Jyothy Labs SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Jyothy Labs stands out with strong brand recognition in FMCG and a diversified product portfolio, but faces margin pressure from commodity volatility and stiff competition from larger peers; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis for an investor-ready Word report plus editable Excel tools to plan, pitch, or act with confidence.

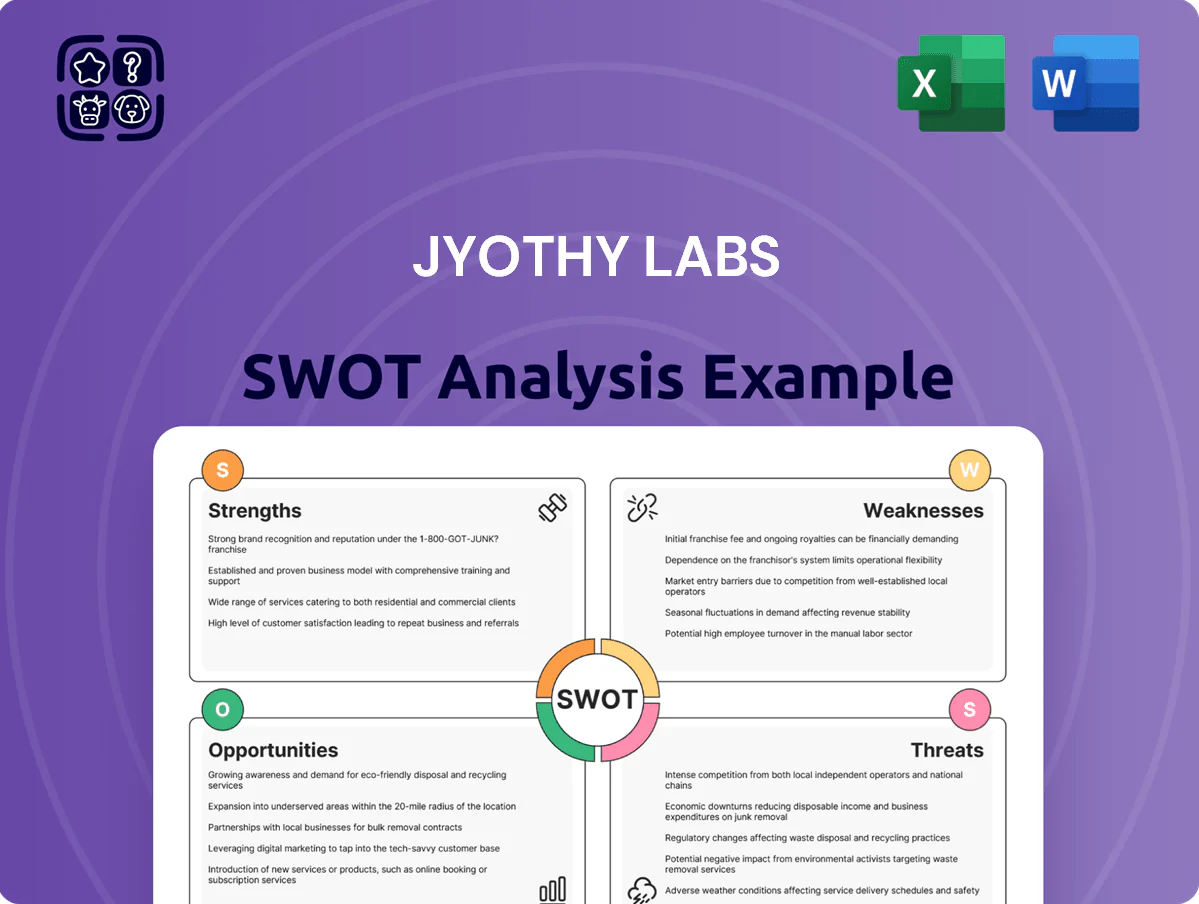

Strengths

Dominant Market Leadership in Fabric Whitening

Ujala holds ~84% share of India’s fabric whitener market as of late 2025, giving Jyothy Labs strong pricing power and recurring cash flow—2024–25 EBITDA margin for the consumer segment rose to roughly 18%, funding category expansion.

Robust Debt-Free Balance Sheet and Liquidity

Jyothy Labs enters 2026 net debt-free with cash and liquid investments above 800 crore INR, preserving a clean balance sheet after FY2025 where interest expense was negligible (below 5 crore INR).

Extensive Multi-Channel Distribution Network

Jyothy Labs has a distribution footprint covering over 3.6 million retail outlets, with direct reach to 1.3 million outlets and 9,900+ channel partners, ensuring strong shelf presence across urban modern trade and deep rural markets.

Agile Localized Manufacturing Infrastructure

Operating 23 plants at 14 locations across India lets Jyothy Labs cut logistics costs and meet regional demand quickly; FY2024 revenue from branded FMCG was Rs 2,047 crore, helping localized sales capture.

This decentralized model boosts resilience to supply disruptions, helps state-level tax planning, and keeps inventory fresher near hubs like South India, shortening the working capital cycle (FY2024 DSO improved by ~6 days).

Successful Diversification into Power Brands

Jyothy Labs has scaled Power Brands beyond Ujala—Exo, Maxo, and Margo—each leading their niches and lowering single-product risk.

Exo and Pril together hold roughly 60% value share in India’s dishwash segment (2024 Kantar); Maxo retained top market share (~30% value) in household insecticides in FY2024, boosting group EBITDA and cross-sell reach.

The multi-category footprint captures more of the household wallet across fabric, home, and personal care, supporting steady revenue diversification and margin resilience.

- Exo+Pril ≈ 60% dishwash value share (2024)

- Maxo ≈ 30% insecticide value share (FY2024)

- Reduces single-product dependency; increases cross-sell

- Positive impact on revenue mix and EBITDA stability

Market‑leading FMCG: Ujala dominance, diversified brands, net‑debt free with ₹800cr+ cash

Market-leading Power Brands: Ujala ~84% fabric whitener share (late 2025); Exo+Pril ≈60% dishwash value (2024); Maxo ≈30% insecticide (FY2024), diversifying revenue and margins.

Net debt-free entering 2026 with cash >800 crore INR; FY2024 branded FMCG revenue Rs 2,047 crore; 23 plants, 14 locations; DSO improved ~6 days (FY2024).

| Metric | Value |

|---|---|

| Ujala market share | ~84% (late 2025) |

| Cash & investments | >800 crore INR (2026) |

| FY2024 branded revenue | Rs 2,047 crore |

| Plants / Locations | 23 / 14 |

What is included in the product

Provides a concise SWOT overview of Jyothy Labs, highlighting its strong brand portfolio and distribution reach, internal cost and innovation challenges, market expansion and product diversification opportunities, and external risks from competition and raw material volatility.

Provides a concise Jyothy Labs SWOT snapshot for rapid strategic alignment, making it easy for executives to visualize strengths, weaknesses, opportunities, and threats in presentations and planning sessions.

Weaknesses

Significant Regional Revenue Concentration

Despite national expansion, about 45% of Jyothy Labs' FY2024 revenue came from South India, with Kerala alone contributing ~18%, leaving the firm exposed to regional shocks. The 2024–25 Kerala floods cut regional sales by an estimated 9–12% in affected quarters, highlighting vulnerability to climatic events and local competition. Rebalancing to a pan‑India mix needs sustained marketing spend—likely 150–200 bps of revenue annually—across North and West.

Margin Vulnerability to Raw Material Inflation

The company’s profitability is highly sensitive to crude-derivative, soda ash and palm oil prices, which pressured gross margins in late 2025; input inflation drove a 210-basis-point YoY gross-margin dip in Q2 FY2026.

Operating margins stayed healthy (around mid-teens EBITDA margin in FY2025), but sudden cost spikes cause temporary contractions.

Competitive pressure to raise grammage or cut retail prices to protect volumes in value segments amplifies margin risk.

Underperformance in the Household Insecticides Segment

Maxo-led household insecticides lagged fabric and dishwash growth, with segment revenue shrinking 6% YoY in FY2024 to about INR 210 crore while fabric care rose 12% and dishwash 9%.

New formats—aerosols and rackets—show early traction, contributing ~8% of insecticide sales in H1 FY2025, but core coil demand fell 14% as consumers shift to incense sticks and electric devices.

Management cites operational challenges to return the category to historical 12–15% CAGR; reviving distribution and SKU rationalization remain key execution gaps.

Limited International Footprint Compared to Peers

Jyothy Labs remains predominantly domestic: international sales were under 2% of revenue in FY2024–25, leaving it exposed to India-only demand and INR volatility.

Limited global diversification prevents capture of higher-growth markets in Africa and Southeast Asia, and curbs currency-hedged revenue streams.

Certain Henkel-acquired brand rights are geographically restricted to India, Bangladesh, and Sri Lanka, blocking wider rollouts.

- International sales <2% of FY2024–25 revenue

Slower Premiumization Pace in Personal Care

While Margo is a respected heritage soap brand, its move into premium personal care and body wash lagged peers, with Jyothy Labs' premium personal care revenue growing about 3% in FY2024 vs. industry peer averages of 8–10%.

GST-driven transitions and price resets in late 2025 caused channel disruption and flat segment growth for that period, shaving an estimated 150–200 bps off category growth.

Shifting from mass soap to full beauty/hygiene requires major brand repositioning, ~₹50–100 crore incremental R&D and marketing annually, and multi-year perception change.

- Heritage strength, weak premium traction

- Late-2025 GST/pricing hit: flat growth

- Needs ₹50–100 crore p.a. R&D/marketing

- Peers growing 8–10% vs Jyothy ~3% (FY2024)

Regional concentration, input-cost pain and lagging premium growth dent Jyothy Labs

Heavy South India dependence (~45% FY2024 revenue; Kerala ~18%) and <2% international sales leave Jyothy Labs exposed to regional shocks and INR risk; Kerala floods cut regional sales ~9–12% in 2024–25. Input-cost swings (crude derivatives, soda ash, palm oil) drove a 210bp gross-margin hit in Q2 FY2026, while insecticide and premium personal-care growth lag peers (Maxo down 6% FY2024; premium +3% vs peers 8–10%).

| Metric | Value |

|---|---|

| South India share FY2024 | ~45% |

| Kerala share FY2024 | ~18% |

| International sales FY2024–25 | <2% |

| Maxo insecticide FY2024 | -6% YoY (~INR 210 cr) |

| Premium personal care FY2024 | +3% (peers 8–10%) |

| Gross-margin impact Q2 FY2026 | -210 bps |

Full Version Awaits

Jyothy Labs SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file available after checkout. Purchase unlocks the complete, in-depth version with actionable insights on Jyothy Labs’ strengths, weaknesses, opportunities, and threats.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Jyothy Labs stands out with strong brand recognition in FMCG and a diversified product portfolio, but faces margin pressure from commodity volatility and stiff competition from larger peers; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis for an investor-ready Word report plus editable Excel tools to plan, pitch, or act with confidence.

Strengths

Dominant Market Leadership in Fabric Whitening

Ujala holds ~84% share of India’s fabric whitener market as of late 2025, giving Jyothy Labs strong pricing power and recurring cash flow—2024–25 EBITDA margin for the consumer segment rose to roughly 18%, funding category expansion.

Robust Debt-Free Balance Sheet and Liquidity

Jyothy Labs enters 2026 net debt-free with cash and liquid investments above 800 crore INR, preserving a clean balance sheet after FY2025 where interest expense was negligible (below 5 crore INR).

Extensive Multi-Channel Distribution Network

Jyothy Labs has a distribution footprint covering over 3.6 million retail outlets, with direct reach to 1.3 million outlets and 9,900+ channel partners, ensuring strong shelf presence across urban modern trade and deep rural markets.

Agile Localized Manufacturing Infrastructure

Operating 23 plants at 14 locations across India lets Jyothy Labs cut logistics costs and meet regional demand quickly; FY2024 revenue from branded FMCG was Rs 2,047 crore, helping localized sales capture.

This decentralized model boosts resilience to supply disruptions, helps state-level tax planning, and keeps inventory fresher near hubs like South India, shortening the working capital cycle (FY2024 DSO improved by ~6 days).

Successful Diversification into Power Brands

Jyothy Labs has scaled Power Brands beyond Ujala—Exo, Maxo, and Margo—each leading their niches and lowering single-product risk.

Exo and Pril together hold roughly 60% value share in India’s dishwash segment (2024 Kantar); Maxo retained top market share (~30% value) in household insecticides in FY2024, boosting group EBITDA and cross-sell reach.

The multi-category footprint captures more of the household wallet across fabric, home, and personal care, supporting steady revenue diversification and margin resilience.

- Exo+Pril ≈ 60% dishwash value share (2024)

- Maxo ≈ 30% insecticide value share (FY2024)

- Reduces single-product dependency; increases cross-sell

- Positive impact on revenue mix and EBITDA stability

Market‑leading FMCG: Ujala dominance, diversified brands, net‑debt free with ₹800cr+ cash

Market-leading Power Brands: Ujala ~84% fabric whitener share (late 2025); Exo+Pril ≈60% dishwash value (2024); Maxo ≈30% insecticide (FY2024), diversifying revenue and margins.

Net debt-free entering 2026 with cash >800 crore INR; FY2024 branded FMCG revenue Rs 2,047 crore; 23 plants, 14 locations; DSO improved ~6 days (FY2024).

| Metric | Value |

|---|---|

| Ujala market share | ~84% (late 2025) |

| Cash & investments | >800 crore INR (2026) |

| FY2024 branded revenue | Rs 2,047 crore |

| Plants / Locations | 23 / 14 |

What is included in the product

Provides a concise SWOT overview of Jyothy Labs, highlighting its strong brand portfolio and distribution reach, internal cost and innovation challenges, market expansion and product diversification opportunities, and external risks from competition and raw material volatility.

Provides a concise Jyothy Labs SWOT snapshot for rapid strategic alignment, making it easy for executives to visualize strengths, weaknesses, opportunities, and threats in presentations and planning sessions.

Weaknesses

Significant Regional Revenue Concentration

Despite national expansion, about 45% of Jyothy Labs' FY2024 revenue came from South India, with Kerala alone contributing ~18%, leaving the firm exposed to regional shocks. The 2024–25 Kerala floods cut regional sales by an estimated 9–12% in affected quarters, highlighting vulnerability to climatic events and local competition. Rebalancing to a pan‑India mix needs sustained marketing spend—likely 150–200 bps of revenue annually—across North and West.

Margin Vulnerability to Raw Material Inflation

The company’s profitability is highly sensitive to crude-derivative, soda ash and palm oil prices, which pressured gross margins in late 2025; input inflation drove a 210-basis-point YoY gross-margin dip in Q2 FY2026.

Operating margins stayed healthy (around mid-teens EBITDA margin in FY2025), but sudden cost spikes cause temporary contractions.

Competitive pressure to raise grammage or cut retail prices to protect volumes in value segments amplifies margin risk.

Underperformance in the Household Insecticides Segment

Maxo-led household insecticides lagged fabric and dishwash growth, with segment revenue shrinking 6% YoY in FY2024 to about INR 210 crore while fabric care rose 12% and dishwash 9%.

New formats—aerosols and rackets—show early traction, contributing ~8% of insecticide sales in H1 FY2025, but core coil demand fell 14% as consumers shift to incense sticks and electric devices.

Management cites operational challenges to return the category to historical 12–15% CAGR; reviving distribution and SKU rationalization remain key execution gaps.

Limited International Footprint Compared to Peers

Jyothy Labs remains predominantly domestic: international sales were under 2% of revenue in FY2024–25, leaving it exposed to India-only demand and INR volatility.

Limited global diversification prevents capture of higher-growth markets in Africa and Southeast Asia, and curbs currency-hedged revenue streams.

Certain Henkel-acquired brand rights are geographically restricted to India, Bangladesh, and Sri Lanka, blocking wider rollouts.

- International sales <2% of FY2024–25 revenue

Slower Premiumization Pace in Personal Care

While Margo is a respected heritage soap brand, its move into premium personal care and body wash lagged peers, with Jyothy Labs' premium personal care revenue growing about 3% in FY2024 vs. industry peer averages of 8–10%.

GST-driven transitions and price resets in late 2025 caused channel disruption and flat segment growth for that period, shaving an estimated 150–200 bps off category growth.

Shifting from mass soap to full beauty/hygiene requires major brand repositioning, ~₹50–100 crore incremental R&D and marketing annually, and multi-year perception change.

- Heritage strength, weak premium traction

- Late-2025 GST/pricing hit: flat growth

- Needs ₹50–100 crore p.a. R&D/marketing

- Peers growing 8–10% vs Jyothy ~3% (FY2024)

Regional concentration, input-cost pain and lagging premium growth dent Jyothy Labs

Heavy South India dependence (~45% FY2024 revenue; Kerala ~18%) and <2% international sales leave Jyothy Labs exposed to regional shocks and INR risk; Kerala floods cut regional sales ~9–12% in 2024–25. Input-cost swings (crude derivatives, soda ash, palm oil) drove a 210bp gross-margin hit in Q2 FY2026, while insecticide and premium personal-care growth lag peers (Maxo down 6% FY2024; premium +3% vs peers 8–10%).

| Metric | Value |

|---|---|

| South India share FY2024 | ~45% |

| Kerala share FY2024 | ~18% |

| International sales FY2024–25 | <2% |

| Maxo insecticide FY2024 | -6% YoY (~INR 210 cr) |

| Premium personal care FY2024 | +3% (peers 8–10%) |

| Gross-margin impact Q2 FY2026 | -210 bps |

Full Version Awaits

Jyothy Labs SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file available after checkout. Purchase unlocks the complete, in-depth version with actionable insights on Jyothy Labs’ strengths, weaknesses, opportunities, and threats.