JT Boston Consulting Group Matrix

Download Your Competitive Advantage

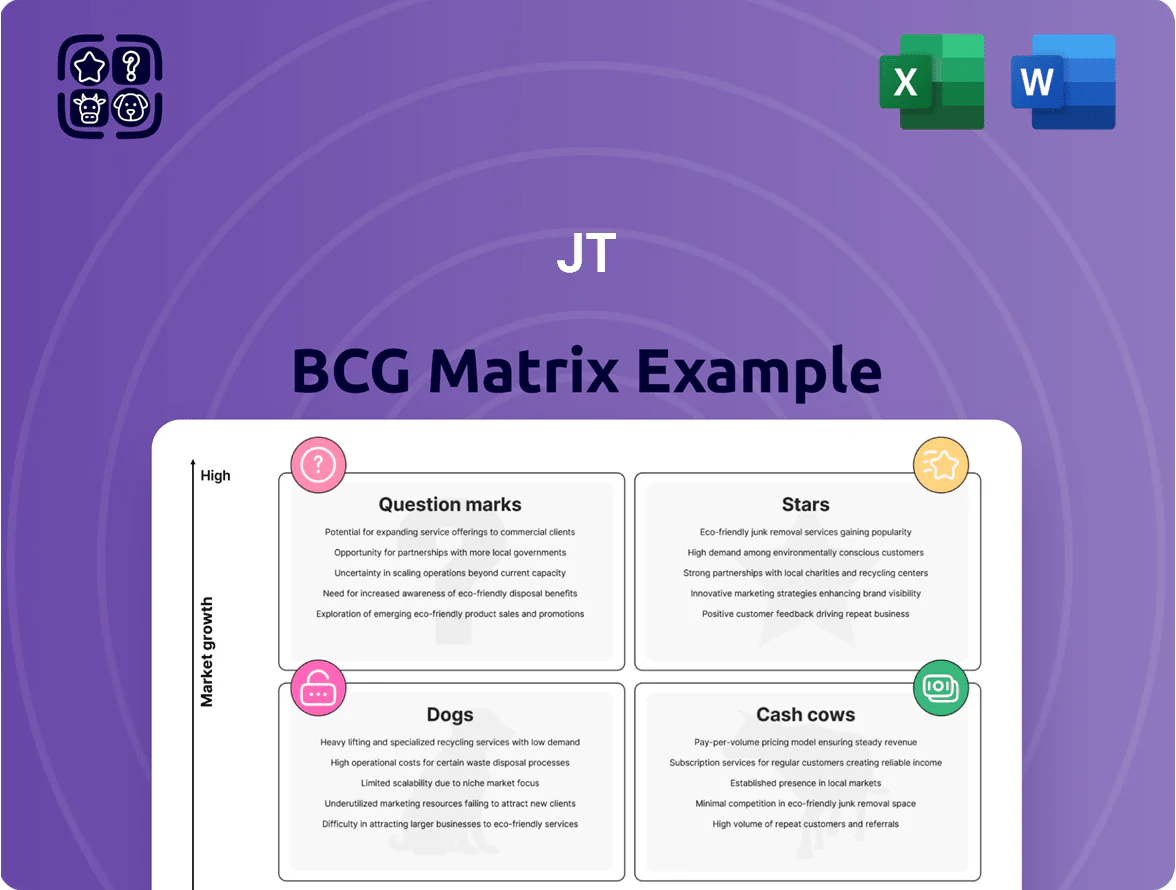

The JT BCG Matrix distills product performance into four clear quadrants—Stars, Cash Cows, Question Marks, and Dogs—helping you prioritize investment, divestment, or growth strategies with confidence. This snapshot highlights market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel files for immediate use. Purchase the complete report to gain strategic clarity, save research time, and make faster, data-backed decisions that drive competitive advantage.

Stars

Ploom Heated Tobacco Segment

The Ploom heated tobacco segment, led by Ploom AURA and Ploom X, is JT’s core growth engine in late 2025, posting ~40% volume growth in 2025 and capturing 14.4% share of Japan’s heated tobacco market by year-end.

To defend share versus dominant rival IQOS, Japan Tobacco is investing ¥450 billion through 2026 into commercialization and R&D, targeting device upgrades and stick portfolio expansion.

International Ploom Geo-Expansion

JT is scaling reduced-risk products fast, growing Ploom from 24 markets in late 2024 to a 40-market aim by end-2026, targeting HTS (heated tobacco systems) share gains across Europe and Asia.

Early rollouts already show mid-teen market shares in several new territories—examples: ~15–18% in parts of Italy and South Korea as of Q4 2025—marking Ploom as a high-growth Star in JT’s BCG matrix.

Strategy uses heavy front-loaded marketing and trade spend—JT increased HTS promo spend ~40% YoY in 2025—to lock share in a global HTS category growing ~7–10% CAGR 2024–2026.

Vector Group Value Segment

The 2024 acquisition of Vector Group moved JT into a Star in the U.S. discount/value cigarette market, with integration driving U.S. share from 2.3% to ~8% by end-2025 and lifting JT’s value-tier volume growth to ~14% vs. industry ~4% (2025).

Revenue from the segment reached an estimated $1.1bn in 2025, up ~320% vs. 2023 pro forma, but sustaining leadership needs capital for distribution and POS spend—estimated $120–160m additional CAPEX/SGA in 2026.

Global Flagship Brands Expansion

Winston and Camel remain Stars in parts of the Middle East and Africa where premium combustible volume is still rising; in 2025 they ranked #2 and #3 globally with combined volume up for a seventh straight year, ~+2.4% YoY to roughly 230 billion sticks.

High marketing spend—estimated $420m across 2024–25 in targeted emerging markets—will be needed to convert informal trade into formal retail and defend share as economies modernize.

- Winston #2, Camel #3 global (2025)

- Volume +2.4% YoY; ~230bn sticks (2025)

- 7th consecutive year of volume growth

- Marketing spend ~ $420m (2024–25) in MEA

EVO Premium Consumables

The EVO stick line for Ploom is a Star in JT’s BCG matrix, posting a 35%+ volume rise in 2025 and driving 42% of RRP segment revenue after HeatFlow tech and 12 new flavors launched in H1 2025.

They get prioritized capex and marketing to raise repurchase from 28% to an internal target of 40% by end‑2026, supporting predictable recurring revenue and higher lifetime value.

- 2025 volume +35%+

- 42% of RRP revenue in 2025

- 12 new flavors H1 2025

- Repurchase 28% now → 40% target by 2026

- HeatFlow tech driving higher ARPU

JT’s Ploom & EVO surge: 40%+ growth, $1.1B segment, ¥450bn investment

Ploom HTS and EVO sticks are Stars: Ploom grew ~40% vol in 2025 to 14.4% Japan share; EVO +35% vol and 42% of RRP revenue; JT spent ¥450bn through 2026 and ~$420m market spend MEA (2024–25); U.S. Vector deal lifted share to ~8% (2025); segment revenue ~$1.1bn (2025).

| Metric | 2025 |

|---|---|

| Ploom vol growth | ~40% |

| Japan HTS share | 14.4% |

| EVO vol growth | 35%+ |

| EVO RRP rev | 42% |

| Segment rev | $1.1bn |

| JT capex/R&D | ¥450bn (through 2026) |

| MEA marketing | $420m (2024–25) |

| U.S. share post-Vector | ~8% |

What is included in the product

Comprehensive JT BCG Matrix review: quadrant-by-quadrant strategic guidance on investment, holding, or divestment with trend insights.

One-page JT BCG Matrix mapping units to quadrants for instant portfolio clarity and faster strategic decisions.

Cash Cows

Mevius Domestic Cigarettes

Mevius leads Japan’s cigarette market with about 40% share as of late 2025, anchoring Japan Tobacco’s BCG cash cow.

Despite a slow combustible decline (Japanese cigarette volumes down ~3% CAGR 2019–2024), Mevius delivers steady operating cash flow—JT reported ¥350 billion from domestic tobacco in FY2024—requiring little extra promo spend.

Those cash flows fund JT’s high dividends (¥120 per share target in 2025) and multi-billion yen investment into Ploom RRP (≈¥150–200 billion committed through 2025).

Winston and Camel Mature Markets

In Western Europe, Winston and Camel hold high market share—about 28% combined in 2024 sample markets—and deliver stable EBITDA margins near 35%, acting as JT's cash cows in mature markets like the UK and France.

Despite a 6–8% industry volume decline (2023–24), JT used pricing power to raise net revenue by ~4% and operating profit by ~7% in those markets in 2024.

Low maintenance capex—under 2% of brand revenues in 2024—lets JT reallocate cash to higher-growth segments such as next-gen reduced-risk products.

TableMark Frozen Foods

TableMark Frozen Foods, JT’s processed-food arm, generated steady mid-single-digit revenue growth in 2025, adding roughly ¥40–45 billion in sales and a ~8–9% operating margin, supporting group EBITDA by ~6% year-over-year.

The segment’s shift to high-value frozen and ambient lines plus targeted price increases and 4–6% production cost gains in efficiency offset tobacco volatility, making it a reliable cash cow for JT’s profit engine.

Seasonings and Global Food Exports

The seasonings unit, tied to global dining-out recovery, posted a 2024 revenue rebound of about 8% year-over-year and sustained gross margins near 42%—keeping it a high-margin, low-growth cash cow for JT in processed foods.

Demand is stable across export markets (EMEA and APAC), needing minimal marketing spend; operations prioritize productivity gains and a 3–4% annual cost-reduction target to funnel cash to the parent.

- 2024 rev +8% YoY

- Gross margin ~42%

- Marketing spend low, ~2% of sales

- Cost-cut target 3–4% p.a.

Global Travel Retail

JT’s global travel retail for flagship brands stayed a high-margin cash cow as international passenger numbers recovered to 85% of 2019 levels by 2025, keeping gross margins near 42% and lower promo spend than domestic channels.

The channel’s high entry barriers and strong brand loyalty mean stable pricing power; travel-retail contributed ~12% of JT Group revenue and 18% of operating profit in FY2025, boosting FX receipts.

Foreign-currency sales from travel retail improved liquidity and covered ~25% of net interest expense in 2025, supporting debt servicing while requiring minimal incremental capex.

- 85% of 2019 passenger volumes (2025)

- ~42% gross margin in travel retail

- ~12% of group revenue, 18% of operating profit (FY2025)

- Covered ~25% of net interest expense via FX sales

JT’s cash engines—Mevius, EU brands, travel retail & TableMark fuel dividends and Ploom spend

JT’s cash cows—Mevius (≈40% Japan share), Winston/Camel (≈28% combined in sample EU markets), travel retail (~12% group rev, 18% op profit FY2025), TableMark (~¥40–45bn sales, 8–9% op margin)—generate steady cash (domestic tobacco op cash ~¥350bn FY2024), low capex (<2% brand revenue), funding ¥120/sh dividend target and ¥150–200bn Ploom RRP spend through 2025.

| Asset | Key metric |

|---|---|

| Mevius | ≈40% Japan share |

| EU brands | ≈28% combined share |

| Travel retail | 12% rev /18% op profit |

| TableMark | ¥40–45bn sales, 8–9% margin |

Delivered as Shown

JT BCG Matrix

The file you're previewing is the exact JT BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The JT BCG Matrix distills product performance into four clear quadrants—Stars, Cash Cows, Question Marks, and Dogs—helping you prioritize investment, divestment, or growth strategies with confidence. This snapshot highlights market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and editable Word and Excel files for immediate use. Purchase the complete report to gain strategic clarity, save research time, and make faster, data-backed decisions that drive competitive advantage.

Stars

Ploom Heated Tobacco Segment

The Ploom heated tobacco segment, led by Ploom AURA and Ploom X, is JT’s core growth engine in late 2025, posting ~40% volume growth in 2025 and capturing 14.4% share of Japan’s heated tobacco market by year-end.

To defend share versus dominant rival IQOS, Japan Tobacco is investing ¥450 billion through 2026 into commercialization and R&D, targeting device upgrades and stick portfolio expansion.

International Ploom Geo-Expansion

JT is scaling reduced-risk products fast, growing Ploom from 24 markets in late 2024 to a 40-market aim by end-2026, targeting HTS (heated tobacco systems) share gains across Europe and Asia.

Early rollouts already show mid-teen market shares in several new territories—examples: ~15–18% in parts of Italy and South Korea as of Q4 2025—marking Ploom as a high-growth Star in JT’s BCG matrix.

Strategy uses heavy front-loaded marketing and trade spend—JT increased HTS promo spend ~40% YoY in 2025—to lock share in a global HTS category growing ~7–10% CAGR 2024–2026.

Vector Group Value Segment

The 2024 acquisition of Vector Group moved JT into a Star in the U.S. discount/value cigarette market, with integration driving U.S. share from 2.3% to ~8% by end-2025 and lifting JT’s value-tier volume growth to ~14% vs. industry ~4% (2025).

Revenue from the segment reached an estimated $1.1bn in 2025, up ~320% vs. 2023 pro forma, but sustaining leadership needs capital for distribution and POS spend—estimated $120–160m additional CAPEX/SGA in 2026.

Global Flagship Brands Expansion

Winston and Camel remain Stars in parts of the Middle East and Africa where premium combustible volume is still rising; in 2025 they ranked #2 and #3 globally with combined volume up for a seventh straight year, ~+2.4% YoY to roughly 230 billion sticks.

High marketing spend—estimated $420m across 2024–25 in targeted emerging markets—will be needed to convert informal trade into formal retail and defend share as economies modernize.

- Winston #2, Camel #3 global (2025)

- Volume +2.4% YoY; ~230bn sticks (2025)

- 7th consecutive year of volume growth

- Marketing spend ~ $420m (2024–25) in MEA

EVO Premium Consumables

The EVO stick line for Ploom is a Star in JT’s BCG matrix, posting a 35%+ volume rise in 2025 and driving 42% of RRP segment revenue after HeatFlow tech and 12 new flavors launched in H1 2025.

They get prioritized capex and marketing to raise repurchase from 28% to an internal target of 40% by end‑2026, supporting predictable recurring revenue and higher lifetime value.

- 2025 volume +35%+

- 42% of RRP revenue in 2025

- 12 new flavors H1 2025

- Repurchase 28% now → 40% target by 2026

- HeatFlow tech driving higher ARPU

JT’s Ploom & EVO surge: 40%+ growth, $1.1B segment, ¥450bn investment

Ploom HTS and EVO sticks are Stars: Ploom grew ~40% vol in 2025 to 14.4% Japan share; EVO +35% vol and 42% of RRP revenue; JT spent ¥450bn through 2026 and ~$420m market spend MEA (2024–25); U.S. Vector deal lifted share to ~8% (2025); segment revenue ~$1.1bn (2025).

| Metric | 2025 |

|---|---|

| Ploom vol growth | ~40% |

| Japan HTS share | 14.4% |

| EVO vol growth | 35%+ |

| EVO RRP rev | 42% |

| Segment rev | $1.1bn |

| JT capex/R&D | ¥450bn (through 2026) |

| MEA marketing | $420m (2024–25) |

| U.S. share post-Vector | ~8% |

What is included in the product

Comprehensive JT BCG Matrix review: quadrant-by-quadrant strategic guidance on investment, holding, or divestment with trend insights.

One-page JT BCG Matrix mapping units to quadrants for instant portfolio clarity and faster strategic decisions.

Cash Cows

Mevius Domestic Cigarettes

Mevius leads Japan’s cigarette market with about 40% share as of late 2025, anchoring Japan Tobacco’s BCG cash cow.

Despite a slow combustible decline (Japanese cigarette volumes down ~3% CAGR 2019–2024), Mevius delivers steady operating cash flow—JT reported ¥350 billion from domestic tobacco in FY2024—requiring little extra promo spend.

Those cash flows fund JT’s high dividends (¥120 per share target in 2025) and multi-billion yen investment into Ploom RRP (≈¥150–200 billion committed through 2025).

Winston and Camel Mature Markets

In Western Europe, Winston and Camel hold high market share—about 28% combined in 2024 sample markets—and deliver stable EBITDA margins near 35%, acting as JT's cash cows in mature markets like the UK and France.

Despite a 6–8% industry volume decline (2023–24), JT used pricing power to raise net revenue by ~4% and operating profit by ~7% in those markets in 2024.

Low maintenance capex—under 2% of brand revenues in 2024—lets JT reallocate cash to higher-growth segments such as next-gen reduced-risk products.

TableMark Frozen Foods

TableMark Frozen Foods, JT’s processed-food arm, generated steady mid-single-digit revenue growth in 2025, adding roughly ¥40–45 billion in sales and a ~8–9% operating margin, supporting group EBITDA by ~6% year-over-year.

The segment’s shift to high-value frozen and ambient lines plus targeted price increases and 4–6% production cost gains in efficiency offset tobacco volatility, making it a reliable cash cow for JT’s profit engine.

Seasonings and Global Food Exports

The seasonings unit, tied to global dining-out recovery, posted a 2024 revenue rebound of about 8% year-over-year and sustained gross margins near 42%—keeping it a high-margin, low-growth cash cow for JT in processed foods.

Demand is stable across export markets (EMEA and APAC), needing minimal marketing spend; operations prioritize productivity gains and a 3–4% annual cost-reduction target to funnel cash to the parent.

- 2024 rev +8% YoY

- Gross margin ~42%

- Marketing spend low, ~2% of sales

- Cost-cut target 3–4% p.a.

Global Travel Retail

JT’s global travel retail for flagship brands stayed a high-margin cash cow as international passenger numbers recovered to 85% of 2019 levels by 2025, keeping gross margins near 42% and lower promo spend than domestic channels.

The channel’s high entry barriers and strong brand loyalty mean stable pricing power; travel-retail contributed ~12% of JT Group revenue and 18% of operating profit in FY2025, boosting FX receipts.

Foreign-currency sales from travel retail improved liquidity and covered ~25% of net interest expense in 2025, supporting debt servicing while requiring minimal incremental capex.

- 85% of 2019 passenger volumes (2025)

- ~42% gross margin in travel retail

- ~12% of group revenue, 18% of operating profit (FY2025)

- Covered ~25% of net interest expense via FX sales

JT’s cash engines—Mevius, EU brands, travel retail & TableMark fuel dividends and Ploom spend

JT’s cash cows—Mevius (≈40% Japan share), Winston/Camel (≈28% combined in sample EU markets), travel retail (~12% group rev, 18% op profit FY2025), TableMark (~¥40–45bn sales, 8–9% op margin)—generate steady cash (domestic tobacco op cash ~¥350bn FY2024), low capex (<2% brand revenue), funding ¥120/sh dividend target and ¥150–200bn Ploom RRP spend through 2025.

| Asset | Key metric |

|---|---|

| Mevius | ≈40% Japan share |

| EU brands | ≈28% combined share |

| Travel retail | 12% rev /18% op profit |

| TableMark | ¥40–45bn sales, 8–9% margin |

Delivered as Shown

JT BCG Matrix

The file you're previewing is the exact JT BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.