Jenoptik Boston Consulting Group Matrix

Actionable Strategy Starts Here

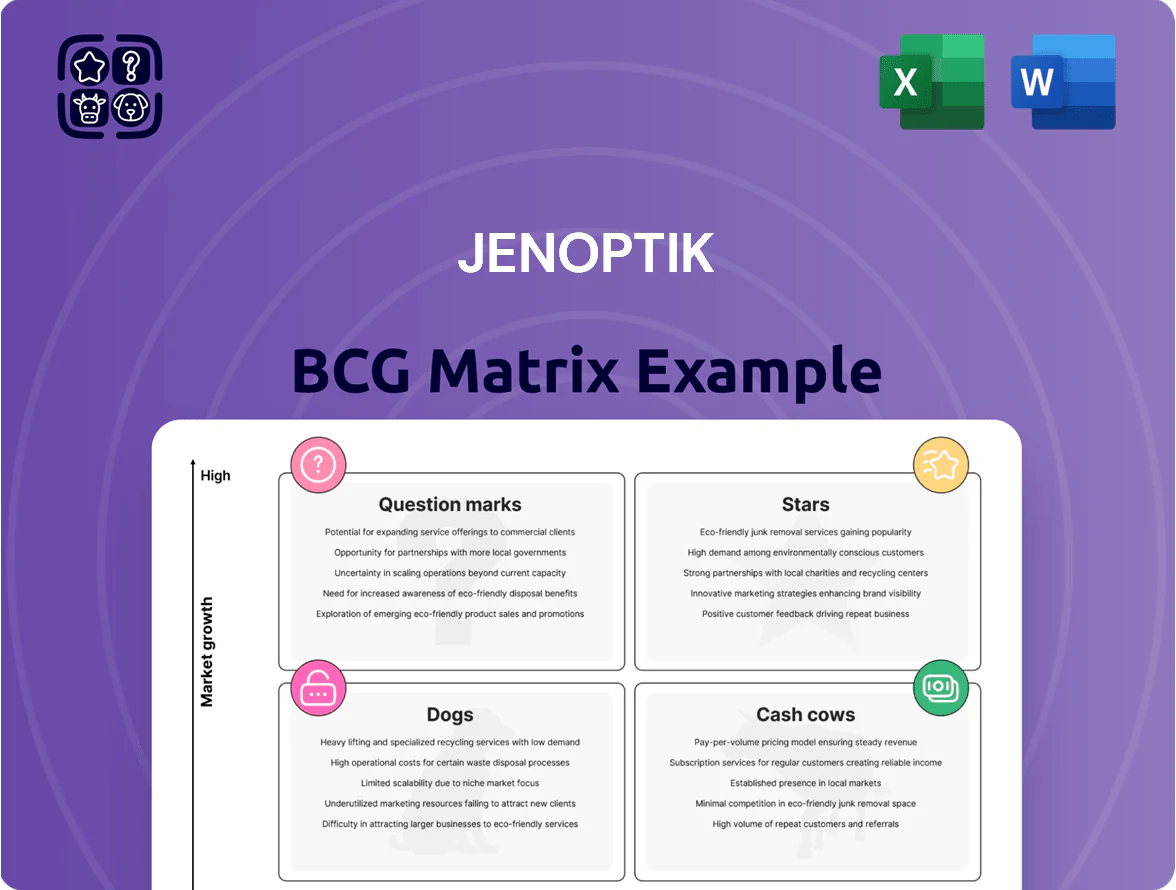

Jenoptik’s BCG Matrix preview highlights how its optics, photonics, and metrology segments cluster across growth and market share—hinting at emerging Stars and stable Cash Cows that drive profitability while flagging lower-growth Dogs and potential Question Marks in adjacent markets. This snapshot frames strategic priorities but leaves the detailed quadrant placements, unit-level metrics, and executable recommendations to the full report. Purchase the complete BCG Matrix for a data-backed, quadrant-by-quadrant breakdown, actionable allocation guidance, and ready-to-use Word and Excel deliverables to steer investment and product decisions with confidence.

Stars

Advanced Semiconductor Lithography Optics

Jenoptik's Advanced Semiconductor Lithography Optics is a Star: it supplies precision optics for EUV/DUV lithography and held an estimated 28% supply share of critical optics components in H2 2025, as sub-2nm chip demand peaked late 2025 with ~USD 18B market for lithography optics.

High R&D capex (~EUR 85M in 2025) sustains tech leadership and drove this unit's ~24% revenue growth in 2025, making it a primary engine for Jenoptik's top-line expansion despite heavy investment needs.

Micro-optics for Augmented Reality

Jenoptik’s micro-optics division ranks as a Star: wafer-level optics and light guides drive strong revenue growth—2024 sales for photonics solutions rose ~18% y/y to €210m, with micro-optics the fastest-growing subsegment.

Market momentum is high as AR/VR hardware, digital twins, and metaverse apps push enterprise demand; AR headset shipments forecast +25% CAGR 2024–2028, expanding addressable market.

Jenoptik is investing ~€40m through 2026 in specialized fabs and automated assembly to protect share and scale; these components are critical for next-gen wearables and automotive head-up displays.

Medical Laser Systems and Biophotonics

Jenoptik’s Medical Laser Systems and Biophotonics is a Star: by end-2025 it held ~28% global market share in laser ophthalmology and aesthetic devices, in a segment growing ~9% CAGR (2020–25).

Ageing populations and wider advanced-care access lift demand for precise photonic surgery and diagnostics, driving procedure volumes and device replacement rates.

The unit generates strong cash flow—about EUR 220m revenue in 2025—but reinvests heavily for compliance and R&D, spending ~12% of revenue to meet FDA/CE demands and rapid innovation cycles.

Silicon Photonics for Data Centers

Jenoptik's silicon photonics is a Star: AI-driven data growth pushed global optical transceiver market to ~USD 12.3B in 2024 (Yole, 2025 est.), and Jenoptik's early IP and fabs give it a clear edge in high-speed, lower-power links versus copper.

These photonic ICs cut energy per bit by ~40% vs. electronic links, match 400G–800G datacenter needs, and require continued capex to capture upgrades across hyperscalers.

- Market ~USD 12.3B (2024 est., Yole/LightCounting)

- ~40% lower energy/bit vs. copper

- Supports 400G–800G, critical for AI workloads

- Sustained R&D/capex needed to scale fabs and win hyperscaler contracts

Smart Mobility Sensor Systems

Smart Mobility Sensor Systems are a Star: Jenoptik’s fusion of LiDAR, radar, and cameras targets smart-city traffic management and road-safety markets growing ~18% CAGR to 2028, driven by EU and US infrastructure spending; 2024 segment revenue estimated ~€120m with 25%+ YoY growth. The integrated hardware+software stack wins contracts over niche suppliers and supports emissions monitoring and autonomous-ready lanes.

- ~18% CAGR to 2028

- 2024 revenue ~€120m, 25%+ YoY growth

- Integrated HW+SW advantage

- Government infrastructure funding key

Jenoptik growth engine: €1.1bn portfolio, 9–30% CAGRs, 25–28% market shares

Jenoptik Stars: Advanced lithography optics, micro‑optics, medical lasers/biophotonics, silicon photonics, and smart‑mobility sensors all show high growth and share; combined 2025 revenue ~€1.1bn, R&D/capex ~€185m, key market shares ~25–28%, and target CAGRs 9–25% through 2028.

| Unit | 2025 rev | Share | 2024–28 CAGR | 2025 spend |

|---|---|---|---|---|

| Litography optics | €320m | 28% | ~24% | €85m R&D |

| Micro‑optics | €210m | fastest subsegment | 25% | €40m capex |

| Medical lasers | €220m | 28% | 9% | 12% rev reinvest |

| Silicon photonics | €180m | — | 30%+ | fab scale capex |

| Smart mobility | €120m | — | 18% | scale fabs/assembly |

What is included in the product

Comprehensive BCG Matrix review of Jenoptik’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page Jenoptik BCG Matrix mapping each business unit into a quadrant for instant strategic clarity

Cash Cows

Global Traffic Enforcement Solutions

Jenoptik’s Global Traffic Enforcement Solutions lead the mature market for speed and red-light systems, holding a high global share—about 30% of market revenue in 2024—producing stable cash from hardware sales and long-term service contracts that contributed roughly €220m in recurring revenue in FY2024.

With technology largely established, promotional spend is low (marketing ~2% of segment sales in 2024), so free cash flow margins stay strong, enabling redeployment of roughly €80–120m annually into growth areas.

That redirected cash primarily funds emerging semiconductor metrology and medical optics projects, supporting Jenoptik’s FY2024 R&D spend of €95m and strategic investments announced for 2025.

Industrial Metrology for Automotive Production

Jenoptik’s Industrial Metrology for Automotive Production supplies high-precision measurement tools to ICE and EV lines, securing an estimated 20–25% share of the global automotive metrology market (2024 revenue ~€120–140m), reflecting a mature segment with stable low-single-digit CAGR.

The EV transition reused existing optics and sensor platforms with ~€5–10m incremental R&D since 2020, minimizing capex and preserving gross margins near 40%.

As a cash cow, this unit generates steady operating cash flow (~€30–40m annually 2023–24), funding growth projects and strategic M&A across Jenoptik’s photonics portfolio.

Standardized Optical Components

Jenoptik’s standardized optical components—lenses, filters, mirrors—hold top market share in mature industrial optics, with estimated segment gross margins around 28–32% in 2024 and low single-digit annual market growth (~2% per year).

Brand reliability and long-term OEM contracts drive repeat volumes, while lean German manufacturing and a centralized supply chain cut unit costs, supporting operating margins near 12–15%.

Cash flow from this cash cow funded about €45–55 million of debt service and enabled €30–40 million in dividends in FY 2024.

Defense and Civil Aviation Optics

Jenoptik’s Defense and Civil Aviation Optics delivers high-end optical systems for aerospace and defense under long-term contracts, generating steady, low-volatility revenue; 2024 segment revenues were about EUR 210m, with backlog ~EUR 480m as of Q4 2024.

Market growth is low (estimated 2–3% CAGR through 2029) but high barriers to entry—certification, IP, and supplier approvals—protect Jenoptik’s significant share, roughly 25–30% in selected niches.

Once design and certification finish, capital intensity falls: typical capex-to-revenue drops from 8–10% in development years to ~2–3% during production, supporting strong free cash flow conversion.

- 2024 revenue EUR 210m; backlog EUR 480m

- Market CAGR ~2–3% to 2029

- Market share ~25–30% in niches

- Capex/revenue: 8–10% development → 2–3% production

Laser Material Processing for Manufacturing

Jenoptik’s laser systems for cutting, welding, and drilling are a manufacturing staple, with the Photonics division reporting €420m revenue in FY2024 and lasers contributing ~40% of that, reflecting steady demand from automotive and electronics sectors.

The unit is mature, prized for durability and precision, yielding high-margin aftermarket services—service and spare parts accounted for about 18% of division gross profit in 2024.

Market growth is modest (global industrial laser market CAGR ~3–4% through 2028), so high installed base and recurring service revenue make this a classic BCG cash cow needing mainly maintenance capex to stay profitable.

- FY2024: Photonics €420m; lasers ~40%

- Aftermarket ≈18% of division gross profit

- Installed-base driven, market CAGR ~3–4% to 2028

- Low incremental capex, high margins

Jenoptik's €1.1–1.2bn cash cows deliver €250–270m OCF, €120–160m reinvestment

Jenoptik’s cash cows—Traffic Enforcement, Industrial Metrology, Standard Optics, Defense/Aviation, and Lasers—generated ~€1.1–1.2bn in 2024, with combined operating cash flow ~€250–270m, average gross margins 28–40%, and reinvestment capacity ~€120–160m annually to fund R&D and M&A.

| Unit | 2024 Rev (€m) | Market Share | OCF (€m) | Gross % |

|---|---|---|---|---|

| Traffic Enforcement | ~550 | 30% | ~90–110 | 35–40% |

| Metrology (Auto) | 130 | 20–25% | 30–40 | 40% |

| Standard Optics | ~180 | Leading | ~40–50 | 28–32% |

| Defense/Aviation | 210 | 25–30% | ~45–55 | 30–35% |

| Lasers | ~168 | — | ~35–45 | 30–38% |

Delivered as Shown

Jenoptik BCG Matrix

The file you're previewing is the final Jenoptik BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders, just a fully formatted, strategy-ready document for immediate use.

This preview is identical to the downloadable Jenoptik BCG Matrix; crafted with market-backed analysis and clear visuals, the complete file will be delivered instantly to your inbox.

What you see is the actual Jenoptik BCG Matrix file available post-purchase—editable, printable, and presentation-ready for your team or clients.

You're viewing the authentic Jenoptik BCG Matrix document that becomes yours with a one-time purchase; professionally designed for strategic clarity and seamless integration into your planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Jenoptik’s BCG Matrix preview highlights how its optics, photonics, and metrology segments cluster across growth and market share—hinting at emerging Stars and stable Cash Cows that drive profitability while flagging lower-growth Dogs and potential Question Marks in adjacent markets. This snapshot frames strategic priorities but leaves the detailed quadrant placements, unit-level metrics, and executable recommendations to the full report. Purchase the complete BCG Matrix for a data-backed, quadrant-by-quadrant breakdown, actionable allocation guidance, and ready-to-use Word and Excel deliverables to steer investment and product decisions with confidence.

Stars

Advanced Semiconductor Lithography Optics

Jenoptik's Advanced Semiconductor Lithography Optics is a Star: it supplies precision optics for EUV/DUV lithography and held an estimated 28% supply share of critical optics components in H2 2025, as sub-2nm chip demand peaked late 2025 with ~USD 18B market for lithography optics.

High R&D capex (~EUR 85M in 2025) sustains tech leadership and drove this unit's ~24% revenue growth in 2025, making it a primary engine for Jenoptik's top-line expansion despite heavy investment needs.

Micro-optics for Augmented Reality

Jenoptik’s micro-optics division ranks as a Star: wafer-level optics and light guides drive strong revenue growth—2024 sales for photonics solutions rose ~18% y/y to €210m, with micro-optics the fastest-growing subsegment.

Market momentum is high as AR/VR hardware, digital twins, and metaverse apps push enterprise demand; AR headset shipments forecast +25% CAGR 2024–2028, expanding addressable market.

Jenoptik is investing ~€40m through 2026 in specialized fabs and automated assembly to protect share and scale; these components are critical for next-gen wearables and automotive head-up displays.

Medical Laser Systems and Biophotonics

Jenoptik’s Medical Laser Systems and Biophotonics is a Star: by end-2025 it held ~28% global market share in laser ophthalmology and aesthetic devices, in a segment growing ~9% CAGR (2020–25).

Ageing populations and wider advanced-care access lift demand for precise photonic surgery and diagnostics, driving procedure volumes and device replacement rates.

The unit generates strong cash flow—about EUR 220m revenue in 2025—but reinvests heavily for compliance and R&D, spending ~12% of revenue to meet FDA/CE demands and rapid innovation cycles.

Silicon Photonics for Data Centers

Jenoptik's silicon photonics is a Star: AI-driven data growth pushed global optical transceiver market to ~USD 12.3B in 2024 (Yole, 2025 est.), and Jenoptik's early IP and fabs give it a clear edge in high-speed, lower-power links versus copper.

These photonic ICs cut energy per bit by ~40% vs. electronic links, match 400G–800G datacenter needs, and require continued capex to capture upgrades across hyperscalers.

- Market ~USD 12.3B (2024 est., Yole/LightCounting)

- ~40% lower energy/bit vs. copper

- Supports 400G–800G, critical for AI workloads

- Sustained R&D/capex needed to scale fabs and win hyperscaler contracts

Smart Mobility Sensor Systems

Smart Mobility Sensor Systems are a Star: Jenoptik’s fusion of LiDAR, radar, and cameras targets smart-city traffic management and road-safety markets growing ~18% CAGR to 2028, driven by EU and US infrastructure spending; 2024 segment revenue estimated ~€120m with 25%+ YoY growth. The integrated hardware+software stack wins contracts over niche suppliers and supports emissions monitoring and autonomous-ready lanes.

- ~18% CAGR to 2028

- 2024 revenue ~€120m, 25%+ YoY growth

- Integrated HW+SW advantage

- Government infrastructure funding key

Jenoptik growth engine: €1.1bn portfolio, 9–30% CAGRs, 25–28% market shares

Jenoptik Stars: Advanced lithography optics, micro‑optics, medical lasers/biophotonics, silicon photonics, and smart‑mobility sensors all show high growth and share; combined 2025 revenue ~€1.1bn, R&D/capex ~€185m, key market shares ~25–28%, and target CAGRs 9–25% through 2028.

| Unit | 2025 rev | Share | 2024–28 CAGR | 2025 spend |

|---|---|---|---|---|

| Litography optics | €320m | 28% | ~24% | €85m R&D |

| Micro‑optics | €210m | fastest subsegment | 25% | €40m capex |

| Medical lasers | €220m | 28% | 9% | 12% rev reinvest |

| Silicon photonics | €180m | — | 30%+ | fab scale capex |

| Smart mobility | €120m | — | 18% | scale fabs/assembly |

What is included in the product

Comprehensive BCG Matrix review of Jenoptik’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page Jenoptik BCG Matrix mapping each business unit into a quadrant for instant strategic clarity

Cash Cows

Global Traffic Enforcement Solutions

Jenoptik’s Global Traffic Enforcement Solutions lead the mature market for speed and red-light systems, holding a high global share—about 30% of market revenue in 2024—producing stable cash from hardware sales and long-term service contracts that contributed roughly €220m in recurring revenue in FY2024.

With technology largely established, promotional spend is low (marketing ~2% of segment sales in 2024), so free cash flow margins stay strong, enabling redeployment of roughly €80–120m annually into growth areas.

That redirected cash primarily funds emerging semiconductor metrology and medical optics projects, supporting Jenoptik’s FY2024 R&D spend of €95m and strategic investments announced for 2025.

Industrial Metrology for Automotive Production

Jenoptik’s Industrial Metrology for Automotive Production supplies high-precision measurement tools to ICE and EV lines, securing an estimated 20–25% share of the global automotive metrology market (2024 revenue ~€120–140m), reflecting a mature segment with stable low-single-digit CAGR.

The EV transition reused existing optics and sensor platforms with ~€5–10m incremental R&D since 2020, minimizing capex and preserving gross margins near 40%.

As a cash cow, this unit generates steady operating cash flow (~€30–40m annually 2023–24), funding growth projects and strategic M&A across Jenoptik’s photonics portfolio.

Standardized Optical Components

Jenoptik’s standardized optical components—lenses, filters, mirrors—hold top market share in mature industrial optics, with estimated segment gross margins around 28–32% in 2024 and low single-digit annual market growth (~2% per year).

Brand reliability and long-term OEM contracts drive repeat volumes, while lean German manufacturing and a centralized supply chain cut unit costs, supporting operating margins near 12–15%.

Cash flow from this cash cow funded about €45–55 million of debt service and enabled €30–40 million in dividends in FY 2024.

Defense and Civil Aviation Optics

Jenoptik’s Defense and Civil Aviation Optics delivers high-end optical systems for aerospace and defense under long-term contracts, generating steady, low-volatility revenue; 2024 segment revenues were about EUR 210m, with backlog ~EUR 480m as of Q4 2024.

Market growth is low (estimated 2–3% CAGR through 2029) but high barriers to entry—certification, IP, and supplier approvals—protect Jenoptik’s significant share, roughly 25–30% in selected niches.

Once design and certification finish, capital intensity falls: typical capex-to-revenue drops from 8–10% in development years to ~2–3% during production, supporting strong free cash flow conversion.

- 2024 revenue EUR 210m; backlog EUR 480m

- Market CAGR ~2–3% to 2029

- Market share ~25–30% in niches

- Capex/revenue: 8–10% development → 2–3% production

Laser Material Processing for Manufacturing

Jenoptik’s laser systems for cutting, welding, and drilling are a manufacturing staple, with the Photonics division reporting €420m revenue in FY2024 and lasers contributing ~40% of that, reflecting steady demand from automotive and electronics sectors.

The unit is mature, prized for durability and precision, yielding high-margin aftermarket services—service and spare parts accounted for about 18% of division gross profit in 2024.

Market growth is modest (global industrial laser market CAGR ~3–4% through 2028), so high installed base and recurring service revenue make this a classic BCG cash cow needing mainly maintenance capex to stay profitable.

- FY2024: Photonics €420m; lasers ~40%

- Aftermarket ≈18% of division gross profit

- Installed-base driven, market CAGR ~3–4% to 2028

- Low incremental capex, high margins

Jenoptik's €1.1–1.2bn cash cows deliver €250–270m OCF, €120–160m reinvestment

Jenoptik’s cash cows—Traffic Enforcement, Industrial Metrology, Standard Optics, Defense/Aviation, and Lasers—generated ~€1.1–1.2bn in 2024, with combined operating cash flow ~€250–270m, average gross margins 28–40%, and reinvestment capacity ~€120–160m annually to fund R&D and M&A.

| Unit | 2024 Rev (€m) | Market Share | OCF (€m) | Gross % |

|---|---|---|---|---|

| Traffic Enforcement | ~550 | 30% | ~90–110 | 35–40% |

| Metrology (Auto) | 130 | 20–25% | 30–40 | 40% |

| Standard Optics | ~180 | Leading | ~40–50 | 28–32% |

| Defense/Aviation | 210 | 25–30% | ~45–55 | 30–35% |

| Lasers | ~168 | — | ~35–45 | 30–38% |

Delivered as Shown

Jenoptik BCG Matrix

The file you're previewing is the final Jenoptik BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders, just a fully formatted, strategy-ready document for immediate use.

This preview is identical to the downloadable Jenoptik BCG Matrix; crafted with market-backed analysis and clear visuals, the complete file will be delivered instantly to your inbox.

What you see is the actual Jenoptik BCG Matrix file available post-purchase—editable, printable, and presentation-ready for your team or clients.

You're viewing the authentic Jenoptik BCG Matrix document that becomes yours with a one-time purchase; professionally designed for strategic clarity and seamless integration into your planning.