JDE Peet's PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, supply-chain inflation, evolving consumer tastes, and sustainability mandates are reshaping JDE Peet's competitive landscape—our concise PESTLE highlights key risks and opportunities to inform strategy and investment calls. Purchase the full PESTLE for a detailed, actionable breakdown with editable charts and citations to use in reports, pitches, or board discussions.

Political factors

Geopolitical instability in sourcing and sales regions

Operating in over 100 countries, JDE Peet’s faces supply-chain and retail disruptions from regional conflicts; in 2024, logistics cost inflation contributed to a 6% rise in selling expenses, pressuring margins. Ongoing tensions in Eastern Europe and the Middle East have pushed energy and freight costs higher—European diesel prices averaged €1.70/l in 2024—raising roasting facility operating expenses. Management must manage political risk to secure green coffee access—global coffee prices rose ~18% in 2024—and protect growth in emerging markets that supplied ~22% of 2024 revenues.

EU Deforestation Regulation compliance

As a major EU-market player, JDE Peet's must comply with the EU Deforestation Regulation fully implemented by late 2025, requiring geolocation-level supplier mapping to verify coffee and cocoa are not from recently deforested land.

Non-compliance risks include fines up to 4% of global turnover and potential exclusion from a market generating ~55% of JDE Peet's 2024 revenue (~€4.1bn of €7.45bn), plus reputational and supply disruptions.

International trade policies and tariffs

Changes in trade agreements or new tariffs between major economies can raise JDE Peet's green coffee import costs; for example, a 5-10% tariff increase between EU and Brazil could add millions to COGS given the company’s 2024 green-bean purchases exceeding $1.2bn. Rising protectionism may push higher duties on processed coffee or roasting machinery, impacting margins in key markets. JDE Peet's monitors global trade relations and uses hedging, diversified sourcing and regional distribution to mitigate sudden policy shifts.

Governmental focus on sugar and health taxes

Political initiatives to combat obesity have led over 45 countries by 2025 to introduce or raise taxes on sugar-sweetened beverages and snacks, increasing excise rates by up to 20% in some markets.

JDE Peet's core roasted and instant coffee lines are often exempt, but ready-to-drink coffee and flavored teas face potential price-driven volume declines and margin pressure.

Reformulating products to reduce sugar—aligned with WHO and local guidelines—has become critical; reformulation investments can protect market share in taxed markets like the UK, Mexico and parts of Southeast Asia.

- 45+ countries with sugar taxes by 2025

- Up to 20% higher excise in some markets

- RTD coffee and flavored tea vulnerable to volume/margin loss

- Reformulation required to comply with health guidelines

Regulatory pressure on corporate transparency

Governments increasingly require social and governance reporting; EU CSRD expands scope to ~50,000 companies by 2026, affecting JDE Peet's disclosures on exec pay, tax and supply-chain human rights.

JDE Peet's must adapt to evolving transparency laws—detailed reporting on executive compensation, tax practices and human-rights due diligence—to satisfy stakeholders and avoid penalties.

Proactive policy engagement helps the company align with mandatory cycles and retain institutional investor confidence; 2024 stewardship codes cite ESG as key in 60-70% of voting guidelines.

- CSRD impact: ~50,000 EU firms by 2026

- Report areas: pay, tax, supply-chain human rights

- Investor focus: ESG in 60-70% of 2024 voting policies

Rising political costs: logistics, green‑bean spend and sugar taxes squeeze EU-dominant sales

Political risks (conflict, tariffs, regulation) raised 2024 costs: logistics +6% selling expenses, green-bean purchases >$1.2bn (+18% price), EU market ~55% revenue (€4.1bn/€7.45bn). EU Deforestation Reg. (full by 2025) and CSRD (≈50,000 firms by 2026) increase compliance; 45+ countries taxed sugar by 2025, excise up to +20% affecting RTD lines.

| Metric | 2024 |

|---|---|

| Logistics impact | +6% selling exp. |

| Green-bean spend | >$1.2bn |

| EU rev. | ~€4.1bn (55%) |

| Sugar tax | 45+ countries, up to +20% |

What is included in the product

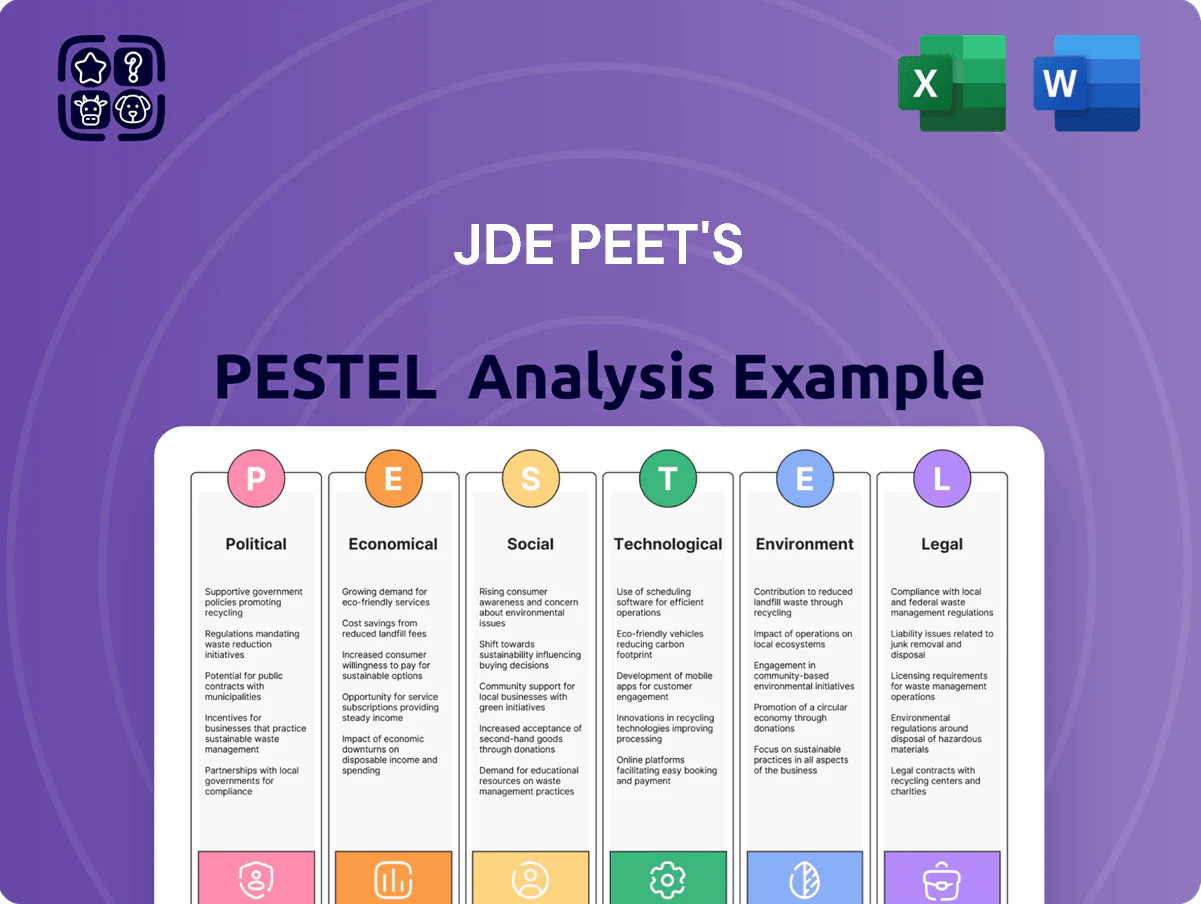

Explores how macro-environmental factors uniquely affect JDE Peet's across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to identify threats and opportunities for executives, investors, and strategists.

Condenses JDE Peet's PESTLE into a single, shareable summary that highlights external risks and opportunities for quick use in meetings or slide decks.

Economic factors

Volatility in green coffee commodity prices

Volatility in Arabica and Robusta prices—Arabica rose ~38% in 2023 while Robusta gained ~22%—driven by Brazil and Vietnam harvest swings and speculative trading, materially affects JDE Peet's COGS and margins. Economic disruptions in Brazil (2023 crop shortfalls) and Vietnam (2024 logistical bottlenecks) translate to price spikes for green beans. JDE Peet's offsets risk via hedging and long-term supplier contracts covering a significant share of volumes to stabilize retail pricing.

Global inflationary pressures on consumer spending

Persistent global inflation—CPI averaging around 5–6% in key markets through 2024—erodes discretionary income, pressuring premium coffee and out-of-home spend as consumers prioritize essentials.

Despite coffee resilience, prolonged downturns drive trade-downs to private-labels; NielsenIQ saw value-brand share gains of 1–2 ppt in 2023–24 in several European markets.

JDE Peet’s multi-tier brand strategy—from premium to mainstream and value—positions it to capture demand across price points and protect margins during varying economic cycles.

Currency exchange rate fluctuations

As a Dutch-headquartered group, JDE Peet's faces material FX risk as the euro fell ~2% vs. the USD in 2024 and emerging-market currencies averaged a 6–8% depreciation vs. EUR in 2023–24; revenues booked in weaker local currencies can shrink on consolidation while coffee, packaging and commodity inputs priced in USD raise cost pass-through risks. Treasury reports show active hedging—forward contracts and natural hedges—covering a significant portion of expected FX exposure to protect margins and the balance sheet.

Rising labor and operational costs

Tight labor markets in developed economies have pushed wages up across JDE Peet's manufacturing, logistics and retail channels, contributing to sector-wide cost inflation of about 4–6% in 2024 wage growth in Europe and North America.

Higher energy and freight costs—roasting energy intensity and 2023–24 European wholesale gas price spikes—added roughly 2–3% to cost of goods sold, pressuring margins.

JDE Peet's capital allocation toward automation and efficiency programs—reflected in ~€100–150m annual productivity investments in 2023–24—aims to offset these pressures and protect operating margins.

- Wage inflation: ~4–6% (2024 developed markets)

- Energy/freight impact: ~2–3% COGS uplift (2023–24)

- Productivity capex: ~€100–150m annually (2023–24)

Growth opportunities in emerging markets

Economic development and a rising middle class in Asia and Latin America—household consumption growth forecasted at 4–6% annually in key markets—boost demand for premium coffee and tea, offering JDE Peet's meaningful growth potential.

Urbanization and Westernized habits are increasing branded coffee penetration; Vietnam, Brazil and Mexico show double-digit retail value growth in specialty coffee in 2024–25.

JDE Peet's is reallocating capital to these regions to diversify revenue, aligning with reported 2024 investments and a target to lift emerging markets share above 25% of group sales.

- Rising middle class: 4–6% household spending growth

- Branded penetration: double-digit retail value growth (2024–25)

- Strategic aim: emerging markets >25% of sales

Rising coffee costs, inflation & wages squeeze margins as EM growth targets >25%

Price volatility (Arabica +38% 2023; Robusta +22%), CPI ~5–6% (2024), wage inflation ~4–6% (2024), energy/freight +2–3% COGS, productivity capex €100–150m (2023–24), emerging markets household growth 4–6% and target >25% sales.

| Metric | Value |

|---|---|

| Arabica/Robusta | +38% / +22% |

| CPI (key markets) | 5–6% |

| Wage growth | 4–6% |

| COGS energy/freight | +2–3% |

| Productivity capex | €100–150m |

| Emerging markets growth | 4–6%; >25% sales target |

Same Document Delivered

JDE Peet's PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of JDE Peet’s covering political, economic, social, technological, legal, and environmental factors. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises, with actionable insights for strategic and investment decisions. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, supply-chain inflation, evolving consumer tastes, and sustainability mandates are reshaping JDE Peet's competitive landscape—our concise PESTLE highlights key risks and opportunities to inform strategy and investment calls. Purchase the full PESTLE for a detailed, actionable breakdown with editable charts and citations to use in reports, pitches, or board discussions.

Political factors

Geopolitical instability in sourcing and sales regions

Operating in over 100 countries, JDE Peet’s faces supply-chain and retail disruptions from regional conflicts; in 2024, logistics cost inflation contributed to a 6% rise in selling expenses, pressuring margins. Ongoing tensions in Eastern Europe and the Middle East have pushed energy and freight costs higher—European diesel prices averaged €1.70/l in 2024—raising roasting facility operating expenses. Management must manage political risk to secure green coffee access—global coffee prices rose ~18% in 2024—and protect growth in emerging markets that supplied ~22% of 2024 revenues.

EU Deforestation Regulation compliance

As a major EU-market player, JDE Peet's must comply with the EU Deforestation Regulation fully implemented by late 2025, requiring geolocation-level supplier mapping to verify coffee and cocoa are not from recently deforested land.

Non-compliance risks include fines up to 4% of global turnover and potential exclusion from a market generating ~55% of JDE Peet's 2024 revenue (~€4.1bn of €7.45bn), plus reputational and supply disruptions.

International trade policies and tariffs

Changes in trade agreements or new tariffs between major economies can raise JDE Peet's green coffee import costs; for example, a 5-10% tariff increase between EU and Brazil could add millions to COGS given the company’s 2024 green-bean purchases exceeding $1.2bn. Rising protectionism may push higher duties on processed coffee or roasting machinery, impacting margins in key markets. JDE Peet's monitors global trade relations and uses hedging, diversified sourcing and regional distribution to mitigate sudden policy shifts.

Governmental focus on sugar and health taxes

Political initiatives to combat obesity have led over 45 countries by 2025 to introduce or raise taxes on sugar-sweetened beverages and snacks, increasing excise rates by up to 20% in some markets.

JDE Peet's core roasted and instant coffee lines are often exempt, but ready-to-drink coffee and flavored teas face potential price-driven volume declines and margin pressure.

Reformulating products to reduce sugar—aligned with WHO and local guidelines—has become critical; reformulation investments can protect market share in taxed markets like the UK, Mexico and parts of Southeast Asia.

- 45+ countries with sugar taxes by 2025

- Up to 20% higher excise in some markets

- RTD coffee and flavored tea vulnerable to volume/margin loss

- Reformulation required to comply with health guidelines

Regulatory pressure on corporate transparency

Governments increasingly require social and governance reporting; EU CSRD expands scope to ~50,000 companies by 2026, affecting JDE Peet's disclosures on exec pay, tax and supply-chain human rights.

JDE Peet's must adapt to evolving transparency laws—detailed reporting on executive compensation, tax practices and human-rights due diligence—to satisfy stakeholders and avoid penalties.

Proactive policy engagement helps the company align with mandatory cycles and retain institutional investor confidence; 2024 stewardship codes cite ESG as key in 60-70% of voting guidelines.

- CSRD impact: ~50,000 EU firms by 2026

- Report areas: pay, tax, supply-chain human rights

- Investor focus: ESG in 60-70% of 2024 voting policies

Rising political costs: logistics, green‑bean spend and sugar taxes squeeze EU-dominant sales

Political risks (conflict, tariffs, regulation) raised 2024 costs: logistics +6% selling expenses, green-bean purchases >$1.2bn (+18% price), EU market ~55% revenue (€4.1bn/€7.45bn). EU Deforestation Reg. (full by 2025) and CSRD (≈50,000 firms by 2026) increase compliance; 45+ countries taxed sugar by 2025, excise up to +20% affecting RTD lines.

| Metric | 2024 |

|---|---|

| Logistics impact | +6% selling exp. |

| Green-bean spend | >$1.2bn |

| EU rev. | ~€4.1bn (55%) |

| Sugar tax | 45+ countries, up to +20% |

What is included in the product

Explores how macro-environmental factors uniquely affect JDE Peet's across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to identify threats and opportunities for executives, investors, and strategists.

Condenses JDE Peet's PESTLE into a single, shareable summary that highlights external risks and opportunities for quick use in meetings or slide decks.

Economic factors

Volatility in green coffee commodity prices

Volatility in Arabica and Robusta prices—Arabica rose ~38% in 2023 while Robusta gained ~22%—driven by Brazil and Vietnam harvest swings and speculative trading, materially affects JDE Peet's COGS and margins. Economic disruptions in Brazil (2023 crop shortfalls) and Vietnam (2024 logistical bottlenecks) translate to price spikes for green beans. JDE Peet's offsets risk via hedging and long-term supplier contracts covering a significant share of volumes to stabilize retail pricing.

Global inflationary pressures on consumer spending

Persistent global inflation—CPI averaging around 5–6% in key markets through 2024—erodes discretionary income, pressuring premium coffee and out-of-home spend as consumers prioritize essentials.

Despite coffee resilience, prolonged downturns drive trade-downs to private-labels; NielsenIQ saw value-brand share gains of 1–2 ppt in 2023–24 in several European markets.

JDE Peet’s multi-tier brand strategy—from premium to mainstream and value—positions it to capture demand across price points and protect margins during varying economic cycles.

Currency exchange rate fluctuations

As a Dutch-headquartered group, JDE Peet's faces material FX risk as the euro fell ~2% vs. the USD in 2024 and emerging-market currencies averaged a 6–8% depreciation vs. EUR in 2023–24; revenues booked in weaker local currencies can shrink on consolidation while coffee, packaging and commodity inputs priced in USD raise cost pass-through risks. Treasury reports show active hedging—forward contracts and natural hedges—covering a significant portion of expected FX exposure to protect margins and the balance sheet.

Rising labor and operational costs

Tight labor markets in developed economies have pushed wages up across JDE Peet's manufacturing, logistics and retail channels, contributing to sector-wide cost inflation of about 4–6% in 2024 wage growth in Europe and North America.

Higher energy and freight costs—roasting energy intensity and 2023–24 European wholesale gas price spikes—added roughly 2–3% to cost of goods sold, pressuring margins.

JDE Peet's capital allocation toward automation and efficiency programs—reflected in ~€100–150m annual productivity investments in 2023–24—aims to offset these pressures and protect operating margins.

- Wage inflation: ~4–6% (2024 developed markets)

- Energy/freight impact: ~2–3% COGS uplift (2023–24)

- Productivity capex: ~€100–150m annually (2023–24)

Growth opportunities in emerging markets

Economic development and a rising middle class in Asia and Latin America—household consumption growth forecasted at 4–6% annually in key markets—boost demand for premium coffee and tea, offering JDE Peet's meaningful growth potential.

Urbanization and Westernized habits are increasing branded coffee penetration; Vietnam, Brazil and Mexico show double-digit retail value growth in specialty coffee in 2024–25.

JDE Peet's is reallocating capital to these regions to diversify revenue, aligning with reported 2024 investments and a target to lift emerging markets share above 25% of group sales.

- Rising middle class: 4–6% household spending growth

- Branded penetration: double-digit retail value growth (2024–25)

- Strategic aim: emerging markets >25% of sales

Rising coffee costs, inflation & wages squeeze margins as EM growth targets >25%

Price volatility (Arabica +38% 2023; Robusta +22%), CPI ~5–6% (2024), wage inflation ~4–6% (2024), energy/freight +2–3% COGS, productivity capex €100–150m (2023–24), emerging markets household growth 4–6% and target >25% sales.

| Metric | Value |

|---|---|

| Arabica/Robusta | +38% / +22% |

| CPI (key markets) | 5–6% |

| Wage growth | 4–6% |

| COGS energy/freight | +2–3% |

| Productivity capex | €100–150m |

| Emerging markets growth | 4–6%; >25% sales target |

Same Document Delivered

JDE Peet's PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of JDE Peet’s covering political, economic, social, technological, legal, and environmental factors. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises, with actionable insights for strategic and investment decisions. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.