Juroku Financial Group Business Model Canvas

Juroku Financial Group: Concise Business Model Canvas & Strategic Blueprint

Unlock the full strategic blueprint behind Juroku Financial Group's business model—this concise Business Model Canvas exposes how the firm creates customer value, leverages regional banking strengths, and generates diversified revenue streams; perfect for investors, consultants, and entrepreneurs seeking actionable insights and ready-to-use templates.

Partnerships

Regional Financial Alliances

Juroku Financial Group partners with regional banks to split IT and infrastructure costs, cutting per-bank digital platform spend by about 40% and lowering capex growth to ~3% annually; shared systems served 1.2 million retail accounts across alliances by Dec 2025.

Local Government and Public Entities

Juroku Financial Group works with Gifu and Aichi prefectural governments to manage public funds and run subsidized lending aimed at SMEs and regional projects; in FY2024 the group administered about ¥28.7 billion in government-backed loans and guarantees supporting roughly 3,200 local firms.

Fintech and Technology Providers

Collaborations with tech firms let Juroku Financial Group embed AI and blockchain into mobile banking and automated credit scoring, cutting loan decision times by ~60% in pilots and reducing fraud losses 18% YTD; partners supply cloud, ledger, and ML stacks that supported a 2024 rollout to 1.2M users and are key to meeting 2025 digital-first demand from customers aged 18–34, who represent 42% of new accounts.

Business Succession and M&A Specialists

The group engages M&A and succession consultants to handle complex exits and reorganizations, giving banks legal and structural know-how that complements Juroku Financial Group’s lending; in 2024 these partnerships helped secure deals worth about ¥48.5 billion for corporate clients, reducing churn by an estimated 12%.

- Specialists provide legal and structural expertise

- Complements lending to enable full-scope transitions

- 2024: ~¥48.5bn in partner-supported deals

- Estimated 12% lower client churn after engagements

Global Banking Correspondents

Juroku maintains correspondent-banking links across 28 countries to support Tokai SMEs in cross-border trade, FX and export finance; in 2024 these corridors handled ¥62.4 billion in trade flows, 42% tied to automotive and machinery suppliers.

- 28-country network

- ¥62.4 billion trade flow (2024)

- 42% automotive/machinery

- services: trade finance, FX, overseas support

Juroku: Shared IT cuts costs 40%, AI + blockchain speed loans 60%, ¥139.6bn 2024 impact

Juroku Financial Group shares IT/infrastructure with regional banks (cuts platform cost ~40%, capex growth ~3%), administers ¥28.7bn gov-backed SME loans (FY2024), embeds AI/blockchain (60% faster credit decisions, fraud −18%), supported ¥48.5bn partner M&A deals (2024), and ran ¥62.4bn cross-border flows across 28 countries (2024).

| Partnership | Key 2024–25 metric |

|---|---|

| Shared IT | −40% cost, capex +3% |

| Gov loans | ¥28.7bn, 3,200 firms |

| Tech | +60% speed, −18% fraud |

| M&A | ¥48.5bn, −12% churn |

| Correspondent | 28 countries, ¥62.4bn |

What is included in the product

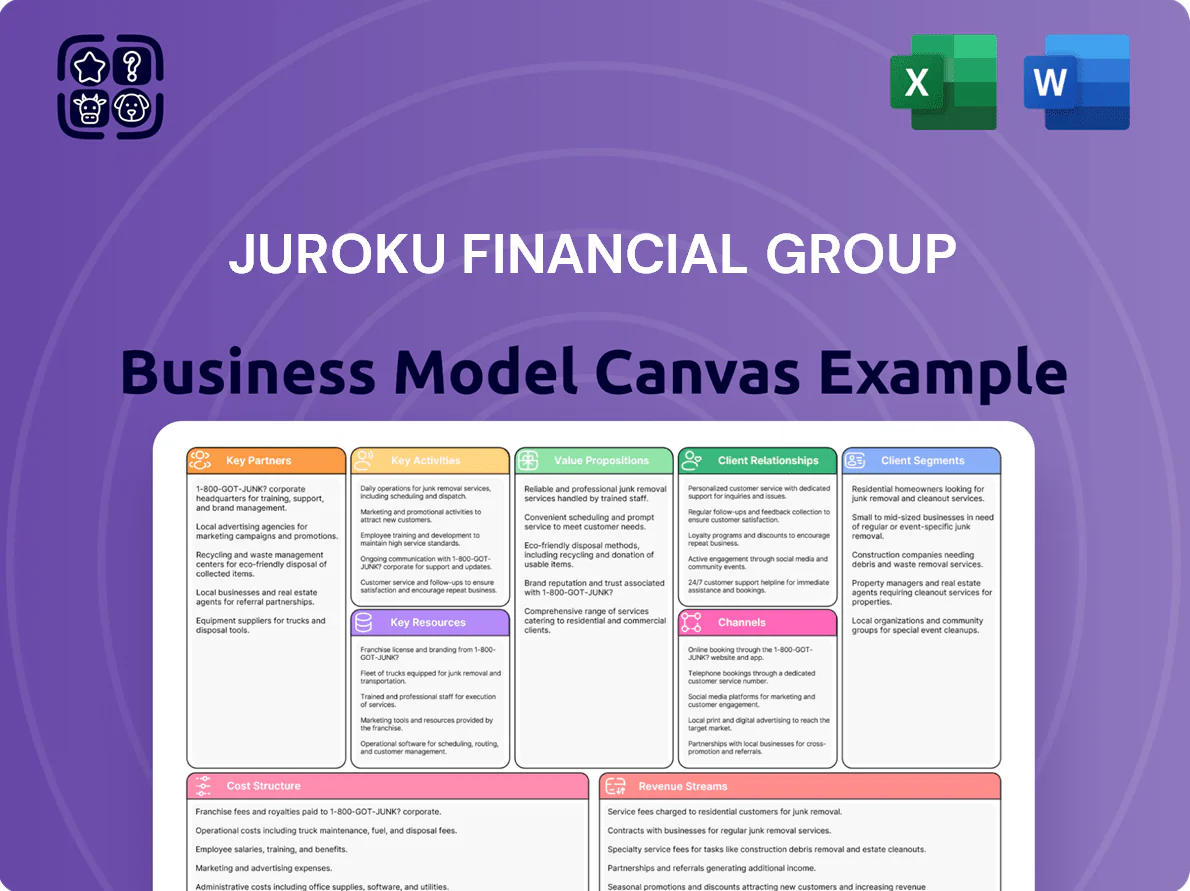

A concise, pre-built Business Model Canvas for Juroku Financial Group detailing customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and governance—aligned with its real-world operations and strategic direction to support presentations, investor discussions, and strategic planning.

High-level view of Juroku Financial Group’s business model with editable cells, condensing its banking, insurance, and asset-management strategies into a single, shareable canvas for fast comparison, collaboration, and executive review.

Activities

Credit and Loan Management

The group conducts rigorous credit assessment and disburses mortgages, small-business loans, and ¥350+ billion in industrial financing concentrated in the Tokai region, matching sector risks to borrower cash flows; retail mortgages account for ~42% of the loan book (2025 YE). Effective risk monitoring uses quarterly PD/LGD models and limits to keep NPLs near 0.6% and maintain CET1-like capital buffers above 11.5%.

Wealth Management and Financial Planning

Juroku provides comprehensive investment advisory and financial planning that shifts household savings into productive vehicles—selling investment trusts, insurance, and inheritance-planning services—to counter mid-2020s inflation (Japan CPI ~3.2% in 2024). This drives fee-based income: advisory fees plus product commissions, aiming to convert a portion of the ¥1,200 trillion household financial assets into higher-yield investments.

Digital Transformation and IT Development

Continuous upgrades to digital touchpoints—notably the Juroku Bank app—plus robotic process automation for back-office tasks are core activities to boost efficiency and CX; by end-2025 Juroku Financial Group targets a digital migration to cut cost-to-income toward 40% (from ~48% in FY2022) and aims to automate ~30% of admin workflows, reducing processing time by roughly 25%.

Regional Economic Consulting

The group provides strategic advisory to local SMEs on expansion and productivity, citing a 2024 pilot where 62 clients raised revenues by a median 18% within 12 months after consulting.

Juroku runs business-matching events linking regional suppliers to national/international buyers—events in 2024 generated ¥1.3bn in confirmed orders—and positions the bank as growth partner, not just lender.

- 62 SMEs: median +18% revenue (2024 pilot)

- ¥1.3bn in orders from 2024 matching events

- Focus: expansion, productivity, buyer links

Compliance and Risk Mitigation

Compliance and Risk Mitigation: Juroku Financial Group continuously aligns with Japan’s Financial Services Agency rules and Basel III capital/liquidity ratios, running real-time monitoring to meet CET1 targets (about 9–11% industry range in 2025) while scanning transactions to curb AML (anti-money laundering) risks.

They stress test for interest-rate shocks after the 2024 global rate shifts, keep internal controls to limit reputational loss, and hold liquidity coverage near 100%+.

- Monitor transactions for AML 24/7

- Maintain CET1 ~9–11% target

- Stress-test IRR (interest rate risk) quarterly

- Keep LCR (liquidity coverage) ~100%+

Juroku: Retail-heavy lender boosts SME growth, cuts costs to 40% with ¥350bn industrial loans

Juroku underwrites mortgages, SME and ¥350bn Tokai industrial loans (retail ~42% of book, 2025 YE), runs advisory/fee sales to shift household assets into higher-yield products, upgrades digital/automation to cut cost-to-income toward 40% by 2025, and delivers SME consulting/matching (2024: 62 SMEs +18% median revenue; ¥1.3bn orders).

| Metric | Value |

|---|---|

| Loan mix | Retail 42% |

| Industrial loans | ¥350bn |

| NPLs | ~0.6% |

| Cost-to-income target | 40% (2025) |

| SME pilot | 62 firms, +18% |

| Matching orders | ¥1.3bn (2024) |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Juroku Financial Group Business Model Canvas—not a mockup—and it matches the full document you’ll receive after purchase.

When you complete your order, you’ll get this exact file in editable formats, with all sections, content, and formatting intact—ready to present or adapt.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Juroku Financial Group: Concise Business Model Canvas & Strategic Blueprint

Unlock the full strategic blueprint behind Juroku Financial Group's business model—this concise Business Model Canvas exposes how the firm creates customer value, leverages regional banking strengths, and generates diversified revenue streams; perfect for investors, consultants, and entrepreneurs seeking actionable insights and ready-to-use templates.

Partnerships

Regional Financial Alliances

Juroku Financial Group partners with regional banks to split IT and infrastructure costs, cutting per-bank digital platform spend by about 40% and lowering capex growth to ~3% annually; shared systems served 1.2 million retail accounts across alliances by Dec 2025.

Local Government and Public Entities

Juroku Financial Group works with Gifu and Aichi prefectural governments to manage public funds and run subsidized lending aimed at SMEs and regional projects; in FY2024 the group administered about ¥28.7 billion in government-backed loans and guarantees supporting roughly 3,200 local firms.

Fintech and Technology Providers

Collaborations with tech firms let Juroku Financial Group embed AI and blockchain into mobile banking and automated credit scoring, cutting loan decision times by ~60% in pilots and reducing fraud losses 18% YTD; partners supply cloud, ledger, and ML stacks that supported a 2024 rollout to 1.2M users and are key to meeting 2025 digital-first demand from customers aged 18–34, who represent 42% of new accounts.

Business Succession and M&A Specialists

The group engages M&A and succession consultants to handle complex exits and reorganizations, giving banks legal and structural know-how that complements Juroku Financial Group’s lending; in 2024 these partnerships helped secure deals worth about ¥48.5 billion for corporate clients, reducing churn by an estimated 12%.

- Specialists provide legal and structural expertise

- Complements lending to enable full-scope transitions

- 2024: ~¥48.5bn in partner-supported deals

- Estimated 12% lower client churn after engagements

Global Banking Correspondents

Juroku maintains correspondent-banking links across 28 countries to support Tokai SMEs in cross-border trade, FX and export finance; in 2024 these corridors handled ¥62.4 billion in trade flows, 42% tied to automotive and machinery suppliers.

- 28-country network

- ¥62.4 billion trade flow (2024)

- 42% automotive/machinery

- services: trade finance, FX, overseas support

Juroku: Shared IT cuts costs 40%, AI + blockchain speed loans 60%, ¥139.6bn 2024 impact

Juroku Financial Group shares IT/infrastructure with regional banks (cuts platform cost ~40%, capex growth ~3%), administers ¥28.7bn gov-backed SME loans (FY2024), embeds AI/blockchain (60% faster credit decisions, fraud −18%), supported ¥48.5bn partner M&A deals (2024), and ran ¥62.4bn cross-border flows across 28 countries (2024).

| Partnership | Key 2024–25 metric |

|---|---|

| Shared IT | −40% cost, capex +3% |

| Gov loans | ¥28.7bn, 3,200 firms |

| Tech | +60% speed, −18% fraud |

| M&A | ¥48.5bn, −12% churn |

| Correspondent | 28 countries, ¥62.4bn |

What is included in the product

A concise, pre-built Business Model Canvas for Juroku Financial Group detailing customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and governance—aligned with its real-world operations and strategic direction to support presentations, investor discussions, and strategic planning.

High-level view of Juroku Financial Group’s business model with editable cells, condensing its banking, insurance, and asset-management strategies into a single, shareable canvas for fast comparison, collaboration, and executive review.

Activities

Credit and Loan Management

The group conducts rigorous credit assessment and disburses mortgages, small-business loans, and ¥350+ billion in industrial financing concentrated in the Tokai region, matching sector risks to borrower cash flows; retail mortgages account for ~42% of the loan book (2025 YE). Effective risk monitoring uses quarterly PD/LGD models and limits to keep NPLs near 0.6% and maintain CET1-like capital buffers above 11.5%.

Wealth Management and Financial Planning

Juroku provides comprehensive investment advisory and financial planning that shifts household savings into productive vehicles—selling investment trusts, insurance, and inheritance-planning services—to counter mid-2020s inflation (Japan CPI ~3.2% in 2024). This drives fee-based income: advisory fees plus product commissions, aiming to convert a portion of the ¥1,200 trillion household financial assets into higher-yield investments.

Digital Transformation and IT Development

Continuous upgrades to digital touchpoints—notably the Juroku Bank app—plus robotic process automation for back-office tasks are core activities to boost efficiency and CX; by end-2025 Juroku Financial Group targets a digital migration to cut cost-to-income toward 40% (from ~48% in FY2022) and aims to automate ~30% of admin workflows, reducing processing time by roughly 25%.

Regional Economic Consulting

The group provides strategic advisory to local SMEs on expansion and productivity, citing a 2024 pilot where 62 clients raised revenues by a median 18% within 12 months after consulting.

Juroku runs business-matching events linking regional suppliers to national/international buyers—events in 2024 generated ¥1.3bn in confirmed orders—and positions the bank as growth partner, not just lender.

- 62 SMEs: median +18% revenue (2024 pilot)

- ¥1.3bn in orders from 2024 matching events

- Focus: expansion, productivity, buyer links

Compliance and Risk Mitigation

Compliance and Risk Mitigation: Juroku Financial Group continuously aligns with Japan’s Financial Services Agency rules and Basel III capital/liquidity ratios, running real-time monitoring to meet CET1 targets (about 9–11% industry range in 2025) while scanning transactions to curb AML (anti-money laundering) risks.

They stress test for interest-rate shocks after the 2024 global rate shifts, keep internal controls to limit reputational loss, and hold liquidity coverage near 100%+.

- Monitor transactions for AML 24/7

- Maintain CET1 ~9–11% target

- Stress-test IRR (interest rate risk) quarterly

- Keep LCR (liquidity coverage) ~100%+

Juroku: Retail-heavy lender boosts SME growth, cuts costs to 40% with ¥350bn industrial loans

Juroku underwrites mortgages, SME and ¥350bn Tokai industrial loans (retail ~42% of book, 2025 YE), runs advisory/fee sales to shift household assets into higher-yield products, upgrades digital/automation to cut cost-to-income toward 40% by 2025, and delivers SME consulting/matching (2024: 62 SMEs +18% median revenue; ¥1.3bn orders).

| Metric | Value |

|---|---|

| Loan mix | Retail 42% |

| Industrial loans | ¥350bn |

| NPLs | ~0.6% |

| Cost-to-income target | 40% (2025) |

| SME pilot | 62 firms, +18% |

| Matching orders | ¥1.3bn (2024) |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Juroku Financial Group Business Model Canvas—not a mockup—and it matches the full document you’ll receive after purchase.

When you complete your order, you’ll get this exact file in editable formats, with all sections, content, and formatting intact—ready to present or adapt.