JFE Holdings Boston Consulting Group Matrix

See the Bigger Picture

JFE Holdings sits at an inflection point where steel demand cycles, high-value specialty products, and green-steel investments determine its quadrant mix—some segments behave like Cash Cows while newer low-carbon initiatives look like Question Marks. This snapshot highlights revenue concentration, margin dynamics, and capital intensity, but the full BCG Matrix maps each product line to a quadrant with quantitative scoring and strategic options. Dive deeper—purchase the full BCG Matrix for quadrant-level insights, data-backed recommendations, and Word/Excel deliverables to guide investment and resource allocation.

Stars

High-Grade Electrical Steel Sheets

High-Grade Electrical Steel Sheets sit in Stars: JFE has expanded non-oriented electrical steel (NOES) capacity by ~40% since 2022 to meet EV motor demand, with this segment accounting for ~18% of group revenue in 2025 and growing at ~25% CAGR (2023–25).

JFE holds a leading tech position with >30% global NOES market share and premium ASPs; heavy capex and R&D—≈¥120 billion spent 2023–25—keep free cash low despite strong sales.

This unit is JFE’s primary green-mobility driver, enabling EV supply contracts worth an estimated ¥500+ billion backlog to 2027 and anchoring future margin expansion as scale and tech improvements mature.

JGreeX Green Steel Products

JGreeX Green Steel Products uses a mass-balance method to certify about 40–60% CO2 intensity reductions versus standard steel, targeting eco-conscious industrial buyers as green-steel demand grew ~35% CAGR through 2021–2025.

By end-2025 low-carbon premiums accounted for roughly 8–12% of JFE Holdings’ steel revenue, cementing its leadership in sustainable materials and supporting higher ASPs.

However, hydrogen-rich gas injection and low-carbon scrap add ~15–25% to production costs, requiring sustained capex—JFE planned ¥120–180 billion 2024–2026 for decarbonization.

These products are strategic to retain market share as global steel decarbonization targets push demand for certified low-CO2 inputs through 2030.

Carbon Capture and Storage Engineering

JFE Engineering leads industrial Carbon Capture and Storage (CCS) deployment, having secured contracts worth about ¥120 billion (≈$820M) in 2024–25 and piloted 200 ktCO2/year capture modules with 85% capture efficiency.

The CCS market is growing ~18% CAGR to 2030 as carbon taxes and regulations tighten across Japan, EU, and US markets.

JFE’s integrated plant construction and chemical-processing know-how gives it a strong market share in Asia—estimated 22% regional share in industrial CCS projects.

Significant capital is needed for pilots and global scale-up—estimated ¥60–100 billion over 2025–28—but CCS is a strategic growth cornerstone for JFE’s low-carbon transition.

Advanced High-Tensile Steel

JFE Holdings’ advanced high-tensile steel sheets have seen demand rise as automakers cut weight to boost EV range; in 2024 JFE reported steel shipments to automotive customers up ~6% and segment ASPs supported margins near 8% in the specialty sheet lines.

The product holds a high market share in ultra-high-strength automotive sheet, offering extreme strength plus formability, used in chassis and body parts to save 10–30 kg per vehicle versus conventional steel.

Competition from aluminum and composites forces R&D investment; JFE increased specialty-steel R&D spend to ~¥40 billion in FY2024 to improve formability and joinability.

It qualifies as a star: strong revenue and margin contribution but needs ongoing technical support and marketing to fend off lighter materials.

- Shipments +6% (2024)

- Specialty ASPs → ~8% margin

- R&D ~¥40B (FY2024)

- Weight savings 10–30 kg/vehicle

- High market share in ultra-high-strength sheets

Hydrogen Supply Chain Infrastructure

JFE’s engineering arm leads construction of hydrogen refueling stations and large cryogenic storage tanks, leveraging metallurgy and pipeline expertise to secure major projects in Japan and select Asian markets; global hydrogen demand forecasts rose to ~145–170 Mt H2 by 2030, supporting near-term growth through 2025.

Despite strong market share, heavy R&D and capex for advanced cryogenics keep the unit cash-neutral—2024 capex rose ~18% YoY and free cash flow approximated zero as development spend matches revenues.

- Leading role: stations + large storage tanks

- Market: strong Japan share; selected overseas projects

- Growth driver: hydrogen demand up to ~145–170 Mt by 2030

- Finance: 2024 capex +18% YoY; FCF ~0 (cash in ≈ cash out)

High‑growth green portfolio: NOES >30% global, ~25% CAGR, ¥120B capex (2023–25)

Stars: High-grade NOES, green steel, CCS, specialty sheets, and hydrogen assets drive ~18% group revenue in 2025, ~25% CAGR (2023–25), with NOES >30% global share; 2023–25 capex ≈¥120B; green premiums 8–12% of steel revenue; CCS contracts ≈¥120B; specialty R&D ¥40B (FY2024); hydrogen capex +18% YoY (2024).

| Item | Key number |

|---|---|

| Group revenue (Stars) | ~18% (2025) |

| NOES CAGR | ~25% (2023–25) |

| NOES share | >30% global |

| Capex (2023–25) | ≈¥120B |

| Green premiums | 8–12% steel rev |

| CCS contracts | ≈¥120B (2024–25) |

| Specialty R&D | ¥40B (FY2024) |

| Hydrogen capex YoY | +18% (2024) |

What is included in the product

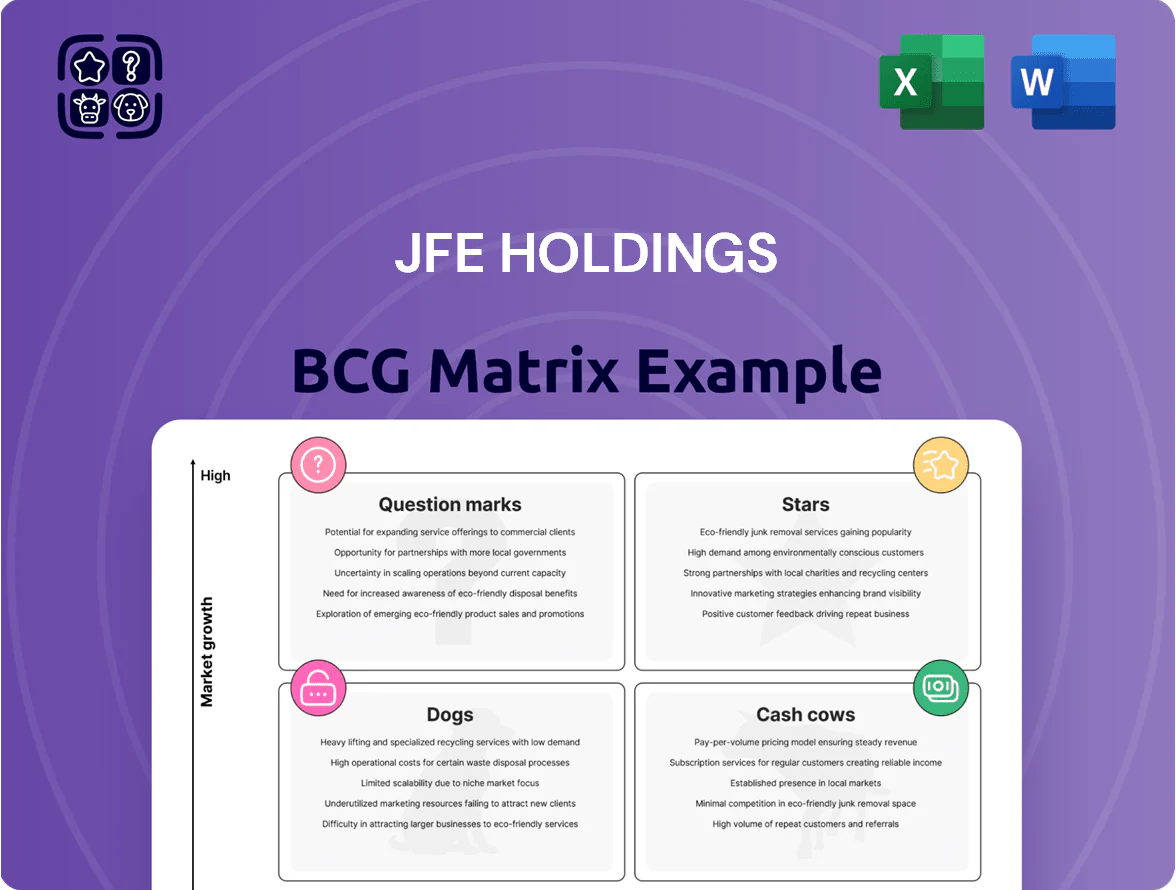

BCG Matrix analysis of JFE Holdings: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations.

One-page JFE Holdings BCG Matrix placing each business unit in a quadrant for swift strategic clarity

Cash Cows

Automotive Flat-Rolled Steel

Standard automotive flat-rolled steel sheets generate steady cash for JFE Steel, serving a mature global market worth roughly $250B in 2024 for automotive steel; JFE’s automotive segment contributed about ¥420 billion in operating profit in FY2024, anchoring cash flow.

JFE holds a leading share with ~30% of Japan’s auto steel supply and strong footing in Asia via long-term contracts and low unit costs from integrated mills—helping gross margins stay near 14% in 2024.

Market growth is low for ICE materials—annual volume growth ~1%—so JFE restricts capex to maintenance and efficiency upgrades, keeping automotive capex around ¥120–150 billion annually (2024 plan).

Surplus cash from this segment funds JFE’s green transition: the company allocated ¥500 billion to green steel and hydrogen R&D/CapEx through 2030, with automotive cash crucial to that pipeline.

Heavy Steel Plates for Shipbuilding

JFE is a dominant supplier of high-strength heavy plates for large container ships and tankers, holding an estimated 30–35% share of Japan’s marine plate market in 2024 and long-term contracts with major shipyards such as Imabari and Japan Marine United.

The market is mature with low growth—global shipbuilding steel demand fell about 3% in 2023 and CAGR to 2028 is forecast ~0–1%—but JFE’s entrenched relationships secure stable volumes and pricing power.

Refined production yields high margins: JFE Steel reported an adjusted operating margin ~9–11% on plate products in FY2024, producing steady cash flow used to service ¥400–¥450 billion corporate debt and fund dividends (¥40–¥50 per share range in 2024).

JFE Shoji Trading Operations

The trading arm, JFE Shoji, is a cash cow for JFE Holdings by handling global distribution and logistics of steel and raw materials, supporting ¥2.1 trillion group revenues in FY2024 and operating in a mature market with top-tier share in Japan and strong export channels.

It leverages an extensive network of domestic and international processing centers and long-term supplier contracts, keeping operating margins stable around 4–6% while requiring far lower capital expenditure than JFE’s steelmaking units.

Minimal capex needs—estimated ¥30–50 billion annually for logistics and IT—free up liquidity; JFE Shoji’s steady cash flow funds higher-risk engineering projects and helped sustain group net debt/EBITDA near 1.8x at end-2024.

Municipal Waste-to-Energy Plants

JFE Engineering leads Japan in waste-to-energy plant construction and ops; domestic market growth is ~1% annually (2024), so it's a cash cow with low expansion but high stability.

Recurring maintenance and O&M contracts generate predictable revenue—JFE reported ¥42.3bn in environmental systems sales in FY2024, with ~60% recurring services, letting the firm milk long-term public projects.

Proprietary gasification and melting techs create a barrier to entry, reducing competition and preserving margins; service contracts average 10–20 years, locking cash flows.

- Market share: leading in Japan

- Growth: ~1% domestic

- FY2024 env. sales: ¥42.3bn

- Recurring revenue: ~60%

- Contracts: 10–20 years

Infrastructure Maintenance Services

JFE’s Infrastructure Maintenance Services—covering bridge, tunnel, and pipeline repair—are a cash cow: low industry growth but commanding significant market share in Japan, supporting steady, predictable revenue as the national infrastructure ages (Japan had 28% of bridges over 50 years old in 2023).

Operating with low marketing needs and high operating margins (JFE Steel margin context: mid-teens pre-2025), this unit generates strong free cash flow that funds R&D and speculative engineering projects in the Question Marks quadrant.

- Stable demand: aging stock → predictable contracts

- High margin, low promo spend → strong FCF

- 2023 Japan stat: 28% bridges >50 years

- Cash funds R&D/speculative ventures

JFE’s cash cows fund ¥500bn green capex—strong margins, low capex, 1.8x net debt/EBITDA

JFE’s cash cows—automotive flat-rolled steel, marine/heavy plates, JFE Shoji trading, environmental systems, and infrastructure maintenance—generated stable FY2024 cash: automotive op profit ≈¥420bn, plate margins 9–11%, Shoji revenue ¥2.1trn, env. sales ¥42.3bn (60% recurring), capex needs low (logistics ¥30–50bn; auto ¥120–150bn), supporting ¥500bn green capex to 2030 and net debt/EBITDA ≈1.8x.

| Segment | FY2024 | Margin/Notes |

|---|---|---|

| Automotive | ¥420bn op profit | ~14% gm |

| Plates | — | 9–11% op margin |

| Shoji | ¥2.1trn rev | 4–6% op |

| Environmental | ¥42.3bn sales | 60% recurring |

Delivered as Shown

JFE Holdings BCG Matrix

The BCG Matrix preview you see here is the exact, final document you'll receive after purchase—no watermarks, no placeholders—just a professionally formatted, analysis-ready report tailored to JFE Holdings for strategic clarity and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

JFE Holdings sits at an inflection point where steel demand cycles, high-value specialty products, and green-steel investments determine its quadrant mix—some segments behave like Cash Cows while newer low-carbon initiatives look like Question Marks. This snapshot highlights revenue concentration, margin dynamics, and capital intensity, but the full BCG Matrix maps each product line to a quadrant with quantitative scoring and strategic options. Dive deeper—purchase the full BCG Matrix for quadrant-level insights, data-backed recommendations, and Word/Excel deliverables to guide investment and resource allocation.

Stars

High-Grade Electrical Steel Sheets

High-Grade Electrical Steel Sheets sit in Stars: JFE has expanded non-oriented electrical steel (NOES) capacity by ~40% since 2022 to meet EV motor demand, with this segment accounting for ~18% of group revenue in 2025 and growing at ~25% CAGR (2023–25).

JFE holds a leading tech position with >30% global NOES market share and premium ASPs; heavy capex and R&D—≈¥120 billion spent 2023–25—keep free cash low despite strong sales.

This unit is JFE’s primary green-mobility driver, enabling EV supply contracts worth an estimated ¥500+ billion backlog to 2027 and anchoring future margin expansion as scale and tech improvements mature.

JGreeX Green Steel Products

JGreeX Green Steel Products uses a mass-balance method to certify about 40–60% CO2 intensity reductions versus standard steel, targeting eco-conscious industrial buyers as green-steel demand grew ~35% CAGR through 2021–2025.

By end-2025 low-carbon premiums accounted for roughly 8–12% of JFE Holdings’ steel revenue, cementing its leadership in sustainable materials and supporting higher ASPs.

However, hydrogen-rich gas injection and low-carbon scrap add ~15–25% to production costs, requiring sustained capex—JFE planned ¥120–180 billion 2024–2026 for decarbonization.

These products are strategic to retain market share as global steel decarbonization targets push demand for certified low-CO2 inputs through 2030.

Carbon Capture and Storage Engineering

JFE Engineering leads industrial Carbon Capture and Storage (CCS) deployment, having secured contracts worth about ¥120 billion (≈$820M) in 2024–25 and piloted 200 ktCO2/year capture modules with 85% capture efficiency.

The CCS market is growing ~18% CAGR to 2030 as carbon taxes and regulations tighten across Japan, EU, and US markets.

JFE’s integrated plant construction and chemical-processing know-how gives it a strong market share in Asia—estimated 22% regional share in industrial CCS projects.

Significant capital is needed for pilots and global scale-up—estimated ¥60–100 billion over 2025–28—but CCS is a strategic growth cornerstone for JFE’s low-carbon transition.

Advanced High-Tensile Steel

JFE Holdings’ advanced high-tensile steel sheets have seen demand rise as automakers cut weight to boost EV range; in 2024 JFE reported steel shipments to automotive customers up ~6% and segment ASPs supported margins near 8% in the specialty sheet lines.

The product holds a high market share in ultra-high-strength automotive sheet, offering extreme strength plus formability, used in chassis and body parts to save 10–30 kg per vehicle versus conventional steel.

Competition from aluminum and composites forces R&D investment; JFE increased specialty-steel R&D spend to ~¥40 billion in FY2024 to improve formability and joinability.

It qualifies as a star: strong revenue and margin contribution but needs ongoing technical support and marketing to fend off lighter materials.

- Shipments +6% (2024)

- Specialty ASPs → ~8% margin

- R&D ~¥40B (FY2024)

- Weight savings 10–30 kg/vehicle

- High market share in ultra-high-strength sheets

Hydrogen Supply Chain Infrastructure

JFE’s engineering arm leads construction of hydrogen refueling stations and large cryogenic storage tanks, leveraging metallurgy and pipeline expertise to secure major projects in Japan and select Asian markets; global hydrogen demand forecasts rose to ~145–170 Mt H2 by 2030, supporting near-term growth through 2025.

Despite strong market share, heavy R&D and capex for advanced cryogenics keep the unit cash-neutral—2024 capex rose ~18% YoY and free cash flow approximated zero as development spend matches revenues.

- Leading role: stations + large storage tanks

- Market: strong Japan share; selected overseas projects

- Growth driver: hydrogen demand up to ~145–170 Mt by 2030

- Finance: 2024 capex +18% YoY; FCF ~0 (cash in ≈ cash out)

High‑growth green portfolio: NOES >30% global, ~25% CAGR, ¥120B capex (2023–25)

Stars: High-grade NOES, green steel, CCS, specialty sheets, and hydrogen assets drive ~18% group revenue in 2025, ~25% CAGR (2023–25), with NOES >30% global share; 2023–25 capex ≈¥120B; green premiums 8–12% of steel revenue; CCS contracts ≈¥120B; specialty R&D ¥40B (FY2024); hydrogen capex +18% YoY (2024).

| Item | Key number |

|---|---|

| Group revenue (Stars) | ~18% (2025) |

| NOES CAGR | ~25% (2023–25) |

| NOES share | >30% global |

| Capex (2023–25) | ≈¥120B |

| Green premiums | 8–12% steel rev |

| CCS contracts | ≈¥120B (2024–25) |

| Specialty R&D | ¥40B (FY2024) |

| Hydrogen capex YoY | +18% (2024) |

What is included in the product

BCG Matrix analysis of JFE Holdings: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest recommendations.

One-page JFE Holdings BCG Matrix placing each business unit in a quadrant for swift strategic clarity

Cash Cows

Automotive Flat-Rolled Steel

Standard automotive flat-rolled steel sheets generate steady cash for JFE Steel, serving a mature global market worth roughly $250B in 2024 for automotive steel; JFE’s automotive segment contributed about ¥420 billion in operating profit in FY2024, anchoring cash flow.

JFE holds a leading share with ~30% of Japan’s auto steel supply and strong footing in Asia via long-term contracts and low unit costs from integrated mills—helping gross margins stay near 14% in 2024.

Market growth is low for ICE materials—annual volume growth ~1%—so JFE restricts capex to maintenance and efficiency upgrades, keeping automotive capex around ¥120–150 billion annually (2024 plan).

Surplus cash from this segment funds JFE’s green transition: the company allocated ¥500 billion to green steel and hydrogen R&D/CapEx through 2030, with automotive cash crucial to that pipeline.

Heavy Steel Plates for Shipbuilding

JFE is a dominant supplier of high-strength heavy plates for large container ships and tankers, holding an estimated 30–35% share of Japan’s marine plate market in 2024 and long-term contracts with major shipyards such as Imabari and Japan Marine United.

The market is mature with low growth—global shipbuilding steel demand fell about 3% in 2023 and CAGR to 2028 is forecast ~0–1%—but JFE’s entrenched relationships secure stable volumes and pricing power.

Refined production yields high margins: JFE Steel reported an adjusted operating margin ~9–11% on plate products in FY2024, producing steady cash flow used to service ¥400–¥450 billion corporate debt and fund dividends (¥40–¥50 per share range in 2024).

JFE Shoji Trading Operations

The trading arm, JFE Shoji, is a cash cow for JFE Holdings by handling global distribution and logistics of steel and raw materials, supporting ¥2.1 trillion group revenues in FY2024 and operating in a mature market with top-tier share in Japan and strong export channels.

It leverages an extensive network of domestic and international processing centers and long-term supplier contracts, keeping operating margins stable around 4–6% while requiring far lower capital expenditure than JFE’s steelmaking units.

Minimal capex needs—estimated ¥30–50 billion annually for logistics and IT—free up liquidity; JFE Shoji’s steady cash flow funds higher-risk engineering projects and helped sustain group net debt/EBITDA near 1.8x at end-2024.

Municipal Waste-to-Energy Plants

JFE Engineering leads Japan in waste-to-energy plant construction and ops; domestic market growth is ~1% annually (2024), so it's a cash cow with low expansion but high stability.

Recurring maintenance and O&M contracts generate predictable revenue—JFE reported ¥42.3bn in environmental systems sales in FY2024, with ~60% recurring services, letting the firm milk long-term public projects.

Proprietary gasification and melting techs create a barrier to entry, reducing competition and preserving margins; service contracts average 10–20 years, locking cash flows.

- Market share: leading in Japan

- Growth: ~1% domestic

- FY2024 env. sales: ¥42.3bn

- Recurring revenue: ~60%

- Contracts: 10–20 years

Infrastructure Maintenance Services

JFE’s Infrastructure Maintenance Services—covering bridge, tunnel, and pipeline repair—are a cash cow: low industry growth but commanding significant market share in Japan, supporting steady, predictable revenue as the national infrastructure ages (Japan had 28% of bridges over 50 years old in 2023).

Operating with low marketing needs and high operating margins (JFE Steel margin context: mid-teens pre-2025), this unit generates strong free cash flow that funds R&D and speculative engineering projects in the Question Marks quadrant.

- Stable demand: aging stock → predictable contracts

- High margin, low promo spend → strong FCF

- 2023 Japan stat: 28% bridges >50 years

- Cash funds R&D/speculative ventures

JFE’s cash cows fund ¥500bn green capex—strong margins, low capex, 1.8x net debt/EBITDA

JFE’s cash cows—automotive flat-rolled steel, marine/heavy plates, JFE Shoji trading, environmental systems, and infrastructure maintenance—generated stable FY2024 cash: automotive op profit ≈¥420bn, plate margins 9–11%, Shoji revenue ¥2.1trn, env. sales ¥42.3bn (60% recurring), capex needs low (logistics ¥30–50bn; auto ¥120–150bn), supporting ¥500bn green capex to 2030 and net debt/EBITDA ≈1.8x.

| Segment | FY2024 | Margin/Notes |

|---|---|---|

| Automotive | ¥420bn op profit | ~14% gm |

| Plates | — | 9–11% op margin |

| Shoji | ¥2.1trn rev | 4–6% op |

| Environmental | ¥42.3bn sales | 60% recurring |

Delivered as Shown

JFE Holdings BCG Matrix

The BCG Matrix preview you see here is the exact, final document you'll receive after purchase—no watermarks, no placeholders—just a professionally formatted, analysis-ready report tailored to JFE Holdings for strategic clarity and decision-making.