JTC PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a competitive edge with our expert PESTLE Analysis of JTC—uncover how political shifts, economic trends, and regulatory changes will shape the company’s future and your strategy; download the full report for actionable, boardroom-ready insights and instant, editable files.

Political factors

Geopolitical instability and sanctions

Ongoing tensions in Eastern Europe and the Middle East require JTC to rigorously monitor international sanction lists—UN, OFAC and EU—after global sanctions rose 22% in 2024, protecting reputation and avoiding multi‑million‑dollar fines (average AML fine >$50m in 2023–24).

As a global provider, JTC must navigate shifting alliances that altered cross‑border capital flows, with UK–US asset transfers up 6% in 2024 while flows to some emerging markets fell 12%.

Political instability can trigger sudden regulatory changes; JTC needs agile compliance frameworks and real‑time screening to ensure client assets remain protected and legally compliant across all jurisdictions.

Global tax transparency initiatives

The OECD/G20 BEPS 2.0 Pillar Two, effective 2024 with 15% global minimum tax adoption by 140+ jurisdictions, increases reporting complexity for JTC’s private and institutional clients and could raise compliance costs by an estimated 5–8% of fee revenue in affected mandates.

Political pressure to curb tax havens compels JTC to validate economic substance across its structures; non-compliance risk has risen as automatic exchange data expanded to 100+ countries under CRS, increasing due-diligence workloads.

Maintaining active engagement with regulators and political bodies—notably in the UK, EU, Cayman Islands and Guernsey, where JTC operates—helps anticipate policy shifts that may alter jurisdiction attractiveness and client structuring decisions.

Regulatory shifts in the United States

The US political environment is pivotal as JTC expands in the American mid-market, where 2024 SEC proposals and state-level regulatory changes have raised private fund reporting scrutiny—SEC’s Form PF and proposed rules could increase compliance costs by an estimated 10–15% for administrators; shifts in Congress or state leadership may accelerate oversight or introduce divergent requirements across key states like California and New York; proactive engagement and scalable compliance platforms are essential to capture rising outsourced administration demand from ~7,000 US private funds.

Trade agreements and market access

Post-Brexit, UK bilateral deals—170+ agreements updated by 2025—shift JTC resource allocation toward UK, EU, UAE, and Singapore hubs as firms seek regulatory certainty and market access.

Political rulings on equivalence and market access, including EU-UK financial services talks and ongoing UK-US regulatory alignment efforts, directly affect JTC’s cross-border capital flows and service licensing costs.

JTC must monitor trade policy shifts and tariff/non-tariff measures that could raise compliance costs or disrupt the firm’s cross-border delivery, where a 1–3% rise in administrative costs could erode margins.

- 170+ UK trade updates by 2025; focus on UK, EU, UAE, Singapore

- Equivalence decisions drive licensing and capital mobility

- Policy shifts can raise compliance costs 1–3%

Stability of offshore financial centers

The political stability of Jersey, Guernsey and the Cayman Islands underpins JTC’s trust, fiduciary and fund administration services; Jersey reported zero government changes since 2018 and Cayman maintains a Moody’s Aa2 local rating as of 2025, which supports client confidence.

Any major policy shifts or unrest could trigger asset relocations and client withdrawals; JTC monitors developments and reported in 2024 that 85% of its offshore revenue was tied to these jurisdictions, guiding its jurisdictional strategy.

- Jersey/Guernsey/Cayman: high political stability, Moody’s Aa2 (Cayman) 2025

- 85% of JTC offshore revenue linked to these centers (2024)

- Active monitoring of local politics to mitigate client flight risk

Political risks surge JTC compliance costs 5–15% as 85% revenue ties to Jersey/Guernsey/Cayman

Political risks (sanctions, tax reform, regulatory shifts) raised JTC compliance costs ~5–15% in 2024–25; 85% offshore revenue tied to Jersey/Guernsey/Cayman; BEPS Pillar Two (15%) adopted by 140+ jurisdictions; UK–US flows +6% (2024), EM flows -12% (2024); ~7,000 US private funds drive SEC scrutiny.

| Metric | Value |

|---|---|

| Offshore revenue exposure (2024) | 85% |

| BEPS Pillar Two adoption | 140+ jurisdictions |

| Compliance cost impact | 5–15% |

| UK–US flows (2024) | +6% |

| EM flows (2024) | -12% |

What is included in the product

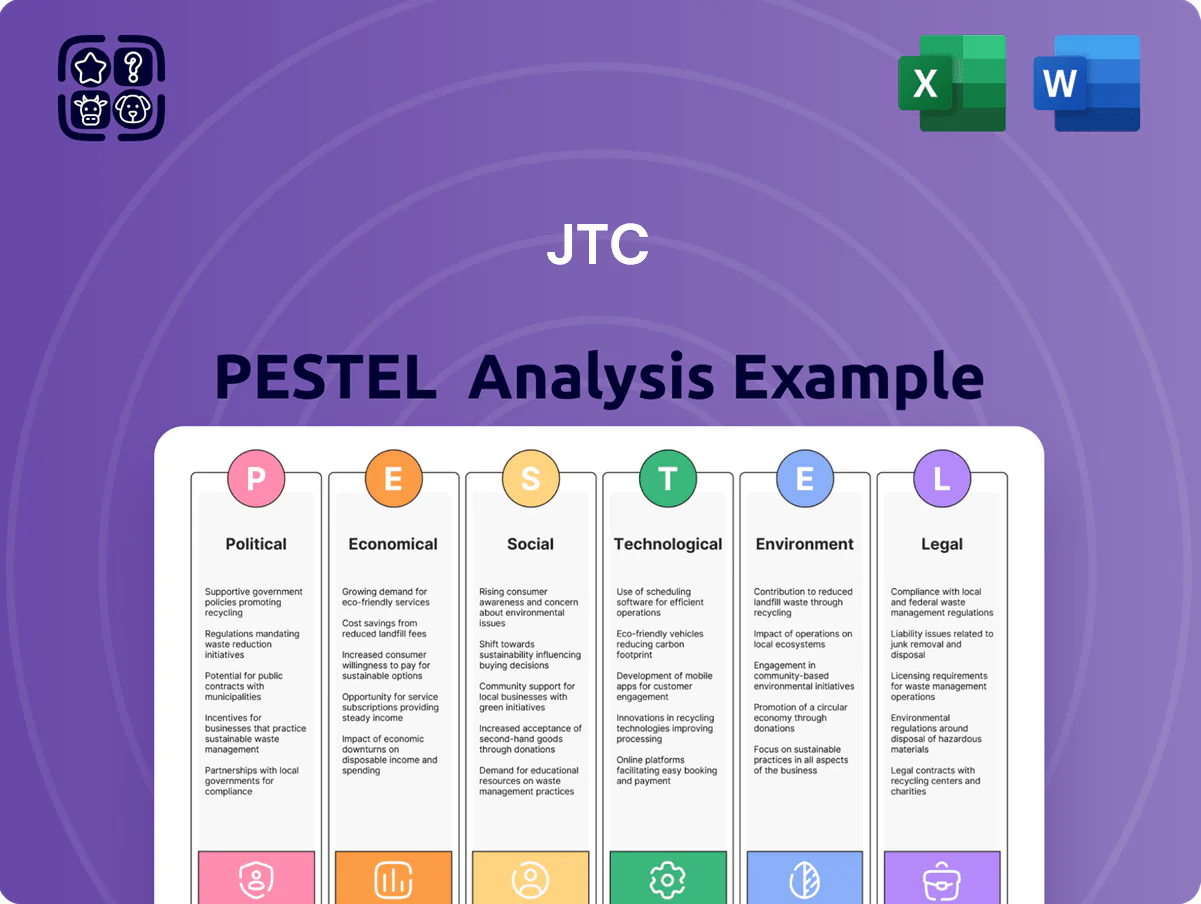

Explores how external macro-environmental factors uniquely affect the JTC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and entrepreneurs.

Offers a concise, visually segmented PESTLE summary tailored for JTC that’s easy to drop into presentations, share across teams, and annotate with region- or business-specific notes to streamline strategic planning and risk discussions.

Economic factors

Interest rate volatility and asset pricing

The transition from high-rate 2022-24 to a more stabilized but elevated cycle by end-2025 shifts discount rates for alternative assets JTC administers, compressing NAVs — for example, a 100bp rise can lower private equity valuations by ~8-12% per MSCI/IRR sensitivity studies.

Rate volatility raises borrowing costs: average commercial mortgage rates rose to ~6.5% in 2024, increasing leverage costs for PE and real estate clients and pressuring fund returns.

JTC must reprice services and adjust financial planning—hedging interest exposure, revising fee schedules, and managing debt (net debt/EBITDA targets) to preserve margins amid higher capital expenditure costs.

Growth of alternative asset classes

The shift to private markets—assets under management in private equity, private debt and infrastructure rose to about $16.6tn in 2024—boosts demand for JTC’s institutional services as investors seek diversification and higher yields.

Growth in global private credit, which hit roughly $1.5tn in 2024, and rising venture capital activity create a steady pipeline of fund administration work for JTC.

JTC’s ability to capture this depends on scalable operations and specialist teams; revenue per employee and investment in tech will determine market share gains.

Inflationary pressure on operating margins

Persistent global inflation in 2021–2024 pushed wage growth and overheads up; UK CPI peaked near 11.1% (Oct 2022) and average UK pay settlements rose ~6% in 2023, pressuring JTC’s operating margins as labor is ~60% of professional services costs. Balancing competitive client pricing with 8–12% salary increases for key talent and targeting 10–15% efficiency gains via automation and process optimization is critical to protect EBITDA margins.

Currency exchange rate fluctuations

Operating across 20+ jurisdictions exposes JTC to FX risk as revenues and costs span GBP, USD, EUR and other currencies; FX moves drove a ~£5–10m swing in reported operating profit sensitivity in 2024 stress tests.

Sharp fluctuations in GBP, USD or EUR can materially affect consolidated results and overseas operation margins; JTC’s 2024 accounts note multi-currency invoicing reduced net translation volatility by ~30% year-on-year.

JTC uses forward hedges, cross-currency swaps and multi-currency accounting to mitigate exposure and deliver transparent FX disclosures to shareholders in quarterly reports.

- 20+ jurisdictions; material FX exposure

- 2024 sensitivity: ~£5–10m P&L swing in stress tests

- Multi-currency invoicing cut translation volatility ~30% YoY (2024)

- Hedging: forwards, cross-currency swaps, transparent quarterly disclosures

Expansion of the UHNW wealth segment

Despite macro uncertainty, the UHNW segment grew to an estimated 295,000 individuals globally in 2024, up ~3.2% year-on-year, sustaining demand for JTC’s private client services.

Rapid wealth accumulation in emerging markets—UHNW population in Asia-Pacific rose ~5% in 2024—and professionalized family offices drive need for bespoke fiduciary and administration solutions.

JTC’s revenue growth depends on penetrating these hubs and delivering intergenerational capital protection and growth services to capture rising client mandates.

- Global UHNW: ~295,000 (2024), +3.2% YoY

Higher-for-longer rates squeeze private NAVs; private credit and FX hedging soften hit

Higher-for-longer rates compressed private-markets NAVs (100bp ≈ −8–12% PE values); commercial mortgage rates ~6.5% in 2024 raised leverage costs; private assets AUM ~ $16.6tn and private credit ~$1.5tn (2024) boost demand; FX exposure across 20+ jurisdictions caused ~£5–10m P&L swing in 2024 stress tests, partly mitigated by multi-currency invoicing (~30% lower translation volatility).

| Metric | 2024 |

|---|---|

| Private assets AUM | $16.6tn |

| Private credit | $1.5tn |

| Commercial mortgage rate | ~6.5% |

| GBP/USD/EUR P&L sensitivity | ~£5–10m |

| Translation volatility reduction | ~30% YoY |

Preview the Actual Deliverable

JTC PESTLE Analysis

The preview shown here is the exact JTC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a competitive edge with our expert PESTLE Analysis of JTC—uncover how political shifts, economic trends, and regulatory changes will shape the company’s future and your strategy; download the full report for actionable, boardroom-ready insights and instant, editable files.

Political factors

Geopolitical instability and sanctions

Ongoing tensions in Eastern Europe and the Middle East require JTC to rigorously monitor international sanction lists—UN, OFAC and EU—after global sanctions rose 22% in 2024, protecting reputation and avoiding multi‑million‑dollar fines (average AML fine >$50m in 2023–24).

As a global provider, JTC must navigate shifting alliances that altered cross‑border capital flows, with UK–US asset transfers up 6% in 2024 while flows to some emerging markets fell 12%.

Political instability can trigger sudden regulatory changes; JTC needs agile compliance frameworks and real‑time screening to ensure client assets remain protected and legally compliant across all jurisdictions.

Global tax transparency initiatives

The OECD/G20 BEPS 2.0 Pillar Two, effective 2024 with 15% global minimum tax adoption by 140+ jurisdictions, increases reporting complexity for JTC’s private and institutional clients and could raise compliance costs by an estimated 5–8% of fee revenue in affected mandates.

Political pressure to curb tax havens compels JTC to validate economic substance across its structures; non-compliance risk has risen as automatic exchange data expanded to 100+ countries under CRS, increasing due-diligence workloads.

Maintaining active engagement with regulators and political bodies—notably in the UK, EU, Cayman Islands and Guernsey, where JTC operates—helps anticipate policy shifts that may alter jurisdiction attractiveness and client structuring decisions.

Regulatory shifts in the United States

The US political environment is pivotal as JTC expands in the American mid-market, where 2024 SEC proposals and state-level regulatory changes have raised private fund reporting scrutiny—SEC’s Form PF and proposed rules could increase compliance costs by an estimated 10–15% for administrators; shifts in Congress or state leadership may accelerate oversight or introduce divergent requirements across key states like California and New York; proactive engagement and scalable compliance platforms are essential to capture rising outsourced administration demand from ~7,000 US private funds.

Trade agreements and market access

Post-Brexit, UK bilateral deals—170+ agreements updated by 2025—shift JTC resource allocation toward UK, EU, UAE, and Singapore hubs as firms seek regulatory certainty and market access.

Political rulings on equivalence and market access, including EU-UK financial services talks and ongoing UK-US regulatory alignment efforts, directly affect JTC’s cross-border capital flows and service licensing costs.

JTC must monitor trade policy shifts and tariff/non-tariff measures that could raise compliance costs or disrupt the firm’s cross-border delivery, where a 1–3% rise in administrative costs could erode margins.

- 170+ UK trade updates by 2025; focus on UK, EU, UAE, Singapore

- Equivalence decisions drive licensing and capital mobility

- Policy shifts can raise compliance costs 1–3%

Stability of offshore financial centers

The political stability of Jersey, Guernsey and the Cayman Islands underpins JTC’s trust, fiduciary and fund administration services; Jersey reported zero government changes since 2018 and Cayman maintains a Moody’s Aa2 local rating as of 2025, which supports client confidence.

Any major policy shifts or unrest could trigger asset relocations and client withdrawals; JTC monitors developments and reported in 2024 that 85% of its offshore revenue was tied to these jurisdictions, guiding its jurisdictional strategy.

- Jersey/Guernsey/Cayman: high political stability, Moody’s Aa2 (Cayman) 2025

- 85% of JTC offshore revenue linked to these centers (2024)

- Active monitoring of local politics to mitigate client flight risk

Political risks surge JTC compliance costs 5–15% as 85% revenue ties to Jersey/Guernsey/Cayman

Political risks (sanctions, tax reform, regulatory shifts) raised JTC compliance costs ~5–15% in 2024–25; 85% offshore revenue tied to Jersey/Guernsey/Cayman; BEPS Pillar Two (15%) adopted by 140+ jurisdictions; UK–US flows +6% (2024), EM flows -12% (2024); ~7,000 US private funds drive SEC scrutiny.

| Metric | Value |

|---|---|

| Offshore revenue exposure (2024) | 85% |

| BEPS Pillar Two adoption | 140+ jurisdictions |

| Compliance cost impact | 5–15% |

| UK–US flows (2024) | +6% |

| EM flows (2024) | -12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the JTC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and entrepreneurs.

Offers a concise, visually segmented PESTLE summary tailored for JTC that’s easy to drop into presentations, share across teams, and annotate with region- or business-specific notes to streamline strategic planning and risk discussions.

Economic factors

Interest rate volatility and asset pricing

The transition from high-rate 2022-24 to a more stabilized but elevated cycle by end-2025 shifts discount rates for alternative assets JTC administers, compressing NAVs — for example, a 100bp rise can lower private equity valuations by ~8-12% per MSCI/IRR sensitivity studies.

Rate volatility raises borrowing costs: average commercial mortgage rates rose to ~6.5% in 2024, increasing leverage costs for PE and real estate clients and pressuring fund returns.

JTC must reprice services and adjust financial planning—hedging interest exposure, revising fee schedules, and managing debt (net debt/EBITDA targets) to preserve margins amid higher capital expenditure costs.

Growth of alternative asset classes

The shift to private markets—assets under management in private equity, private debt and infrastructure rose to about $16.6tn in 2024—boosts demand for JTC’s institutional services as investors seek diversification and higher yields.

Growth in global private credit, which hit roughly $1.5tn in 2024, and rising venture capital activity create a steady pipeline of fund administration work for JTC.

JTC’s ability to capture this depends on scalable operations and specialist teams; revenue per employee and investment in tech will determine market share gains.

Inflationary pressure on operating margins

Persistent global inflation in 2021–2024 pushed wage growth and overheads up; UK CPI peaked near 11.1% (Oct 2022) and average UK pay settlements rose ~6% in 2023, pressuring JTC’s operating margins as labor is ~60% of professional services costs. Balancing competitive client pricing with 8–12% salary increases for key talent and targeting 10–15% efficiency gains via automation and process optimization is critical to protect EBITDA margins.

Currency exchange rate fluctuations

Operating across 20+ jurisdictions exposes JTC to FX risk as revenues and costs span GBP, USD, EUR and other currencies; FX moves drove a ~£5–10m swing in reported operating profit sensitivity in 2024 stress tests.

Sharp fluctuations in GBP, USD or EUR can materially affect consolidated results and overseas operation margins; JTC’s 2024 accounts note multi-currency invoicing reduced net translation volatility by ~30% year-on-year.

JTC uses forward hedges, cross-currency swaps and multi-currency accounting to mitigate exposure and deliver transparent FX disclosures to shareholders in quarterly reports.

- 20+ jurisdictions; material FX exposure

- 2024 sensitivity: ~£5–10m P&L swing in stress tests

- Multi-currency invoicing cut translation volatility ~30% YoY (2024)

- Hedging: forwards, cross-currency swaps, transparent quarterly disclosures

Expansion of the UHNW wealth segment

Despite macro uncertainty, the UHNW segment grew to an estimated 295,000 individuals globally in 2024, up ~3.2% year-on-year, sustaining demand for JTC’s private client services.

Rapid wealth accumulation in emerging markets—UHNW population in Asia-Pacific rose ~5% in 2024—and professionalized family offices drive need for bespoke fiduciary and administration solutions.

JTC’s revenue growth depends on penetrating these hubs and delivering intergenerational capital protection and growth services to capture rising client mandates.

- Global UHNW: ~295,000 (2024), +3.2% YoY

Higher-for-longer rates squeeze private NAVs; private credit and FX hedging soften hit

Higher-for-longer rates compressed private-markets NAVs (100bp ≈ −8–12% PE values); commercial mortgage rates ~6.5% in 2024 raised leverage costs; private assets AUM ~ $16.6tn and private credit ~$1.5tn (2024) boost demand; FX exposure across 20+ jurisdictions caused ~£5–10m P&L swing in 2024 stress tests, partly mitigated by multi-currency invoicing (~30% lower translation volatility).

| Metric | 2024 |

|---|---|

| Private assets AUM | $16.6tn |

| Private credit | $1.5tn |

| Commercial mortgage rate | ~6.5% |

| GBP/USD/EUR P&L sensitivity | ~£5–10m |

| Translation volatility reduction | ~30% YoY |

Preview the Actual Deliverable

JTC PESTLE Analysis

The preview shown here is the exact JTC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.