JinJiang Hotels SWOT Analysis

Your Strategic Toolkit Starts Here

JinJiang Hotels leverages a vast, diversified portfolio and strong state-backed backing to capture domestic and inbound travel growth, yet faces margin pressure from intense competition and integration risks from recent acquisitions. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

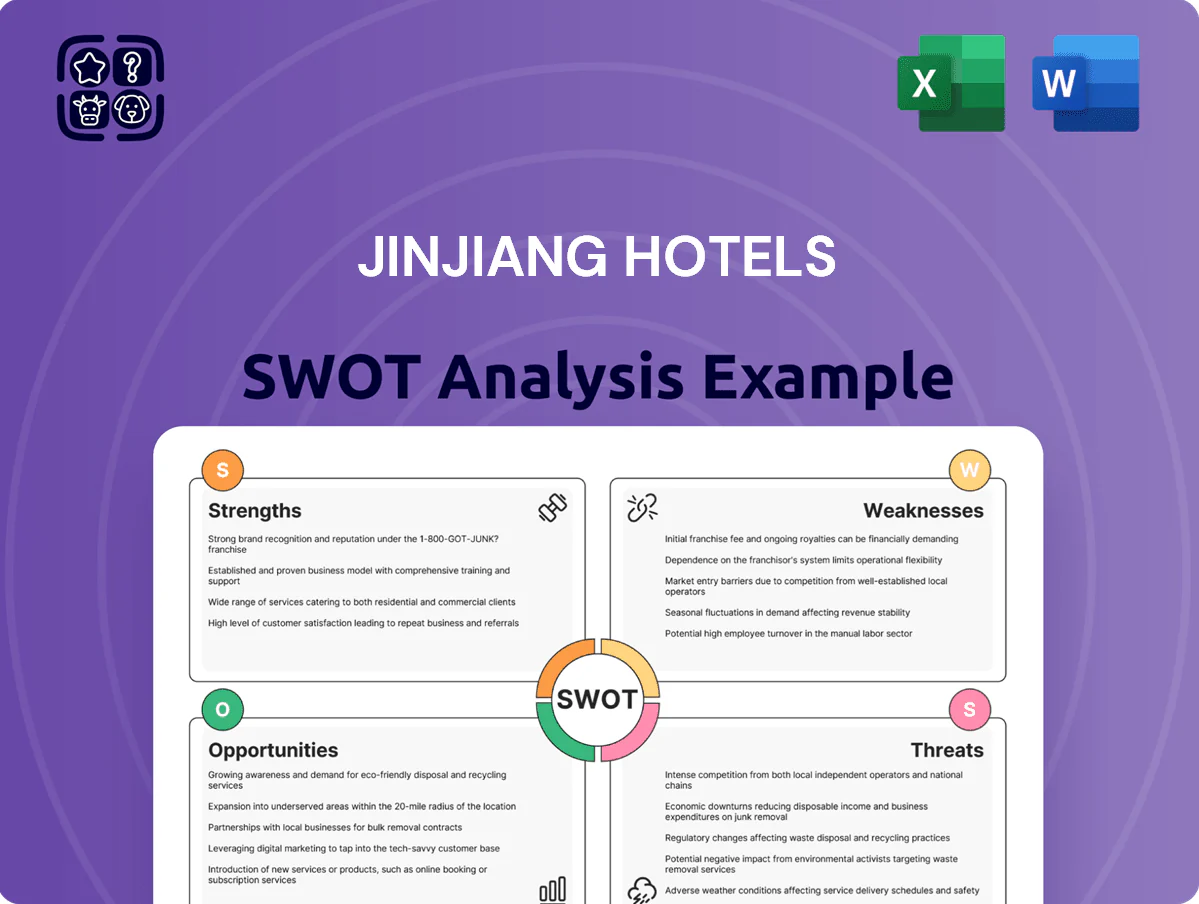

Strengths

Global Scale and Market Leadership

As of late 2025, JinJiang Hotels operates over 10,000 properties and roughly 800,000 rooms, ranking among the world’s largest hotel groups by room count. This scale gives strong bargaining power with suppliers, lowering procurement costs and improving margin levers—JinJiang reported group revenue of CNY 110 billion in FY2024. The network spans 120+ countries, securing broad presence in China and Europe and capturing leisure, business, and budget traveler segments.

State-Owned Enterprise Support

JinJiang, as a leading Chinese state-owned enterprise, enjoys preferential capital access—its 2024 group debt refinancing included a CNY 8.5 billion facility backed by state-linked banks—giving it resilience in downturns. Government backing speeds domestic rollouts: JinJiang opened 1,200+ new rooms in 2024 under state-supported financing. This institutional support lowers funding costs for multiyear infrastructure and underpins large overseas deals, such as the 2023 minority stake acquisitions financed with state-backed credit.

Diverse Brand Portfolio

JinJiang Hotels runs a wide brand mix from economy to luxury—covering domestic budget chains and global names like Radisson, Louvre Hotels, and Vienna Hotels—totaling over 10,000 hotels and 1.4 million rooms by end-2024.

Integrated Tourism Ecosystem

JinJiang’s holdings in travel agencies and transport create a tourism ecosystem that captured about 42% of group room nights via internal channels in 2024, boosting direct revenue and reducing OTA fees.

Controlling bookings, transfers, and packages lets JinJiang bundle stays with flights and tours, raising repeat-booking rates—group loyalty program members drove 36% of revenue in 2024.

This vertical integration gives JinJiang a cost and distribution edge vs pure-play hotels, cutting customer acquisition costs and improving RevPAR resilience during demand shocks.

- 42% internal room nights (2024)

- 36% revenue from loyalty members (2024)

- Lower OTA fees, higher RevPAR stability

Dominant Position in China

JinJiang scale and state backing power margins: 1.4M rooms, CNY110bn, RevPAR near 2019

JinJiang’s scale (10,000+ hotels, ~1.4m rooms by 2024) drives procurement leverage and margin upside; group revenue was CNY 110bn in FY2024. State backing enabled a CNY 8.5bn refinancing facility in 2024 and rapid rollout (1,200+ rooms opened). Vertical integration (42% internal room nights; 36% loyalty revenue in 2024) cuts OTA costs and boosts RevPAR resilience (domestic RevPAR 96% of 2019).

| Metric | Value (2024) |

|---|---|

| Hotels / Rooms | 10,000+ / 1.4m |

| Group revenue | CNY 110bn |

| State-backed facility | CNY 8.5bn |

| Internal room nights | 42% |

| Loyalty revenue | 36% |

| Domestic RevPAR vs 2019 | 96% |

What is included in the product

Delivers a strategic overview of JinJiang Hotels’s internal and external business factors, highlighting its brand scale and distribution strengths, operational and integration challenges, growth opportunities in domestic and international leisure travel, and risks from market competition and regulatory shifts.

Delivers a compact SWOT matrix that highlights JinJiang Hotels' strategic strengths and risks for rapid executive alignment and decision-making.

Weaknesses

High Debt and Financial Leverage

The aggressive acquisition-led growth left JinJiang Hotels (JinJiang International, listed 600754.SH) with about RMB 97.6 billion total debt and a net gearing ~62% as of FY2024, constraining cash for organic renovations and tech upgrades amid higher borrowing costs.

Higher interest expense—RMB 4.1 billion in 2024—means servicing debt can crowd out capex; analysts warn leverage becomes a material risk if operating cash flow dips, given thin margins in budget segments.

Complex Brand Integration

Managing a wide portfolio—Radisson (acquired stake 2022) and Louvre Hotels Group (2021 acquisition completed)—creates operational and cultural friction, with Jin Jiang operating 9,000+ hotels in 2024 across 20+ countries, raising integration costs and coordination overhead.

Disparate PMS and reporting systems slow decisions; a 2023 internal review cited 12–18 month lag times for global policy rollouts, increasing SG&A per room by an estimated 6% vs. peers.

Maintaining consistent brand standards across brands with different service models remains tough: guest NPS variance reached 18 points in 2024 between legacy Jin Jiang and recently acquired European brands.

Heavy Reliance on Domestic Market

Despite operating in 60+ countries, JinJiang International Holdings (parent of JinJiang Hotels) earned about 82% of 2024 revenue and ~85% of operating profit from Mainland China, concentrating cashflow in one market.

This exposes the group to China-specific risks: 2023–24 GDP growth dips (5.2% in 2023, 2024 est. 4.5%), policy shifts, and travel restrictions that can cut occupancy and ADR quickly.

Diversification remains slow: international room count was only ~18% of total in 2024, so geographic risk is not yet balanced.

Lower Margins in Economy Segments

- ~62% room share in economy brands

- Economy EBITDA ~8–10% (2024)

- OpEx/room +9% (2023–2025)

- Break-even occupancy often >75%

Bureaucratic Decision Making

As a large state-owned enterprise, Jinjiang Hotels (Jinjiang International, 600754.SS) often faces bureaucratic hurdles that slow responses to rapid market shifts; in 2024 the group’s decision cycles reportedly extended rollout times by 30–40% versus private peers.

The layered management slows agility against tech-driven rivals, delaying digital upgrades—Jinjiang spent 1.8% of 2024 revenue on IT versus 3.5% industry average—hindering quick pivots in fast-moving international markets.

- Decision cycles 30–40% longer than private rivals

- IT spend 1.8% of 2024 revenue vs 3.5% industry avg

- Slower rollout of digital booking/CRM features

- Reduced agility in international expansion

High leverage and China concentration squeeze margins, capex and digital agility

Heavy acquisition-driven debt (RMB 97.6bn; net gearing ~62% in FY2024) raises interest costs (RMB 4.1bn in 2024) and limits capex; 82% revenue concentration in Mainland China with only ~18% rooms abroad increases market risk; ~62% room share in economy brands yields low EBITDA (8–10% in 2024) and requires >75% break-even occupancy; IT spend 1.8% of revenue vs 3.5% peers slows digital agility.

| Metric | 2024 |

|---|---|

| Total debt | RMB 97.6bn |

| Net gearing | ~62% |

| Interest expense | RMB 4.1bn |

| Revenue from China | ~82% |

| International room share | ~18% |

| Economy room share | ~62% |

| Economy EBITDA | 8–10% |

| IT spend | 1.8% of revenue |

Preview Before You Purchase

JinJiang Hotels SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you can download after payment. Purchase unlocks the complete, in-depth JinJiang Hotels analysis for immediate use in strategy or valuation work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

JinJiang Hotels leverages a vast, diversified portfolio and strong state-backed backing to capture domestic and inbound travel growth, yet faces margin pressure from intense competition and integration risks from recent acquisitions. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Global Scale and Market Leadership

As of late 2025, JinJiang Hotels operates over 10,000 properties and roughly 800,000 rooms, ranking among the world’s largest hotel groups by room count. This scale gives strong bargaining power with suppliers, lowering procurement costs and improving margin levers—JinJiang reported group revenue of CNY 110 billion in FY2024. The network spans 120+ countries, securing broad presence in China and Europe and capturing leisure, business, and budget traveler segments.

State-Owned Enterprise Support

JinJiang, as a leading Chinese state-owned enterprise, enjoys preferential capital access—its 2024 group debt refinancing included a CNY 8.5 billion facility backed by state-linked banks—giving it resilience in downturns. Government backing speeds domestic rollouts: JinJiang opened 1,200+ new rooms in 2024 under state-supported financing. This institutional support lowers funding costs for multiyear infrastructure and underpins large overseas deals, such as the 2023 minority stake acquisitions financed with state-backed credit.

Diverse Brand Portfolio

JinJiang Hotels runs a wide brand mix from economy to luxury—covering domestic budget chains and global names like Radisson, Louvre Hotels, and Vienna Hotels—totaling over 10,000 hotels and 1.4 million rooms by end-2024.

Integrated Tourism Ecosystem

JinJiang’s holdings in travel agencies and transport create a tourism ecosystem that captured about 42% of group room nights via internal channels in 2024, boosting direct revenue and reducing OTA fees.

Controlling bookings, transfers, and packages lets JinJiang bundle stays with flights and tours, raising repeat-booking rates—group loyalty program members drove 36% of revenue in 2024.

This vertical integration gives JinJiang a cost and distribution edge vs pure-play hotels, cutting customer acquisition costs and improving RevPAR resilience during demand shocks.

- 42% internal room nights (2024)

- 36% revenue from loyalty members (2024)

- Lower OTA fees, higher RevPAR stability

Dominant Position in China

JinJiang scale and state backing power margins: 1.4M rooms, CNY110bn, RevPAR near 2019

JinJiang’s scale (10,000+ hotels, ~1.4m rooms by 2024) drives procurement leverage and margin upside; group revenue was CNY 110bn in FY2024. State backing enabled a CNY 8.5bn refinancing facility in 2024 and rapid rollout (1,200+ rooms opened). Vertical integration (42% internal room nights; 36% loyalty revenue in 2024) cuts OTA costs and boosts RevPAR resilience (domestic RevPAR 96% of 2019).

| Metric | Value (2024) |

|---|---|

| Hotels / Rooms | 10,000+ / 1.4m |

| Group revenue | CNY 110bn |

| State-backed facility | CNY 8.5bn |

| Internal room nights | 42% |

| Loyalty revenue | 36% |

| Domestic RevPAR vs 2019 | 96% |

What is included in the product

Delivers a strategic overview of JinJiang Hotels’s internal and external business factors, highlighting its brand scale and distribution strengths, operational and integration challenges, growth opportunities in domestic and international leisure travel, and risks from market competition and regulatory shifts.

Delivers a compact SWOT matrix that highlights JinJiang Hotels' strategic strengths and risks for rapid executive alignment and decision-making.

Weaknesses

High Debt and Financial Leverage

The aggressive acquisition-led growth left JinJiang Hotels (JinJiang International, listed 600754.SH) with about RMB 97.6 billion total debt and a net gearing ~62% as of FY2024, constraining cash for organic renovations and tech upgrades amid higher borrowing costs.

Higher interest expense—RMB 4.1 billion in 2024—means servicing debt can crowd out capex; analysts warn leverage becomes a material risk if operating cash flow dips, given thin margins in budget segments.

Complex Brand Integration

Managing a wide portfolio—Radisson (acquired stake 2022) and Louvre Hotels Group (2021 acquisition completed)—creates operational and cultural friction, with Jin Jiang operating 9,000+ hotels in 2024 across 20+ countries, raising integration costs and coordination overhead.

Disparate PMS and reporting systems slow decisions; a 2023 internal review cited 12–18 month lag times for global policy rollouts, increasing SG&A per room by an estimated 6% vs. peers.

Maintaining consistent brand standards across brands with different service models remains tough: guest NPS variance reached 18 points in 2024 between legacy Jin Jiang and recently acquired European brands.

Heavy Reliance on Domestic Market

Despite operating in 60+ countries, JinJiang International Holdings (parent of JinJiang Hotels) earned about 82% of 2024 revenue and ~85% of operating profit from Mainland China, concentrating cashflow in one market.

This exposes the group to China-specific risks: 2023–24 GDP growth dips (5.2% in 2023, 2024 est. 4.5%), policy shifts, and travel restrictions that can cut occupancy and ADR quickly.

Diversification remains slow: international room count was only ~18% of total in 2024, so geographic risk is not yet balanced.

Lower Margins in Economy Segments

- ~62% room share in economy brands

- Economy EBITDA ~8–10% (2024)

- OpEx/room +9% (2023–2025)

- Break-even occupancy often >75%

Bureaucratic Decision Making

As a large state-owned enterprise, Jinjiang Hotels (Jinjiang International, 600754.SS) often faces bureaucratic hurdles that slow responses to rapid market shifts; in 2024 the group’s decision cycles reportedly extended rollout times by 30–40% versus private peers.

The layered management slows agility against tech-driven rivals, delaying digital upgrades—Jinjiang spent 1.8% of 2024 revenue on IT versus 3.5% industry average—hindering quick pivots in fast-moving international markets.

- Decision cycles 30–40% longer than private rivals

- IT spend 1.8% of 2024 revenue vs 3.5% industry avg

- Slower rollout of digital booking/CRM features

- Reduced agility in international expansion

High leverage and China concentration squeeze margins, capex and digital agility

Heavy acquisition-driven debt (RMB 97.6bn; net gearing ~62% in FY2024) raises interest costs (RMB 4.1bn in 2024) and limits capex; 82% revenue concentration in Mainland China with only ~18% rooms abroad increases market risk; ~62% room share in economy brands yields low EBITDA (8–10% in 2024) and requires >75% break-even occupancy; IT spend 1.8% of revenue vs 3.5% peers slows digital agility.

| Metric | 2024 |

|---|---|

| Total debt | RMB 97.6bn |

| Net gearing | ~62% |

| Interest expense | RMB 4.1bn |

| Revenue from China | ~82% |

| International room share | ~18% |

| Economy room share | ~62% |

| Economy EBITDA | 8–10% |

| IT spend | 1.8% of revenue |

Preview Before You Purchase

JinJiang Hotels SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you can download after payment. Purchase unlocks the complete, in-depth JinJiang Hotels analysis for immediate use in strategy or valuation work.