JFrog PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and rapid technological change are shaping JFrog’s growth and risks—our concise PESTLE snapshot highlights the key external drivers you need to act on now; purchase the full analysis for a detailed, actionable roadmap to inform investment, strategy, or competitive planning.

Political factors

US Federal Security Mandates

The US executive orders now require a Software Bill of Materials (SBOM) for all federal contractors, expanding after 2021 to cover critical software procurement; federal IT spending was $97.6B in 2024, raising stakes for compliance.

JFrog’s Xray and Artifactory map dependencies and vulnerabilities to produce SBOMs, positioning the company to capture rising demand—JFrog reported 2024 revenue of $338M, with security-driving ARR growth.

Political pressure effectively forces private firms seeking federal contracts to adopt SBOM-capable tooling, broadening JFrog’s addressable market as contractors and suppliers align with mandates.

Geopolitical Stability in Israel

International Trade and Tech Sanctions

Global trade tensions—especially US-China-Russia frictions—have prompted tighter export controls on software/security tech; in 2024 US BIS expanded rules impacting code and dev tools, forcing JFrog to manage distribution of binaries to avoid sanctions breaches. Regulatory complexity raises compliance costs—estimated software firms face 5–10% higher G&A—and can block sales in sanctioned markets, constraining revenue growth.

Public Sector Digital Transformation

- Global gov tech spend ~1T USD (2024)

- EU Digital Decade & US funding funnel billions to cloud-native upgrades

- Demand for secure CI/CD and SBOMs aligns with JFrog offerings

Global Software Sovereignty Initiatives

- EU policy favors interoperable tools; market tailwinds for neutrality

- JFrog supports multi-cloud/on-prem binary governance

- 2025: 35% ARR growth; presence in 40+ countries

JFrog tapped by $97.6B US IT spend as SBOM demand rises—Israel risk and export limits persist

US SBOM mandates and $97.6B federal IT spend (2024) expand demand for JFrog’s SBOM-capable tooling; 2024 revenue $338M and security-led ARR growth show market fit. Israel operations (~30% workforce, 2024) create geopolitical risk requiring redundancy. Export controls raised G&A ~5–10% and limit sales in sanctioned regions; global gov tech spend ≈ $1T (2024) and EU sovereignty drives multi-cloud demand.

| Metric | Value |

|---|---|

| Federal IT spend (2024) | $97.6B |

| JFrog revenue (2024) | $338M |

| Workforce in Israel (2024) | ~30% |

| Global gov tech spend (2024) | ≈$1T |

What is included in the product

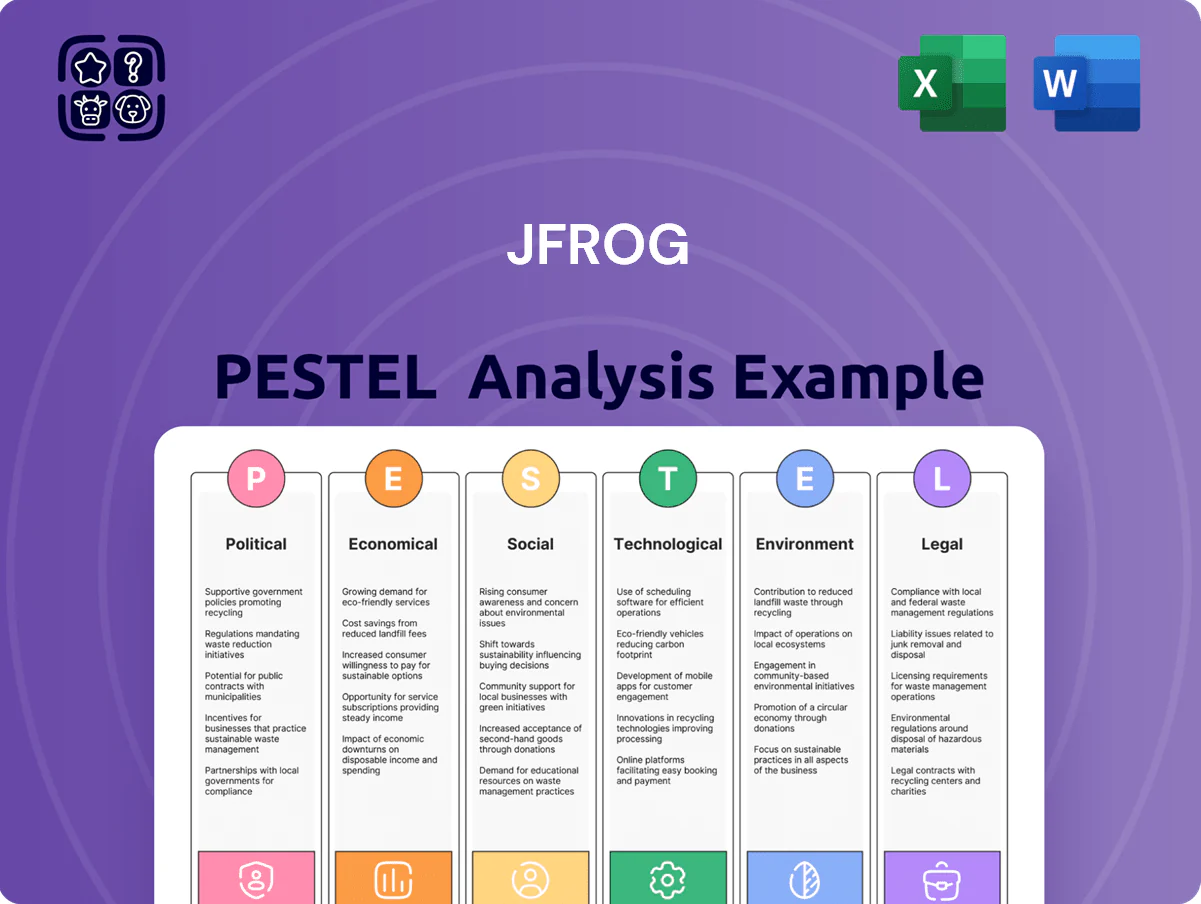

Explores how external macro-environmental factors uniquely affect JFrog across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented JFrog PESTLE summary that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and regulatory impacts.

Economic factors

Enterprise IT Spending Consolidation

By end-2025 many large enterprises are shifting from fragmented toolchains to consolidated DevOps platforms to cut TCO; Gartner estimated in 2024 that 40% of enterprise DevOps tool spend would be consolidated by 2026, accelerating vendor rationalization. JFrog stands to gain as customers replace multiple niche vendors with an integrated solution for binary management and security, supporting its subscription revenue growth (JFrog reported 2024 ARR of $214m). This consolidation is driven by IT budget scrutiny—CFOs demanding efficiency amid tighter macro conditions—boosting demand for platforms that lower license and maintenance costs.

Cloud Infrastructure Cost Management

Rising cloud storage and egress costs—Amazon S3 egress fees rose ~15% YoY in some segments through 2024—drive FinOps adoption and cloud optimization; JFrog’s artifact lifecycle and storage reclamation can cut binary storage by 30–60%, lowering recurring storage bills. JFrog’s edge caching and distribution reduce repeated egress, addressing CFO pressure as enterprises report cloud wastees at 20–35% of spend.

Global Interest Rate Stability and Growth

In late 2025, global policy rates stabilized around 3.5% on average in advanced economies, easing borrowing costs versus 2022–23 peaks and increasing available capital for corporate digital transformation. Lower yields have driven a 12–18% rise in enterprise IT CapEx allocations year-over-year, boosting investments in long-term infrastructure such as automated CI/CD pipelines. This economic stability enables JFrog to secure longer-term enterprise contracts as customers commit to multi-year technology roadmaps with greater confidence.

Labor Market for DevOps Talent

The persistent shortage of skilled DevOps and security engineers keeps US median DevOps salaries around $140k in 2024, sustaining high labor costs and driving demand for automation.

JFrog automates software supply chain and security auditing, reducing manual workload and effectively lowering per-feature engineering cost for firms.

Many organizations treat JFrog as a capitalized investment to boost productivity of costly technical staff and shorten time-to-market.

- High DevOps median pay ~$140k (2024)

- Automation reduces manual auditing hours

- JFrog seen as ROI trade-off to maximize expensive talent

Subscription Economy Resilience

JFrog's shift to a cloud-first, subscription model produced 2024 ARR of about $470m, boosting revenue visibility and cushioning against market swings.

As software repositories are mission-critical, enterprise churn remains low—net retention above 110% in 2024—preserving continuous development pipelines.

Predictable recurring cash flow enabled R&D spending near 22% of FY2024 revenue, sustaining innovation despite short-term economic pressures.

- 2024 ARR ≈ $470m

- Net dollar retention >110%

- R&D ≈22% of FY2024 revenue

JFrog surges as DevOps consolidation and FinOps cut cloud costs, driving ARR growth

Consolidation to integrated DevOps platforms (Gartner: 40% tool spend consolidated by 2026) boosts JFrog subscription growth; 2024 ARR reported ~470m and net retention >110%. Cloud egress/storage inflation (~15% YoY segments) and 20–35% cloud waste drive FinOps adoption; JFrog claims 30–60% artifact storage reduction. Skilled DevOps pay ~140k (2024) sustains automation demand; R&D ~22% of FY2024 revenue.

| Metric | 2024/2025 |

|---|---|

| ARR | $470m |

| Net retention | >110% |

| R&D | ~22% rev |

| DevOps median pay | $140k |

| Storage reduction | 30–60% |

Preview the Actual Deliverable

JFrog PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This JFrog PESTLE Analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and concise summaries. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and rapid technological change are shaping JFrog’s growth and risks—our concise PESTLE snapshot highlights the key external drivers you need to act on now; purchase the full analysis for a detailed, actionable roadmap to inform investment, strategy, or competitive planning.

Political factors

US Federal Security Mandates

The US executive orders now require a Software Bill of Materials (SBOM) for all federal contractors, expanding after 2021 to cover critical software procurement; federal IT spending was $97.6B in 2024, raising stakes for compliance.

JFrog’s Xray and Artifactory map dependencies and vulnerabilities to produce SBOMs, positioning the company to capture rising demand—JFrog reported 2024 revenue of $338M, with security-driving ARR growth.

Political pressure effectively forces private firms seeking federal contracts to adopt SBOM-capable tooling, broadening JFrog’s addressable market as contractors and suppliers align with mandates.

Geopolitical Stability in Israel

International Trade and Tech Sanctions

Global trade tensions—especially US-China-Russia frictions—have prompted tighter export controls on software/security tech; in 2024 US BIS expanded rules impacting code and dev tools, forcing JFrog to manage distribution of binaries to avoid sanctions breaches. Regulatory complexity raises compliance costs—estimated software firms face 5–10% higher G&A—and can block sales in sanctioned markets, constraining revenue growth.

Public Sector Digital Transformation

- Global gov tech spend ~1T USD (2024)

- EU Digital Decade & US funding funnel billions to cloud-native upgrades

- Demand for secure CI/CD and SBOMs aligns with JFrog offerings

Global Software Sovereignty Initiatives

- EU policy favors interoperable tools; market tailwinds for neutrality

- JFrog supports multi-cloud/on-prem binary governance

- 2025: 35% ARR growth; presence in 40+ countries

JFrog tapped by $97.6B US IT spend as SBOM demand rises—Israel risk and export limits persist

US SBOM mandates and $97.6B federal IT spend (2024) expand demand for JFrog’s SBOM-capable tooling; 2024 revenue $338M and security-led ARR growth show market fit. Israel operations (~30% workforce, 2024) create geopolitical risk requiring redundancy. Export controls raised G&A ~5–10% and limit sales in sanctioned regions; global gov tech spend ≈ $1T (2024) and EU sovereignty drives multi-cloud demand.

| Metric | Value |

|---|---|

| Federal IT spend (2024) | $97.6B |

| JFrog revenue (2024) | $338M |

| Workforce in Israel (2024) | ~30% |

| Global gov tech spend (2024) | ≈$1T |

What is included in the product

Explores how external macro-environmental factors uniquely affect JFrog across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented JFrog PESTLE summary that can be dropped into presentations or shared across teams to quickly align on external risks, market positioning, and regulatory impacts.

Economic factors

Enterprise IT Spending Consolidation

By end-2025 many large enterprises are shifting from fragmented toolchains to consolidated DevOps platforms to cut TCO; Gartner estimated in 2024 that 40% of enterprise DevOps tool spend would be consolidated by 2026, accelerating vendor rationalization. JFrog stands to gain as customers replace multiple niche vendors with an integrated solution for binary management and security, supporting its subscription revenue growth (JFrog reported 2024 ARR of $214m). This consolidation is driven by IT budget scrutiny—CFOs demanding efficiency amid tighter macro conditions—boosting demand for platforms that lower license and maintenance costs.

Cloud Infrastructure Cost Management

Rising cloud storage and egress costs—Amazon S3 egress fees rose ~15% YoY in some segments through 2024—drive FinOps adoption and cloud optimization; JFrog’s artifact lifecycle and storage reclamation can cut binary storage by 30–60%, lowering recurring storage bills. JFrog’s edge caching and distribution reduce repeated egress, addressing CFO pressure as enterprises report cloud wastees at 20–35% of spend.

Global Interest Rate Stability and Growth

In late 2025, global policy rates stabilized around 3.5% on average in advanced economies, easing borrowing costs versus 2022–23 peaks and increasing available capital for corporate digital transformation. Lower yields have driven a 12–18% rise in enterprise IT CapEx allocations year-over-year, boosting investments in long-term infrastructure such as automated CI/CD pipelines. This economic stability enables JFrog to secure longer-term enterprise contracts as customers commit to multi-year technology roadmaps with greater confidence.

Labor Market for DevOps Talent

The persistent shortage of skilled DevOps and security engineers keeps US median DevOps salaries around $140k in 2024, sustaining high labor costs and driving demand for automation.

JFrog automates software supply chain and security auditing, reducing manual workload and effectively lowering per-feature engineering cost for firms.

Many organizations treat JFrog as a capitalized investment to boost productivity of costly technical staff and shorten time-to-market.

- High DevOps median pay ~$140k (2024)

- Automation reduces manual auditing hours

- JFrog seen as ROI trade-off to maximize expensive talent

Subscription Economy Resilience

JFrog's shift to a cloud-first, subscription model produced 2024 ARR of about $470m, boosting revenue visibility and cushioning against market swings.

As software repositories are mission-critical, enterprise churn remains low—net retention above 110% in 2024—preserving continuous development pipelines.

Predictable recurring cash flow enabled R&D spending near 22% of FY2024 revenue, sustaining innovation despite short-term economic pressures.

- 2024 ARR ≈ $470m

- Net dollar retention >110%

- R&D ≈22% of FY2024 revenue

JFrog surges as DevOps consolidation and FinOps cut cloud costs, driving ARR growth

Consolidation to integrated DevOps platforms (Gartner: 40% tool spend consolidated by 2026) boosts JFrog subscription growth; 2024 ARR reported ~470m and net retention >110%. Cloud egress/storage inflation (~15% YoY segments) and 20–35% cloud waste drive FinOps adoption; JFrog claims 30–60% artifact storage reduction. Skilled DevOps pay ~140k (2024) sustains automation demand; R&D ~22% of FY2024 revenue.

| Metric | 2024/2025 |

|---|---|

| ARR | $470m |

| Net retention | >110% |

| R&D | ~22% rev |

| DevOps median pay | $140k |

| Storage reduction | 30–60% |

Preview the Actual Deliverable

JFrog PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This JFrog PESTLE Analysis covers political, economic, social, technological, legal, and environmental factors with actionable insights and concise summaries. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.