JetBlue PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are shaping JetBlue’s strategic outlook—our concise PESTLE highlights key risks and opportunities to inform smarter decisions; purchase the full analysis to access the complete, ready-to-use report and actionable intelligence instantly.

Political factors

Federal Regulatory Scrutiny

The U.S. DOT and DOJ tightened oversight after blocking the $3.8bn JetBlue-Spirit deal in 2023, signaling sustained scrutiny of airline consolidation; regulators rejected the merger over competition and fare concerns affecting transcontinental markets.

This political stance, prioritizing consumer protection, limits JetBlue’s near-term M&A runway and complicates joint ventures, reducing acquisition probability below historical industry averages for 2024–25.

International Aviation Accords

JetBlue’s transatlantic growth into London, Paris and Amsterdam hinges on bilateral air service agreements and scarce slot allocations; UK/EU slot coordination affects yields on routes generating up to an estimated $300–500m annual revenue per major city pair for carriers of similar scale.

EU moves on airport congestion pricing and aviation environmental levies—e.g., the EU ETS expansion which raised average CO2 compliance costs to about €80/tonne in 2024—can erode margins on long-haul flights.

Stable diplomatic ties and renegotiated traffic rights are critical for securing long-term access to high-yield corridors and protecting projected transatlantic unit revenues.

Government Infrastructure Funding

The federal push to modernize FAA air traffic control and fund airport projects directly affects JetBlue's operational efficiency, with the FAA's $25+ billion NextGen backlog and $17.5 billion in Airport Improvement Program grants through 2024 shaping upgrade timelines. Delays in appropriations or a 2024 FAA staffing shortfall that increased traffic flow restrictions raise congestion risk at JFK and Boston Logan, where JetBlue held ~30% and ~23% market share respectively in 2024. JetBlue lobbies Congress and spent $1.2 million on federal lobbying in 2023 to secure funding and policy changes aimed at reducing delays and improving infrastructure resilience.

Taxation and Fiscal Policy

These fiscal uncertainties force JetBlue to keep flexible hedging, capex timing, and liquidity targets—JetBlue ended 2024 with ~$2.1B cash and equivalents—to protect margins against sudden tax shifts.

- Fuel as ~22% of operating costs (2024 industry estimate)

- JetBlue cash ≈ $2.1B end of 2024

- Federal corporate tax discussions: ~21–25% range in 2024

- Risk: new environmental/aviation-specific levies

Geopolitical Stability in the Caribbean

Approximately 20% of JetBlue's 2025 international ASMs cover Latin America and the Caribbean, exposing revenue to regional political volatility; events like Haiti unrest or Barbados policy shifts can cut leisure demand sharply.

Changes in visa rules or diplomatic ties have historically triggered double-digit weekly traffic declines on affected routes; JetBlue actively monitors developments and reassigns aircraft to minimize seat-mile loss and protect margins.

- ~20% of 2025 international ASMs in region

- Localized unrest can cause >10% short-term demand drops

- Proactive capacity reallocation to limit revenue impact

Regulatory hangover caps JetBlue M&A; transatlantic upside vs ETS and fuel headwinds

Regulatory scrutiny after the blocked 2023 Spirit deal limits JetBlue M&A and JV options; transatlantic growth depends on slots and bilateral rights with estimated $300–500m route upside per major city pair for peers. EU ETS compliance costs averaged ~€80/tonne in 2024, raising long‑haul CASM; fuel ≈22% of costs and JetBlue cash ≈$2.1B (end‑2024) buffer fiscal shocks.

| Metric | Value |

|---|---|

| Blocked merger impact | High scrutiny (post‑2023) |

| EU ETS cost (2024) | €80/tonne |

| Fuel share of costs (2024) | ~22% |

| JetBlue cash (end‑2024) | $2.1B |

What is included in the product

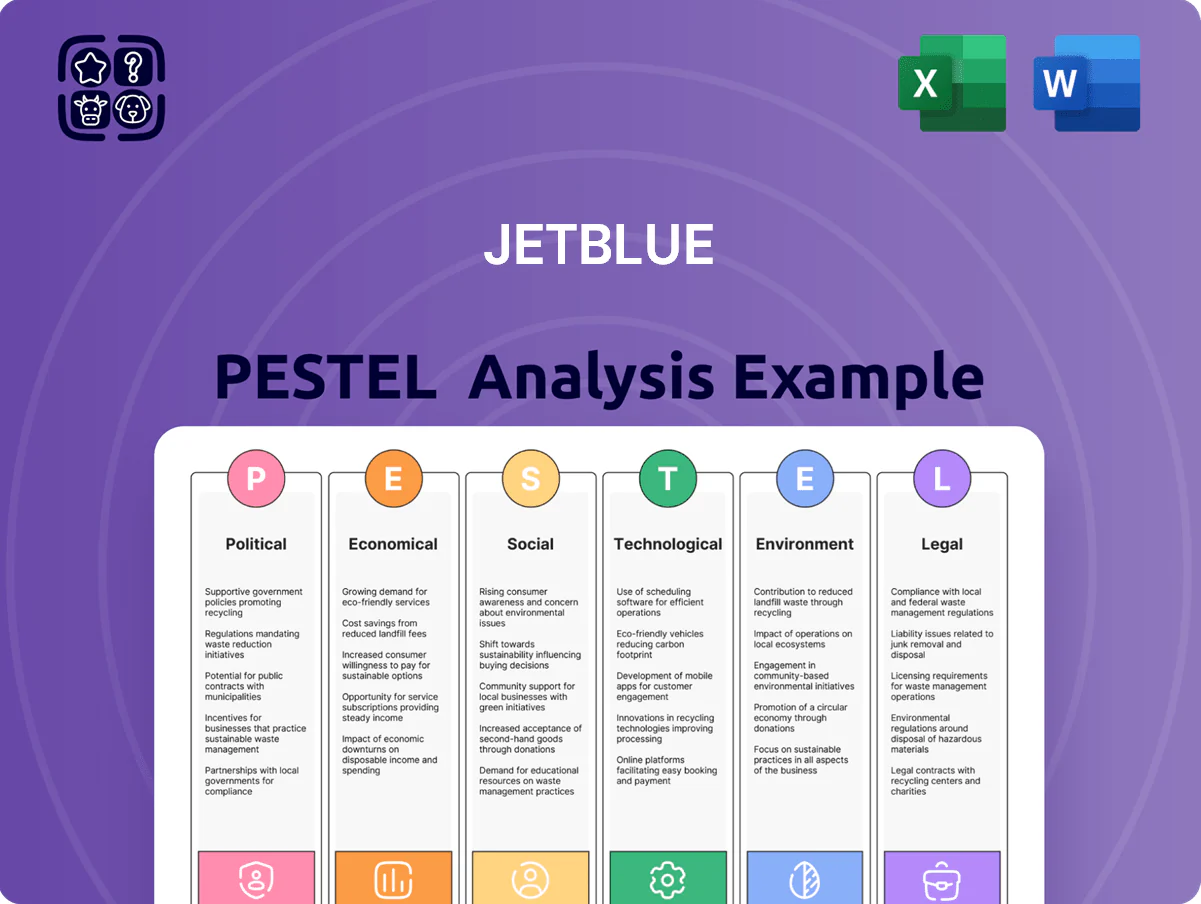

Explores how macro-environmental factors uniquely affect JetBlue across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategy.

A concise, JetBlue-specific PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, and editable with notes for regional or business-line context to streamline strategic meetings and cross-team alignment.

Economic factors

Jet Fuel Price Volatility

Fluctuations in global oil prices remain a top driver of JetBlue’s costs: jet fuel was ~28% of US airlines’ CASM in 2024 and Brent averaged $85/bbl in 2024 versus $100+/bbl spikes in 2022–23, so sustained high prices would compress JetBlue’s margins despite hedging covering portions of 2025 volumes; persistent fuel pressure could force fare increases, making ongoing 2025 energy-market monitoring essential to balance fuel-efficiency investments with competitive pricing.

Inflationary Pressures on Consumer Spending

Persistent CPI inflation at 3.4% year-over-year (Jan 2026) erodes discretionary income for leisure travelers—JetBlue’s core segment—after housing and essentials consuming about 55% of median household budgets in 2024–25. While U.S. air travel demand recovered to 95% of 2019 levels in 2025, sustained high living costs risk downgrades to ULCCs or fewer trips. JetBlue must reinforce its premium-for-less positioning, balancing modest fares with differentiated service to retain experience-oriented, cost-sensitive customers.

Interest Rate Environment and Debt Management

The Federal Reserve's 2024-25 tightening kept the effective Fed funds rate near 5.25–5.50%, raising JetBlue's cost to finance new Airbus A220/A321neo deliveries and refinance outstanding debt; higher yields pushed average borrowing spreads above pre‑pandemic levels, increasing annual interest expense (JetBlue reported $1.1bn interest expense in 2024).

Labor Market Dynamics and Wage Inflation

Labor costs rose industry-wide, with US airline labor expense per ASM up ~12% in 2024 vs 2022; JetBlue must manage higher wages as pilots and flight attendants win raises, keeping unit labor cost control central to margin recovery.

JetBlue faces competitive talent markets—pilot average pay rose ~15% 2023–2024—requiring retention packages that pressure CASM; effective bargaining avoids strikes that could disrupt capacity and revenue.

Maintaining labor cost parity with peers (Spirit/Frontier) is vital—2024 unit cost targets hinge on negotiated benefits and productivity gains to sustain operating margin improvements.

- Industry labor expense/ASM +12% (2022–2024)

- Pilot pay +15% (2023–2024)

- CASM sensitivity to wage inflation critical for margins

- Union negotiations key to operational continuity

Currency Exchange Fluctuations

As JetBlue expands internationally, currency volatility—notably in the Caribbean and Europe—raises revenue risk; in 2024 roughly 12–15% of departures were international, increasing FX exposure.

A stronger U.S. dollar can reduce inbound tourism demand, with CBP data showing U.S. dollar strength in 2023–24 lowered travel spending by an estimated 3–5% in key markets.

Local currency depreciation erodes reported revenue when converted to dollars; JetBlue reported 2024 international revenue of about $1.1B, vulnerable to FX swings.

- International share ~12–15% of departures

- 2024 international revenue ≈ $1.1B

- USD strength cut travel spending ~3–5% in 2023–24

- FX moves directly affect reported USD revenue and demand

Rising fuel, wages & rates squeeze margins as FX and inflation bite airline profits

Fuel (jet fuel ~28% of CASM in 2024; Brent avg $85/bbl in 2024), inflation (CPI 3.4% Jan 2026), high rates (Fed funds ~5.25–5.50%; $1.1B interest expense 2024), wage inflation (labor/ASM +12% 2022–24; pilot pay +15% 2023–24), FX exposure (intl rev ≈ $1.1B; intl departures 12–15%; USD strength cut spending ~3–5%).

| Metric | Value |

|---|---|

| Jet fuel share of CASM (2024) | ~28% |

| Brent avg (2024) | $85/bbl |

| CPI (Jan 2026) | 3.4% |

| Fed funds (2024–25) | 5.25–5.50% |

| Interest expense (2024) | $1.1B |

| Labor expense/ASM (2022–24) | +12% |

| Pilot pay (2023–24) | +15% |

| Intl revenue (2024) | ≈ $1.1B |

| Intl departures share | 12–15% |

Preview Before You Purchase

JetBlue PESTLE Analysis

The preview shown here is the exact JetBlue PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are shaping JetBlue’s strategic outlook—our concise PESTLE highlights key risks and opportunities to inform smarter decisions; purchase the full analysis to access the complete, ready-to-use report and actionable intelligence instantly.

Political factors

Federal Regulatory Scrutiny

The U.S. DOT and DOJ tightened oversight after blocking the $3.8bn JetBlue-Spirit deal in 2023, signaling sustained scrutiny of airline consolidation; regulators rejected the merger over competition and fare concerns affecting transcontinental markets.

This political stance, prioritizing consumer protection, limits JetBlue’s near-term M&A runway and complicates joint ventures, reducing acquisition probability below historical industry averages for 2024–25.

International Aviation Accords

JetBlue’s transatlantic growth into London, Paris and Amsterdam hinges on bilateral air service agreements and scarce slot allocations; UK/EU slot coordination affects yields on routes generating up to an estimated $300–500m annual revenue per major city pair for carriers of similar scale.

EU moves on airport congestion pricing and aviation environmental levies—e.g., the EU ETS expansion which raised average CO2 compliance costs to about €80/tonne in 2024—can erode margins on long-haul flights.

Stable diplomatic ties and renegotiated traffic rights are critical for securing long-term access to high-yield corridors and protecting projected transatlantic unit revenues.

Government Infrastructure Funding

The federal push to modernize FAA air traffic control and fund airport projects directly affects JetBlue's operational efficiency, with the FAA's $25+ billion NextGen backlog and $17.5 billion in Airport Improvement Program grants through 2024 shaping upgrade timelines. Delays in appropriations or a 2024 FAA staffing shortfall that increased traffic flow restrictions raise congestion risk at JFK and Boston Logan, where JetBlue held ~30% and ~23% market share respectively in 2024. JetBlue lobbies Congress and spent $1.2 million on federal lobbying in 2023 to secure funding and policy changes aimed at reducing delays and improving infrastructure resilience.

Taxation and Fiscal Policy

These fiscal uncertainties force JetBlue to keep flexible hedging, capex timing, and liquidity targets—JetBlue ended 2024 with ~$2.1B cash and equivalents—to protect margins against sudden tax shifts.

- Fuel as ~22% of operating costs (2024 industry estimate)

- JetBlue cash ≈ $2.1B end of 2024

- Federal corporate tax discussions: ~21–25% range in 2024

- Risk: new environmental/aviation-specific levies

Geopolitical Stability in the Caribbean

Approximately 20% of JetBlue's 2025 international ASMs cover Latin America and the Caribbean, exposing revenue to regional political volatility; events like Haiti unrest or Barbados policy shifts can cut leisure demand sharply.

Changes in visa rules or diplomatic ties have historically triggered double-digit weekly traffic declines on affected routes; JetBlue actively monitors developments and reassigns aircraft to minimize seat-mile loss and protect margins.

- ~20% of 2025 international ASMs in region

- Localized unrest can cause >10% short-term demand drops

- Proactive capacity reallocation to limit revenue impact

Regulatory hangover caps JetBlue M&A; transatlantic upside vs ETS and fuel headwinds

Regulatory scrutiny after the blocked 2023 Spirit deal limits JetBlue M&A and JV options; transatlantic growth depends on slots and bilateral rights with estimated $300–500m route upside per major city pair for peers. EU ETS compliance costs averaged ~€80/tonne in 2024, raising long‑haul CASM; fuel ≈22% of costs and JetBlue cash ≈$2.1B (end‑2024) buffer fiscal shocks.

| Metric | Value |

|---|---|

| Blocked merger impact | High scrutiny (post‑2023) |

| EU ETS cost (2024) | €80/tonne |

| Fuel share of costs (2024) | ~22% |

| JetBlue cash (end‑2024) | $2.1B |

What is included in the product

Explores how macro-environmental factors uniquely affect JetBlue across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategy.

A concise, JetBlue-specific PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations, and editable with notes for regional or business-line context to streamline strategic meetings and cross-team alignment.

Economic factors

Jet Fuel Price Volatility

Fluctuations in global oil prices remain a top driver of JetBlue’s costs: jet fuel was ~28% of US airlines’ CASM in 2024 and Brent averaged $85/bbl in 2024 versus $100+/bbl spikes in 2022–23, so sustained high prices would compress JetBlue’s margins despite hedging covering portions of 2025 volumes; persistent fuel pressure could force fare increases, making ongoing 2025 energy-market monitoring essential to balance fuel-efficiency investments with competitive pricing.

Inflationary Pressures on Consumer Spending

Persistent CPI inflation at 3.4% year-over-year (Jan 2026) erodes discretionary income for leisure travelers—JetBlue’s core segment—after housing and essentials consuming about 55% of median household budgets in 2024–25. While U.S. air travel demand recovered to 95% of 2019 levels in 2025, sustained high living costs risk downgrades to ULCCs or fewer trips. JetBlue must reinforce its premium-for-less positioning, balancing modest fares with differentiated service to retain experience-oriented, cost-sensitive customers.

Interest Rate Environment and Debt Management

The Federal Reserve's 2024-25 tightening kept the effective Fed funds rate near 5.25–5.50%, raising JetBlue's cost to finance new Airbus A220/A321neo deliveries and refinance outstanding debt; higher yields pushed average borrowing spreads above pre‑pandemic levels, increasing annual interest expense (JetBlue reported $1.1bn interest expense in 2024).

Labor Market Dynamics and Wage Inflation

Labor costs rose industry-wide, with US airline labor expense per ASM up ~12% in 2024 vs 2022; JetBlue must manage higher wages as pilots and flight attendants win raises, keeping unit labor cost control central to margin recovery.

JetBlue faces competitive talent markets—pilot average pay rose ~15% 2023–2024—requiring retention packages that pressure CASM; effective bargaining avoids strikes that could disrupt capacity and revenue.

Maintaining labor cost parity with peers (Spirit/Frontier) is vital—2024 unit cost targets hinge on negotiated benefits and productivity gains to sustain operating margin improvements.

- Industry labor expense/ASM +12% (2022–2024)

- Pilot pay +15% (2023–2024)

- CASM sensitivity to wage inflation critical for margins

- Union negotiations key to operational continuity

Currency Exchange Fluctuations

As JetBlue expands internationally, currency volatility—notably in the Caribbean and Europe—raises revenue risk; in 2024 roughly 12–15% of departures were international, increasing FX exposure.

A stronger U.S. dollar can reduce inbound tourism demand, with CBP data showing U.S. dollar strength in 2023–24 lowered travel spending by an estimated 3–5% in key markets.

Local currency depreciation erodes reported revenue when converted to dollars; JetBlue reported 2024 international revenue of about $1.1B, vulnerable to FX swings.

- International share ~12–15% of departures

- 2024 international revenue ≈ $1.1B

- USD strength cut travel spending ~3–5% in 2023–24

- FX moves directly affect reported USD revenue and demand

Rising fuel, wages & rates squeeze margins as FX and inflation bite airline profits

Fuel (jet fuel ~28% of CASM in 2024; Brent avg $85/bbl in 2024), inflation (CPI 3.4% Jan 2026), high rates (Fed funds ~5.25–5.50%; $1.1B interest expense 2024), wage inflation (labor/ASM +12% 2022–24; pilot pay +15% 2023–24), FX exposure (intl rev ≈ $1.1B; intl departures 12–15%; USD strength cut spending ~3–5%).

| Metric | Value |

|---|---|

| Jet fuel share of CASM (2024) | ~28% |

| Brent avg (2024) | $85/bbl |

| CPI (Jan 2026) | 3.4% |

| Fed funds (2024–25) | 5.25–5.50% |

| Interest expense (2024) | $1.1B |

| Labor expense/ASM (2022–24) | +12% |

| Pilot pay (2023–24) | +15% |

| Intl revenue (2024) | ≈ $1.1B |

| Intl departures share | 12–15% |

Preview Before You Purchase

JetBlue PESTLE Analysis

The preview shown here is the exact JetBlue PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.