Kadant Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

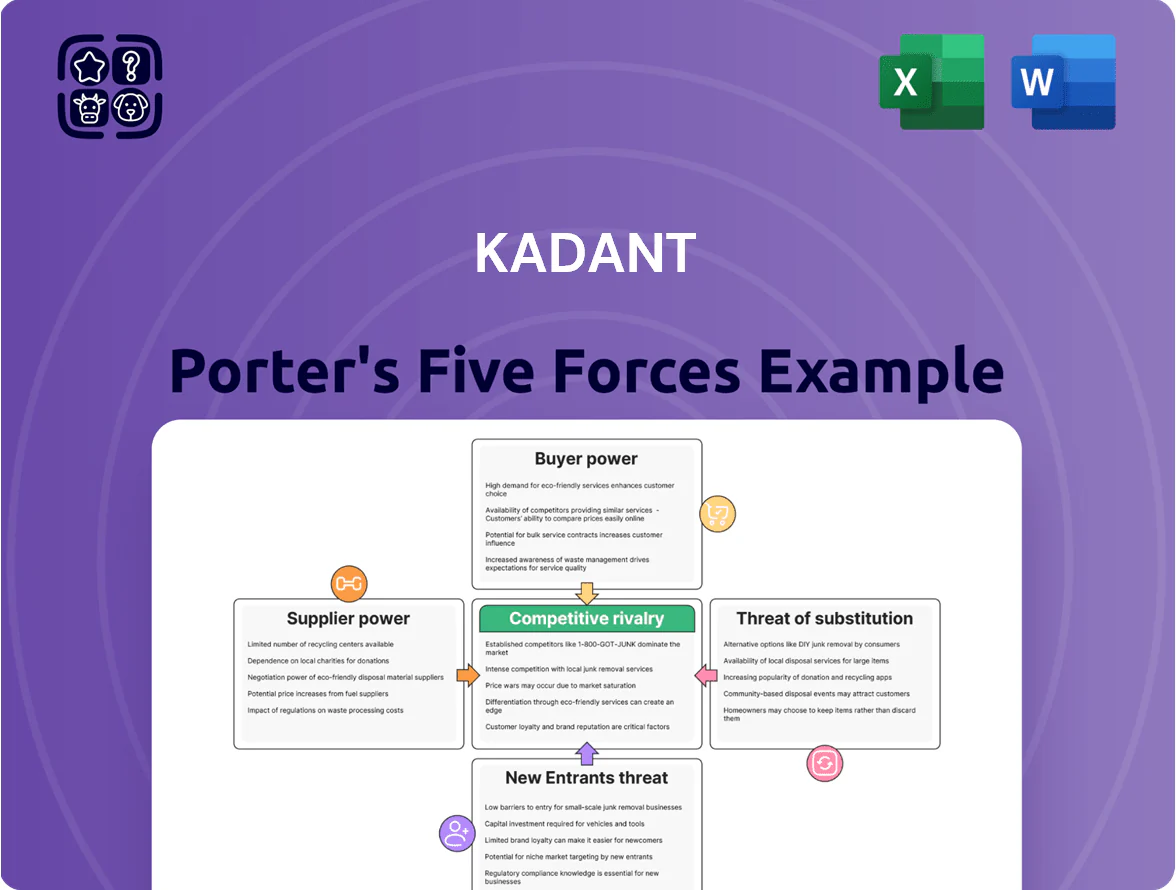

Kadant operates in a niche industrial-processing space where supplier concentration, moderate buyer power, and technological specialization shape competitive intensity—this snapshot highlights key tensions but omits the granular force ratings and strategic levers.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kadant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized raw material requirements

Kadant depends on high-grade stainless steel and specialty nickel alloys for its pulpers and heat exchangers; these inputs account for about 22% of COGS. By end-2025, green-energy demand lifted global stainless orderbooks ~9% YoY, giving metal producers moderate leverage and squeezing spot margins. Kadant offsets risk with multi-year purchase agreements covering ~65% of needs and diversified sourcing across North America, Europe, and Asia to keep plants running.

Dependence on technological component providers

Increasing IoT and smart sensors in fiber processing raise Kadant’s reliance on specialized electronics makers; industrial-grade components carry strict specs and certifications, giving suppliers pricing and delivery leverage—global industrial sensor market was $27.5B in 2024, growing 8.2% CAGR. Kadant counters by modular designs that accept multiple certified brands, cutting single-supplier risk and reducing component cost volatility by an estimated 10–15% in sourcing trials.

Geopolitical influence on supply chains

Kadant sources a large share of raw materials and sub-assemblies internationally, exposing it to trade volatility—about 38% of procurement was from APAC in 2024, increasing supplier risk. By late 2025, regionalized supply chains are standard: Kadant reported shifting 22% of volumes to North America and Europe to reduce disruption from tariffs and logistics bottlenecks. Localized manufacturing has cut single-region supplier leverage, lowering procurement concentration risk.

Energy costs affecting input pricing

Suppliers of heavy industrial components are highly sensitive to energy price swings and typically pass higher costs to equipment makers like Kadant; in 2024 global steel and aluminum energy surcharges averaged 5–8% of metal prices, lifting input costs for forgings and castings.

Through 2025 the carbon-intensive forging/casting cost remains variable—carbon pricing and fossil-fuel volatility added an estimated $20–40/ton to producer margins in 2024—so suppliers can shift price risk downstream.

Kadant mitigates this by selling high-value engineering where material cost is a smaller share of price; premium engineered systems earned ~45% gross margin in 2024, reducing exposure to raw-material swings.

- Energy surcharges ≈5–8% of metal price (2024)

- Carbon/fuel added ~$20–40/ton to costs (2024)

- Kadant premium systems gross margin ≈45% (2024)

Scarcity of skilled fabrication partners

Scarcity of skilled fabrication partners raises supplier power for Kadant because a 2024 ILO report showed a 12% shortfall in skilled manufacturing labor in advanced markets, limiting qualified precision shops.

These specialists command 8–15% price premiums for tight-tolerance work that meets Kadant’s specs, so Kadant keeps close supplier ties and expanded internal capacity—capital capex rose 18% in FY2024 to $42M—to reduce dependence.

- Limited vendor pool: global skilled-labor shortfall ~12% (2024 ILO)

- Price premium: 8–15% on specialized fabrication

- Kadant response: FY2024 capex +18% to $42M

Kadant navigates supplier pressures with reshoring, capex, multi‑year contracts

Kadant faces moderate supplier power: metals (22% COGS) and industrial sensors give vendors leverage; energy surcharges (5–8% of metal price) and carbon costs ($20–40/ton in 2024) amplify this. Kadant offsets risk via 65% multi-year contracts, 22% reshoring to NA/EU, FY2024 capex +18% to $42M, and 45% gross margin on premium systems.

| Metric | Value (2024–25) |

|---|---|

| Metals % of COGS | 22% |

| Energy surcharge | 5–8% |

| Carbon cost add | $20–40/ton |

| Multi-year coverage | 65% |

| Reshoring shift | 22% |

| FY2024 capex | $42M (+18%) |

| Premium systems GM | 45% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Kadant, evaluating supplier and buyer power, substitutes, new entrants, and industry rivalry with strategic commentary and editable findings for reports.

A concise Porter's Five Forces summary tailored for Kadant—quickly reveals competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Concentration of large industrial players

Kadant’s primary customers are a concentrated set of large paper, packaging, and tissue manufacturers—top 10 global pulp and paper firms account for roughly 40% of industry production—giving buyers strong leverage on pricing and multi-year service contracts.

These customers use volume discounts and extended payment terms to pressure capital-equipment suppliers, often negotiating 5–10% lower list prices on big orders.

Still, Kadant’s proprietary, high-efficiency systems support higher gross margins (reported ~33% in FY2024) by offering lifecycle cost savings buyers value, which blunts pure price competition.

High switching costs for integrated systems

Once a Kadant fluid-handling or fiber-processing system is installed it becomes mission-critical to production; customers face average downtime costs of $50,000–$200,000 per day in pulp and paper operations, so replacement carries heavy economic pain. Capital outlay and integration risk—often 6–18 months and $1–10M per line—discourage switching, creating technical lock-in. This lock-in weakens buyer price leverage and supports Kadant’s 20–30% aftermarket margin resilience.

Demand for sustainability and efficiency

By 2025 industrial customers face strict rules to cut water and energy use—EU industrial Emissions Directive updates and US EPA targets push 10–30% reductions in many sectors, raising demand for efficiency tech.

Kadant’s systems improve resource efficiency—company reported 2024 sales mix with >40% of revenue from filtration and heat-recovery products that lower water/energy use—making them critical for compliance and ESG targets.

This strategic fit reduces customer price sensitivity; firms under regulatory fines or investor scrutiny are less likely to pick cheaper, less efficient alternatives that risk noncompliance.

Price sensitivity in cyclical markets

Kadant faces higher customer bargaining power in cyclical paper and packaging markets; during 2020–2023 downturns customers cut capex—US paperboard mill investments fell ~18% in 2023—so buyers delay large purchases and choose suppliers more selectively.

Kadant offsets this by selling aftermarket services and parts that generated about 55% of service revenue in 2024, stabilizing cash flow when new-equipment orders drop.

- Cycle-driven capex cuts raise buyer leverage

- 2023 US paperboard capex down ~18%

- Aftermarket/services ≈55% of Kadant service revenue 2024

- Parts/service provide recurring, less cyclical income

Importance of aftermarket service reliability

Customers prioritize vendors offering rapid maintenance and OEM-quality replacement parts to avoid unplanned outages that can cost pulp and paper mills $10,000–$50,000 per hour in lost production (industry estimates, 2024).

Kadant’s global service network—over 40 field service locations and 200 certified technicians as of 2025—adds recurring revenue and value beyond equipment sale.

That service-led model shifts buyer focus to total cost of ownership, reducing sensitivity to upfront price and weakening pure bargaining power.

- Kadant service footprint: 40+ locations, 200 techs (2025)

- Downtime cost: $10k–$50k/hr (2024 industry)

- Model effect: increases recurring revenue, lowers price-driven bargaining

Kadant: Resilient aftermarket leader—33% margin, 55% service revenue, strong price leverage

Kadant customers are large, concentrated pulp/paper firms (top 10 ≈40% production), giving price leverage; they secure 5–10% discounts and extended terms. Kadant’s FY2024 gross margin ≈33% and >40% revenue from efficiency products, plus 55% service revenue, create switching costs and aftermarket resilience. Service network (40+ locations, 200 techs in 2025) reduces pure price pressure.

| Metric | Value |

|---|---|

| Top-10 share | ≈40% |

| Price concessions | 5–10% |

| Gross margin FY2024 | ≈33% |

| Efficiency revenue | >40% |

| Service rev share 2024 | ≈55% |

| Service footprint 2025 | 40+ locations, 200 techs |

Full Version Awaits

Kadant Porter's Five Forces Analysis

This preview shows the exact Kadant Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Kadant operates in a niche industrial-processing space where supplier concentration, moderate buyer power, and technological specialization shape competitive intensity—this snapshot highlights key tensions but omits the granular force ratings and strategic levers.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kadant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized raw material requirements

Kadant depends on high-grade stainless steel and specialty nickel alloys for its pulpers and heat exchangers; these inputs account for about 22% of COGS. By end-2025, green-energy demand lifted global stainless orderbooks ~9% YoY, giving metal producers moderate leverage and squeezing spot margins. Kadant offsets risk with multi-year purchase agreements covering ~65% of needs and diversified sourcing across North America, Europe, and Asia to keep plants running.

Dependence on technological component providers

Increasing IoT and smart sensors in fiber processing raise Kadant’s reliance on specialized electronics makers; industrial-grade components carry strict specs and certifications, giving suppliers pricing and delivery leverage—global industrial sensor market was $27.5B in 2024, growing 8.2% CAGR. Kadant counters by modular designs that accept multiple certified brands, cutting single-supplier risk and reducing component cost volatility by an estimated 10–15% in sourcing trials.

Geopolitical influence on supply chains

Kadant sources a large share of raw materials and sub-assemblies internationally, exposing it to trade volatility—about 38% of procurement was from APAC in 2024, increasing supplier risk. By late 2025, regionalized supply chains are standard: Kadant reported shifting 22% of volumes to North America and Europe to reduce disruption from tariffs and logistics bottlenecks. Localized manufacturing has cut single-region supplier leverage, lowering procurement concentration risk.

Energy costs affecting input pricing

Suppliers of heavy industrial components are highly sensitive to energy price swings and typically pass higher costs to equipment makers like Kadant; in 2024 global steel and aluminum energy surcharges averaged 5–8% of metal prices, lifting input costs for forgings and castings.

Through 2025 the carbon-intensive forging/casting cost remains variable—carbon pricing and fossil-fuel volatility added an estimated $20–40/ton to producer margins in 2024—so suppliers can shift price risk downstream.

Kadant mitigates this by selling high-value engineering where material cost is a smaller share of price; premium engineered systems earned ~45% gross margin in 2024, reducing exposure to raw-material swings.

- Energy surcharges ≈5–8% of metal price (2024)

- Carbon/fuel added ~$20–40/ton to costs (2024)

- Kadant premium systems gross margin ≈45% (2024)

Scarcity of skilled fabrication partners

Scarcity of skilled fabrication partners raises supplier power for Kadant because a 2024 ILO report showed a 12% shortfall in skilled manufacturing labor in advanced markets, limiting qualified precision shops.

These specialists command 8–15% price premiums for tight-tolerance work that meets Kadant’s specs, so Kadant keeps close supplier ties and expanded internal capacity—capital capex rose 18% in FY2024 to $42M—to reduce dependence.

- Limited vendor pool: global skilled-labor shortfall ~12% (2024 ILO)

- Price premium: 8–15% on specialized fabrication

- Kadant response: FY2024 capex +18% to $42M

Kadant navigates supplier pressures with reshoring, capex, multi‑year contracts

Kadant faces moderate supplier power: metals (22% COGS) and industrial sensors give vendors leverage; energy surcharges (5–8% of metal price) and carbon costs ($20–40/ton in 2024) amplify this. Kadant offsets risk via 65% multi-year contracts, 22% reshoring to NA/EU, FY2024 capex +18% to $42M, and 45% gross margin on premium systems.

| Metric | Value (2024–25) |

|---|---|

| Metals % of COGS | 22% |

| Energy surcharge | 5–8% |

| Carbon cost add | $20–40/ton |

| Multi-year coverage | 65% |

| Reshoring shift | 22% |

| FY2024 capex | $42M (+18%) |

| Premium systems GM | 45% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Kadant, evaluating supplier and buyer power, substitutes, new entrants, and industry rivalry with strategic commentary and editable findings for reports.

A concise Porter's Five Forces summary tailored for Kadant—quickly reveals competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Concentration of large industrial players

Kadant’s primary customers are a concentrated set of large paper, packaging, and tissue manufacturers—top 10 global pulp and paper firms account for roughly 40% of industry production—giving buyers strong leverage on pricing and multi-year service contracts.

These customers use volume discounts and extended payment terms to pressure capital-equipment suppliers, often negotiating 5–10% lower list prices on big orders.

Still, Kadant’s proprietary, high-efficiency systems support higher gross margins (reported ~33% in FY2024) by offering lifecycle cost savings buyers value, which blunts pure price competition.

High switching costs for integrated systems

Once a Kadant fluid-handling or fiber-processing system is installed it becomes mission-critical to production; customers face average downtime costs of $50,000–$200,000 per day in pulp and paper operations, so replacement carries heavy economic pain. Capital outlay and integration risk—often 6–18 months and $1–10M per line—discourage switching, creating technical lock-in. This lock-in weakens buyer price leverage and supports Kadant’s 20–30% aftermarket margin resilience.

Demand for sustainability and efficiency

By 2025 industrial customers face strict rules to cut water and energy use—EU industrial Emissions Directive updates and US EPA targets push 10–30% reductions in many sectors, raising demand for efficiency tech.

Kadant’s systems improve resource efficiency—company reported 2024 sales mix with >40% of revenue from filtration and heat-recovery products that lower water/energy use—making them critical for compliance and ESG targets.

This strategic fit reduces customer price sensitivity; firms under regulatory fines or investor scrutiny are less likely to pick cheaper, less efficient alternatives that risk noncompliance.

Price sensitivity in cyclical markets

Kadant faces higher customer bargaining power in cyclical paper and packaging markets; during 2020–2023 downturns customers cut capex—US paperboard mill investments fell ~18% in 2023—so buyers delay large purchases and choose suppliers more selectively.

Kadant offsets this by selling aftermarket services and parts that generated about 55% of service revenue in 2024, stabilizing cash flow when new-equipment orders drop.

- Cycle-driven capex cuts raise buyer leverage

- 2023 US paperboard capex down ~18%

- Aftermarket/services ≈55% of Kadant service revenue 2024

- Parts/service provide recurring, less cyclical income

Importance of aftermarket service reliability

Customers prioritize vendors offering rapid maintenance and OEM-quality replacement parts to avoid unplanned outages that can cost pulp and paper mills $10,000–$50,000 per hour in lost production (industry estimates, 2024).

Kadant’s global service network—over 40 field service locations and 200 certified technicians as of 2025—adds recurring revenue and value beyond equipment sale.

That service-led model shifts buyer focus to total cost of ownership, reducing sensitivity to upfront price and weakening pure bargaining power.

- Kadant service footprint: 40+ locations, 200 techs (2025)

- Downtime cost: $10k–$50k/hr (2024 industry)

- Model effect: increases recurring revenue, lowers price-driven bargaining

Kadant: Resilient aftermarket leader—33% margin, 55% service revenue, strong price leverage

Kadant customers are large, concentrated pulp/paper firms (top 10 ≈40% production), giving price leverage; they secure 5–10% discounts and extended terms. Kadant’s FY2024 gross margin ≈33% and >40% revenue from efficiency products, plus 55% service revenue, create switching costs and aftermarket resilience. Service network (40+ locations, 200 techs in 2025) reduces pure price pressure.

| Metric | Value |

|---|---|

| Top-10 share | ≈40% |

| Price concessions | 5–10% |

| Gross margin FY2024 | ≈33% |

| Efficiency revenue | >40% |

| Service rev share 2024 | ≈55% |

| Service footprint 2025 | 40+ locations, 200 techs |

Full Version Awaits

Kadant Porter's Five Forces Analysis

This preview shows the exact Kadant Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.