J. M. Smucker Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

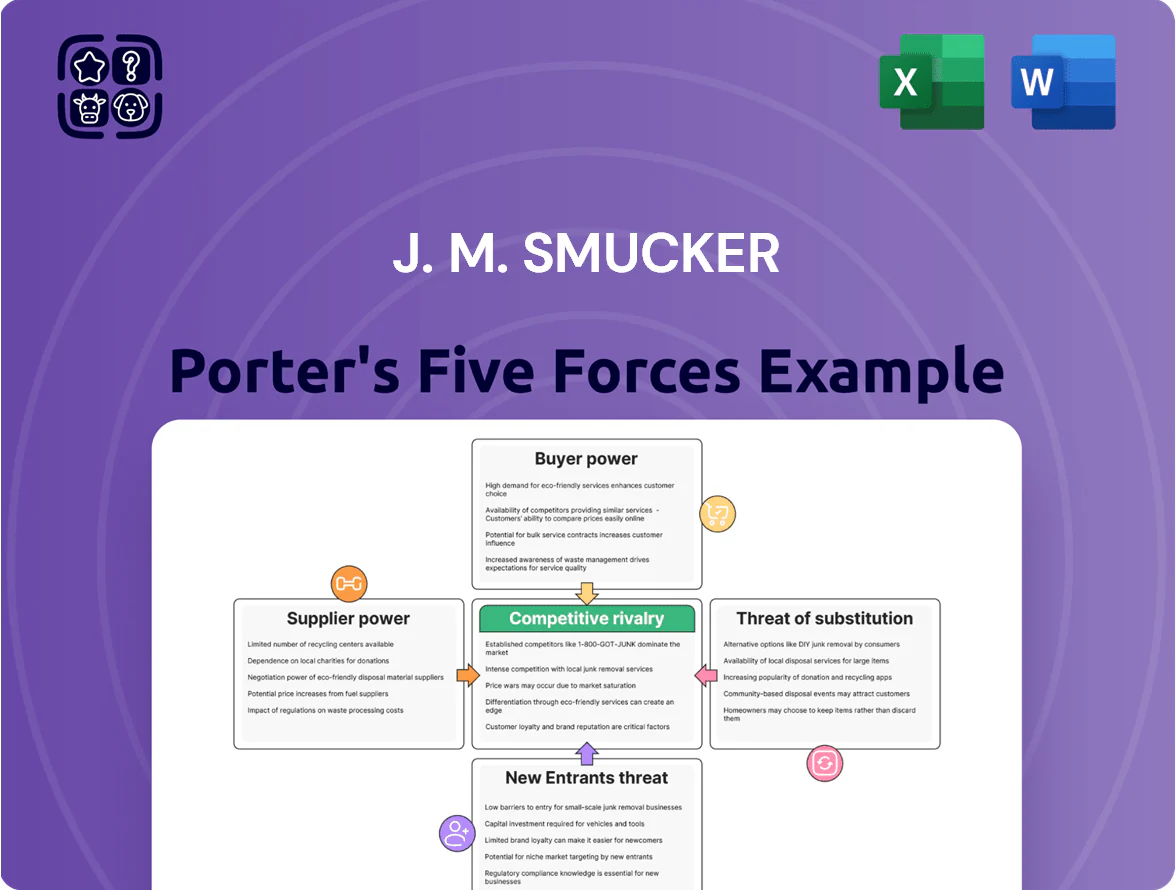

J. M. Smucker faces intense rivalry from national brands and private labels, moderate supplier power for key inputs, and steady buyer leverage from large retailers—while moderate product differentiation and moderate barriers to entry shape its strategic landscape. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore J. M. Smucker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Agricultural Commodity Prices

Smucker depends on commodities like green coffee, peanuts, and grains that saw price swings—Arabica coffee rose ~45% in 2023–24 and global wheat jumped 20% in 2022–23—so weather and supply shocks can compress margins unless hedged.

These undifferentiated inputs give suppliers leverage; Smucker’s 2024 CPG gross margin of 31.8% shows sensitivity to raw-cost moves, and coffee concentration in Brazil and Vietnam strengthens traders’ bargaining power.

Energy and Packaging Material Costs

Suppliers of plastic, glass, and aluminum plus energy providers drive a large share of Smucker’s COGS; resin and aluminum prices rose ~18% and 12% YoY in 2025, pushing packaging spend higher and squeezing margins.

New 2025 sustainability rules raised demand for bio-resins and recycled aluminum, adding roughly $40–60 million in annual packaging costs industry-wide; Smucker faces these added premiums.

Smucker’s negotiating room is limited because global resin and energy prices tied to geopolitics—Brent crude volatility of ±15% in 2025—set input costs beyond firm control.

Labor Market Constraints

Suppliers of logistics, transportation, and specialized manufacturing labor have gained leverage from a 2024 North American industrial labor shortage—industry vacancy rates hit ~6.5% in 2024—pushing Smucker to absorb higher wages and contractor premiums that raised distribution costs by an estimated 2–3% of COGS in 2024.

Supplier Concentration in Pet Food Ingredients

As Smucker shifts toward pet food—which accounted for 37% of 2024 net sales ($4.1B of $11.1B total in fiscal 2024)—it relies on a narrow set of suppliers for specialized proteins and nutrients, concentrating supplier power.

Technical specs for premium nutrition cut viable vendors to a few, letting suppliers push pricing and lead times; a raw‑material disruption could stall production of high‑margin brands like Meow Mix and Milk‑Bone, hurting gross margins.

- Pet food = 37% of Smucker 2024 net sales ($4.1B)

- Specialized proteins limit vendors to a few

- Suppliers can raise prices, extend lead times

- Disruption risks delay for Meow Mix, Milk‑Bone

Impact of ESG Compliance Requirements

Suppliers are passing ESG compliance costs to J. M. Smucker, raising input costs—verified by industry data showing certified coffee premiums rose ~12% in 2024 and RSPO‑certified palm oil premiums averaged $30–$50/ton in 2023–24.

Smucker’s tighter transparency and ethical sourcing reduces qualified suppliers, shrinking supply and letting compliant vendors charge premiums, pressuring gross margins.

- Certified coffee premiums +12% (2024)

- RSPO palm oil premium $30–$50/ton (2023–24)

- Supplier pool contraction → higher bargaining power

Supplier shocks and rising input costs squeeze Smucker margins, pet-food exposure a risk

Smucker faces high supplier power: commodity shocks (Arabica +45% 2023–24; wheat +20% 2022–23), packaging/resin (+18% YoY 2025), and certified-input premiums (+12% coffee 2024; RSPO $30–$50/ton) squeeze margins; pet-food proteins (37% of 2024 sales, $4.1B) concentrate suppliers; logistics labor shortage (6.5% vacancy 2024) raises distribution costs ~2–3% of COGS.

| Metric | Value |

|---|---|

| Pet food share | 37% ($4.1B, 2024) |

| Arabica coffee | +45% (2023–24) |

| Wheat | +20% (2022–23) |

| Resin/aluminum | +18%/+12% (2025) |

| Certified coffee premium | +12% (2024) |

| Logistics vacancy | 6.5% (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored to J. M. Smucker, highlighting substitutes, disruptive threats, and strategic protections for its market position.

Concise Porter's Five Forces summary for J. M. Smucker—quickly spot competitive threats and opportunities to inform strategic moves.

Customers Bargaining Power

Concentration of Major Retail Partners

Growth of Private Label Alternatives

Retailers’ private-label shares in US grocery reached about 17% in 2024, and grocers like Kroger and Walmart are rolling out premium store brands that directly compete with J. M. Smucker Co.’s fruit spreads and coffee lines. These private-label alternatives are typically 10–30% cheaper, pressuring Smucker to cut prices or increase promotional discounts to protect volume. During 2022–2024 inflation spikes, NielsenIQ data showed private-label unit growth outpaced national brands by ~5 percentage points as consumers traded down. That shift raises retailers’ bargaining power, forcing margins compression for Smucker unless it differentiates by innovation or branding.

Shift Toward E-commerce and Direct-to-Consumer

The rise of e-commerce makes J. M. Smucker customers more price-sensitive and less brand-loyal; 2024 data show online grocery penetration at ~16% in the US, letting shoppers compare prices instantly and switch options. Smucker sells on Amazon and Walmart.com, but these platforms control search placement and own buyer data, reducing Smucker’s margin power. A single-click switch is real: 63% of online shoppers in 2024 said they'd switch brands for lower price or faster delivery.

Consolidation in the Foodservice Channel

Consolidation among large restaurant chains and institutional food providers has created buying groups controlling an estimated 35–45% of US foodservice purchases in 2024, giving them scale and negotiation expertise that pressure J. M. Smucker’s away-from-home margins.

These customers demand custom formulations and volume discounts—contracts often cutting list prices by 10–20%—and can shift to regional or niche suppliers, eroding Smucker’s leverage in the foodservice channel.

- Buying groups: 35–45% of US foodservice spend (2024)

- Typical demanded discounts: 10–20%

- Switching risk: regional/niche suppliers growing share

Consumer Demand for Transparency and Health

Consumers push Smucker to reformulate toward low-sugar, organic, and non-GMO products; NielsenIQ reported 2024 US organic food sales rose 8.5% to $62.6B, showing clear demand.

This gives end-users leverage over Smucker’s product cycles and marketing; in 2023 Smucker lost shelf space to niche brands growing 12–20% yearly in better-for-you segments.

Failing to adapt risks swift share loss to agile health-focused competitors, and 2024 EBITDA pressure from reformulation costs tightened margins by ~0.5–1.0 percentage points.

- Organic sales +8.5% (2024), $62.6B

- Niche healthier brands growth 12–20% (2023)

- Reformulation tightened EBITDA ~0.5–1.0 pp

Retailer pressure squeezes Smucker’s margins: slotting, private label & foodservice cuts

Large retailers drive ~45% of Smucker’s FY2024 revenue, extract discounts/slotting (Smucker reported $120M in trade/slotting costs FY2024), and face of private-label growth (~17% share in 2024) and online grocery (~16% penetration in 2024) that increase price pressure; foodservice buying groups control ~35–45% of spend, demanding 10–20% discounts and squeezing margins (reformulation tightened EBITDA ~0.5–1.0 pp).

| Metric | 2024 / Source |

|---|---|

| Revenue from large retailers | ~45% (FY2024) |

| Trade/slotting costs | $120M (FY2024) |

| Private-label grocery share | ~17% (2024) |

| Online grocery penetration | ~16% (2024) |

| Foodservice buying group spend | 35–45% (2024) |

| Typical foodservice discounts | 10–20% |

| Reformulation EBITDA hit | ~0.5–1.0 pp (2024) |

Full Version Awaits

J. M. Smucker Porter's Five Forces Analysis

This preview shows the exact J. M. Smucker Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights tailored to Smucker's market position. The document is fully formatted and ready for download the moment you buy. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

J. M. Smucker faces intense rivalry from national brands and private labels, moderate supplier power for key inputs, and steady buyer leverage from large retailers—while moderate product differentiation and moderate barriers to entry shape its strategic landscape. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore J. M. Smucker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Agricultural Commodity Prices

Smucker depends on commodities like green coffee, peanuts, and grains that saw price swings—Arabica coffee rose ~45% in 2023–24 and global wheat jumped 20% in 2022–23—so weather and supply shocks can compress margins unless hedged.

These undifferentiated inputs give suppliers leverage; Smucker’s 2024 CPG gross margin of 31.8% shows sensitivity to raw-cost moves, and coffee concentration in Brazil and Vietnam strengthens traders’ bargaining power.

Energy and Packaging Material Costs

Suppliers of plastic, glass, and aluminum plus energy providers drive a large share of Smucker’s COGS; resin and aluminum prices rose ~18% and 12% YoY in 2025, pushing packaging spend higher and squeezing margins.

New 2025 sustainability rules raised demand for bio-resins and recycled aluminum, adding roughly $40–60 million in annual packaging costs industry-wide; Smucker faces these added premiums.

Smucker’s negotiating room is limited because global resin and energy prices tied to geopolitics—Brent crude volatility of ±15% in 2025—set input costs beyond firm control.

Labor Market Constraints

Suppliers of logistics, transportation, and specialized manufacturing labor have gained leverage from a 2024 North American industrial labor shortage—industry vacancy rates hit ~6.5% in 2024—pushing Smucker to absorb higher wages and contractor premiums that raised distribution costs by an estimated 2–3% of COGS in 2024.

Supplier Concentration in Pet Food Ingredients

As Smucker shifts toward pet food—which accounted for 37% of 2024 net sales ($4.1B of $11.1B total in fiscal 2024)—it relies on a narrow set of suppliers for specialized proteins and nutrients, concentrating supplier power.

Technical specs for premium nutrition cut viable vendors to a few, letting suppliers push pricing and lead times; a raw‑material disruption could stall production of high‑margin brands like Meow Mix and Milk‑Bone, hurting gross margins.

- Pet food = 37% of Smucker 2024 net sales ($4.1B)

- Specialized proteins limit vendors to a few

- Suppliers can raise prices, extend lead times

- Disruption risks delay for Meow Mix, Milk‑Bone

Impact of ESG Compliance Requirements

Suppliers are passing ESG compliance costs to J. M. Smucker, raising input costs—verified by industry data showing certified coffee premiums rose ~12% in 2024 and RSPO‑certified palm oil premiums averaged $30–$50/ton in 2023–24.

Smucker’s tighter transparency and ethical sourcing reduces qualified suppliers, shrinking supply and letting compliant vendors charge premiums, pressuring gross margins.

- Certified coffee premiums +12% (2024)

- RSPO palm oil premium $30–$50/ton (2023–24)

- Supplier pool contraction → higher bargaining power

Supplier shocks and rising input costs squeeze Smucker margins, pet-food exposure a risk

Smucker faces high supplier power: commodity shocks (Arabica +45% 2023–24; wheat +20% 2022–23), packaging/resin (+18% YoY 2025), and certified-input premiums (+12% coffee 2024; RSPO $30–$50/ton) squeeze margins; pet-food proteins (37% of 2024 sales, $4.1B) concentrate suppliers; logistics labor shortage (6.5% vacancy 2024) raises distribution costs ~2–3% of COGS.

| Metric | Value |

|---|---|

| Pet food share | 37% ($4.1B, 2024) |

| Arabica coffee | +45% (2023–24) |

| Wheat | +20% (2022–23) |

| Resin/aluminum | +18%/+12% (2025) |

| Certified coffee premium | +12% (2024) |

| Logistics vacancy | 6.5% (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored to J. M. Smucker, highlighting substitutes, disruptive threats, and strategic protections for its market position.

Concise Porter's Five Forces summary for J. M. Smucker—quickly spot competitive threats and opportunities to inform strategic moves.

Customers Bargaining Power

Concentration of Major Retail Partners

Growth of Private Label Alternatives

Retailers’ private-label shares in US grocery reached about 17% in 2024, and grocers like Kroger and Walmart are rolling out premium store brands that directly compete with J. M. Smucker Co.’s fruit spreads and coffee lines. These private-label alternatives are typically 10–30% cheaper, pressuring Smucker to cut prices or increase promotional discounts to protect volume. During 2022–2024 inflation spikes, NielsenIQ data showed private-label unit growth outpaced national brands by ~5 percentage points as consumers traded down. That shift raises retailers’ bargaining power, forcing margins compression for Smucker unless it differentiates by innovation or branding.

Shift Toward E-commerce and Direct-to-Consumer

The rise of e-commerce makes J. M. Smucker customers more price-sensitive and less brand-loyal; 2024 data show online grocery penetration at ~16% in the US, letting shoppers compare prices instantly and switch options. Smucker sells on Amazon and Walmart.com, but these platforms control search placement and own buyer data, reducing Smucker’s margin power. A single-click switch is real: 63% of online shoppers in 2024 said they'd switch brands for lower price or faster delivery.

Consolidation in the Foodservice Channel

Consolidation among large restaurant chains and institutional food providers has created buying groups controlling an estimated 35–45% of US foodservice purchases in 2024, giving them scale and negotiation expertise that pressure J. M. Smucker’s away-from-home margins.

These customers demand custom formulations and volume discounts—contracts often cutting list prices by 10–20%—and can shift to regional or niche suppliers, eroding Smucker’s leverage in the foodservice channel.

- Buying groups: 35–45% of US foodservice spend (2024)

- Typical demanded discounts: 10–20%

- Switching risk: regional/niche suppliers growing share

Consumer Demand for Transparency and Health

Consumers push Smucker to reformulate toward low-sugar, organic, and non-GMO products; NielsenIQ reported 2024 US organic food sales rose 8.5% to $62.6B, showing clear demand.

This gives end-users leverage over Smucker’s product cycles and marketing; in 2023 Smucker lost shelf space to niche brands growing 12–20% yearly in better-for-you segments.

Failing to adapt risks swift share loss to agile health-focused competitors, and 2024 EBITDA pressure from reformulation costs tightened margins by ~0.5–1.0 percentage points.

- Organic sales +8.5% (2024), $62.6B

- Niche healthier brands growth 12–20% (2023)

- Reformulation tightened EBITDA ~0.5–1.0 pp

Retailer pressure squeezes Smucker’s margins: slotting, private label & foodservice cuts

Large retailers drive ~45% of Smucker’s FY2024 revenue, extract discounts/slotting (Smucker reported $120M in trade/slotting costs FY2024), and face of private-label growth (~17% share in 2024) and online grocery (~16% penetration in 2024) that increase price pressure; foodservice buying groups control ~35–45% of spend, demanding 10–20% discounts and squeezing margins (reformulation tightened EBITDA ~0.5–1.0 pp).

| Metric | 2024 / Source |

|---|---|

| Revenue from large retailers | ~45% (FY2024) |

| Trade/slotting costs | $120M (FY2024) |

| Private-label grocery share | ~17% (2024) |

| Online grocery penetration | ~16% (2024) |

| Foodservice buying group spend | 35–45% (2024) |

| Typical foodservice discounts | 10–20% |

| Reformulation EBITDA hit | ~0.5–1.0 pp (2024) |

Full Version Awaits

J. M. Smucker Porter's Five Forces Analysis

This preview shows the exact J. M. Smucker Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights tailored to Smucker's market position. The document is fully formatted and ready for download the moment you buy. You're viewing the final deliverable.