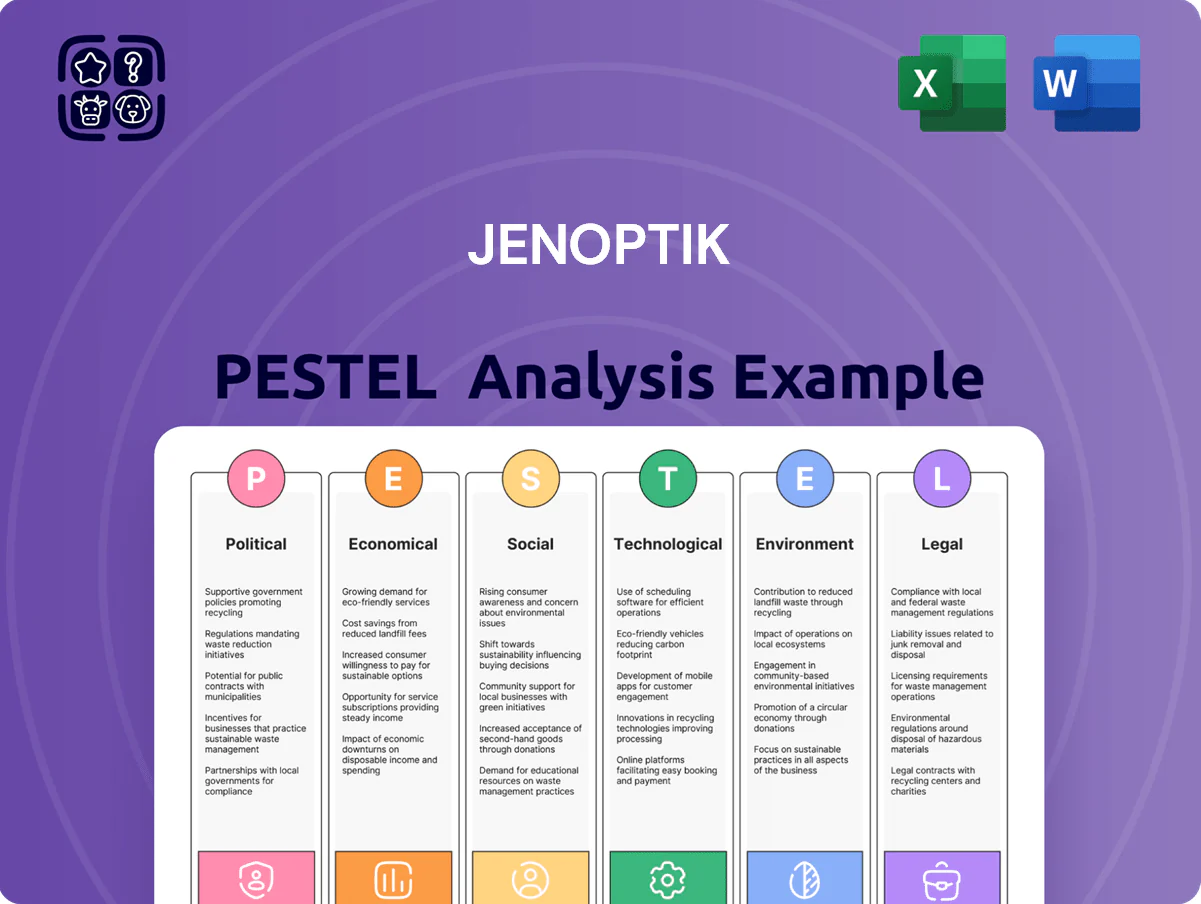

Jenoptik PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, supply-chain dynamics, and rapid optics-tech innovation are shaping Jenoptik’s strategic horizon—our concise PESTLE highlights key risks and opportunities you need now. Purchase the full PESTLE for a sector‑specific, actionable breakdown and downloadable templates to inform investment decisions and strategic planning instantly.

Political factors

Trade Protectionism and Export Controls

The global photonics sector faces rising export controls: since 2022 restrictions on semiconductor equipment have expanded, with US-led curbs affecting shipments worth an estimated $20–30bn annually; Jenoptik, a supplier to chipmakers, must navigate EU, US and Chinese rules to retain access to markets that drove 2024 photonics demand growth of ~8%.

European Semiconductor Sovereignty

The EU Chips Act targets 20% of global semiconductor production in Europe by 2030 and mobilizes over EUR 43 billion in public and private investment; Jenoptik gains from subsidies and R&D grants tied to these programs that reduce supply-chain reliance.

Geopolitical Tensions in the Asia-Pacific

Ongoing instability in the Asia-Pacific threatens optics manufacturing and distribution; trade along the Taiwan Strait and South China Sea accounts for roughly 30% of global semiconductor shipments, elevating supply-chain risk for Jenoptik’s optics and photonics components.

Disruptions could affect raw-material flows and major electronics customers—Taiwan supplies ~60% of advanced chips—potentially hitting revenue tied to Asia sales, which were about 22% of Jenoptik’s 2024 group revenue.

Jenoptik closely monitors developments, maintains contingency plans, and is diversifying production and supplier bases across Europe and Southeast Asia to reduce concentration risk.

Defense and Security Spending Shifts

Shifts in national defense budgets—NATO defense spending rose to 2.2% of GDP on average in 2024, with EU members increasing procurement—boost demand for Jenoptik’s sensing and surveillance optics used in reconnaissance and border security.

Geopolitical tensions in 2024–25 drove higher procurement: German defense procurement rose 18% YoY in 2024, underpinning near-term revenue visibility for defense-focused product lines.

Alignment with NATO and allied procurement standards remains crucial for Jenoptik’s long-term contracts, export approvals, and revenue stability across defense portfolios.

- 2024 NATO avg defense spend 2.2% GDP

- Germany procurement +18% YoY 2024

- Higher border-security procurements boost optics demand

- NATO alignment critical for export/contracts

Global Trade Agreements and Tariffs

The implementation of new trade agreements or retaliatory tariffs can shift Jenoptik’s international cost base; for example, a 10% tariff on optical components could raise COGS materially given components accounted for ~32% of 2024 production input costs.

Trade disputes between major economies risk duties on laser systems—Jenoptik booked €1.1bn revenue in 2024, so even 2–3% margin pressure from tariffs would cut EBITDA by €22–33m.

Navigating fiscal hurdles requires flexible sourcing, nearshoring, and proactive engagement with trade policymakers to preserve competitive pricing and supply continuity.

- Tariff sensitivity: 2–3% EBITDA downside per modest tariff rise

- Input concentration: ~32% of production inputs from specialized suppliers (2024)

- Revenue exposure: €1.1bn global revenue (2024)

- Mitigation: diversify suppliers, nearshoring, policy engagement

Geopolitics Bite: Export Curbs, Tariffs Risk €22–33m EBITDA as Asia & Supply Chains Strain

Political risks include export controls (US-led curbs since 2022 impacting $20–30bn of semiconductor equipment) constraining Jenoptik’s market access; EU Chips Act (EUR 43bn) and German defense procurement (+18% YoY 2024) boost subsidies and defense demand; Asia-Pacific tensions threaten supply chains (Taiwan ~60% advanced chips) vs. 22% revenue exposure in Asia (2024); tariffs could cut EBITDA 2–3% (€22–33m on €1.1bn revenue).

| Metric | Value (2024/2025) |

|---|---|

| Group revenue | €1.1bn |

| Asia revenue share | 22% |

| Tariff EBITDA hit | 2–3% (€22–33m) |

| Input concentration | 32% of production costs |

| NATO avg defense spend | 2.2% GDP (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Jenoptik across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights tailored to its optics, photonics, and defense-adjacent markets to support strategic planning and investor communications.

A concise Jenoptik PESTLE summary that highlights regulatory, technological, and market risks in plain language for quick inclusion in presentations or strategy sessions, easily shared across teams and annotated with region- or division-specific notes.

Economic factors

Semiconductor Market Volatility

The cyclical semiconductor industry strongly influences Jenoptik’s revenue as a key equipment supplier, with global chip capex swinging—IC Insights reported 2024 fab equipment spending at about $91bn after a 2023 trough—causing quarters of reduced orders when consumer electronics demand softens. Long-term chip demand (IDC forecasts ~6–8% CAGR 2024–2029) supports sustained need for tools, but short-term volatility pressures near-term cash flow. Jenoptik mitigates this by diversifying into medical tech and smart mobility, where FY2024 reported group revenue of €1.02bn and growing service contracts that smooth cyclicality.

Global Inflationary Pressures

Persistently high inflation across major economies—with Euro area CPI at 5.3% and US CPI at 3.4% in 2024—elevates costs for Jenoptik’s specialized materials, energy and skilled labor.

Jenoptik must balance rising operational costs against competitive pricing to protect margins in a crowded global market.

Effective cost management and inclusion of price escalation clauses in long-term contracts are essential tools to navigate these headwinds through 2025.

Currency Exchange Rate Fluctuations

As a Euro-reporter, Jenoptik faces transaction and translation risks from USD and CNY; in 2024 roughly 40% of revenues were non-euro, amplifying exposure when EUR/USD swung ~8% and EUR/CNY ~6% year-on-year.

Exchange moves can erode export competitiveness and shift reported subsidiary earnings; a 5% EUR strengthening in 2024 reduced reported international EBIT by an estimated mid-single-digit percentage.

The group uses forward contracts, options and natural hedges; at FY2024 Jenoptik disclosed hedges covering a significant portion of 12–24 month FX exposure to stabilize consolidated results.

Capital Expenditure Trends in Healthcare

Economic stability in healthcare affects hospitals’ and labs’ capital expenditure on advanced medical lasers and diagnostic systems; global healthcare capex rose ~4% in 2024 to $1.75 trillion, supporting selective upgrades.

Life sciences spending shows resilience—2024 medtech revenue grew ~6%—but recessions can postpone large equipment purchases, with procurement cycles extending 6–18 months in downturns.

Jenoptik targets high-growth niches (ophthalmology, dermatology, lab automation) where CAGR expectations of 7–9% through 2028 help stabilize demand despite macro swings.

- Healthcare capex ~ $1.75T in 2024, +4%

- Medtech revenue growth ~6% in 2024

- Procurement delays 6–18 months in downturns

- Target niches CAGR 7–9% to 2028

Supply Chain Diversification Costs

The shift from just-in-time to just-in-case raises capital needs for Jenoptik; building redundant plants and local suppliers can increase capex by an estimated 5–10% annually, with supply‑chain resilience programs often costing €20–50m for mid-sized industrial optics firms.

Such investments lower short-term liquidity and can compress ROIC by 1–3 percentage points, yet reduce expected disruption losses (historical global shock losses averaged 2–6% of revenue for comparable manufacturers).

Capex cycles vs rising costs: €1.02bn revenue, $91bn fab spend, capex squeezes ROIC

Key economic drivers: semiconductor capex cyclical (2024 fab equipment ~$91bn) vs long-term chip demand (IDC ~6–8% CAGR 2024–29); FY2024 group revenue €1.02bn with ~40% non-euro exposure; 2024 Eurozone CPI 5.3%/US CPI 3.4% raising input costs; healthcare capex ~$1.75T (+4%) and medtech +6% supporting niche demand; supply‑chain resilience adds ~5–10% capex, costing €20–50m and compressing ROIC ~1–3pp.

| Metric | 2024 |

|---|---|

| Fab equip spend | $91bn |

| Jenoptik rev | €1.02bn |

| Non-euro rev | ~40% |

| Euro CPI | 5.3% |

| Healthcare capex | $1.75T |

Preview the Actual Deliverable

Jenoptik PESTLE Analysis

The preview shown here is the exact Jenoptik PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, supply-chain dynamics, and rapid optics-tech innovation are shaping Jenoptik’s strategic horizon—our concise PESTLE highlights key risks and opportunities you need now. Purchase the full PESTLE for a sector‑specific, actionable breakdown and downloadable templates to inform investment decisions and strategic planning instantly.

Political factors

Trade Protectionism and Export Controls

The global photonics sector faces rising export controls: since 2022 restrictions on semiconductor equipment have expanded, with US-led curbs affecting shipments worth an estimated $20–30bn annually; Jenoptik, a supplier to chipmakers, must navigate EU, US and Chinese rules to retain access to markets that drove 2024 photonics demand growth of ~8%.

European Semiconductor Sovereignty

The EU Chips Act targets 20% of global semiconductor production in Europe by 2030 and mobilizes over EUR 43 billion in public and private investment; Jenoptik gains from subsidies and R&D grants tied to these programs that reduce supply-chain reliance.

Geopolitical Tensions in the Asia-Pacific

Ongoing instability in the Asia-Pacific threatens optics manufacturing and distribution; trade along the Taiwan Strait and South China Sea accounts for roughly 30% of global semiconductor shipments, elevating supply-chain risk for Jenoptik’s optics and photonics components.

Disruptions could affect raw-material flows and major electronics customers—Taiwan supplies ~60% of advanced chips—potentially hitting revenue tied to Asia sales, which were about 22% of Jenoptik’s 2024 group revenue.

Jenoptik closely monitors developments, maintains contingency plans, and is diversifying production and supplier bases across Europe and Southeast Asia to reduce concentration risk.

Defense and Security Spending Shifts

Shifts in national defense budgets—NATO defense spending rose to 2.2% of GDP on average in 2024, with EU members increasing procurement—boost demand for Jenoptik’s sensing and surveillance optics used in reconnaissance and border security.

Geopolitical tensions in 2024–25 drove higher procurement: German defense procurement rose 18% YoY in 2024, underpinning near-term revenue visibility for defense-focused product lines.

Alignment with NATO and allied procurement standards remains crucial for Jenoptik’s long-term contracts, export approvals, and revenue stability across defense portfolios.

- 2024 NATO avg defense spend 2.2% GDP

- Germany procurement +18% YoY 2024

- Higher border-security procurements boost optics demand

- NATO alignment critical for export/contracts

Global Trade Agreements and Tariffs

The implementation of new trade agreements or retaliatory tariffs can shift Jenoptik’s international cost base; for example, a 10% tariff on optical components could raise COGS materially given components accounted for ~32% of 2024 production input costs.

Trade disputes between major economies risk duties on laser systems—Jenoptik booked €1.1bn revenue in 2024, so even 2–3% margin pressure from tariffs would cut EBITDA by €22–33m.

Navigating fiscal hurdles requires flexible sourcing, nearshoring, and proactive engagement with trade policymakers to preserve competitive pricing and supply continuity.

- Tariff sensitivity: 2–3% EBITDA downside per modest tariff rise

- Input concentration: ~32% of production inputs from specialized suppliers (2024)

- Revenue exposure: €1.1bn global revenue (2024)

- Mitigation: diversify suppliers, nearshoring, policy engagement

Geopolitics Bite: Export Curbs, Tariffs Risk €22–33m EBITDA as Asia & Supply Chains Strain

Political risks include export controls (US-led curbs since 2022 impacting $20–30bn of semiconductor equipment) constraining Jenoptik’s market access; EU Chips Act (EUR 43bn) and German defense procurement (+18% YoY 2024) boost subsidies and defense demand; Asia-Pacific tensions threaten supply chains (Taiwan ~60% advanced chips) vs. 22% revenue exposure in Asia (2024); tariffs could cut EBITDA 2–3% (€22–33m on €1.1bn revenue).

| Metric | Value (2024/2025) |

|---|---|

| Group revenue | €1.1bn |

| Asia revenue share | 22% |

| Tariff EBITDA hit | 2–3% (€22–33m) |

| Input concentration | 32% of production costs |

| NATO avg defense spend | 2.2% GDP (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Jenoptik across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights tailored to its optics, photonics, and defense-adjacent markets to support strategic planning and investor communications.

A concise Jenoptik PESTLE summary that highlights regulatory, technological, and market risks in plain language for quick inclusion in presentations or strategy sessions, easily shared across teams and annotated with region- or division-specific notes.

Economic factors

Semiconductor Market Volatility

The cyclical semiconductor industry strongly influences Jenoptik’s revenue as a key equipment supplier, with global chip capex swinging—IC Insights reported 2024 fab equipment spending at about $91bn after a 2023 trough—causing quarters of reduced orders when consumer electronics demand softens. Long-term chip demand (IDC forecasts ~6–8% CAGR 2024–2029) supports sustained need for tools, but short-term volatility pressures near-term cash flow. Jenoptik mitigates this by diversifying into medical tech and smart mobility, where FY2024 reported group revenue of €1.02bn and growing service contracts that smooth cyclicality.

Global Inflationary Pressures

Persistently high inflation across major economies—with Euro area CPI at 5.3% and US CPI at 3.4% in 2024—elevates costs for Jenoptik’s specialized materials, energy and skilled labor.

Jenoptik must balance rising operational costs against competitive pricing to protect margins in a crowded global market.

Effective cost management and inclusion of price escalation clauses in long-term contracts are essential tools to navigate these headwinds through 2025.

Currency Exchange Rate Fluctuations

As a Euro-reporter, Jenoptik faces transaction and translation risks from USD and CNY; in 2024 roughly 40% of revenues were non-euro, amplifying exposure when EUR/USD swung ~8% and EUR/CNY ~6% year-on-year.

Exchange moves can erode export competitiveness and shift reported subsidiary earnings; a 5% EUR strengthening in 2024 reduced reported international EBIT by an estimated mid-single-digit percentage.

The group uses forward contracts, options and natural hedges; at FY2024 Jenoptik disclosed hedges covering a significant portion of 12–24 month FX exposure to stabilize consolidated results.

Capital Expenditure Trends in Healthcare

Economic stability in healthcare affects hospitals’ and labs’ capital expenditure on advanced medical lasers and diagnostic systems; global healthcare capex rose ~4% in 2024 to $1.75 trillion, supporting selective upgrades.

Life sciences spending shows resilience—2024 medtech revenue grew ~6%—but recessions can postpone large equipment purchases, with procurement cycles extending 6–18 months in downturns.

Jenoptik targets high-growth niches (ophthalmology, dermatology, lab automation) where CAGR expectations of 7–9% through 2028 help stabilize demand despite macro swings.

- Healthcare capex ~ $1.75T in 2024, +4%

- Medtech revenue growth ~6% in 2024

- Procurement delays 6–18 months in downturns

- Target niches CAGR 7–9% to 2028

Supply Chain Diversification Costs

The shift from just-in-time to just-in-case raises capital needs for Jenoptik; building redundant plants and local suppliers can increase capex by an estimated 5–10% annually, with supply‑chain resilience programs often costing €20–50m for mid-sized industrial optics firms.

Such investments lower short-term liquidity and can compress ROIC by 1–3 percentage points, yet reduce expected disruption losses (historical global shock losses averaged 2–6% of revenue for comparable manufacturers).

Capex cycles vs rising costs: €1.02bn revenue, $91bn fab spend, capex squeezes ROIC

Key economic drivers: semiconductor capex cyclical (2024 fab equipment ~$91bn) vs long-term chip demand (IDC ~6–8% CAGR 2024–29); FY2024 group revenue €1.02bn with ~40% non-euro exposure; 2024 Eurozone CPI 5.3%/US CPI 3.4% raising input costs; healthcare capex ~$1.75T (+4%) and medtech +6% supporting niche demand; supply‑chain resilience adds ~5–10% capex, costing €20–50m and compressing ROIC ~1–3pp.

| Metric | 2024 |

|---|---|

| Fab equip spend | $91bn |

| Jenoptik rev | €1.02bn |

| Non-euro rev | ~40% |

| Euro CPI | 5.3% |

| Healthcare capex | $1.75T |

Preview the Actual Deliverable

Jenoptik PESTLE Analysis

The preview shown here is the exact Jenoptik PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.