Kalpataru Projects International Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

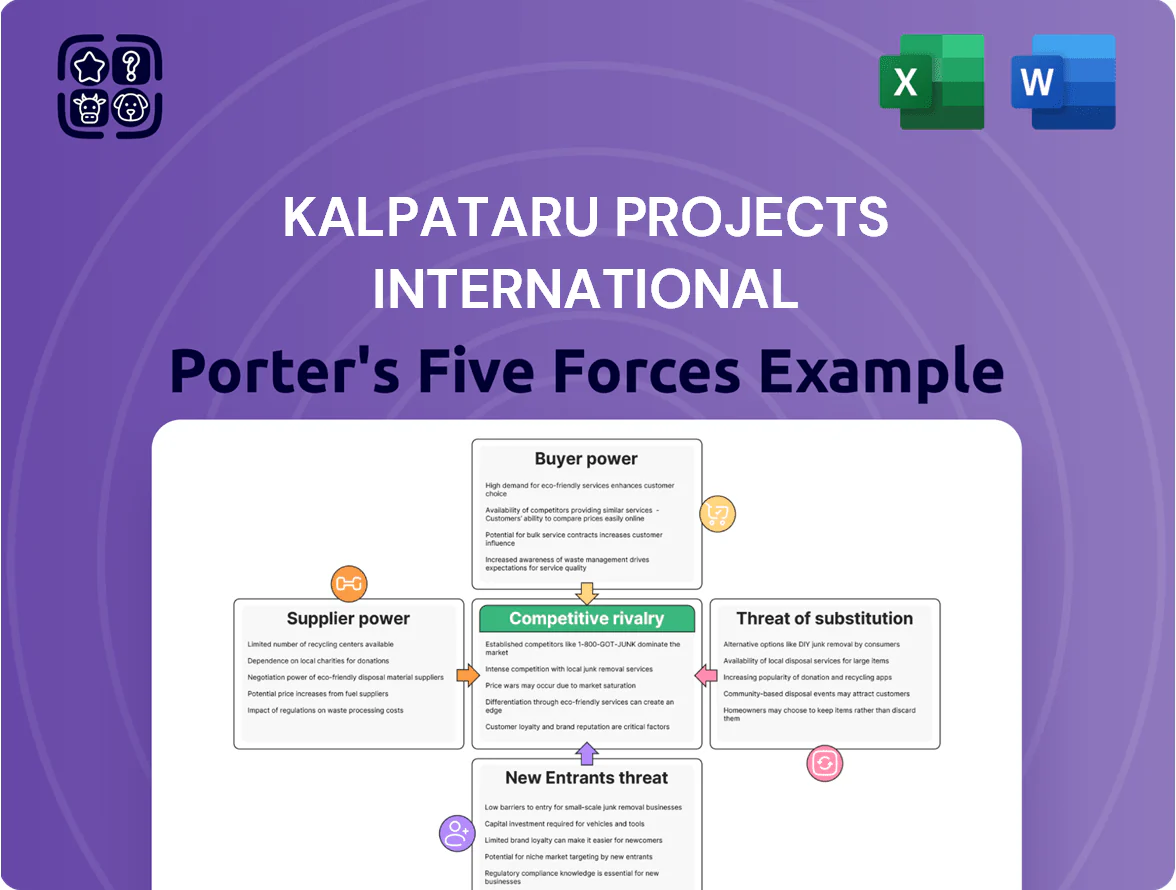

Kalpataru Projects International faces moderate supplier power and elevated buyer bargaining as project scale and price sensitivity shape margins, while rivalry is intensified by regional EPC competitors and project cyclicality.

Suppliers Bargaining Power

Volatility in Commodity Pricing

Procurement of steel, aluminum and zinc makes up roughly 18–25% of Kalpataru Projects International Limited’s (KPIL) project costs; global commodity markets set prices, giving suppliers leverage when supply tightens or demand spikes.

KPIL uses strategic sourcing, multi-vendor contracts and price variation clauses; still, 2021–2024 steel price volatility (steel HRC up ~45% peak-to-trough) shows sudden spikes can cut short-term EBITDA by several percentage points.

Dependence on Specialized Equipment Providers

KPIL depends on sophisticated machinery—HV transformers, OPGW fiber, and EHV switchgear—sourced from a handful of global makers; roughly 70–80% of such equipment meeting IEC/ASTM standards comes from top 5 suppliers worldwide, concentrating supply risk.

This vendor concentration lets suppliers influence prices and lead times: in 2024 global lead times for EHV transformers averaged 28–40 weeks, pushing KPIL to accept price escalations of 6–10% on large contracts.

Availability of Skilled Labor and Subcontractors

The execution of complex EPC projects across diverse geographies requires highly skilled engineers and reliable local subcontractors; in India and the Middle East KPIL operates, demand for civil and MEP engineers rose ~8–12% y/y in 2024, tightening supply. In boom regions like India—where infrastructure capex jumped to $150B in FY2024—labor unions and niche service providers gain bargaining leverage. KPIL must pay competitive wages, invest in training, and secure long-term subcontractor ties to avoid schedule slippage and cost overruns. Maintaining these relationships preserves project continuity and quality under rising wage pressure.

Logistical and Supply Chain Constraints

Global logistics providers move Kalpataru Projects International's heavy equipment across borders, and in 2024 average global container freight rates rose 18% year-on-year, raising landed costs for heavy projects.

Availability of specialized vessels and containers gives logistics firms leverage; limited capacity during 2023–24 port congestions increased lead times by 10–25%, forcing higher inventory and contingency spending.

Any service disruption—strikes, Suez delays, or blank sailings—can delay projects and push overheads; Kalpataru faces measurable margin pressure when freight spikes exceed 5–7% of project budgets.

- Freight rates +18% in 2024

- Lead times up 10–25% during 2023–24 congestion

- Freight spikes >5–7% hit project margins

Energy and Fuel Cost Sensitivity

Energy and fuel price swings materially impact KPIL because heavy machinery and transport are energy-intensive; global Brent crude rose ~43% from Jan 2023 to Dec 2024, pushing diesel costs for Indian contractors up ~35% in 2024, raising operating margins pressure.

Suppliers set pricing that ripples across the value chain; KPIL stays exposed on fixed-price projects where fuel escalation clauses are limited or absent.

- Brent +43% (Jan 2023–Dec 2024)

- Diesel cost to contractors +35% in 2024

- Fixed-price contract exposure increases margin risk

Supply squeeze: concentrated EHV vendors, long lead times and rising freight eat EPC margins

Suppliers wield moderate-to-high power: raw materials (18–25% of costs), concentrated EHV equipment supply (70–80% from top 5), long lead times (28–40 weeks) and logistics/fuel shocks (freight +18% 2024; Brent +43% 2023–24) squeeze margins on fixed-price EPCs; KPIL relies on multi-vendor sourcing, price clauses, training and long-term subcontractor ties to mitigate risk.

| Metric | Value |

|---|---|

| Materials % of cost | 18–25% |

| Top-5 equipment share | 70–80% |

| EHV lead time | 28–40 wks |

| Freight 2024 | +18% |

| Brent 2023–24 | +43% |

What is included in the product

Tailored exclusively for Kalpataru Projects International, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Kalpataru Projects International—quickly identify competitive pressures and strategic levers to relieve pain points in bidding, supplier negotiations, and market expansion.

Customers Bargaining Power

Concentration of Government and PSU Clients

A large majority of Kalpataru Projects International Limited’s (KPIL) FY2024 revenue—about 72% of INR 4,120 crore consolidated revenue—came from government utilities, railways, and PSUs, concentrating buyer power.

These institutional clients use standardized public tenders and typically set stringent contract clauses, fixed payment cycles (often 60–120 days) and strict performance benchmarks, squeezing contractor margins.

Competitive Bidding and Price Transparency

The rise of e-tendering and reverse auctions has increased price transparency; EPC clients now compare bids in real time, pushing Kalpataru Projects International Limited (KPIL) to cut margins to win work.

In 2024, public-sector utilities ran >60% of large EPC tenders via e-platforms, lowering award-price dispersion by ~12%, so customers demand more scope and lower rates from KPIL.

Stringent Quality and Timeline Requirements

Infrastructure clients levy steep liquidated damages—often 0.1–0.5% of contract value per week—so KPIL faces real cash risk: on a typical three-year EPC contract worth $200m this can be $200k–$1m weekly; clients also insist on extended testing and commissioning windows due to national-critical status, boosting QA capex and O&M staffing; KPIL must therefore allocate higher upfront QA spend and contingency to avoid penalties and preserve margins.

Low Switching Costs at the Bidding Stage

Customers face low switching costs during the bidding phase, able to shift between established EPC contractors like Kalpataru Projects International based on price and technical scores; industry tender analysis shows 60–70% of large infrastructure contracts awarded on lowest-cost technical-compliant bids in India in 2024.

This bidding flexibility lets buyers pit competitors for better margins and payment terms, often driving down contractor bid premiums by 2–5 percentage points versus historical averages, squeezing profitability before construction risks lock in.

Global Market Diversification Benefits Customers

As Kalpataru Projects International (KPIL) grows overseas, customers leverage local-content rules and partnership mandates—seen in 2024 where 18% of Gulf tenders required local JV partners—to force KPIL to hire locally and transfer tech.

Clients extract extra socio-economic value: in 2023 KPIL projects in Africa reported 12–20% local procurement, boosting jobs and skills while squeezing margins.

- Local-content mandates rise 10–25% across target markets (2022–24)

- KPIL local procurement in recent projects: 12–20% (2023)

- Customer leverage increases capex for tech transfer and training

Govt-led tenders drive 72% of KPIL revenue, e-auctions squeeze margins and raise QA costs

Buyers (govt, utilities, PSUs) drive 72% of KPIL’s FY2024 INR 4,120 crore revenue, use e-tenders/reverse auctions (60%+ of large tenders in 2024) to force 2–5ppt lower bid premiums, impose 60–120 day payments and 0.1–0.5%/week liquidated damages; low switching costs and local-content mandates (18% Gulf tenders, KPIL 12–20% local procurement) raise QA capex and margin pressure.

| Metric | Value |

|---|---|

| FY2024 revenue share | 72% |

| Consolidated revenue | INR 4,120 crore |

| Tenders via e-platforms | >60% |

| Bid premium compression | 2–5 ppt |

| Payment terms | 60–120 days |

| LDs | 0.1–0.5%/week |

| Local-content Gulf | 18% |

| KPIL local procurement | 12–20% |

Full Version Awaits

Kalpataru Projects International Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Kalpataru Projects International you'll receive after purchase—no samples or placeholders, fully formatted and ready for immediate use.

You're viewing the actual document that will be available for instant download upon payment, containing detailed competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry assessments.

The file shown is the complete, professionally written deliverable—use it as-is for strategy, investment, or presentation needs without any additional setup.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kalpataru Projects International faces moderate supplier power and elevated buyer bargaining as project scale and price sensitivity shape margins, while rivalry is intensified by regional EPC competitors and project cyclicality.

Suppliers Bargaining Power

Volatility in Commodity Pricing

Procurement of steel, aluminum and zinc makes up roughly 18–25% of Kalpataru Projects International Limited’s (KPIL) project costs; global commodity markets set prices, giving suppliers leverage when supply tightens or demand spikes.

KPIL uses strategic sourcing, multi-vendor contracts and price variation clauses; still, 2021–2024 steel price volatility (steel HRC up ~45% peak-to-trough) shows sudden spikes can cut short-term EBITDA by several percentage points.

Dependence on Specialized Equipment Providers

KPIL depends on sophisticated machinery—HV transformers, OPGW fiber, and EHV switchgear—sourced from a handful of global makers; roughly 70–80% of such equipment meeting IEC/ASTM standards comes from top 5 suppliers worldwide, concentrating supply risk.

This vendor concentration lets suppliers influence prices and lead times: in 2024 global lead times for EHV transformers averaged 28–40 weeks, pushing KPIL to accept price escalations of 6–10% on large contracts.

Availability of Skilled Labor and Subcontractors

The execution of complex EPC projects across diverse geographies requires highly skilled engineers and reliable local subcontractors; in India and the Middle East KPIL operates, demand for civil and MEP engineers rose ~8–12% y/y in 2024, tightening supply. In boom regions like India—where infrastructure capex jumped to $150B in FY2024—labor unions and niche service providers gain bargaining leverage. KPIL must pay competitive wages, invest in training, and secure long-term subcontractor ties to avoid schedule slippage and cost overruns. Maintaining these relationships preserves project continuity and quality under rising wage pressure.

Logistical and Supply Chain Constraints

Global logistics providers move Kalpataru Projects International's heavy equipment across borders, and in 2024 average global container freight rates rose 18% year-on-year, raising landed costs for heavy projects.

Availability of specialized vessels and containers gives logistics firms leverage; limited capacity during 2023–24 port congestions increased lead times by 10–25%, forcing higher inventory and contingency spending.

Any service disruption—strikes, Suez delays, or blank sailings—can delay projects and push overheads; Kalpataru faces measurable margin pressure when freight spikes exceed 5–7% of project budgets.

- Freight rates +18% in 2024

- Lead times up 10–25% during 2023–24 congestion

- Freight spikes >5–7% hit project margins

Energy and Fuel Cost Sensitivity

Energy and fuel price swings materially impact KPIL because heavy machinery and transport are energy-intensive; global Brent crude rose ~43% from Jan 2023 to Dec 2024, pushing diesel costs for Indian contractors up ~35% in 2024, raising operating margins pressure.

Suppliers set pricing that ripples across the value chain; KPIL stays exposed on fixed-price projects where fuel escalation clauses are limited or absent.

- Brent +43% (Jan 2023–Dec 2024)

- Diesel cost to contractors +35% in 2024

- Fixed-price contract exposure increases margin risk

Supply squeeze: concentrated EHV vendors, long lead times and rising freight eat EPC margins

Suppliers wield moderate-to-high power: raw materials (18–25% of costs), concentrated EHV equipment supply (70–80% from top 5), long lead times (28–40 weeks) and logistics/fuel shocks (freight +18% 2024; Brent +43% 2023–24) squeeze margins on fixed-price EPCs; KPIL relies on multi-vendor sourcing, price clauses, training and long-term subcontractor ties to mitigate risk.

| Metric | Value |

|---|---|

| Materials % of cost | 18–25% |

| Top-5 equipment share | 70–80% |

| EHV lead time | 28–40 wks |

| Freight 2024 | +18% |

| Brent 2023–24 | +43% |

What is included in the product

Tailored exclusively for Kalpataru Projects International, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Kalpataru Projects International—quickly identify competitive pressures and strategic levers to relieve pain points in bidding, supplier negotiations, and market expansion.

Customers Bargaining Power

Concentration of Government and PSU Clients

A large majority of Kalpataru Projects International Limited’s (KPIL) FY2024 revenue—about 72% of INR 4,120 crore consolidated revenue—came from government utilities, railways, and PSUs, concentrating buyer power.

These institutional clients use standardized public tenders and typically set stringent contract clauses, fixed payment cycles (often 60–120 days) and strict performance benchmarks, squeezing contractor margins.

Competitive Bidding and Price Transparency

The rise of e-tendering and reverse auctions has increased price transparency; EPC clients now compare bids in real time, pushing Kalpataru Projects International Limited (KPIL) to cut margins to win work.

In 2024, public-sector utilities ran >60% of large EPC tenders via e-platforms, lowering award-price dispersion by ~12%, so customers demand more scope and lower rates from KPIL.

Stringent Quality and Timeline Requirements

Infrastructure clients levy steep liquidated damages—often 0.1–0.5% of contract value per week—so KPIL faces real cash risk: on a typical three-year EPC contract worth $200m this can be $200k–$1m weekly; clients also insist on extended testing and commissioning windows due to national-critical status, boosting QA capex and O&M staffing; KPIL must therefore allocate higher upfront QA spend and contingency to avoid penalties and preserve margins.

Low Switching Costs at the Bidding Stage

Customers face low switching costs during the bidding phase, able to shift between established EPC contractors like Kalpataru Projects International based on price and technical scores; industry tender analysis shows 60–70% of large infrastructure contracts awarded on lowest-cost technical-compliant bids in India in 2024.

This bidding flexibility lets buyers pit competitors for better margins and payment terms, often driving down contractor bid premiums by 2–5 percentage points versus historical averages, squeezing profitability before construction risks lock in.

Global Market Diversification Benefits Customers

As Kalpataru Projects International (KPIL) grows overseas, customers leverage local-content rules and partnership mandates—seen in 2024 where 18% of Gulf tenders required local JV partners—to force KPIL to hire locally and transfer tech.

Clients extract extra socio-economic value: in 2023 KPIL projects in Africa reported 12–20% local procurement, boosting jobs and skills while squeezing margins.

- Local-content mandates rise 10–25% across target markets (2022–24)

- KPIL local procurement in recent projects: 12–20% (2023)

- Customer leverage increases capex for tech transfer and training

Govt-led tenders drive 72% of KPIL revenue, e-auctions squeeze margins and raise QA costs

Buyers (govt, utilities, PSUs) drive 72% of KPIL’s FY2024 INR 4,120 crore revenue, use e-tenders/reverse auctions (60%+ of large tenders in 2024) to force 2–5ppt lower bid premiums, impose 60–120 day payments and 0.1–0.5%/week liquidated damages; low switching costs and local-content mandates (18% Gulf tenders, KPIL 12–20% local procurement) raise QA capex and margin pressure.

| Metric | Value |

|---|---|

| FY2024 revenue share | 72% |

| Consolidated revenue | INR 4,120 crore |

| Tenders via e-platforms | >60% |

| Bid premium compression | 2–5 ppt |

| Payment terms | 60–120 days |

| LDs | 0.1–0.5%/week |

| Local-content Gulf | 18% |

| KPIL local procurement | 12–20% |

Full Version Awaits

Kalpataru Projects International Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Kalpataru Projects International you'll receive after purchase—no samples or placeholders, fully formatted and ready for immediate use.

You're viewing the actual document that will be available for instant download upon payment, containing detailed competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry assessments.

The file shown is the complete, professionally written deliverable—use it as-is for strategy, investment, or presentation needs without any additional setup.