JGC Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

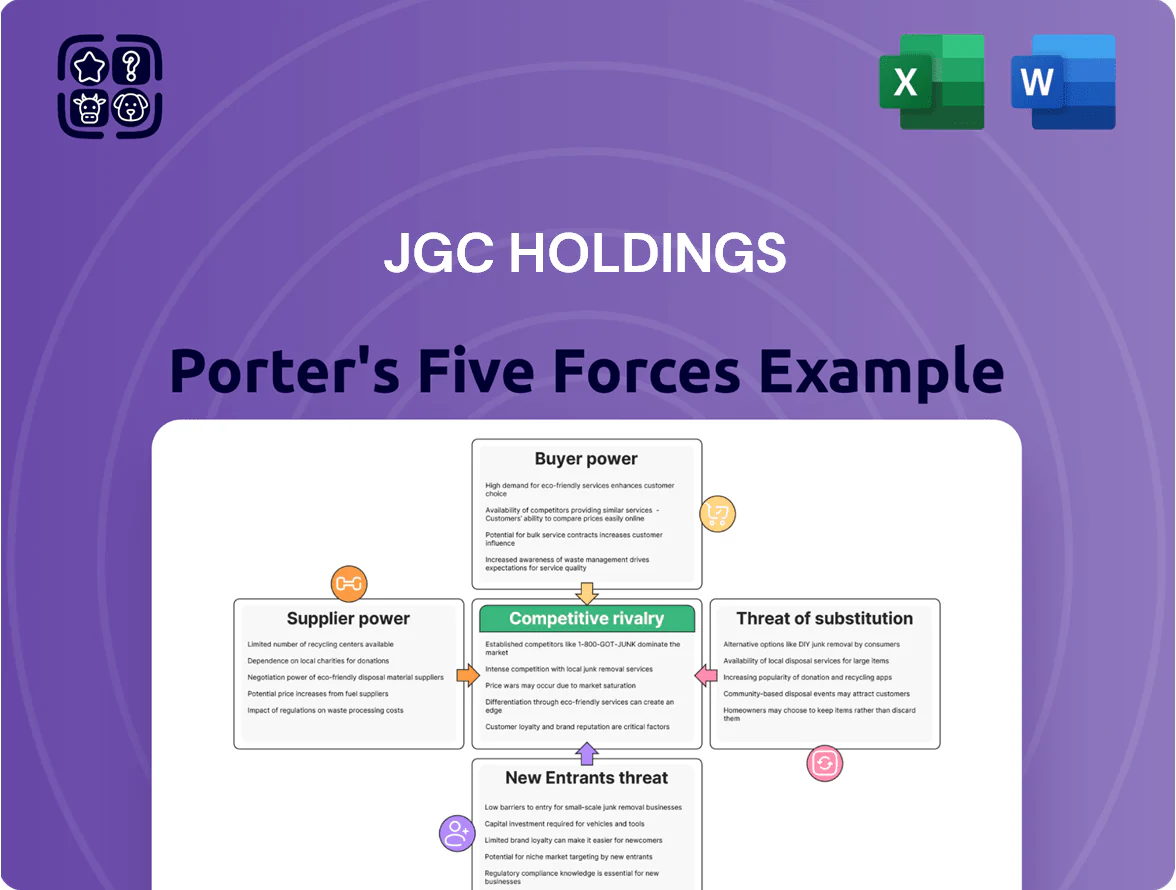

JGC Holdings faces moderate supplier power and high project complexity that shape contract margins, while buyer concentration and competitive rivalry pressure pricing and innovation—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JGC Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

JGC depends on a small set of high-tech makers for turbines, compressors and reactors, giving those suppliers strong leverage because failures hit plant performance and safety; procurement data shows a top-5 supplier concentration around 68% in large EPC contracts as of 2025.

Skilled Engineering and Technical Labor

The global shortage of highly specialized engineers and project managers creates dependence on a mobile expert workforce; McKinsey estimated a 2024 shortfall of 1.2 million skilled energy transition workers in Asia-Pacific, raising hiring costs for JGC.

As JGC expands in green hydrogen and CCS, demand for decarbonization skills has outpaced supply, with LinkedIn data showing 42% annual vacancy growth for such roles in 2024.

Specialized consultants and technical staff command 15–35% higher day rates versus conventional engineers, squeezing JGC project margins and increasing fixed labor overhead.

Raw Material and Commodity Providers

The procurement of steel, copper and specialized alloys exposes JGC Holdings to global price swings and geopolitics; steel futures rose 18% in 2024 and copper climbed 22% through Q3 2025, increasing input cost risk. Large commodity producers retain pricing leverage—top 5 steelmakers control ~40% of capacity—so JGC faces supplier-driven margin pressure during demand cycles. By end-2025, demand for certified low-carbon steel and alloys grew 35%, but certified supply is concentrated among a few firms, raising sourcing complexity and premium costs.

Regional Subcontractors and Local Content

In Middle East and Southeast Asia projects, JGC must use licensed local subcontractors to meet local content rules; in Saudi Arabia and Indonesia this affects ~35–50% of scope on large LNG/complex EPC jobs in 2024–25.

Those local firms hold strong bargaining power due to exclusive regional licenses, logistics networks, and limited qualified partners, forcing JGC into concentrated negotiations that can raise subcontract costs by 8–15% and extend mobilization by 2–6 weeks.

Logistics and Freight Service Providers

Supplier dominance, rising input costs & labor shortfalls squeeze project margins

Suppliers wield strong leverage: top‑5 equipment suppliers ≈68% share (2025), specialized labor shortfall ~1.2M in APAC (2024) pushed day rates +15–35%, steel +18% (2024) and copper +22% (YTD 2025) raised input costs, local content tied 35–50% scope (2024–25) adding 8–15% subcontract premium and 2–6 week delays; logistics consolidation → top10 carriers ~80% (2024), causing 5–8% bid variance.

| Metric | Value |

|---|---|

| Top‑5 supplier concentration | 68% (2025) |

| Skilled labor shortfall APAC | 1.2M (2024) |

| Specialist day‑rate premium | 15–35% |

| Steel price change | +18% (2024) |

| Copper price change | +22% (YTD 2025) |

| Local content scope | 35–50% (2024–25) |

| Local subcontract premium | 8–15% |

| Mobilization delay | +2–6 weeks |

| Top10 carrier share | ~80% (2024) |

| Logistics impact on bids | 5–8% variance (2023–24) |

What is included in the product

Tailored Porter's Five Forces analysis for JGC Holdings, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for JGC Holdings—quickly highlights competitive pressures and strategic risks to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Major Energy Clients

JGC’s revenue relies on a handful of national oil companies and global majors—top 10 clients account for roughly 60% of group orders in 2024—giving buyers strong leverage to push for lower margins and stricter payment terms.

These customers wield scale in tenders and often demand aggressive pricing and contract protections, compressing EPC margins and shifting risk to suppliers.

By late 2025 clients increasingly prefer partners with low-carbon credentials; procurement now scores lifecycle carbon intensity, and JGC faces loss of bids unless it proves emissions reductions across design and construction.

High Value and Complexity of Contracts

The multi-billion dollar scale of JGC Holdings’ EPC contracts (typical projects range USD 0.5–5.0bn) gives customers strong leverage to demand strict performance guarantees and liquidated damages, with penalty clauses often exceeding 5% of contract value; competitive bidding (50%+ of large projects in 2024 used two‑stage bids) forces JGC to balance technical innovation and cost cuts, and clients pressure execution throughout the lifecycle to protect their multi‑year capital commitments.

Shift Toward Sustainable Energy Mandates

Customers now require energy-transition tech—carbon capture and green ammonia—shaping JGC Holdings’ project scopes and boosting buyer leverage; 58% of major EPC contracts in 2024 included decarbonization clauses, rising to ~72% in 2025.

Buyers can demand JGC fund capability builds or adopt proprietary processes as contract terms, increasing upfront capital and R&D commitments by an estimated $120–180m annually for large contractors.

Since 2025 clients push decarbonization across supply chains, JGC faces faster adaptation cycles, with contract win rates tied to demonstrated low‑carbon credentials—projects meeting clients’ net‑zero criteria saw 30% higher award probability.

Information Symmetry and Procurement Expertise

Modern energy clients often have in-house engineering and procurement teams with deep EPC cost knowledge, shrinking JGC Holdings’ information advantage and pressuring margins; for example, 2024 surveys show 62% of oil & gas majors conduct detailed bid-cost benchmarking internally.

Clients routinely benchmark JGC bids against global peers—competitive pressure was visible in JGC’s FY2024 backlog growth of 3% despite 8% industry tendering growth—forcing tighter pricing and value-based contract terms.

- 62% of majors do internal bid benchmarking

- JGC FY2024 backlog +3% vs industry tenders +8%

- Higher client procurement skill → lower JGC pricing power

Low Switching Costs at the Bidding Stage

Before contract award customers can switch among top EPCs like JGC, Fluor, and Saipem, using bids to extract price and scope concessions; industry surveys show 65% of large oil & gas owners solicited three+ bids in 2024.

Mid-project switching costs are huge—change orders and delays can exceed 20% of contract value—so buyers press hard only during bidding.

JGC must sharpen technical differentiation, guaranteeability, and lifecycle cost data to avoid commoditization in a field where the top five EPCs shared ~60% of global LNG/FPSO awards in 2023.

- 65% of owners solicited 3+ bids (2024)

- Mid-project change can add 20%+ cost

- Top 5 EPCs won ~60% LNG/FPSO awards (2023)

- Differentiate on guarantees and lifecycle cost

Buyers’ leverage crushes EPC margins—decarb clauses up; carbon proofing boosts wins ~30%

Buyers wield high leverage: top 10 clients = ~60% of 2024 orders, 65% solicited 3+ bids (2024), and 62% do internal bid benchmarking, forcing lower EPC margins and strict guarantees (penalties often >5%). Decarbonization raises stakes—58% of major contracts had decarb clauses in 2024, ~72% in 2025—so lifecycle carbon proof now boosts win rates by ~30%.

| Metric | Value |

|---|---|

| Top‑10 client share (2024) | ~60% |

| Owners soliciting 3+ bids (2024) | 65% |

| Owners doing bid benchmarking (2024) | 62% |

| Decarb clauses in contracts (2024→2025) | 58% → ~72% |

| Penalty clauses | Often >5% contract value |

Same Document Delivered

JGC Holdings Porter's Five Forces Analysis

This preview shows the exact JGC Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment is complete you’ll get instant access to this same file. No mockups or samples—just the actual report.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

JGC Holdings faces moderate supplier power and high project complexity that shape contract margins, while buyer concentration and competitive rivalry pressure pricing and innovation—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JGC Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

JGC depends on a small set of high-tech makers for turbines, compressors and reactors, giving those suppliers strong leverage because failures hit plant performance and safety; procurement data shows a top-5 supplier concentration around 68% in large EPC contracts as of 2025.

Skilled Engineering and Technical Labor

The global shortage of highly specialized engineers and project managers creates dependence on a mobile expert workforce; McKinsey estimated a 2024 shortfall of 1.2 million skilled energy transition workers in Asia-Pacific, raising hiring costs for JGC.

As JGC expands in green hydrogen and CCS, demand for decarbonization skills has outpaced supply, with LinkedIn data showing 42% annual vacancy growth for such roles in 2024.

Specialized consultants and technical staff command 15–35% higher day rates versus conventional engineers, squeezing JGC project margins and increasing fixed labor overhead.

Raw Material and Commodity Providers

The procurement of steel, copper and specialized alloys exposes JGC Holdings to global price swings and geopolitics; steel futures rose 18% in 2024 and copper climbed 22% through Q3 2025, increasing input cost risk. Large commodity producers retain pricing leverage—top 5 steelmakers control ~40% of capacity—so JGC faces supplier-driven margin pressure during demand cycles. By end-2025, demand for certified low-carbon steel and alloys grew 35%, but certified supply is concentrated among a few firms, raising sourcing complexity and premium costs.

Regional Subcontractors and Local Content

In Middle East and Southeast Asia projects, JGC must use licensed local subcontractors to meet local content rules; in Saudi Arabia and Indonesia this affects ~35–50% of scope on large LNG/complex EPC jobs in 2024–25.

Those local firms hold strong bargaining power due to exclusive regional licenses, logistics networks, and limited qualified partners, forcing JGC into concentrated negotiations that can raise subcontract costs by 8–15% and extend mobilization by 2–6 weeks.

Logistics and Freight Service Providers

Supplier dominance, rising input costs & labor shortfalls squeeze project margins

Suppliers wield strong leverage: top‑5 equipment suppliers ≈68% share (2025), specialized labor shortfall ~1.2M in APAC (2024) pushed day rates +15–35%, steel +18% (2024) and copper +22% (YTD 2025) raised input costs, local content tied 35–50% scope (2024–25) adding 8–15% subcontract premium and 2–6 week delays; logistics consolidation → top10 carriers ~80% (2024), causing 5–8% bid variance.

| Metric | Value |

|---|---|

| Top‑5 supplier concentration | 68% (2025) |

| Skilled labor shortfall APAC | 1.2M (2024) |

| Specialist day‑rate premium | 15–35% |

| Steel price change | +18% (2024) |

| Copper price change | +22% (YTD 2025) |

| Local content scope | 35–50% (2024–25) |

| Local subcontract premium | 8–15% |

| Mobilization delay | +2–6 weeks |

| Top10 carrier share | ~80% (2024) |

| Logistics impact on bids | 5–8% variance (2023–24) |

What is included in the product

Tailored Porter's Five Forces analysis for JGC Holdings, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its profitability and strategic positioning.

A concise Porter's Five Forces snapshot for JGC Holdings—quickly highlights competitive pressures and strategic risks to streamline boardroom decisions.

Customers Bargaining Power

Concentration of Major Energy Clients

JGC’s revenue relies on a handful of national oil companies and global majors—top 10 clients account for roughly 60% of group orders in 2024—giving buyers strong leverage to push for lower margins and stricter payment terms.

These customers wield scale in tenders and often demand aggressive pricing and contract protections, compressing EPC margins and shifting risk to suppliers.

By late 2025 clients increasingly prefer partners with low-carbon credentials; procurement now scores lifecycle carbon intensity, and JGC faces loss of bids unless it proves emissions reductions across design and construction.

High Value and Complexity of Contracts

The multi-billion dollar scale of JGC Holdings’ EPC contracts (typical projects range USD 0.5–5.0bn) gives customers strong leverage to demand strict performance guarantees and liquidated damages, with penalty clauses often exceeding 5% of contract value; competitive bidding (50%+ of large projects in 2024 used two‑stage bids) forces JGC to balance technical innovation and cost cuts, and clients pressure execution throughout the lifecycle to protect their multi‑year capital commitments.

Shift Toward Sustainable Energy Mandates

Customers now require energy-transition tech—carbon capture and green ammonia—shaping JGC Holdings’ project scopes and boosting buyer leverage; 58% of major EPC contracts in 2024 included decarbonization clauses, rising to ~72% in 2025.

Buyers can demand JGC fund capability builds or adopt proprietary processes as contract terms, increasing upfront capital and R&D commitments by an estimated $120–180m annually for large contractors.

Since 2025 clients push decarbonization across supply chains, JGC faces faster adaptation cycles, with contract win rates tied to demonstrated low‑carbon credentials—projects meeting clients’ net‑zero criteria saw 30% higher award probability.

Information Symmetry and Procurement Expertise

Modern energy clients often have in-house engineering and procurement teams with deep EPC cost knowledge, shrinking JGC Holdings’ information advantage and pressuring margins; for example, 2024 surveys show 62% of oil & gas majors conduct detailed bid-cost benchmarking internally.

Clients routinely benchmark JGC bids against global peers—competitive pressure was visible in JGC’s FY2024 backlog growth of 3% despite 8% industry tendering growth—forcing tighter pricing and value-based contract terms.

- 62% of majors do internal bid benchmarking

- JGC FY2024 backlog +3% vs industry tenders +8%

- Higher client procurement skill → lower JGC pricing power

Low Switching Costs at the Bidding Stage

Before contract award customers can switch among top EPCs like JGC, Fluor, and Saipem, using bids to extract price and scope concessions; industry surveys show 65% of large oil & gas owners solicited three+ bids in 2024.

Mid-project switching costs are huge—change orders and delays can exceed 20% of contract value—so buyers press hard only during bidding.

JGC must sharpen technical differentiation, guaranteeability, and lifecycle cost data to avoid commoditization in a field where the top five EPCs shared ~60% of global LNG/FPSO awards in 2023.

- 65% of owners solicited 3+ bids (2024)

- Mid-project change can add 20%+ cost

- Top 5 EPCs won ~60% LNG/FPSO awards (2023)

- Differentiate on guarantees and lifecycle cost

Buyers’ leverage crushes EPC margins—decarb clauses up; carbon proofing boosts wins ~30%

Buyers wield high leverage: top 10 clients = ~60% of 2024 orders, 65% solicited 3+ bids (2024), and 62% do internal bid benchmarking, forcing lower EPC margins and strict guarantees (penalties often >5%). Decarbonization raises stakes—58% of major contracts had decarb clauses in 2024, ~72% in 2025—so lifecycle carbon proof now boosts win rates by ~30%.

| Metric | Value |

|---|---|

| Top‑10 client share (2024) | ~60% |

| Owners soliciting 3+ bids (2024) | 65% |

| Owners doing bid benchmarking (2024) | 62% |

| Decarb clauses in contracts (2024→2025) | 58% → ~72% |

| Penalty clauses | Often >5% contract value |

Same Document Delivered

JGC Holdings Porter's Five Forces Analysis

This preview shows the exact JGC Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment is complete you’ll get instant access to this same file. No mockups or samples—just the actual report.