Kansai Paint Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

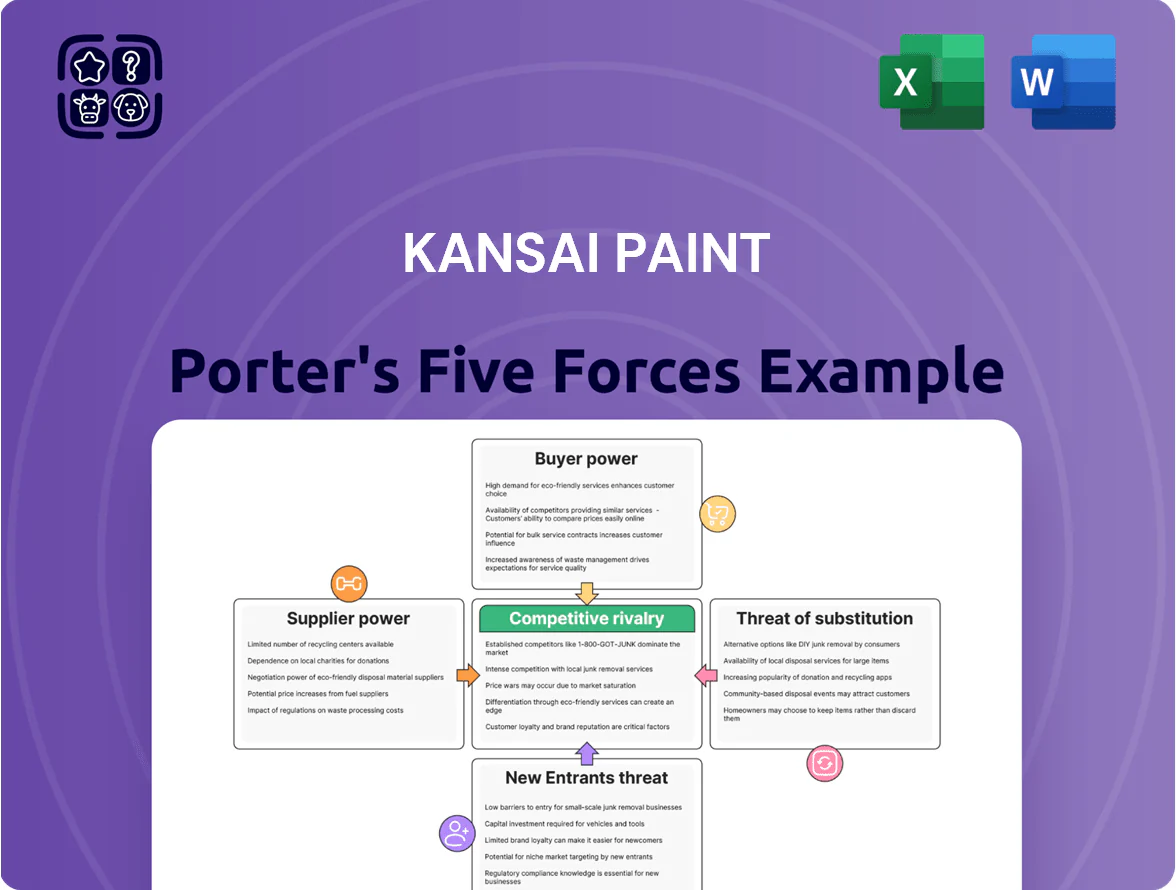

Kansai Paint faces moderate supplier power and high rivalry from global and regional coatings players, while buyer sensitivity and substitute materials exert mixed pressure on margins; regulatory and raw-material volatility add strategic complexity. This snapshot highlights key competitive levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Kansai Paint. Get the complete report to inform investment or strategic decisions with consultant-grade detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The paint industry relies on petrochemical derivatives and pigments like titanium dioxide, whose prices swung 18% year‑on‑year in 2025, driving raw material cost volatility for Kansai Paint. Large chemical suppliers—BASF, Dow, and Evonik—have tightened supply, and global feedstock disruptions kept specialty chemical spot premiums near 12% in Q4 2025, raising bargaining power. Kansai Paint faces margin pressure: raw materials were ~38% of COGS in FY2024, so managing procurement and pass‑throughs is critical to preserve profitability across its automotive, industrial and decorative lines.

Limited Number of Specialized Chemical Providers

Shift Toward Sustainable and Bio-based Inputs

In 2025 tighter environmental rules pushed demand for bio-based inputs, raising supplier leverage; global bio-resin prices rose ~12% YoY to $1,850/ton in 2025, per industry tracker. Suppliers with proprietary green tech or sustainable feedstocks now set premiums, capturing 5–15% price uplift. Kansai Paint’s 2024 sustainability targets require securing scarce eco-raws, often buying long-term at higher margins to avoid disruption.

Energy Costs and Utility Dependency

The energy-intensive paint manufacturing process makes Kansai Paint vulnerable to utility pricing power; global average industrial electricity rose ~14% in 2022–2024 and Japan’s industrial power prices were ~¥25–30/kWh in 2024, directly lifting overheads.

Despite ¥5–10bn annual capex on energy efficiency and onsite solar pilots, local utility monopolies and regional gas price swings limit Kansai’s rate-negotiation leverage in 2025.

- Energy-driven COGS exposure: ~10–15% of manufacturing costs

- 2024 Japan industrial electricity: ¥25–30/kWh

- Annual energy-efficiency capex: ¥5–10bn

- Localized utility markets reduce bargaining power

Impact of Forward Integration by Suppliers

Large chemical conglomerates (BASF, Dow, Mitsui) show a moderate forward-integration threat into specialty coatings; in 2024 BASF’s coatings-related revenues were ~5.6bn EUR, signaling scale to enter finished paints.

If suppliers start making finished coatings, they may prioritize captive demand, risking volume and margin pressure for Kansai Paint (Kansai’s 2024 net sales ¥578bn vs. global coatings market ~$160bn).

This risk forces Kansai to secure long-term contracts, co-development deals, and dual-sourcing to protect supply continuity and margin—stable supplier partnerships reduced raw-material cost volatility by ~3–5% in similar cases.

- Moderate threat from big chem players (BASF, Dow, Mitsui)

- BASF coatings scale: ~5.6bn EUR (2024)

- Kansai Paint sales: ¥578bn (2024)

- Mitigation: long-term contracts, co-development, dual-sourcing

Kansai counters high supplier power—38% COGS, ±18% TiO2 swings, costly OEM lock-ins

Suppliers hold moderate-to-high power: petrochemical and pigment price swings (TiO2 ±18% YoY in 2025) and specialty resin concentration (US$45.2bn market, few large players) raise input costs; raw materials ≈38% of COGS (FY2024). Kansai offsets via 18% strategic-partner sourcing, multi-year contracts, dual-sourcing and ¥5–10bn energy capex, but OEM reapproval (6–18 months, >US$1m) keeps switching costs high.

| Metric | Value |

|---|---|

| Raw materials of COGS (FY2024) | ≈38% |

| TiO2 price swing (2025) | ±18% YoY |

| Specialty resin market (2024) | US$45.2bn |

| Strategic-partner sourcing | ≈18% of raw materials |

| OEM reapproval time/cost | 6–18 months; >US$1m |

| Energy capex (annual) | ¥5–10bn |

What is included in the product

Concise Porter’s Five Forces assessment of Kansai Paint, highlighting competitive rivalry, buyer/supplier power, threats from new entrants and substitutes, and strategic levers to protect margins and market share.

A concise, one-sheet Porter's Five Forces for Kansai Paint—instantly reveals competitive pressures and strategic levers for quick decision-making by investors and executives.

Customers Bargaining Power

Concentrated Power of Automotive OEMs

Kansai Paint supplies auto OEMs where the top 10 global manufacturers account for roughly 60% of vehicle production, giving buyers concentrated leverage that forces strict quality, JIT delivery, and aggressive price pressure that compresses supplier margins.

OEMs’ demands push Kansai to invest in process control and inventory systems; Kansai’s FY2024 gross margin of ~28% reflects this squeeze versus pre-2020 levels near 31%.

By end-2025, EVs made up ~16% of global sales, raising demand for functional, cost-effective coatings (thermal management, EMI shielding) and increasing R&D and pricing pressure on suppliers like Kansai.

Price Sensitivity in Decorative Markets

In Kansai Paint’s decorative segment, consumers and contractors face low switching costs and high price sensitivity, with retail shelf competition — over 30 major brands in key markets like India and Southeast Asia as of 2025 — enabling quick cross-price comparison. Price-driven buying is backed by surveys showing 58% of DIY buyers cite price as primary factor. Kansai must lean on branding, loyalty schemes and targeted trade discounts to prevent churn to cheaper alternatives.

Rising Demand for Functional and Smart Coatings

Industrial and marine clients increasingly demand functional and smart coatings—anti-corrosion, self-cleaning, heat-reflective—that can command 10–30% price premiums, per 2024 industry reports showing smart-coating adoption rising ~12% YoY in marine sectors.

These buyers require documented performance and ROI, pushing Kansai Paint to deliver third-party test data and lifecycle cost analyses to win contracts.

As a result bargaining power shifts toward sophisticated customers who insist on bespoke formulations, long-term warranties, and extensive technical support, raising service and R&D costs by an estimated 3–5% of revenues for leading suppliers.

Transparency Through Digital Comparison Tools

By 2025, digital procurement platforms and review sites have cut opacity: 78% of APAC buyers use online comparisons for paint specs and 64% for supplier pricing, exposing VOC levels, durability tests, and cost-per-square-meter data.

That visibility caps Kansai Paint’s pricing power—premium tags only stick when third-party data proves superior performance and lifecycle ROI.

- 78% APAC buyers use online comparisons

- 64% use platforms for supplier pricing

- Customers compare VOC, durability, cost/m2

- Premium pricing demands independent data

Bulk Purchasing Power of Large Retailers

Large home-improvement chains and global distributors extract deep discounts and shelf-space terms from paint makers; in 2024 big-box buyers accounted for ~28% of Japan decorative paint volume, squeezing margins by 150–300 bps on average.

Kansai Paint counters by keeping direct distribution, owning ~12% of domestic dealer outlets, and shifting sales to pro channels where gross margins are ~6–8 percentage points higher.

- Retailers' volume share ~28%

- Margin pressure 150–300 bps

- Kansai dealer share ~12%

- Pro-channel margin premium 6–8 ppt

Rising Customer Clout Cuts Margins as OEMs Concentrate and Online Shopping Soars

Bargaining power of customers is high: top 10 OEMs ~60% global production, FY2024 gross margin ~28% (vs ~31% pre-2020), EVs ~16% of sales by end-2025, APAC buyers: 78% use online comparisons, 64% price platforms, big-box retailers ~28% decorative volume causing 150–300 bps margin pressure; Kansai dealer share ~12%, pro-channel margin +6–8 ppt.

| Metric | Value |

|---|---|

| OEM concentration | Top10 ~60% |

| FY2024 gross margin | ~28% |

| EV share (2025) | ~16% |

| APAC online comps | 78% |

| Retailer volume | ~28% |

What You See Is What You Get

Kansai Paint Porter's Five Forces Analysis

This preview shows the exact Kansai Paint Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same fully formatted, professionally written file you'll be able to download and use the moment you buy.

You're viewing the final deliverable: a complete, ready-to-use analysis available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kansai Paint faces moderate supplier power and high rivalry from global and regional coatings players, while buyer sensitivity and substitute materials exert mixed pressure on margins; regulatory and raw-material volatility add strategic complexity. This snapshot highlights key competitive levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Kansai Paint. Get the complete report to inform investment or strategic decisions with consultant-grade detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The paint industry relies on petrochemical derivatives and pigments like titanium dioxide, whose prices swung 18% year‑on‑year in 2025, driving raw material cost volatility for Kansai Paint. Large chemical suppliers—BASF, Dow, and Evonik—have tightened supply, and global feedstock disruptions kept specialty chemical spot premiums near 12% in Q4 2025, raising bargaining power. Kansai Paint faces margin pressure: raw materials were ~38% of COGS in FY2024, so managing procurement and pass‑throughs is critical to preserve profitability across its automotive, industrial and decorative lines.

Limited Number of Specialized Chemical Providers

Shift Toward Sustainable and Bio-based Inputs

In 2025 tighter environmental rules pushed demand for bio-based inputs, raising supplier leverage; global bio-resin prices rose ~12% YoY to $1,850/ton in 2025, per industry tracker. Suppliers with proprietary green tech or sustainable feedstocks now set premiums, capturing 5–15% price uplift. Kansai Paint’s 2024 sustainability targets require securing scarce eco-raws, often buying long-term at higher margins to avoid disruption.

Energy Costs and Utility Dependency

The energy-intensive paint manufacturing process makes Kansai Paint vulnerable to utility pricing power; global average industrial electricity rose ~14% in 2022–2024 and Japan’s industrial power prices were ~¥25–30/kWh in 2024, directly lifting overheads.

Despite ¥5–10bn annual capex on energy efficiency and onsite solar pilots, local utility monopolies and regional gas price swings limit Kansai’s rate-negotiation leverage in 2025.

- Energy-driven COGS exposure: ~10–15% of manufacturing costs

- 2024 Japan industrial electricity: ¥25–30/kWh

- Annual energy-efficiency capex: ¥5–10bn

- Localized utility markets reduce bargaining power

Impact of Forward Integration by Suppliers

Large chemical conglomerates (BASF, Dow, Mitsui) show a moderate forward-integration threat into specialty coatings; in 2024 BASF’s coatings-related revenues were ~5.6bn EUR, signaling scale to enter finished paints.

If suppliers start making finished coatings, they may prioritize captive demand, risking volume and margin pressure for Kansai Paint (Kansai’s 2024 net sales ¥578bn vs. global coatings market ~$160bn).

This risk forces Kansai to secure long-term contracts, co-development deals, and dual-sourcing to protect supply continuity and margin—stable supplier partnerships reduced raw-material cost volatility by ~3–5% in similar cases.

- Moderate threat from big chem players (BASF, Dow, Mitsui)

- BASF coatings scale: ~5.6bn EUR (2024)

- Kansai Paint sales: ¥578bn (2024)

- Mitigation: long-term contracts, co-development, dual-sourcing

Kansai counters high supplier power—38% COGS, ±18% TiO2 swings, costly OEM lock-ins

Suppliers hold moderate-to-high power: petrochemical and pigment price swings (TiO2 ±18% YoY in 2025) and specialty resin concentration (US$45.2bn market, few large players) raise input costs; raw materials ≈38% of COGS (FY2024). Kansai offsets via 18% strategic-partner sourcing, multi-year contracts, dual-sourcing and ¥5–10bn energy capex, but OEM reapproval (6–18 months, >US$1m) keeps switching costs high.

| Metric | Value |

|---|---|

| Raw materials of COGS (FY2024) | ≈38% |

| TiO2 price swing (2025) | ±18% YoY |

| Specialty resin market (2024) | US$45.2bn |

| Strategic-partner sourcing | ≈18% of raw materials |

| OEM reapproval time/cost | 6–18 months; >US$1m |

| Energy capex (annual) | ¥5–10bn |

What is included in the product

Concise Porter’s Five Forces assessment of Kansai Paint, highlighting competitive rivalry, buyer/supplier power, threats from new entrants and substitutes, and strategic levers to protect margins and market share.

A concise, one-sheet Porter's Five Forces for Kansai Paint—instantly reveals competitive pressures and strategic levers for quick decision-making by investors and executives.

Customers Bargaining Power

Concentrated Power of Automotive OEMs

Kansai Paint supplies auto OEMs where the top 10 global manufacturers account for roughly 60% of vehicle production, giving buyers concentrated leverage that forces strict quality, JIT delivery, and aggressive price pressure that compresses supplier margins.

OEMs’ demands push Kansai to invest in process control and inventory systems; Kansai’s FY2024 gross margin of ~28% reflects this squeeze versus pre-2020 levels near 31%.

By end-2025, EVs made up ~16% of global sales, raising demand for functional, cost-effective coatings (thermal management, EMI shielding) and increasing R&D and pricing pressure on suppliers like Kansai.

Price Sensitivity in Decorative Markets

In Kansai Paint’s decorative segment, consumers and contractors face low switching costs and high price sensitivity, with retail shelf competition — over 30 major brands in key markets like India and Southeast Asia as of 2025 — enabling quick cross-price comparison. Price-driven buying is backed by surveys showing 58% of DIY buyers cite price as primary factor. Kansai must lean on branding, loyalty schemes and targeted trade discounts to prevent churn to cheaper alternatives.

Rising Demand for Functional and Smart Coatings

Industrial and marine clients increasingly demand functional and smart coatings—anti-corrosion, self-cleaning, heat-reflective—that can command 10–30% price premiums, per 2024 industry reports showing smart-coating adoption rising ~12% YoY in marine sectors.

These buyers require documented performance and ROI, pushing Kansai Paint to deliver third-party test data and lifecycle cost analyses to win contracts.

As a result bargaining power shifts toward sophisticated customers who insist on bespoke formulations, long-term warranties, and extensive technical support, raising service and R&D costs by an estimated 3–5% of revenues for leading suppliers.

Transparency Through Digital Comparison Tools

By 2025, digital procurement platforms and review sites have cut opacity: 78% of APAC buyers use online comparisons for paint specs and 64% for supplier pricing, exposing VOC levels, durability tests, and cost-per-square-meter data.

That visibility caps Kansai Paint’s pricing power—premium tags only stick when third-party data proves superior performance and lifecycle ROI.

- 78% APAC buyers use online comparisons

- 64% use platforms for supplier pricing

- Customers compare VOC, durability, cost/m2

- Premium pricing demands independent data

Bulk Purchasing Power of Large Retailers

Large home-improvement chains and global distributors extract deep discounts and shelf-space terms from paint makers; in 2024 big-box buyers accounted for ~28% of Japan decorative paint volume, squeezing margins by 150–300 bps on average.

Kansai Paint counters by keeping direct distribution, owning ~12% of domestic dealer outlets, and shifting sales to pro channels where gross margins are ~6–8 percentage points higher.

- Retailers' volume share ~28%

- Margin pressure 150–300 bps

- Kansai dealer share ~12%

- Pro-channel margin premium 6–8 ppt

Rising Customer Clout Cuts Margins as OEMs Concentrate and Online Shopping Soars

Bargaining power of customers is high: top 10 OEMs ~60% global production, FY2024 gross margin ~28% (vs ~31% pre-2020), EVs ~16% of sales by end-2025, APAC buyers: 78% use online comparisons, 64% price platforms, big-box retailers ~28% decorative volume causing 150–300 bps margin pressure; Kansai dealer share ~12%, pro-channel margin +6–8 ppt.

| Metric | Value |

|---|---|

| OEM concentration | Top10 ~60% |

| FY2024 gross margin | ~28% |

| EV share (2025) | ~16% |

| APAC online comps | 78% |

| Retailer volume | ~28% |

What You See Is What You Get

Kansai Paint Porter's Five Forces Analysis

This preview shows the exact Kansai Paint Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same fully formatted, professionally written file you'll be able to download and use the moment you buy.

You're viewing the final deliverable: a complete, ready-to-use analysis available instantly upon payment.