JD Logistics PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

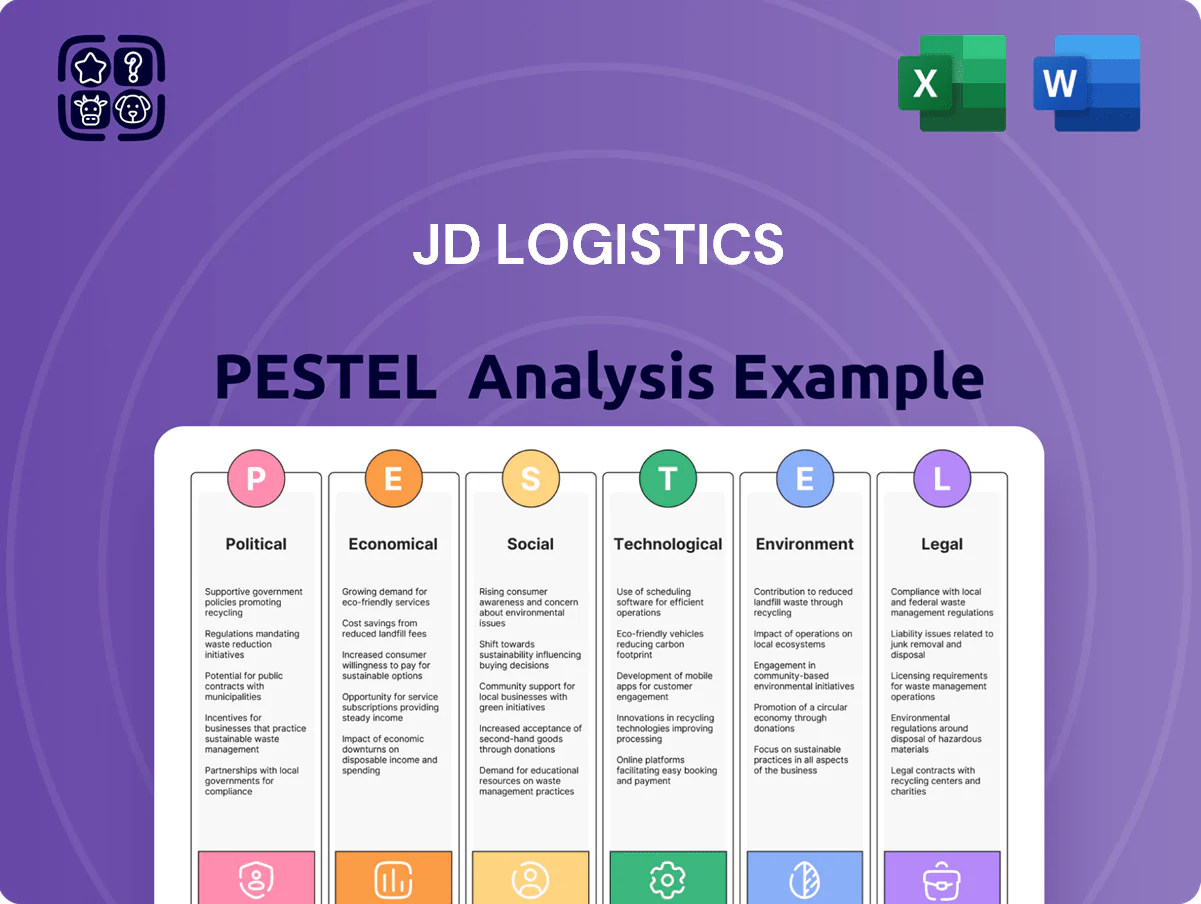

Our PESTLE Analysis of JD Logistics reveals how political shifts, economic cycles, technological innovation, and regulatory trends converge to shape its logistics strategy and competitive edge—use these insights to anticipate risks and spot growth opportunities. Purchase the full, fully editable report for a complete breakdown and actionable recommendations tailored for investors, strategists, and consultants.

Political factors

Government support for logistics infrastructure

Chinese government plans through 2025 prioritize a modern logistics system; state budgets committed about CNY 1.2 trillion to transport and logistics-related projects in 2023–2024, boosting JD Logistics' network reach.

State-led investment in transportation hubs and rural revitalization expands JD Logistics' serviceable market by supporting last-mile access to millions of households.

These initiatives target a reduction in social logistics costs from roughly 15% of GDP toward single digits, aligning with JD Logistics' integrated supply-chain efficiency and lowering unit delivery costs.

Regulatory oversight of platform economies

As a major tech-driven services player, JD Logistics faces evolving regulations on platform competition and market dominance; China’s antitrust fines totaled about CNY 197bn in 2022–2024, signaling continued oversight. The peak regulatory tightening has eased, but JD Logistics must proactively comply with fair competition rules to avoid penalties and ensure its integrated services do not undercut smaller logistics firms or third-party merchants.

Geopolitical trade tensions

Fluctuating China-West trade relations cut cross-border e-commerce volumes; Chinese exports to the EU fell 4.3% YoY in 2024, pressuring international freight demand and forcing JD Logistics to adjust capacity. Shifting tariffs and export controls raise unit costs—2024 trade barriers added an estimated 1.2–2.0% to logistics expenses for China-origin shipments—complicating hub expansion plans. JD mitigates regional political risk by diversifying routes and opening 12 new Southeast Asia gateways in 2024 to spread exposure.

Dual Circulation economic policy

China’s Dual Circulation policy, prioritizing domestic consumption while keeping trade open, benefits JD Logistics as retail consumption rose 5.4% YoY in 2025 Q4, boosting parcel volumes; JD Logistics reported 2025 revenue growth in logistics services of ~18% YoY.

By optimizing internal supply chains, JD Logistics aligns with the government aim to make domestic demand the mainstay, reducing dependency on export cycles and improving resilience.

The policy drives investment into high-end warehousing and cold chain: China cold-chain market reached ~RMB 430 billion in 2024, prompting JD Logistics to expand temperature-controlled capacity and premium fulfillment services.

- Domestic retail up 5.4% YoY (2025 Q4)

- JD Logistics logistics revenue growth ~18% YoY (2025)

- China cold-chain market ~RMB 430bn (2024)

Data sovereignty and security mandates

Political emphasis on national data security forces JD Logistics to implement rigorous data governance across its 1,000+ fulfillment centers, ensuring compliance with China’s Data Security Law and Personal Information Protection Law that mandate localized storage for critical infrastructure data.

Handling sensitive logistics and consumer behavior data tied to national infrastructure compels JD to align operations with state mandates, driving capital expenditure—JD reported RMB 17.6 billion in tech and infrastructure capex in 2024—into secure, localized cloud and encryption solutions.

- Compliance with China DSL and PIPL

- RMB 17.6bn 2024 tech/infrastructure capex

- Localized cloud storage for critical data

- Ongoing investment in encryption and governance

Policy-led transport boost fuels JD Logistics growth amid heavy compliance capex

Political support for transport (CNY 1.2tn 2023–24) and Dual Circulation lift domestic volumes (retail +5.4% YoY 2025 Q4), aiding JD Logistics revenue (+~18% logistics 2025) and cold-chain expansion (RMB 430bn market 2024); antitrust scrutiny (CNY 197bn fines 2022–24) and data-security laws (DSL, PIPL) force compliance and RMB 17.6bn tech/infrastructure capex (2024).

| Metric | Value |

|---|---|

| State transport spend | CNY 1.2tn (2023–24) |

| Retail growth | +5.4% (2025 Q4) |

| JD Logistics rev growth | ~+18% (2025) |

| Cold-chain market | RMB 430bn (2024) |

| Antitrust fines | CNY 197bn (2022–24) |

| Tech capex | RMB 17.6bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect JD Logistics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, sector-tailored PESTLE summary for JD Logistics that highlights key external risks and opportunities, designed for quick insertion into presentations or strategy sessions to streamline decision-making.

Economic factors

Post-pandemic consumption recovery patterns

By end-2025 China GDP growth is projected around 4.5% with consumption shifting to high-quality spending; JD Logistics pivots from volume-led fulfillment to value-added services such as white-glove delivery and integrated inventory solutions for premium brands, supporting higher margin contracts. The firm reported logistics revenue sensitivity to disposable income swings—China retail sales rose 6.7% y/y in 2024—so demand in APAC remains tied to consumer confidence and regional retail cycles.

Labor cost inflation and workforce availability

Rising wages in China—average urban non-private sector wages rose about 6.8% in 2024—inflate operating costs for traditional logistics providers, pressuring margins. JD Logistics is accelerating automation: by end-2024 it operated over 1,000 automated warehouses and expanded unmanned delivery pilots, cutting labor intensity. Balancing competitive courier pay (industry average delivery worker pay rose ~8% in 2024) with margin protection remains a top economic priority.

Fuel and energy price volatility

Fluctuations in global oil prices and rising electricity costs—Brent crude ranged 2023–2025 between about $70–95/bbl and China industrial electricity tariffs rose ~8% YoY in 2024—squeeze margins for transportation and cold-chain storage. JD Logistics reduces exposure by expanding a green fleet (over 10,000 EVs by end-2024) and using AI route optimization that cut fuel/electricity use ~12% in 2023 pilots. These efficiencies help sustain price competitiveness where shipping accounts for up to 40% of merchants’ logistics costs.

Interest rate environment and capital expenditure

The cost of borrowing directly influences JD Logistics ability to fund large-scale projects like the Asia No. 1 smart warehouses; China 1-year loan prime rate hovered around 3.65% in 2025, easing financing relative to 2022–23 peaks.

With rates stabilizing in 2024–25, JD Logistics can more reliably schedule long-term capital deployments to expand its physical network and optimize ROIC.

Robust strategic capital management is essential to sustain its heavy-asset model—in 2024 JD Logistics capex rose to about RMB 14.5 billion, underscoring the need for disciplined funding.

- Borrowing cost: LPR ~3.65% (2025)

- Capex 2024: ~RMB 14.5bn

- Heavy-asset model requires disciplined capital management

Growth of the integrated supply chain market

The global third-party logistics market grew to about USD 1.4 trillion in 2024, and outsourcing of complex supply-chain functions is driving enterprise demand that JD Logistics targets.

Enterprises shifting to integrated providers to improve capital turnover favor integrated solutions covering manufacturing logistics to last-mile delivery, allowing JD Logistics to win higher-margin, long-term contracts.

Integrated supply-chain contracts offer steadier revenue—enterprise logistics revenue streams fell less than 5% in downturns versus up to 20% for C2C parcel volumes in 2023–24—supporting JD Logistics’ revenue stability.

- 3rd-party logistics market ~USD 1.4T (2024)

- Enterprise contracts lower revenue volatility vs C2C (≈5% vs ≈20% downturn impact)

- Integrated services improve client capital turnover, boosting long-term, higher-margin deals

JD Logistics pivots to higher‑margin services, automation and disciplined capex amid China headwinds

Economic headwinds—China GDP ~4.5% (2025), retail sales +6.7% (2024), wage inflation ~6.8% (2024), LPR ~3.65% (2025)—shift JD Logistics toward higher-margin integrated services, automation (1,000+ automated warehouses, 10,000+ EVs) and disciplined capex (RMB 14.5bn 2024) to protect margins amid fuel/electricity cost pressure and a USD 1.4T 3PL market (2024).

| Metric | Value |

|---|---|

| China GDP (2025) | ~4.5% |

| Retail sales (2024) | +6.7% y/y |

| Wage inflation (2024) | ~6.8% |

| LPR (2025) | ~3.65% |

| Capex (2024) | RMB 14.5bn |

| 3PL market (2024) | USD 1.4T |

Same Document Delivered

JD Logistics PESTLE Analysis

The preview shown here is the exact JD Logistics PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get upon payment, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of JD Logistics reveals how political shifts, economic cycles, technological innovation, and regulatory trends converge to shape its logistics strategy and competitive edge—use these insights to anticipate risks and spot growth opportunities. Purchase the full, fully editable report for a complete breakdown and actionable recommendations tailored for investors, strategists, and consultants.

Political factors

Government support for logistics infrastructure

Chinese government plans through 2025 prioritize a modern logistics system; state budgets committed about CNY 1.2 trillion to transport and logistics-related projects in 2023–2024, boosting JD Logistics' network reach.

State-led investment in transportation hubs and rural revitalization expands JD Logistics' serviceable market by supporting last-mile access to millions of households.

These initiatives target a reduction in social logistics costs from roughly 15% of GDP toward single digits, aligning with JD Logistics' integrated supply-chain efficiency and lowering unit delivery costs.

Regulatory oversight of platform economies

As a major tech-driven services player, JD Logistics faces evolving regulations on platform competition and market dominance; China’s antitrust fines totaled about CNY 197bn in 2022–2024, signaling continued oversight. The peak regulatory tightening has eased, but JD Logistics must proactively comply with fair competition rules to avoid penalties and ensure its integrated services do not undercut smaller logistics firms or third-party merchants.

Geopolitical trade tensions

Fluctuating China-West trade relations cut cross-border e-commerce volumes; Chinese exports to the EU fell 4.3% YoY in 2024, pressuring international freight demand and forcing JD Logistics to adjust capacity. Shifting tariffs and export controls raise unit costs—2024 trade barriers added an estimated 1.2–2.0% to logistics expenses for China-origin shipments—complicating hub expansion plans. JD mitigates regional political risk by diversifying routes and opening 12 new Southeast Asia gateways in 2024 to spread exposure.

Dual Circulation economic policy

China’s Dual Circulation policy, prioritizing domestic consumption while keeping trade open, benefits JD Logistics as retail consumption rose 5.4% YoY in 2025 Q4, boosting parcel volumes; JD Logistics reported 2025 revenue growth in logistics services of ~18% YoY.

By optimizing internal supply chains, JD Logistics aligns with the government aim to make domestic demand the mainstay, reducing dependency on export cycles and improving resilience.

The policy drives investment into high-end warehousing and cold chain: China cold-chain market reached ~RMB 430 billion in 2024, prompting JD Logistics to expand temperature-controlled capacity and premium fulfillment services.

- Domestic retail up 5.4% YoY (2025 Q4)

- JD Logistics logistics revenue growth ~18% YoY (2025)

- China cold-chain market ~RMB 430bn (2024)

Data sovereignty and security mandates

Political emphasis on national data security forces JD Logistics to implement rigorous data governance across its 1,000+ fulfillment centers, ensuring compliance with China’s Data Security Law and Personal Information Protection Law that mandate localized storage for critical infrastructure data.

Handling sensitive logistics and consumer behavior data tied to national infrastructure compels JD to align operations with state mandates, driving capital expenditure—JD reported RMB 17.6 billion in tech and infrastructure capex in 2024—into secure, localized cloud and encryption solutions.

- Compliance with China DSL and PIPL

- RMB 17.6bn 2024 tech/infrastructure capex

- Localized cloud storage for critical data

- Ongoing investment in encryption and governance

Policy-led transport boost fuels JD Logistics growth amid heavy compliance capex

Political support for transport (CNY 1.2tn 2023–24) and Dual Circulation lift domestic volumes (retail +5.4% YoY 2025 Q4), aiding JD Logistics revenue (+~18% logistics 2025) and cold-chain expansion (RMB 430bn market 2024); antitrust scrutiny (CNY 197bn fines 2022–24) and data-security laws (DSL, PIPL) force compliance and RMB 17.6bn tech/infrastructure capex (2024).

| Metric | Value |

|---|---|

| State transport spend | CNY 1.2tn (2023–24) |

| Retail growth | +5.4% (2025 Q4) |

| JD Logistics rev growth | ~+18% (2025) |

| Cold-chain market | RMB 430bn (2024) |

| Antitrust fines | CNY 197bn (2022–24) |

| Tech capex | RMB 17.6bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect JD Logistics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, sector-tailored PESTLE summary for JD Logistics that highlights key external risks and opportunities, designed for quick insertion into presentations or strategy sessions to streamline decision-making.

Economic factors

Post-pandemic consumption recovery patterns

By end-2025 China GDP growth is projected around 4.5% with consumption shifting to high-quality spending; JD Logistics pivots from volume-led fulfillment to value-added services such as white-glove delivery and integrated inventory solutions for premium brands, supporting higher margin contracts. The firm reported logistics revenue sensitivity to disposable income swings—China retail sales rose 6.7% y/y in 2024—so demand in APAC remains tied to consumer confidence and regional retail cycles.

Labor cost inflation and workforce availability

Rising wages in China—average urban non-private sector wages rose about 6.8% in 2024—inflate operating costs for traditional logistics providers, pressuring margins. JD Logistics is accelerating automation: by end-2024 it operated over 1,000 automated warehouses and expanded unmanned delivery pilots, cutting labor intensity. Balancing competitive courier pay (industry average delivery worker pay rose ~8% in 2024) with margin protection remains a top economic priority.

Fuel and energy price volatility

Fluctuations in global oil prices and rising electricity costs—Brent crude ranged 2023–2025 between about $70–95/bbl and China industrial electricity tariffs rose ~8% YoY in 2024—squeeze margins for transportation and cold-chain storage. JD Logistics reduces exposure by expanding a green fleet (over 10,000 EVs by end-2024) and using AI route optimization that cut fuel/electricity use ~12% in 2023 pilots. These efficiencies help sustain price competitiveness where shipping accounts for up to 40% of merchants’ logistics costs.

Interest rate environment and capital expenditure

The cost of borrowing directly influences JD Logistics ability to fund large-scale projects like the Asia No. 1 smart warehouses; China 1-year loan prime rate hovered around 3.65% in 2025, easing financing relative to 2022–23 peaks.

With rates stabilizing in 2024–25, JD Logistics can more reliably schedule long-term capital deployments to expand its physical network and optimize ROIC.

Robust strategic capital management is essential to sustain its heavy-asset model—in 2024 JD Logistics capex rose to about RMB 14.5 billion, underscoring the need for disciplined funding.

- Borrowing cost: LPR ~3.65% (2025)

- Capex 2024: ~RMB 14.5bn

- Heavy-asset model requires disciplined capital management

Growth of the integrated supply chain market

The global third-party logistics market grew to about USD 1.4 trillion in 2024, and outsourcing of complex supply-chain functions is driving enterprise demand that JD Logistics targets.

Enterprises shifting to integrated providers to improve capital turnover favor integrated solutions covering manufacturing logistics to last-mile delivery, allowing JD Logistics to win higher-margin, long-term contracts.

Integrated supply-chain contracts offer steadier revenue—enterprise logistics revenue streams fell less than 5% in downturns versus up to 20% for C2C parcel volumes in 2023–24—supporting JD Logistics’ revenue stability.

- 3rd-party logistics market ~USD 1.4T (2024)

- Enterprise contracts lower revenue volatility vs C2C (≈5% vs ≈20% downturn impact)

- Integrated services improve client capital turnover, boosting long-term, higher-margin deals

JD Logistics pivots to higher‑margin services, automation and disciplined capex amid China headwinds

Economic headwinds—China GDP ~4.5% (2025), retail sales +6.7% (2024), wage inflation ~6.8% (2024), LPR ~3.65% (2025)—shift JD Logistics toward higher-margin integrated services, automation (1,000+ automated warehouses, 10,000+ EVs) and disciplined capex (RMB 14.5bn 2024) to protect margins amid fuel/electricity cost pressure and a USD 1.4T 3PL market (2024).

| Metric | Value |

|---|---|

| China GDP (2025) | ~4.5% |

| Retail sales (2024) | +6.7% y/y |

| Wage inflation (2024) | ~6.8% |

| LPR (2025) | ~3.65% |

| Capex (2024) | RMB 14.5bn |

| 3PL market (2024) | USD 1.4T |

Same Document Delivered

JD Logistics PESTLE Analysis

The preview shown here is the exact JD Logistics PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get upon payment, with no placeholders or surprises.