Juroku Financial Group PESTLE Analysis

Skip the Research. Get the Strategy.

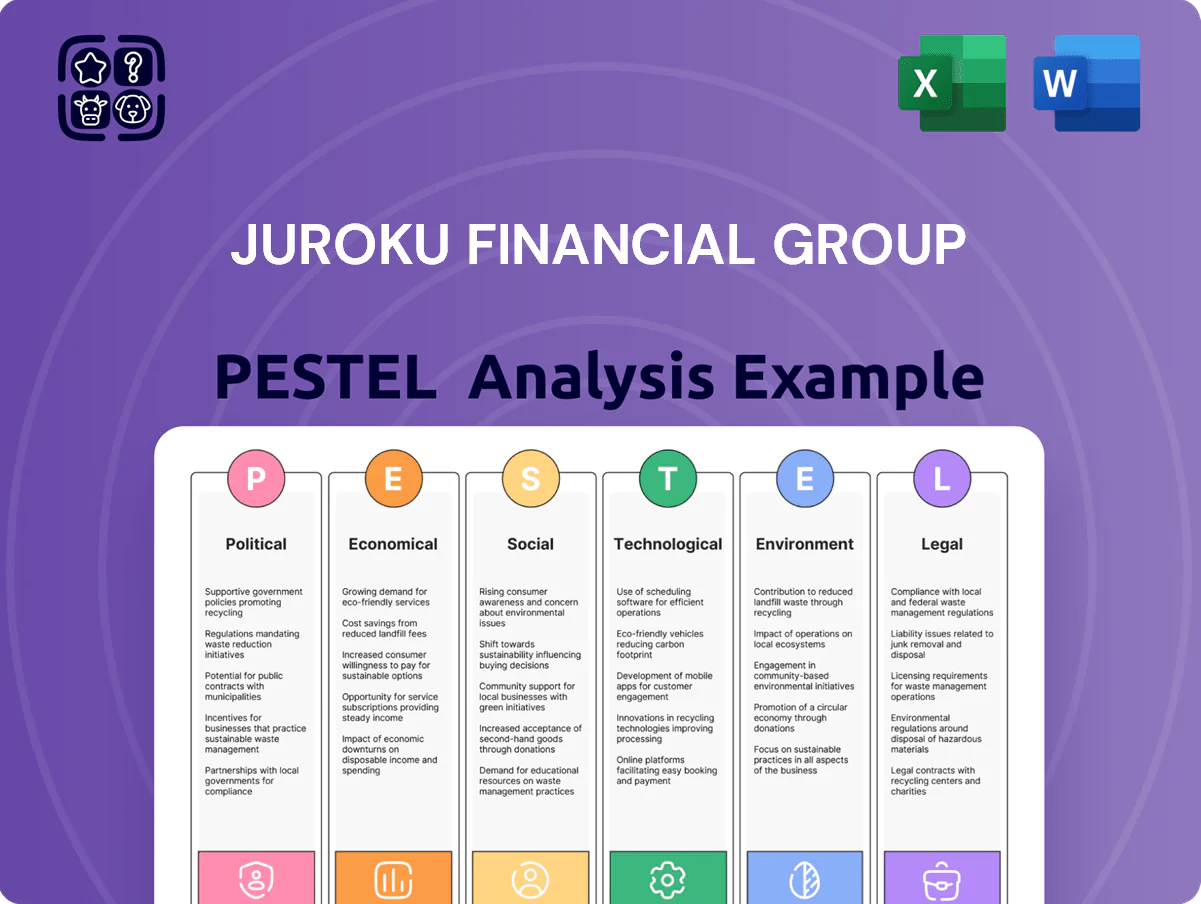

Gain a strategic advantage with our PESTLE Analysis of Juroku Financial Group—uncover how political, economic, social, technological, legal, and environmental forces will shape its future performance and risk profile. Ideal for investors, advisors, and strategists, this concise briefing highlights actionable insights to inform decisions and scenario planning. Purchase the full report for the complete, editable breakdown and immediate download.

Political factors

BoJ Monetary Policy Shift

The BoJ exited negative rates in 2024–25, raising the policy rate to around 0.1–0.5% by mid-2025, forcing Juroku to adjust net interest margins amid political demands to curb inflation (CPI ~3% in 2024) while supporting regional growth.

Heightened pressure from national and local governments pushes Juroku to balance higher lending yields with credit relief for SMEs, which comprise over 70% of its corporate loan book, to avoid local economic strain.

Regional Revitalization Initiatives

The Japanese government’s Regional Revitalization policy, backed by a ¥1.5 trillion budget in 2024, targets depopulated prefectures—directly affecting Juroku’s Gifu base where population fell 0.8% in 2023—pushing banks to support business succession and local industry growth.

Political mandates encourage regional banks to act as coordinators for M&A and SME support; Juroku’s 2024 strategy must align to access subsidies and low-interest public loans.

Geopolitical Trade Volatility

As a key financier for Chubu-region manufacturers that account for over 40% of Gifu and Aichi industrial exports, Juroku is highly exposed to shifting trade policies and US-China tariffs that raised regional export volatility by 18% in 2024.

Escalating geopolitical tensions and supply-chain disruptions drove delinquency risk up 60 bps for corporate loans in FY2024, increasing expected credit losses for export-dependent clients.

Management must closely monitor diplomatic shifts—notably Japan-EU EPA adjustments and China trade measures—that could materially affect capital needs across the export-heavy clusters in Gifu and Aichi.

Financial Services Agency Oversight

The Financial Services Agency intensified oversight in late 2025, targeting governance and sustainability of regional holding companies after a 2024 review found 28% of regional groups had inadequate risk frameworks; Juroku faces demands for greater transparency and capital planning disclosures.

Regulatory expectations now require strengthened risk management, board-level compliance reporting, and stress-testing; noncompliance risks higher supervisory measures that could affect Juroku’s ROE target of ~6.5% in FY2025.

- FSA tightened oversight late 2025 following 2024 review (28% gaps)

- Higher disclosure and stress-test requirements

- Potential impact on Juroku’s FY2025 ROE ~6.5% and profitability targets

Tax Reform and Investment Incentives

Japanese tax reforms since 2023, including incentives to shift household assets toward risk-bearing instruments, have grown retail investment: NISA accounts reached about 30 million by end-2024, boosting assets under management in regional banks like Juroku, which increased investment trust sales by mid-single digits in 2024.

Political backing for expanded NISA (higher contribution caps from 2024) aligns Juroku Financial Group’s push into wealth management, aiding diversification away from net interest income that fell industry-wide to near historic lows (NIMs ~0.10% in 2024).

- 30 million NISA accounts (end-2024)

- Mid-single-digit growth in Juroku investment trust sales (2024)

- Industry NIM ~0.10% (2024)

Juroku pivots: BoJ normalization, regional stimulus & tougher oversight squeeze NIMs

Political shifts—BoJ rate normalization (policy ~0.1–0.5% mid‑2025), Regional Revitalization ¥1.5T (2024), stronger FSA oversight (late‑2025) and expanded NISA (30M accounts end‑2024)—force Juroku to rebalance NIMs (~0.10% 2024), SME relief (70% of loan book), higher stress‑testing and capital planning to protect FY2025 ROE ~6.5%.

| Metric | Value |

|---|---|

| Policy rate | 0.1–0.5% (mid‑2025) |

| NISA accounts | 30M (end‑2024) |

| NIM | ~0.10% (2024) |

| SME loans | ~70% of book |

| Regional budget | ¥1.5T (2024) |

| FY2025 ROE target | ~6.5% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Juroku Financial Group, with data-backed trends, region-specific regulatory insights, and forward-looking scenarios to help executives and investors identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Juroku Financial Group that’s visually segmented for quick meeting reference, easily dropped into presentations, and editable for regional or business-line notes to support rapid alignment and risk discussions.

Economic factors

Interest Rate Margin Expansion

Normalization of interest rates by end-2025 lifted Juroku Financial Group's net interest margin to about 1.35% in FY2025 from 0.95% in FY2022, driven by average loan yields rising ~120 bps while deposit costs rose only ~30 bps.

Regional Manufacturing Health

Gifu Prefecture’s economy remains concentrated in automotive and precision machinery; these sectors saw a 2024 output drop of 3.8% YoY and faced raw material price volatility—steel up ~12% in 2023–24—pressuring margins.

Juroku Financial Group’s loan book exposure to regional manufacturers was ~28% of corporate lending in FY2024, tying performance to local industrial output and capex cycles.

Global auto downturns in 2024 reduced vehicle production ~5% globally, raising Juroku’s reported NPL ratio to 1.15% in FY2024, signaling heightened credit risk from the sector.

Inflationary Pressure on SMEs

Persistent inflation through 2025 raised input costs for Juroku Financial Group’s SME clients, with Japan’s core CPI averaging about 2.7% in 2024 and CPI remaining above 2% into 2025, increasing operating expenses and supply costs.

While larger SMEs passed on price rises, many smaller firms saw margins shrink—SME operating margins fell by an estimated 1.2–2.0 percentage points in 2024—weakening debt-servicing capacity.

Juroku must tighten credit provisioning and stress-test portfolios: nonperforming loan ratios for regional banks nudged up in 2024, prompting higher loan-loss reserves amid a higher-cost local adjustment.

Labor Shortages and Wage Growth

Japan's unemployment rate remained low at 2.5% in 2025, pressuring Chubu employers to raise base wages by about 3.2% year-on-year, altering local wage equilibrium and lifting household income.

Higher wages support consumer spending and pushed mortgage applications up ~4% in the Chubu region in 2024–25, but raise operating costs for Juroku’s corporate borrowers, tightening credit metrics.

Juroku’s economic forecasts must embed structural labor shifts—projecting continued wage growth of 2–3% annually and scenario-testing borrower stress under rising labor costs.

- Unemployment 2.5% (2025)

- Chubu wage growth ~3.2% YoY

- Mortgage demand +4% (2024–25)

- Forecast wage growth 2–3% p.a.; model borrower cost stress

Wealth Transfer and Inheritance

The impending intergenerational wealth transfer—Japan’s estimated 400 trillion yen shift by 2040—creates both growth and retention risks for Juroku Financial Group; its aging depositor base means capturing inherited assets via specialized inheritance consulting and trust services is crucial to prevent migration to Tokyo-based banks.

Failure to secure these flows could trigger sizable deposit outflows, given metropolitan competitors already gaining market share; targeted legacy planning, tax-efficient trust products, and proactive client outreach are essential to convert an estimated multi-trillion-yen opportunity into retained AUM.

- Japan wealth transfer ~400 trillion yen by 2040

- Large aging depositor base = priority for inheritance services

- Risk: deposit outflows to metropolitan banks if assets not retained

- Mitigation: inheritance consulting, trusts, tax-efficient products, outreach

Rising NIM amid manufacturing slump, higher wages lift mortgages but squeeze SMEs

Economic pressures: NIM rose to ~1.35% in FY2025 vs 0.95% FY2022; regional manufacturing (28% loan book) saw output down 3.8% in 2024 and steel costs +12% (2023–24), lifting NPLs to 1.15% in FY2024; core CPI ~2.7% in 2024 with wages +3.2% in Chubu (2025) boosting mortgage demand +4% but squeezing SME margins ~1.2–2.0ppt.

| Metric | Value |

|---|---|

| NIM FY2025 | 1.35% |

| NPL FY2024 | 1.15% |

| Manufacturing output 2024 | -3.8% YoY |

| Core CPI 2024 | 2.7% |

| Chubu wage growth 2025 | +3.2% YoY |

Same Document Delivered

Juroku Financial Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Juroku Financial Group you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic advantage with our PESTLE Analysis of Juroku Financial Group—uncover how political, economic, social, technological, legal, and environmental forces will shape its future performance and risk profile. Ideal for investors, advisors, and strategists, this concise briefing highlights actionable insights to inform decisions and scenario planning. Purchase the full report for the complete, editable breakdown and immediate download.

Political factors

BoJ Monetary Policy Shift

The BoJ exited negative rates in 2024–25, raising the policy rate to around 0.1–0.5% by mid-2025, forcing Juroku to adjust net interest margins amid political demands to curb inflation (CPI ~3% in 2024) while supporting regional growth.

Heightened pressure from national and local governments pushes Juroku to balance higher lending yields with credit relief for SMEs, which comprise over 70% of its corporate loan book, to avoid local economic strain.

Regional Revitalization Initiatives

The Japanese government’s Regional Revitalization policy, backed by a ¥1.5 trillion budget in 2024, targets depopulated prefectures—directly affecting Juroku’s Gifu base where population fell 0.8% in 2023—pushing banks to support business succession and local industry growth.

Political mandates encourage regional banks to act as coordinators for M&A and SME support; Juroku’s 2024 strategy must align to access subsidies and low-interest public loans.

Geopolitical Trade Volatility

As a key financier for Chubu-region manufacturers that account for over 40% of Gifu and Aichi industrial exports, Juroku is highly exposed to shifting trade policies and US-China tariffs that raised regional export volatility by 18% in 2024.

Escalating geopolitical tensions and supply-chain disruptions drove delinquency risk up 60 bps for corporate loans in FY2024, increasing expected credit losses for export-dependent clients.

Management must closely monitor diplomatic shifts—notably Japan-EU EPA adjustments and China trade measures—that could materially affect capital needs across the export-heavy clusters in Gifu and Aichi.

Financial Services Agency Oversight

The Financial Services Agency intensified oversight in late 2025, targeting governance and sustainability of regional holding companies after a 2024 review found 28% of regional groups had inadequate risk frameworks; Juroku faces demands for greater transparency and capital planning disclosures.

Regulatory expectations now require strengthened risk management, board-level compliance reporting, and stress-testing; noncompliance risks higher supervisory measures that could affect Juroku’s ROE target of ~6.5% in FY2025.

- FSA tightened oversight late 2025 following 2024 review (28% gaps)

- Higher disclosure and stress-test requirements

- Potential impact on Juroku’s FY2025 ROE ~6.5% and profitability targets

Tax Reform and Investment Incentives

Japanese tax reforms since 2023, including incentives to shift household assets toward risk-bearing instruments, have grown retail investment: NISA accounts reached about 30 million by end-2024, boosting assets under management in regional banks like Juroku, which increased investment trust sales by mid-single digits in 2024.

Political backing for expanded NISA (higher contribution caps from 2024) aligns Juroku Financial Group’s push into wealth management, aiding diversification away from net interest income that fell industry-wide to near historic lows (NIMs ~0.10% in 2024).

- 30 million NISA accounts (end-2024)

- Mid-single-digit growth in Juroku investment trust sales (2024)

- Industry NIM ~0.10% (2024)

Juroku pivots: BoJ normalization, regional stimulus & tougher oversight squeeze NIMs

Political shifts—BoJ rate normalization (policy ~0.1–0.5% mid‑2025), Regional Revitalization ¥1.5T (2024), stronger FSA oversight (late‑2025) and expanded NISA (30M accounts end‑2024)—force Juroku to rebalance NIMs (~0.10% 2024), SME relief (70% of loan book), higher stress‑testing and capital planning to protect FY2025 ROE ~6.5%.

| Metric | Value |

|---|---|

| Policy rate | 0.1–0.5% (mid‑2025) |

| NISA accounts | 30M (end‑2024) |

| NIM | ~0.10% (2024) |

| SME loans | ~70% of book |

| Regional budget | ¥1.5T (2024) |

| FY2025 ROE target | ~6.5% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Juroku Financial Group, with data-backed trends, region-specific regulatory insights, and forward-looking scenarios to help executives and investors identify risks, opportunities, and strategic responses.

A concise, shareable PESTLE snapshot of Juroku Financial Group that’s visually segmented for quick meeting reference, easily dropped into presentations, and editable for regional or business-line notes to support rapid alignment and risk discussions.

Economic factors

Interest Rate Margin Expansion

Normalization of interest rates by end-2025 lifted Juroku Financial Group's net interest margin to about 1.35% in FY2025 from 0.95% in FY2022, driven by average loan yields rising ~120 bps while deposit costs rose only ~30 bps.

Regional Manufacturing Health

Gifu Prefecture’s economy remains concentrated in automotive and precision machinery; these sectors saw a 2024 output drop of 3.8% YoY and faced raw material price volatility—steel up ~12% in 2023–24—pressuring margins.

Juroku Financial Group’s loan book exposure to regional manufacturers was ~28% of corporate lending in FY2024, tying performance to local industrial output and capex cycles.

Global auto downturns in 2024 reduced vehicle production ~5% globally, raising Juroku’s reported NPL ratio to 1.15% in FY2024, signaling heightened credit risk from the sector.

Inflationary Pressure on SMEs

Persistent inflation through 2025 raised input costs for Juroku Financial Group’s SME clients, with Japan’s core CPI averaging about 2.7% in 2024 and CPI remaining above 2% into 2025, increasing operating expenses and supply costs.

While larger SMEs passed on price rises, many smaller firms saw margins shrink—SME operating margins fell by an estimated 1.2–2.0 percentage points in 2024—weakening debt-servicing capacity.

Juroku must tighten credit provisioning and stress-test portfolios: nonperforming loan ratios for regional banks nudged up in 2024, prompting higher loan-loss reserves amid a higher-cost local adjustment.

Labor Shortages and Wage Growth

Japan's unemployment rate remained low at 2.5% in 2025, pressuring Chubu employers to raise base wages by about 3.2% year-on-year, altering local wage equilibrium and lifting household income.

Higher wages support consumer spending and pushed mortgage applications up ~4% in the Chubu region in 2024–25, but raise operating costs for Juroku’s corporate borrowers, tightening credit metrics.

Juroku’s economic forecasts must embed structural labor shifts—projecting continued wage growth of 2–3% annually and scenario-testing borrower stress under rising labor costs.

- Unemployment 2.5% (2025)

- Chubu wage growth ~3.2% YoY

- Mortgage demand +4% (2024–25)

- Forecast wage growth 2–3% p.a.; model borrower cost stress

Wealth Transfer and Inheritance

The impending intergenerational wealth transfer—Japan’s estimated 400 trillion yen shift by 2040—creates both growth and retention risks for Juroku Financial Group; its aging depositor base means capturing inherited assets via specialized inheritance consulting and trust services is crucial to prevent migration to Tokyo-based banks.

Failure to secure these flows could trigger sizable deposit outflows, given metropolitan competitors already gaining market share; targeted legacy planning, tax-efficient trust products, and proactive client outreach are essential to convert an estimated multi-trillion-yen opportunity into retained AUM.

- Japan wealth transfer ~400 trillion yen by 2040

- Large aging depositor base = priority for inheritance services

- Risk: deposit outflows to metropolitan banks if assets not retained

- Mitigation: inheritance consulting, trusts, tax-efficient products, outreach

Rising NIM amid manufacturing slump, higher wages lift mortgages but squeeze SMEs

Economic pressures: NIM rose to ~1.35% in FY2025 vs 0.95% FY2022; regional manufacturing (28% loan book) saw output down 3.8% in 2024 and steel costs +12% (2023–24), lifting NPLs to 1.15% in FY2024; core CPI ~2.7% in 2024 with wages +3.2% in Chubu (2025) boosting mortgage demand +4% but squeezing SME margins ~1.2–2.0ppt.

| Metric | Value |

|---|---|

| NIM FY2025 | 1.35% |

| NPL FY2024 | 1.15% |

| Manufacturing output 2024 | -3.8% YoY |

| Core CPI 2024 | 2.7% |

| Chubu wage growth 2025 | +3.2% YoY |

Same Document Delivered

Juroku Financial Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Juroku Financial Group you’ll receive after purchase—fully formatted, professionally structured, and ready to use.