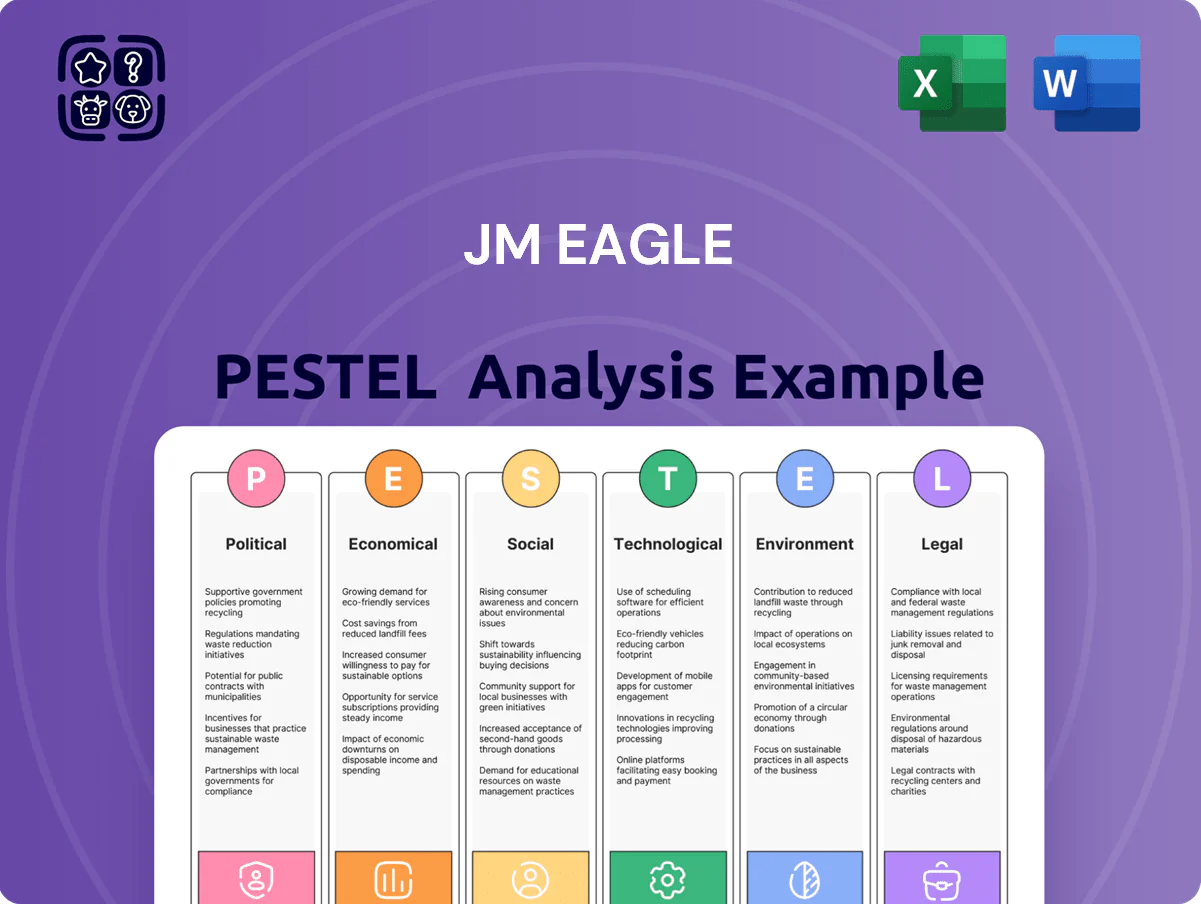

JM Eagle PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of JM Eagle—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full, editable report to access deep-dive risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Infrastructure Investment and Jobs Act Implementation

The Infrastructure Investment and Jobs Act channels roughly $110 billion to water infrastructure through 2021–2026, boosting demand for JM Eagle’s PVC and HDPE pipes as states accelerate lead-pipe replacements; EPA grants and state programs are expected to fund thousands of municipal contracts annually. Analysts should track 2024–2026 state allocations—e.g., California’s $20B-plus water funding vs. smaller Midwest shares—to forecast regional order spikes and capacity needs.

Trade Policies and Tariffs on Raw Materials

As a major consumer of PVC resin and polyethylene, JM Eagle is exposed to trade relations with petrochemical exporters like Saudi Arabia and the US Gulf suppliers; in 2024 the US imported roughly 25% of its ethylene-derived feedstocks, making supply disruptions material to margins.

Tariffs on imported chemical precursors or finished plastic goods can change with Washington’s stance; recent 2023–24 tariff reviews saw duties on select polymer inputs fluctuate between 0–7%, directly affecting input costs.

Rising protectionism—US safeguard measures and Section 301-style actions—could tighten competition: a 5% tariff swing can alter end-product price competitiveness versus Asian and European manufacturers with lower production costs.

Buy American Act Requirements

Buy American Act sourcing rules favor JM Eagle, the largest US PVC pipe maker with estimated 2024 US sales over $1.1 billion, since federal and state public works projects must use domestic suppliers; recent 2023–2025 federal procurement guidance increased domestic-content thresholds, directing an estimated $1.2 trillion in infrastructure spending toward Buy American-compliant firms and reducing competition from lower-cost foreign imports, protecting JM Eagle’s core market share.

Geopolitical Stability and Global Supply Chains

Political instability in energy-producing regions drives volatility in oil and natural gas prices, key feedstocks for polyethylene and PVC; Brent crude averaged about $86/barrel in 2025 with spikes of 20% around regional conflicts, raising feedstock and energy costs for plastics makers.

Regional conflicts in late 2025 disrupted shipping lanes and raised LNG spot prices by roughly 35% year-over-year, forcing JM Eagle to hedge and adjust procurement to protect margins.

JM Eagle must manage geopolitical risk across supply chains—through diversified suppliers, long-term contracts, and energy-efficiency investments—to stabilize manufacturing costs amid an energy-intensive production model.

- Brent ~ $86/bbl (2025 average); 20% conflict-driven spikes

- LNG spot prices up ~35% YoY late 2025

- Mitigation: supplier diversification, long-term contracts, efficiency capex

Federal and State Lobbying Efforts

The US plastic pipe industry spent about $8.3 million on federal and state lobbying in 2023, aiming to influence building codes and material standards that favor PVC and HDPE over ductile iron and concrete.

Political backing for plastics is pivotal: markets with pro-plastic codes show adoption rates 20–35% higher; JM Eagle’s state-level lobbying and partnerships directly affect its ability to win multi-million-dollar utility contracts.

- 2023 industry lobbying spend: $8.3M

- Adoption uplift in pro-plastic jurisdictions: 20–35%

- State-level advocacy linked to success in multi-million utility projects

Infrastructure, Buy American and lobbying drive JM Eagle’s $1.1B U.S. PVC surge

Federal infrastructure funds (~$110B water 2021–26) and Buy American rules (2023–25 domestic-content hikes) boost JM Eagle’s US demand; 2024 US sales ~ $1.1B. Feedstock exposure: US imports ~25% ethylene feedstocks; Brent ~$86/bbl (2025 avg). Industry lobbying $8.3M (2023) raises PVC adoption +20–35% in pro-plastic jurisdictions.

| Metric | Value |

|---|---|

| Water infra funds | $110B (2021–26) |

| JM Eagle US sales | $1.1B (2024 est) |

| Ethylene imports | ~25% |

| Brent | $86/bbl (2025) |

| Lobbying | $8.3M (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect JM Eagle across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable JM Eagle PESTLE summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations or planning sessions, and editable for region- or business-specific notes to align teams and support risk discussions.

Economic factors

Interest Rate Environment and Construction Activity

By late 2025, the Fed funds rate near 5.25%–5.50% continues to curb US housing starts, which fell 4.8% year-over-year in 2024 to 1.21 million units, lowering demand for irrigation and sewage piping.

High borrowing costs have pressured commercial construction permits, down 6% in 2024, reducing JM Eagle’s immediate order pipeline.

A shift toward rate cuts in 2025 would likely spur project restarts; a 1% drop in mortgage rates historically correlates with a 3–4% rise in housing starts, boosting pipe demand.

Volatility in Petrochemical Feedstock Costs

The cost of PVC and HDPE for JM Eagle is tightly tied to oil and natural gas prices—WTI crude rose ~20% in 2024 to average $80/bbl, while Henry Hub gas averaged $3.60/MMBtu—driving feedstock-linked resin price volatility. Rapid energy-sector swings can raise production costs faster than JM Eagle can raise prices, compressing margins; resin spreads moved +/-15% intrayear in 2024. Strategic hedging and long-term supply contracts, plus inventory management, are essential to protect gross margins during commodity-driven inflation.

Labor Market Trends and Manufacturing Automation

Availability of skilled manufacturing labor affects JM Eagle’s efficiency and wage bill; US manufacturing job openings averaged 558,000 in 2024, pushing firms toward higher pay and training costs. Rising state minimum wages (e.g., 2024 weighted average up ~4% YoY) and sectoral labor shortages drove JM Eagle–scale players to boost automation CAPEX; global industrial robot installations rose 9% in 2024, signaling trade-offs between wage inflation and upfront tech investment.

Municipal Budget Health and Tax Revenue

A significant share of JM Eagle’s revenue is tied to public infrastructure contracts; U.S. state and local capital outlays for water and sewer were about $76.6 billion in 2023, and municipalities facing a 2024–25 median property tax revenue decline of 2–4% risk deferring projects.

Economic downturns that cut sales or property tax receipts correlate with higher project delays; approximately 18% of U.S. water utility capital projects were postponed in 2023 due to fiscal constraints.

JM Eagle’s sales and backlog closely track municipal fiscal health, making municipal budget volatility a material operational risk.

- ~$76.6B U.S. water/sewer capital outlays (2023)

- Median municipal property tax declines 2–4% (2024–25 est.)

- ~18% of water projects postponed in 2023

- Revenue sensitivity tied to municipal budgets and project backlog

Global Economic Growth and Export Potential

Global GDP growth slowed to an estimated 3.3% in 2024 (IMF), constraining demand in many emerging markets where JM Eagle seeks expansion; the company’s strong US base faces headwinds as a strong dollar—up ~5% vs. EM currencies in 2024—makes American-made plastic pipes pricier abroad.

Tracking regional GDP forecasts (e.g., 2024–25 growth: South Asia ~5.8%, Sub-Saharan Africa ~3.6%) helps JM Eagle target high-growth markets for distribution and prioritize capex and pricing strategies.

- Watch global GDP (IMF 2024: 3.3%)

- Monitor USD strength (~+5% vs EM in 2024)

- Prioritize South Asia, Sub-Saharan Africa for expansion

Higher US rates, oil swings dent construction and pipe demand; capex strains weigh

Higher US rates (Fed 5.25%–5.50% late-2025) cut 2024 housing starts −4.8% to 1.21M and commercial permits −6%, lowering pipe demand; WTI avg ~$80/bbl and Henry Hub ~$3.60/MMBtu in 2024 raised resin cost volatility (~±15% spreads); US water/sewer capex ~$76.6B (2023) with ~18% projects postponed (2023)—municipal budget stress and strong USD (~+5% vs EM in 2024) constrain international growth.

| Metric | Value (2024/2023) |

|---|---|

| Housing starts | 1.21M (−4.8% YoY) |

| WTI avg | $80/bbl (+20%) |

| Henry Hub | $3.60/MMBtu |

| US water/sewer capex | $76.6B (2023) |

| Projects postponed | ~18% (2023) |

| USD vs EM | ~+5% (2024) |

What You See Is What You Get

JM Eagle PESTLE Analysis

The preview shown here is the exact JM Eagle PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are the final file you can download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of JM Eagle—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full, editable report to access deep-dive risks, opportunities, and actionable recommendations you can use immediately.

Political factors

Infrastructure Investment and Jobs Act Implementation

The Infrastructure Investment and Jobs Act channels roughly $110 billion to water infrastructure through 2021–2026, boosting demand for JM Eagle’s PVC and HDPE pipes as states accelerate lead-pipe replacements; EPA grants and state programs are expected to fund thousands of municipal contracts annually. Analysts should track 2024–2026 state allocations—e.g., California’s $20B-plus water funding vs. smaller Midwest shares—to forecast regional order spikes and capacity needs.

Trade Policies and Tariffs on Raw Materials

As a major consumer of PVC resin and polyethylene, JM Eagle is exposed to trade relations with petrochemical exporters like Saudi Arabia and the US Gulf suppliers; in 2024 the US imported roughly 25% of its ethylene-derived feedstocks, making supply disruptions material to margins.

Tariffs on imported chemical precursors or finished plastic goods can change with Washington’s stance; recent 2023–24 tariff reviews saw duties on select polymer inputs fluctuate between 0–7%, directly affecting input costs.

Rising protectionism—US safeguard measures and Section 301-style actions—could tighten competition: a 5% tariff swing can alter end-product price competitiveness versus Asian and European manufacturers with lower production costs.

Buy American Act Requirements

Buy American Act sourcing rules favor JM Eagle, the largest US PVC pipe maker with estimated 2024 US sales over $1.1 billion, since federal and state public works projects must use domestic suppliers; recent 2023–2025 federal procurement guidance increased domestic-content thresholds, directing an estimated $1.2 trillion in infrastructure spending toward Buy American-compliant firms and reducing competition from lower-cost foreign imports, protecting JM Eagle’s core market share.

Geopolitical Stability and Global Supply Chains

Political instability in energy-producing regions drives volatility in oil and natural gas prices, key feedstocks for polyethylene and PVC; Brent crude averaged about $86/barrel in 2025 with spikes of 20% around regional conflicts, raising feedstock and energy costs for plastics makers.

Regional conflicts in late 2025 disrupted shipping lanes and raised LNG spot prices by roughly 35% year-over-year, forcing JM Eagle to hedge and adjust procurement to protect margins.

JM Eagle must manage geopolitical risk across supply chains—through diversified suppliers, long-term contracts, and energy-efficiency investments—to stabilize manufacturing costs amid an energy-intensive production model.

- Brent ~ $86/bbl (2025 average); 20% conflict-driven spikes

- LNG spot prices up ~35% YoY late 2025

- Mitigation: supplier diversification, long-term contracts, efficiency capex

Federal and State Lobbying Efforts

The US plastic pipe industry spent about $8.3 million on federal and state lobbying in 2023, aiming to influence building codes and material standards that favor PVC and HDPE over ductile iron and concrete.

Political backing for plastics is pivotal: markets with pro-plastic codes show adoption rates 20–35% higher; JM Eagle’s state-level lobbying and partnerships directly affect its ability to win multi-million-dollar utility contracts.

- 2023 industry lobbying spend: $8.3M

- Adoption uplift in pro-plastic jurisdictions: 20–35%

- State-level advocacy linked to success in multi-million utility projects

Infrastructure, Buy American and lobbying drive JM Eagle’s $1.1B U.S. PVC surge

Federal infrastructure funds (~$110B water 2021–26) and Buy American rules (2023–25 domestic-content hikes) boost JM Eagle’s US demand; 2024 US sales ~ $1.1B. Feedstock exposure: US imports ~25% ethylene feedstocks; Brent ~$86/bbl (2025 avg). Industry lobbying $8.3M (2023) raises PVC adoption +20–35% in pro-plastic jurisdictions.

| Metric | Value |

|---|---|

| Water infra funds | $110B (2021–26) |

| JM Eagle US sales | $1.1B (2024 est) |

| Ethylene imports | ~25% |

| Brent | $86/bbl (2025) |

| Lobbying | $8.3M (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect JM Eagle across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

A concise, shareable JM Eagle PESTLE summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations or planning sessions, and editable for region- or business-specific notes to align teams and support risk discussions.

Economic factors

Interest Rate Environment and Construction Activity

By late 2025, the Fed funds rate near 5.25%–5.50% continues to curb US housing starts, which fell 4.8% year-over-year in 2024 to 1.21 million units, lowering demand for irrigation and sewage piping.

High borrowing costs have pressured commercial construction permits, down 6% in 2024, reducing JM Eagle’s immediate order pipeline.

A shift toward rate cuts in 2025 would likely spur project restarts; a 1% drop in mortgage rates historically correlates with a 3–4% rise in housing starts, boosting pipe demand.

Volatility in Petrochemical Feedstock Costs

The cost of PVC and HDPE for JM Eagle is tightly tied to oil and natural gas prices—WTI crude rose ~20% in 2024 to average $80/bbl, while Henry Hub gas averaged $3.60/MMBtu—driving feedstock-linked resin price volatility. Rapid energy-sector swings can raise production costs faster than JM Eagle can raise prices, compressing margins; resin spreads moved +/-15% intrayear in 2024. Strategic hedging and long-term supply contracts, plus inventory management, are essential to protect gross margins during commodity-driven inflation.

Labor Market Trends and Manufacturing Automation

Availability of skilled manufacturing labor affects JM Eagle’s efficiency and wage bill; US manufacturing job openings averaged 558,000 in 2024, pushing firms toward higher pay and training costs. Rising state minimum wages (e.g., 2024 weighted average up ~4% YoY) and sectoral labor shortages drove JM Eagle–scale players to boost automation CAPEX; global industrial robot installations rose 9% in 2024, signaling trade-offs between wage inflation and upfront tech investment.

Municipal Budget Health and Tax Revenue

A significant share of JM Eagle’s revenue is tied to public infrastructure contracts; U.S. state and local capital outlays for water and sewer were about $76.6 billion in 2023, and municipalities facing a 2024–25 median property tax revenue decline of 2–4% risk deferring projects.

Economic downturns that cut sales or property tax receipts correlate with higher project delays; approximately 18% of U.S. water utility capital projects were postponed in 2023 due to fiscal constraints.

JM Eagle’s sales and backlog closely track municipal fiscal health, making municipal budget volatility a material operational risk.

- ~$76.6B U.S. water/sewer capital outlays (2023)

- Median municipal property tax declines 2–4% (2024–25 est.)

- ~18% of water projects postponed in 2023

- Revenue sensitivity tied to municipal budgets and project backlog

Global Economic Growth and Export Potential

Global GDP growth slowed to an estimated 3.3% in 2024 (IMF), constraining demand in many emerging markets where JM Eagle seeks expansion; the company’s strong US base faces headwinds as a strong dollar—up ~5% vs. EM currencies in 2024—makes American-made plastic pipes pricier abroad.

Tracking regional GDP forecasts (e.g., 2024–25 growth: South Asia ~5.8%, Sub-Saharan Africa ~3.6%) helps JM Eagle target high-growth markets for distribution and prioritize capex and pricing strategies.

- Watch global GDP (IMF 2024: 3.3%)

- Monitor USD strength (~+5% vs EM in 2024)

- Prioritize South Asia, Sub-Saharan Africa for expansion

Higher US rates, oil swings dent construction and pipe demand; capex strains weigh

Higher US rates (Fed 5.25%–5.50% late-2025) cut 2024 housing starts −4.8% to 1.21M and commercial permits −6%, lowering pipe demand; WTI avg ~$80/bbl and Henry Hub ~$3.60/MMBtu in 2024 raised resin cost volatility (~±15% spreads); US water/sewer capex ~$76.6B (2023) with ~18% projects postponed (2023)—municipal budget stress and strong USD (~+5% vs EM in 2024) constrain international growth.

| Metric | Value (2024/2023) |

|---|---|

| Housing starts | 1.21M (−4.8% YoY) |

| WTI avg | $80/bbl (+20%) |

| Henry Hub | $3.60/MMBtu |

| US water/sewer capex | $76.6B (2023) |

| Projects postponed | ~18% (2023) |

| USD vs EM | ~+5% (2024) |

What You See Is What You Get

JM Eagle PESTLE Analysis

The preview shown here is the exact JM Eagle PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are the final file you can download immediately after payment.