Kagome Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Kagome faces moderate supplier power due to specialized tomato sourcing, steady buyer power from diverse retail channels, and manageable threats from substitutes and new entrants driven by brand loyalty and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kagome’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Tomato Paste Volatility

Kagome depends on global tomato paste markets, sourcing ~40% of paste from China and Europe; price swings hit COGS when regional FOB prices rose 28% in 2024 and spot prices spiked another 17% by Q3 2025.

Climate-driven crop failures in 2024–2025 raised supplier leverage, contributing to a 12% year-on-year raw-material cost increase for Kagome by FY2025.

Kagome limits exposure via diversified sourcing across six countries and multi-year contracts covering ~60% of volumes, but residual commodity risk keeps supplier power high.

Vertical Integration and Seed Control

Kagome reduces supplier power by owning over 1,200 proprietary tomato lines and supplying licensed seeds to roughly 3,500 contracted Japanese growers, making many farms dependent on its high-lycopene, high-yield varieties.

This seed control turns genetic IP into leverage: growers face switching costs and yield risks, cutting their bargaining leverage and stabilizing Kagome’s raw supply and margins.

Climate Change and Agricultural Risk

Increasing extreme weather in Japan and globally has cut high-quality vegetable yields—Japan saw a 12% drop in some vegetable crops after 2018–2023 floods—so suppliers in stable regions are charging premiums for organic and non-GMO inputs through 2025. Suppliers with resilient production can demand 5–15% higher prices as buyers compete for scarce raw materials. Kagome’s smart-agriculture capex (~¥10bn by 2024) cushions its own supply but does not fully offset the macro upward pressure on supplier bargaining power.

Logistics and Packaging Costs

Suppliers of aluminum, plastic, and paper packaging exert strong bargaining power in 2025 as energy-driven input costs rose ~18% YoY and strict EU/Japan recycling rules raised compliance costs by ~12% per unit, making many costs non-negotiable and forcing Kagome to absorb or pass increases to price-sensitive consumers.

The move to biodegradable packaging boosts niche eco-supplier power; proprietary biopolymer tech raised supplier margins 20–30%, limiting Kagome’s sourcing options and raising capex for switching.

- Energy-linked input costs +18% YoY (2025)

- Regulatory compliance adds ~12% per-unit cost

- Eco-material suppliers' margins +20–30%

- Passing costs risks volume drop among price-sensitive consumers

Labor Shortages in Domestic Farming

The aging population in Japan cut the farm labor pool by about 20% between 2010–2020, raising domestic harvesting costs; Kagome faces rising supplier leverage as manual wages and one-time automation costs (harvest robots ≈ ¥30–¥80 million per unit) climb.

Kagome must subsidize capital for cooperatives and offer premium contracts—recently paying ~10–15% above market rates—to secure reliable tomato and vegetable supply.

- Japan farm labor down ~20% (2010–2020)

- Harvest robots cost ¥30–¥80M each

- Kagome paying ~10–15% premium to partners

Kagome offsets surging tomato costs with contracts, smart‑agri capex and grower premiums

Suppliers exert high bargaining power: commodity tomato paste drove COGS up 12% FY2025 after 28% FOB rise (2024) +17% spot (Q3 2025); packaging and energy added ~18% YoY and ~12% regulatory cost; eco-material margins +20–30%; Kagome offsets via 60% multi‑year contracts, 1,200 seed lines, ¥10bn smart‑agri capex and 10–15% premiums to growers.

| Metric | Value |

|---|---|

| Tomato paste share | ~40% |

| Raw material cost rise | +12% FY2025 |

| Energy/input rise | +18% YoY (2025) |

| Smart‑agri capex | ¥10bn (2024) |

What is included in the product

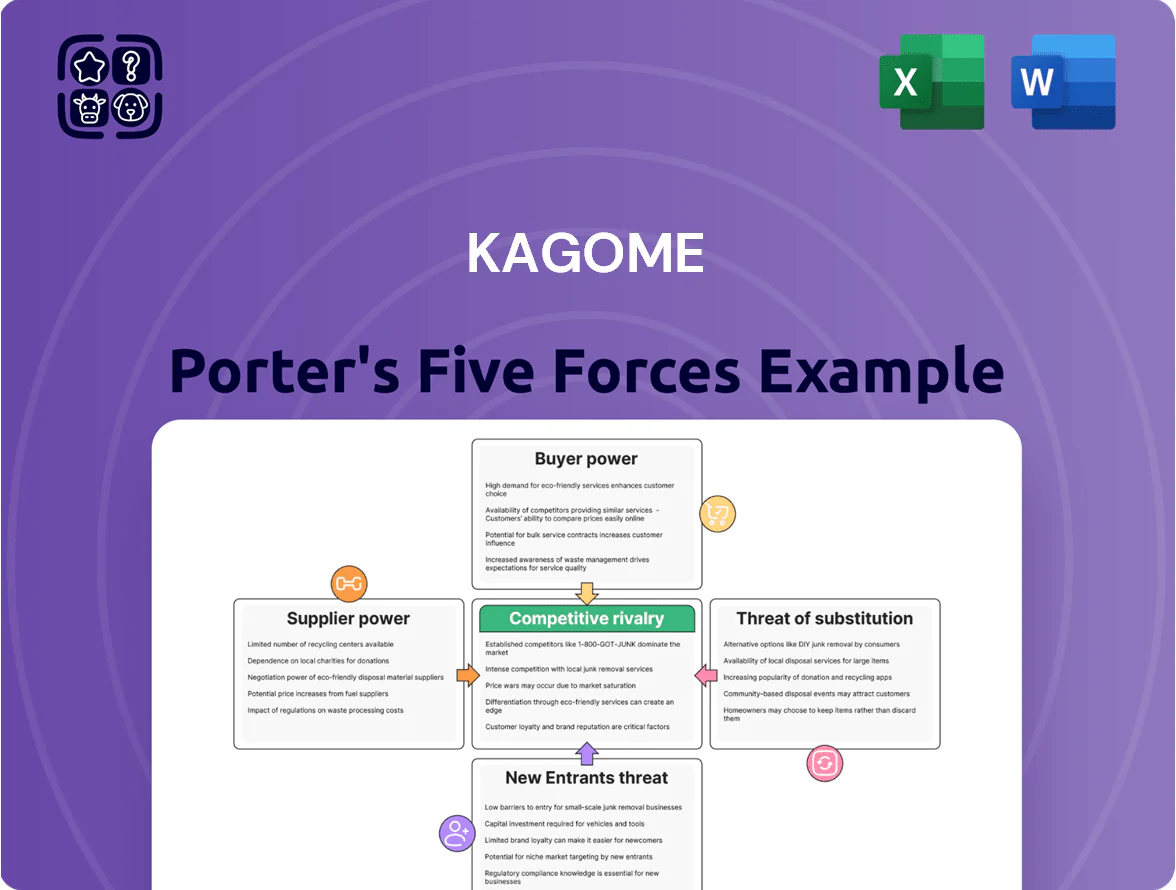

Tailored Porter's Five Forces for Kagome: examines competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers affecting Kagome’s pricing, margins, and market resilience.

A concise, one-sheet Kagome Porter’s Five Forces summary that visualizes competitive pressure and relief options—ideal for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

Retail Giant Dominance

Proliferation of Private Brands

Supermarkets’ private-label tomato products and vegetable juices, now 15–30% cheaper than Kagome’s premium lines, erode brand loyalty as 42% of Japanese shoppers cited price over brand for basic cooking items in 2024; this raises customer bargaining power by making switching a simple cost decision. Kagome must thus boost measurable functional benefits—like 20% higher lycopene content or added probiotics—to defend premium pricing and retain margin.

Low Switching Costs for Consumers

Individual shoppers face virtually no financial or psychological cost switching from Kagome ketchup or juice to rivals, so demand is highly elastic; NielsenIQ data for 2024–2025 shows private-label share in Japan's condiments rose to 18.7%, signaling easy defections.

Kagome must protect brand equity and flavor consistency; a Kantar 2025 survey found 62% of households cite taste and 58% cite price as top purchase drivers.

Growth of Digital Comparison Shopping

The rise of online grocery platforms and mobile apps lets consumers compare prices and nutrition across brands in seconds, cutting information asymmetry that favored big brands.

Even though Kagome sells direct, digital transparency (price comparison, barcode scanners) empowers buyers to hunt deals; global online grocery sales reached about $1.3 trillion in 2024, boosting shopper leverage.

Retail transparency pressures margins and forces clearer value propositions and promo tactics.

- Online grocery sales $1.3T (2024)

- Comparison apps reduce search time to seconds

- Direct channels help Kagome but don’t stop price transparency

Health-Conscious Demand Shifts

- 72% avoid preservatives (FMI 2024)

- lycopene claims lift tomato product premiums ~5–8%

- Kagome lost 1.8% volume in 2023 vs niche double-digit gains

Kagome under pressure: retailers, private‑labels and online sales force price proofing

| Metric | Value |

|---|---|

| Top retailers share | ~45% (2024) |

| Promotion margin hit | 2–4 ppt |

| Private-label price gap | 15–30% |

| Private-label condiment share | 18.7% (2024) |

| Online grocery sales | $1.3T (2024) |

| Taste vs price | 62% / 58% (Kantar 2025) |

What You See Is What You Get

Kagome Porter's Five Forces Analysis

This preview shows the exact Kagome Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The file is the final, professionally formatted document, ready for download and instant use the moment you buy. What you see here is precisely what will be delivered, fully complete and usable for your analysis or presentation needs.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kagome faces moderate supplier power due to specialized tomato sourcing, steady buyer power from diverse retail channels, and manageable threats from substitutes and new entrants driven by brand loyalty and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kagome’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Tomato Paste Volatility

Kagome depends on global tomato paste markets, sourcing ~40% of paste from China and Europe; price swings hit COGS when regional FOB prices rose 28% in 2024 and spot prices spiked another 17% by Q3 2025.

Climate-driven crop failures in 2024–2025 raised supplier leverage, contributing to a 12% year-on-year raw-material cost increase for Kagome by FY2025.

Kagome limits exposure via diversified sourcing across six countries and multi-year contracts covering ~60% of volumes, but residual commodity risk keeps supplier power high.

Vertical Integration and Seed Control

Kagome reduces supplier power by owning over 1,200 proprietary tomato lines and supplying licensed seeds to roughly 3,500 contracted Japanese growers, making many farms dependent on its high-lycopene, high-yield varieties.

This seed control turns genetic IP into leverage: growers face switching costs and yield risks, cutting their bargaining leverage and stabilizing Kagome’s raw supply and margins.

Climate Change and Agricultural Risk

Increasing extreme weather in Japan and globally has cut high-quality vegetable yields—Japan saw a 12% drop in some vegetable crops after 2018–2023 floods—so suppliers in stable regions are charging premiums for organic and non-GMO inputs through 2025. Suppliers with resilient production can demand 5–15% higher prices as buyers compete for scarce raw materials. Kagome’s smart-agriculture capex (~¥10bn by 2024) cushions its own supply but does not fully offset the macro upward pressure on supplier bargaining power.

Logistics and Packaging Costs

Suppliers of aluminum, plastic, and paper packaging exert strong bargaining power in 2025 as energy-driven input costs rose ~18% YoY and strict EU/Japan recycling rules raised compliance costs by ~12% per unit, making many costs non-negotiable and forcing Kagome to absorb or pass increases to price-sensitive consumers.

The move to biodegradable packaging boosts niche eco-supplier power; proprietary biopolymer tech raised supplier margins 20–30%, limiting Kagome’s sourcing options and raising capex for switching.

- Energy-linked input costs +18% YoY (2025)

- Regulatory compliance adds ~12% per-unit cost

- Eco-material suppliers' margins +20–30%

- Passing costs risks volume drop among price-sensitive consumers

Labor Shortages in Domestic Farming

The aging population in Japan cut the farm labor pool by about 20% between 2010–2020, raising domestic harvesting costs; Kagome faces rising supplier leverage as manual wages and one-time automation costs (harvest robots ≈ ¥30–¥80 million per unit) climb.

Kagome must subsidize capital for cooperatives and offer premium contracts—recently paying ~10–15% above market rates—to secure reliable tomato and vegetable supply.

- Japan farm labor down ~20% (2010–2020)

- Harvest robots cost ¥30–¥80M each

- Kagome paying ~10–15% premium to partners

Kagome offsets surging tomato costs with contracts, smart‑agri capex and grower premiums

Suppliers exert high bargaining power: commodity tomato paste drove COGS up 12% FY2025 after 28% FOB rise (2024) +17% spot (Q3 2025); packaging and energy added ~18% YoY and ~12% regulatory cost; eco-material margins +20–30%; Kagome offsets via 60% multi‑year contracts, 1,200 seed lines, ¥10bn smart‑agri capex and 10–15% premiums to growers.

| Metric | Value |

|---|---|

| Tomato paste share | ~40% |

| Raw material cost rise | +12% FY2025 |

| Energy/input rise | +18% YoY (2025) |

| Smart‑agri capex | ¥10bn (2024) |

What is included in the product

Tailored Porter's Five Forces for Kagome: examines competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers affecting Kagome’s pricing, margins, and market resilience.

A concise, one-sheet Kagome Porter’s Five Forces summary that visualizes competitive pressure and relief options—ideal for quick strategic decisions and slide-ready presentations.

Customers Bargaining Power

Retail Giant Dominance

Proliferation of Private Brands

Supermarkets’ private-label tomato products and vegetable juices, now 15–30% cheaper than Kagome’s premium lines, erode brand loyalty as 42% of Japanese shoppers cited price over brand for basic cooking items in 2024; this raises customer bargaining power by making switching a simple cost decision. Kagome must thus boost measurable functional benefits—like 20% higher lycopene content or added probiotics—to defend premium pricing and retain margin.

Low Switching Costs for Consumers

Individual shoppers face virtually no financial or psychological cost switching from Kagome ketchup or juice to rivals, so demand is highly elastic; NielsenIQ data for 2024–2025 shows private-label share in Japan's condiments rose to 18.7%, signaling easy defections.

Kagome must protect brand equity and flavor consistency; a Kantar 2025 survey found 62% of households cite taste and 58% cite price as top purchase drivers.

Growth of Digital Comparison Shopping

The rise of online grocery platforms and mobile apps lets consumers compare prices and nutrition across brands in seconds, cutting information asymmetry that favored big brands.

Even though Kagome sells direct, digital transparency (price comparison, barcode scanners) empowers buyers to hunt deals; global online grocery sales reached about $1.3 trillion in 2024, boosting shopper leverage.

Retail transparency pressures margins and forces clearer value propositions and promo tactics.

- Online grocery sales $1.3T (2024)

- Comparison apps reduce search time to seconds

- Direct channels help Kagome but don’t stop price transparency

Health-Conscious Demand Shifts

- 72% avoid preservatives (FMI 2024)

- lycopene claims lift tomato product premiums ~5–8%

- Kagome lost 1.8% volume in 2023 vs niche double-digit gains

Kagome under pressure: retailers, private‑labels and online sales force price proofing

| Metric | Value |

|---|---|

| Top retailers share | ~45% (2024) |

| Promotion margin hit | 2–4 ppt |

| Private-label price gap | 15–30% |

| Private-label condiment share | 18.7% (2024) |

| Online grocery sales | $1.3T (2024) |

| Taste vs price | 62% / 58% (Kantar 2025) |

What You See Is What You Get

Kagome Porter's Five Forces Analysis

This preview shows the exact Kagome Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups. The file is the final, professionally formatted document, ready for download and instant use the moment you buy. What you see here is precisely what will be delivered, fully complete and usable for your analysis or presentation needs.