, so JD reported 2024 gross merchandise volume (GMV) promotions up 9% year-over-year to stay competitive, forcing pricing transparency.

Retailers now must show exact specs, seller ratings, and dynamic prices in real time; missing transparency raises cart abandonment by up to 18% per 2023 UX studies.

- 62% use comparison apps (McKinsey 2024)

- JD 2024 GMV promotions +9% YoY

- 18% higher cart abandonment without clear specs (2023 UX)

JD under pressure: price, speed and transparency essential to retain 580M users

Customers hold strong bargaining power: near-zero switching costs and high price sensitivity forced JD to spend RMB 233B on promotions and RMB 46.7B logistics capex in 2024 while serving ~580M active users; 62% use comparison apps and 63% avoid brands after bad social posts, so JD must match price, speed (70% orders <24h) and transparency to retain buyers.

| Metric | 2024 |

|---|---|

| Active users | ~580M |

| Promotions | RMB 233B |

| Logistics capex | RMB 46.7B |

| Orders <24h | ~70% |

| Use comparison apps | 62% |

| Avoid after bad post | 63% |

Full Version Awaits

JD.com Porter's Five Forces Analysis

This preview shows the exact JD.com Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable: once payment is complete, you’ll get instant access to this same file. No mockups or samples—the preview is the final, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

JD.com operates in a high-volume, low-margin e‑commerce landscape where supplier scale and logistics control limit supplier power, buyer bargaining is moderate due to strong brand and service, and intense rivalry plus high tech-driven switching raise competitive pressure.

Suppliers Bargaining Power

Dominance of Large Global Brands

Major electronics and luxury brands wield strong bargaining power at JD.com because offering Apple, Samsung, LVMH and similar names is key to JD’s premium image; in 2024 JD’s electronics GMV topped ¥500 billion, so these suppliers can demand prime placement and lower commission rates—often 1–3 percentage points below marketplace averages. JD must carefully balance concessions and purchase guarantees to secure authentic, high-demand stock and protect its brand reputation.

Fragmentation of Third-Party Merchants

The thousands of small and medium merchants on JD’s marketplace hold limited bargaining power; as of 2024 JD Retail hosted over 1.2 million active merchants, most single-digit sellers by GMV. These suppliers depend on JD’s 600+ million annual active users and its nationwide logistics network (over 1,400 warehouses in 2024), so JD can enforce strict service-level agreements and fee schedules. As a result, JD imposes platform fees and fulfillment terms with little risk of mass defection, since individual sellers account for small shares of total GMV.

Vertical Integration via JD Logistics

By running JD Logistics, JD.com cut reliance on third-party carriers—JD operated over 1,600 warehouses and 1,330 delivery stations by end-2024, handling ~60% of its last-mile orders in 2024, so supplier leverage fell sharply.

This vertical integration lets JD set terms for smaller regional carriers and partners, often dictating rates and service standards tied to platform volume.

Controlling fulfillment reduces exposure to supplier-driven price hikes: JD Logistics reported a 3.8% decline in per-order delivery cost in 2024 versus 2023, insulating margins.

Expansion into Private Label Products

JD.com has scaled private labels to 7% of GMV in 2024, using in-house brands to cut suppliers' leverage by offering comparable quality at lower prices.

Private labels let JD pressure branded suppliers to trim wholesale margins while JD captures higher retail margins and passes savings to customers, improving competitiveness.

Strict Quality Control and Authentication Standards

JD’s zero-tolerance counterfeit policy gives it leverage to force suppliers into strict quality and authentication standards, cutting platform fraud rates to 0.03% in 2024 per JD’s safety reports and reducing dispute costs by ~18% year-over-year.

Suppliers face vetting, on-site audits, and GS1/ISO product-traceability requirements to join JD, letting JD set operational norms and reject noncompliant vendors quickly.

- 0.03% counterfeit incidence (2024).

- ~18% lower dispute costs YoY (2023–2024).

- Mandatory GS1/ISO traceability and audits.

JD’s supplier power split: mega-brands dominate, mass merchants weakened by scale

Suppliers' power is mixed: top brands (Apple, Samsung, LVMH) exert strong leverage—electronics GMV >¥500bn (2024)—demanding favorable placement and lower commissions, while 1.2M+ small merchants (2024) have low leverage due to JD’s 600M+ users and 1,600+ warehouses. Vertical integration (JD Logistics handled ~60% last-mile, 2024) + 7% GMV private labels and 0.03% counterfeit rate (2024) reduce supplier bargaining power.

| Metric | 2024 |

|---|---|

| Electronics GMV | ¥500bn+ |

| Active merchants | 1.2M+ |

| Active users | 600M+ |

| JD warehouses | 1,600+ |

| Last-mile share | ~60% |

| Private labels | 7% GMV |

| Counterfeit rate | 0.03% |

What is included in the product

Tailored exclusively for JD.com, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats shaping JD.com's pricing, profitability, and market positioning.

A concise Porter's Five Forces snapshot for JD.com—swiftly highlights supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Low Switching Costs across Platforms

Chinese shoppers face near-zero switching costs between JD.com, Alibaba (Taobao/Tmall), and Pinduoduo, so JD must continuously innovate and price competitively to retain users; in 2024 JD reported 587 million annual active users, yet lost market share to rivals.

High Price Sensitivity in Lower-Tier Cities

As JD.com pushes into smaller Chinese cities and rural areas, consumers show high price sensitivity—McKinsey estimated in 2024 that 60% of lower-tier shoppers compare prices across three or more apps before buying, giving them collective bargaining power.

JD must sustain subsidies and discount schemes: in FY2024 JD Group reported 233 billion RMB in promotions and logistics discounts, reflecting price-driven retention strategy in these segments.

Demand for Premium Logistics and Speed

JD’s customers expect same-day or next-day delivery as standard, and in 2024 JD Logistics handled over 70% of orders within 24 hours, cementing speed as a must-have.

That expectation gives customers bargaining power: a single delivery miss can drive them to Alibaba or Pinduoduo, shrinking JD’s active buyers—JD reported 580 million annual active customers in 2024.

JD must keep high logistics capex to meet demand; JD invested RMB 46.7 billion (≈ USD 6.8 billion) in logistics and fulfillment in 2024 to expand warehouses and last-mile networks.

Influence of Social Media and Reviews

Social media and JD’s review system make customer feedback highly visible, empowering users to shape JD.com’s reputation; in 2024, JD reported 580 million annual active customers, amplifying reach when reviews go viral.

A single viral negative post can hit sales fast in China’s digital market—Kantar found 63% of Chinese shoppers avoid brands after one bad social post—so JD must act quickly.

This collective power pushes JD to prioritize customer service and product quality, reflected in its 2024 net promoter improvements and lower return rates after faster dispute resolutions.

- 580M active customers (2024)

- 63% avoid brands after bad social post (Kantar, 2023)

- Faster dispute resolution cut returns in 2024

Availability of Comprehensive Product Information

With comparison tools and live-stream demos, customers entering JD.com are highly informed, cutting JD’s pricing power; a 2024 McKinsey survey found 62% of Chinese e-shoppers use comparison apps before buying, reducing brand-based premiums.

Information symmetry lets buyers demand lower prices and clearer specs, so JD reported 2024 gross merchandise volume (GMV) promotions up 9% year-over-year to stay competitive, forcing pricing transparency.

Retailers now must show exact specs, seller ratings, and dynamic prices in real time; missing transparency raises cart abandonment by up to 18% per 2023 UX studies.

- 62% use comparison apps (McKinsey 2024)

- JD 2024 GMV promotions +9% YoY

- 18% higher cart abandonment without clear specs (2023 UX)

JD under pressure: price, speed and transparency essential to retain 580M users

Customers hold strong bargaining power: near-zero switching costs and high price sensitivity forced JD to spend RMB 233B on promotions and RMB 46.7B logistics capex in 2024 while serving ~580M active users; 62% use comparison apps and 63% avoid brands after bad social posts, so JD must match price, speed (70% orders <24h) and transparency to retain buyers.

| Metric | 2024 |

|---|---|

| Active users | ~580M |

| Promotions | RMB 233B |

| Logistics capex | RMB 46.7B |

| Orders <24h | ~70% |

| Use comparison apps | 62% |

| Avoid after bad post | 63% |

Full Version Awaits

JD.com Porter's Five Forces Analysis

This preview shows the exact JD.com Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download and use the moment you buy. You're looking at the actual deliverable: once payment is complete, you’ll get instant access to this same file. No mockups or samples—the preview is the final, ready-to-use analysis.