JINS Holdings PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and rapid eyewear tech innovation are reshaping JINS Holdings' competitive outlook—our concise PESTLE snapshot highlights risks and opportunities you can act on today. Purchase the full PESTLE analysis to access detailed regulatory, social, and environmental insights, ready-made for investors, strategists, and planners seeking an immediate strategic advantage.

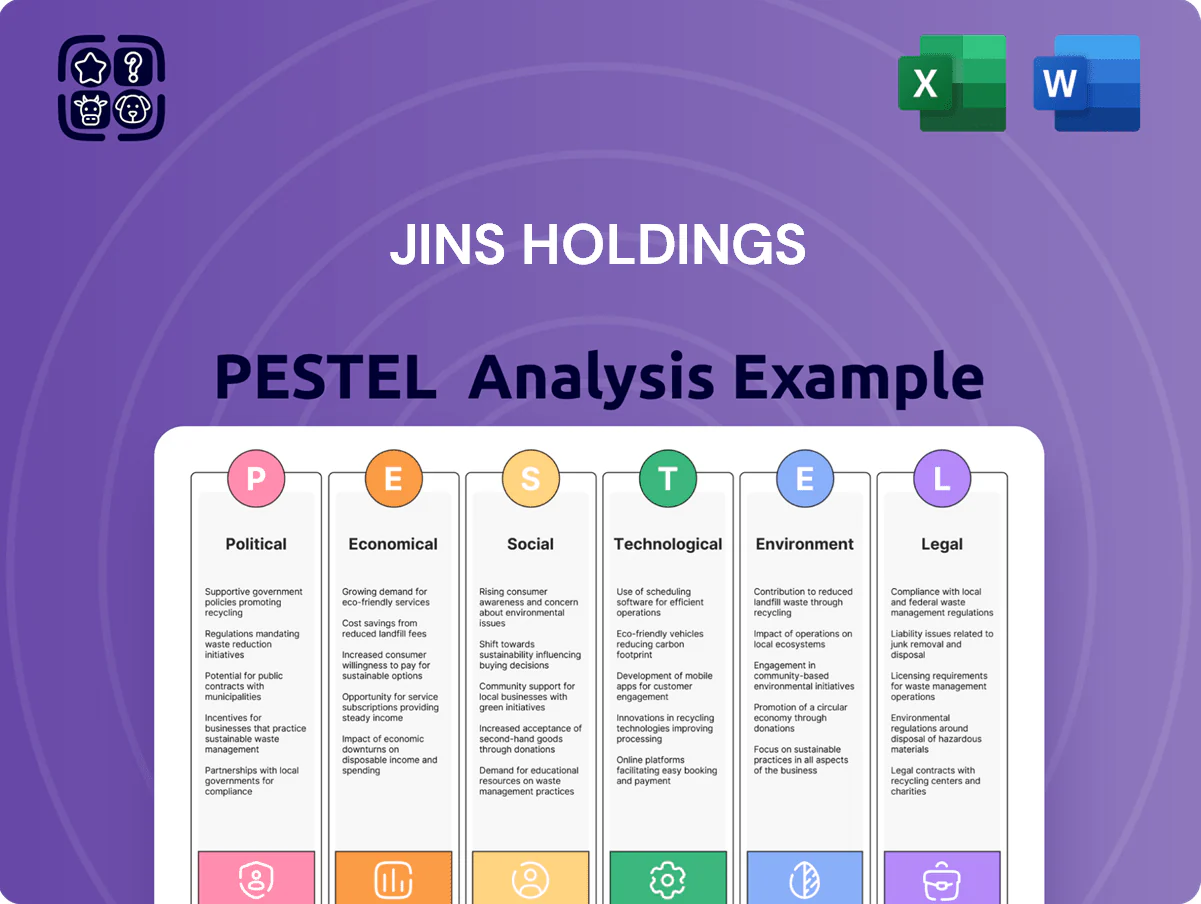

Political factors

Geopolitical supply chain risks

JINS Holdings depends on China and Asian manufacturing for ~70% of its frames to sustain low-cost operations; in 2024 rising US-China tensions and a 12% average tariff scenario could raise COGS materially. Ongoing geopolitical risks—shipping delays (Suez/Red Sea and South China Sea congestion increased lead times by ~20% in 2023)—threaten margins and retail prices. Management must diversify suppliers, add nearshoring in ASEAN/Japan, and hedge tariff exposure to preserve price stability and continuity.

Japan-China trade relations

As a Japanese entity with major production and retail in China, JINS is exposed to Tokyo-Beijing tensions; after 2019 trade frictions and a 2023 surge in consumer nationalism, Japanese brands faced up to 15-25% temporary sales drops in China, risking similar impacts on JINS, which reported ~¥40bn consolidated revenue in FY2024 with China as a key growth market; diplomatic escalation could trigger boycotts or stricter approvals that impede expansion.

National health promotion policies

The Japanese government has intensified focus on eye health as myopia rates among children rose to about 50% by 2023 and an aging workforce pushed demand for vision care; JINS gains from public campaigns promoting regular eye exams and protective eyewear, evidenced by government subsidies for vision screening programs reaching municipalities nationwide. Alignment with these initiatives lets JINS market frames and blue-light lenses as essential health tools, supporting its FY2024 retail growth and helping capture a larger share of an estimated ¥300 billion domestic eyewear market.

Foreign investment and trade agreements

Participation in CPTPP and similar agreements eases JINS Holdings expansion into Southeast Asia, where eyewear market growth is forecast at ~6–8% CAGR to 2028 and Vietnam/Philippines retail sales grew 8.2% and 7.5% in 2024 respectively.

Reduced tariffs and clearer investment rules lower entry costs and legal risk for JINS, supporting targets to lift international revenue share above 25% by 2026.

- Lower tariffs and harmonized standards via CPTPP

- Regional retail growth: Vietnam 8.2% (2024), Philippines 7.5% (2024)

- Target: international revenue >25% by 2026

Changes in retail tax regulations

Potential adjustments to Japan's consumption tax (10% since 2019) or corporate tax revisions could compress JINS Holdings' FY2024 operating margin (3.8% in FY2023) and reduce retail spending—household real consumption rose 1.2% YoY in 2024, but a tax hike could reverse this trend.

Political debate on fiscal tightening affects timing of JINS's store expansion and CAPEX: JINS opened 28 net stores in 2024; uncertainty may delay further openings.

The company must stay agile, adjusting pricing, promotions, and cost structure to legislative shifts impacting the retail sector.

- Consumption tax at 10% since 2019; any hike could cut consumer spend and margins

- FY2023 operating margin 3.8%; sensitive to tax/corporate rate changes

- Opened 28 net stores in 2024—expansion timing tied to fiscal policy clarity

- Requires dynamic pricing and CAPEX flexibility to mitigate legislative risks

Tariff, tax and China risks threaten ¥40bn revenue and thin 3.8% margins

Political risks: US-China tensions and possible 12% tariffs could raise COGS; shipping delays added ~20% lead times in 2023. Tokyo-Beijing frictions risk 15–25% China sales dips; China crucial to ~¥40bn FY2024 revenue. CPTPP lowers entry costs for SEA (Vietnam 8.2%, Philippines 7.5% retail growth in 2024). Consumption tax at 10% and potential hikes threaten margins (FY2023 OM 3.8%); opened 28 net stores in 2024.

| Metric | Value |

|---|---|

| FY2024 revenue (approx.) | ¥40bn |

| FY2023 operating margin | 3.8% |

| China sales drop risk | 15–25% |

| Tariff stress case | ~12% avg |

| SEA retail growth (2024) | VNM 8.2%, PHL 7.5% |

| Net stores opened (2024) | 28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically shape JINS Holdings’ eyewear manufacturing, retail and DTC channels, combining current data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for JINS Holdings that eases meeting prep, supports quick alignment across teams, and can be dropped into presentations or strategy packs for clear discussion of external risks and market positioning.

Economic factors

Japanese Yen exchange rate volatility

JINS imports much of its materials and finished goods, so Yen volatility materially affects COGS: a 10% Yen depreciation vs USD in 2023 raised import costs and, per industry estimates, could cut gross margin by ~1.5–2.0 percentage points if retail prices remain unchanged; the Yen strengthened ~6% in 2024 y/y, easing procurement costs and enabling either modest price reductions or margin expansion on JINS’s value eyewear lines.

Rising domestic labor costs

Japan's chronic labor shortage has pushed average hourly wages up 3.3% year-on-year in 2024, increasing costs for retail and manufacturing staff at JINS Holdings. The company must balance high-touch in-store service with rising human capital expenses that pressured operating margins in FY2024. JINS is investing in automation and self-service kiosks—capital expenditures rose 12% in 2024—to preserve service quality while improving labor productivity. These tech investments aim to offset wage inflation and stabilize unit labor costs.

Consumer spending power shifts

Economic stagnation and 2.6% CPI inflation in Japan (2024) pressure middle-class discretionary spending, risking delays in non-essential eyewear purchases despite JINS’s value-based pricing and FY2024 domestic same-store sales growth of 1.8%. Prolonged downturns could reduce unit volumes even as ASP resilience helps protect margins. JINS monitors CPI, household spending (down 0.4% YoY in 2024 Q3) and adjusts marketing spend and promotions to align with consumer sentiment.

Global inflationary pressures

Rising global energy, logistics and raw-material costs—container rates up ~25% in 2024 vs 2022 and global oil prices averaging ~$80/barrel in 2024—increase eyewear production costs, pressuring JINS to absorb margin hits or raise prices against price-sensitive customers.

JINS must deploy strategic sourcing and lean supply-chain measures; in 2024 efficient procurement and supplier diversification helped peers limit COGS inflation to ~3–5 percentage points.

- Container rates +25% (2024 vs 2022)

- Oil ~$80/barrel (2024 average)

- Peers limited COGS inflation to ~3–5 pp via sourcing

Expansion into emerging markets

Expansion into Taiwan and Southeast Asia taps regions with 2024 GDP growth forecasts of 2.5–5.0% (Taiwan ~2.8%, ASEAN average ~4.5%), offering JINS higher growth than Japan’s ~1.0% in 2024; rising middle-class households—projected to add ~140 million people in Asia by 2030—increase demand for fashionable, functional eyewear, supporting revenue diversification beyond mature domestic sales.

- Higher regional GDP growth vs Japan (~4–5% ASEAN vs ~1% Japan in 2024)

- Taiwan GDP ~2.8% (2024 est.)

- Asian middle class to grow by ~140M by 2030

- Opportunity for revenue diversification and price-premium products

JINS margins squeezed by costs; yen strength and ASEAN growth offer partial relief

Yen volatility, rising wages (+3.3% 2024), and higher logistics/oil (container +25% vs 2022; oil ~$80/barrel 2024) pressured COGS and margins, partially offset by Yen strengthening ~6% in 2024 and JINS automation capex +12%; domestic demand weak (CPI 2.6%, household spending -0.4% Q3 2024) while ASEAN/Taiwan growth (ASEAN ~4.5%, Taiwan ~2.8% 2024) offers diversification.

| Metric | 2024 |

|---|---|

| Yen vs USD | +6% strength |

| Wage growth | +3.3% |

| Container rates | +25% vs 2022 |

| Oil | ~$80/barrel |

| Japan GDP | ~1.0% |

| ASEAN avg GDP | ~4.5% |

Preview Before You Purchase

JINS Holdings PESTLE Analysis

The preview shown here is the exact JINS Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or omissions. After checkout you’ll instantly download this same final document, suitable for analysis, presentations, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and rapid eyewear tech innovation are reshaping JINS Holdings' competitive outlook—our concise PESTLE snapshot highlights risks and opportunities you can act on today. Purchase the full PESTLE analysis to access detailed regulatory, social, and environmental insights, ready-made for investors, strategists, and planners seeking an immediate strategic advantage.

Political factors

Geopolitical supply chain risks

JINS Holdings depends on China and Asian manufacturing for ~70% of its frames to sustain low-cost operations; in 2024 rising US-China tensions and a 12% average tariff scenario could raise COGS materially. Ongoing geopolitical risks—shipping delays (Suez/Red Sea and South China Sea congestion increased lead times by ~20% in 2023)—threaten margins and retail prices. Management must diversify suppliers, add nearshoring in ASEAN/Japan, and hedge tariff exposure to preserve price stability and continuity.

Japan-China trade relations

As a Japanese entity with major production and retail in China, JINS is exposed to Tokyo-Beijing tensions; after 2019 trade frictions and a 2023 surge in consumer nationalism, Japanese brands faced up to 15-25% temporary sales drops in China, risking similar impacts on JINS, which reported ~¥40bn consolidated revenue in FY2024 with China as a key growth market; diplomatic escalation could trigger boycotts or stricter approvals that impede expansion.

National health promotion policies

The Japanese government has intensified focus on eye health as myopia rates among children rose to about 50% by 2023 and an aging workforce pushed demand for vision care; JINS gains from public campaigns promoting regular eye exams and protective eyewear, evidenced by government subsidies for vision screening programs reaching municipalities nationwide. Alignment with these initiatives lets JINS market frames and blue-light lenses as essential health tools, supporting its FY2024 retail growth and helping capture a larger share of an estimated ¥300 billion domestic eyewear market.

Foreign investment and trade agreements

Participation in CPTPP and similar agreements eases JINS Holdings expansion into Southeast Asia, where eyewear market growth is forecast at ~6–8% CAGR to 2028 and Vietnam/Philippines retail sales grew 8.2% and 7.5% in 2024 respectively.

Reduced tariffs and clearer investment rules lower entry costs and legal risk for JINS, supporting targets to lift international revenue share above 25% by 2026.

- Lower tariffs and harmonized standards via CPTPP

- Regional retail growth: Vietnam 8.2% (2024), Philippines 7.5% (2024)

- Target: international revenue >25% by 2026

Changes in retail tax regulations

Potential adjustments to Japan's consumption tax (10% since 2019) or corporate tax revisions could compress JINS Holdings' FY2024 operating margin (3.8% in FY2023) and reduce retail spending—household real consumption rose 1.2% YoY in 2024, but a tax hike could reverse this trend.

Political debate on fiscal tightening affects timing of JINS's store expansion and CAPEX: JINS opened 28 net stores in 2024; uncertainty may delay further openings.

The company must stay agile, adjusting pricing, promotions, and cost structure to legislative shifts impacting the retail sector.

- Consumption tax at 10% since 2019; any hike could cut consumer spend and margins

- FY2023 operating margin 3.8%; sensitive to tax/corporate rate changes

- Opened 28 net stores in 2024—expansion timing tied to fiscal policy clarity

- Requires dynamic pricing and CAPEX flexibility to mitigate legislative risks

Tariff, tax and China risks threaten ¥40bn revenue and thin 3.8% margins

Political risks: US-China tensions and possible 12% tariffs could raise COGS; shipping delays added ~20% lead times in 2023. Tokyo-Beijing frictions risk 15–25% China sales dips; China crucial to ~¥40bn FY2024 revenue. CPTPP lowers entry costs for SEA (Vietnam 8.2%, Philippines 7.5% retail growth in 2024). Consumption tax at 10% and potential hikes threaten margins (FY2023 OM 3.8%); opened 28 net stores in 2024.

| Metric | Value |

|---|---|

| FY2024 revenue (approx.) | ¥40bn |

| FY2023 operating margin | 3.8% |

| China sales drop risk | 15–25% |

| Tariff stress case | ~12% avg |

| SEA retail growth (2024) | VNM 8.2%, PHL 7.5% |

| Net stores opened (2024) | 28 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically shape JINS Holdings’ eyewear manufacturing, retail and DTC channels, combining current data and trends to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for JINS Holdings that eases meeting prep, supports quick alignment across teams, and can be dropped into presentations or strategy packs for clear discussion of external risks and market positioning.

Economic factors

Japanese Yen exchange rate volatility

JINS imports much of its materials and finished goods, so Yen volatility materially affects COGS: a 10% Yen depreciation vs USD in 2023 raised import costs and, per industry estimates, could cut gross margin by ~1.5–2.0 percentage points if retail prices remain unchanged; the Yen strengthened ~6% in 2024 y/y, easing procurement costs and enabling either modest price reductions or margin expansion on JINS’s value eyewear lines.

Rising domestic labor costs

Japan's chronic labor shortage has pushed average hourly wages up 3.3% year-on-year in 2024, increasing costs for retail and manufacturing staff at JINS Holdings. The company must balance high-touch in-store service with rising human capital expenses that pressured operating margins in FY2024. JINS is investing in automation and self-service kiosks—capital expenditures rose 12% in 2024—to preserve service quality while improving labor productivity. These tech investments aim to offset wage inflation and stabilize unit labor costs.

Consumer spending power shifts

Economic stagnation and 2.6% CPI inflation in Japan (2024) pressure middle-class discretionary spending, risking delays in non-essential eyewear purchases despite JINS’s value-based pricing and FY2024 domestic same-store sales growth of 1.8%. Prolonged downturns could reduce unit volumes even as ASP resilience helps protect margins. JINS monitors CPI, household spending (down 0.4% YoY in 2024 Q3) and adjusts marketing spend and promotions to align with consumer sentiment.

Global inflationary pressures

Rising global energy, logistics and raw-material costs—container rates up ~25% in 2024 vs 2022 and global oil prices averaging ~$80/barrel in 2024—increase eyewear production costs, pressuring JINS to absorb margin hits or raise prices against price-sensitive customers.

JINS must deploy strategic sourcing and lean supply-chain measures; in 2024 efficient procurement and supplier diversification helped peers limit COGS inflation to ~3–5 percentage points.

- Container rates +25% (2024 vs 2022)

- Oil ~$80/barrel (2024 average)

- Peers limited COGS inflation to ~3–5 pp via sourcing

Expansion into emerging markets

Expansion into Taiwan and Southeast Asia taps regions with 2024 GDP growth forecasts of 2.5–5.0% (Taiwan ~2.8%, ASEAN average ~4.5%), offering JINS higher growth than Japan’s ~1.0% in 2024; rising middle-class households—projected to add ~140 million people in Asia by 2030—increase demand for fashionable, functional eyewear, supporting revenue diversification beyond mature domestic sales.

- Higher regional GDP growth vs Japan (~4–5% ASEAN vs ~1% Japan in 2024)

- Taiwan GDP ~2.8% (2024 est.)

- Asian middle class to grow by ~140M by 2030

- Opportunity for revenue diversification and price-premium products

JINS margins squeezed by costs; yen strength and ASEAN growth offer partial relief

Yen volatility, rising wages (+3.3% 2024), and higher logistics/oil (container +25% vs 2022; oil ~$80/barrel 2024) pressured COGS and margins, partially offset by Yen strengthening ~6% in 2024 and JINS automation capex +12%; domestic demand weak (CPI 2.6%, household spending -0.4% Q3 2024) while ASEAN/Taiwan growth (ASEAN ~4.5%, Taiwan ~2.8% 2024) offers diversification.

| Metric | 2024 |

|---|---|

| Yen vs USD | +6% strength |

| Wage growth | +3.3% |

| Container rates | +25% vs 2022 |

| Oil | ~$80/barrel |

| Japan GDP | ~1.0% |

| ASEAN avg GDP | ~4.5% |

Preview Before You Purchase

JINS Holdings PESTLE Analysis

The preview shown here is the exact JINS Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or omissions. After checkout you’ll instantly download this same final document, suitable for analysis, presentations, or strategic planning.