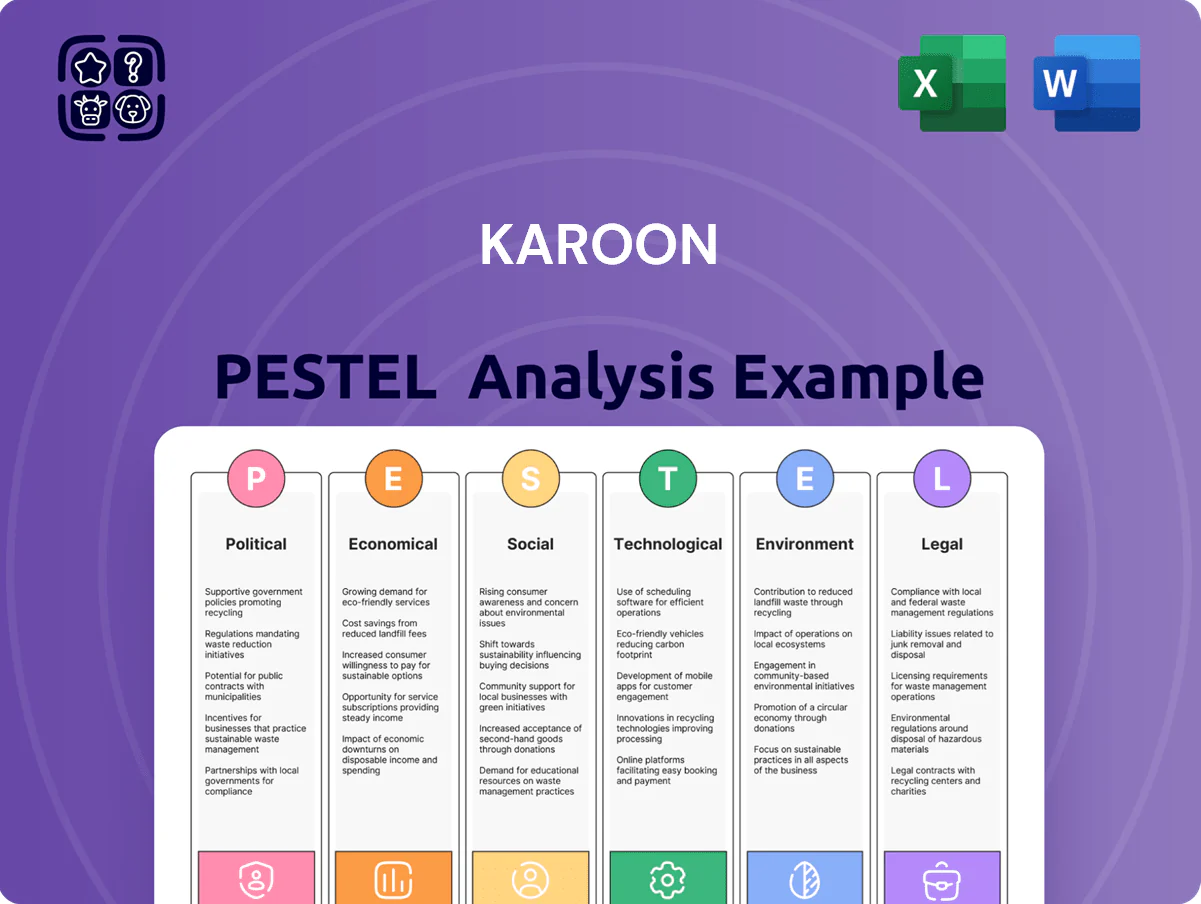

Karoon PESTLE Analysis

Skip the Research. Get the Strategy.

Unpack the external forces shaping Karoon with our concise PESTLE snapshot—highlighting regulatory risks, commodity price exposure, technological shifts, and environmental pressures that matter to investors and strategists; purchase the full PESTLE to access detailed, actionable insights and downloadable formats for immediate use.

Political factors

Geopolitical Stability in Brazil

Brazil's political stability is pivotal for Karoon, which held 100% of its producing assets in Brazil until its 2024 takeover by Woodside; government shifts can alter Petrobras divestment timing and ANP regulatory enforcement—ANP issued 12 deepwater licensing decisions in 2023–2024 affecting Santos Basin activity. Contract sanctity remains vital for Karoon's planned Santos Basin CAPEX, which was estimated at ~US$150–200 million pre-takeover.

Australian Energy Policy Shifts

As an Australian-listed E&P, Karoon faces domestic policy shifts on offshore exploration and gas firming; federal debate in 2024 over a national gas trigger and state moratoriums (e.g., WA's tightened approvals) affects permit timing and project NPV—Karoon reported A$238m revenue in FY2024, so delays materially hit cash flow. Changes in leadership can reintroduce drilling moratoriums or fast-track permits, forcing trade-offs between domestic gas security and export price parity.

Global Trade and Energy Sanctions

Karoon must navigate a complex web of international trade relations that shape oil benchmarks and supply chain logistics; Brent averaged about 96 USD/bbl in 2024, shifting Karoon’s revenue sensitivity by roughly ±8% for every 10 USD move in price given its FY24 oil sales exposure.

Political tensions in the Middle East and Eastern Europe drove Brent volatility (+28% peak-to-trough in 2024), directly compressing Karoon’s margins through higher lift and transport costs and uneven offtake timing.

Strict adherence to international sanctions remains mandatory to preserve access to global financing and partners; in 2024, 70% of project funding and export routes for Australian oil firms relied on banks and insurers with sanctions compliance programs.

Fiscal Regime Stability

The company faces material fiscal regime risk in Brazil where effective royalties plus special participation can rise; Brazil’s 2024 average government take from deepwater fields has reached ~70% at peak prices, and proposed legislative drafts in 2024–25 signaled potential increases of 3–7 percentage points.

Political pressure to raise state revenue during the 2022–24 oil price upcycle (Brent averaging ~$87/bbl in 2024) increases this risk, making cash flow sensitive to royalty/surtax shifts.

Maintaining constructive engagement with Brazilian and Australian tax authorities is essential for predictable modeling; stress tests should include royalty hikes of 5–10% and special participation volatility of ±USD 50–100m annually.

- Brazil government take ~70% peak (2024)

- Potential royalty/surtax increases 3–7ppt (2024–25 drafts)

- Brent avg ~$87/bbl (2024) heightens pressure

- Model stress: royalty +5–10% or ±USD50–100m/yr

Resource Nationalism Trends

Resource nationalism is rising; in 2024 Argentina increased local content rules to 50% for oil services, pressuring foreign operators like Karoon which earned A$174m revenue in FY2024—Karoon must boost local employment and community spends to retain access.

Demonstrating local value via jobs and community investment reduces risk of protectionist measures; aligning projects with provincial governments and unions can shield operations from populist shifts.

- Local content rule example: Argentina 50% (2024)

- Karoon FY2024 revenue: A$174m

- Mitigation: hire locally, increase community investment, stakeholder alignment

Karoon outlook: Brazil take, ANP deepwater moves and rising local costs squeeze cash flow

Brazil political stability, ANP licensing (12 deepwater decisions 2023–24) and ~70% peak government take (2024) materially affect Karoon’s Santos Basin CAPEX (~US$150–200m pre-takeover) and cash flow; Australian gas policy debate and WA approvals impact permit timing; Brent avg ~$87–96/bbl in 2024 drove revenue sensitivity; sanctions/compliance and rising local content (Argentina 50% 2024) increase operational costs.

| Metric | 2024/24–25 |

|---|---|

| ANP deepwater decisions | 12 (2023–24) |

| Brazil gov't take | ~70% peak (2024) |

| Brent avg | $87–96/bbl (2024) |

| Santos CAPEX | US$150–200m (pre-takeover) |

| Local content (ARG) | 50% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Karoon across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios to pinpoint threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Karoon PESTLE summary that’s easily dropped into presentations or shared across teams to streamline risk discussions and decision-making.

Economic factors

Crude Oil Price Volatility

Karoon's earnings are highly correlated with Brent crude, which averaged about 88 USD/bbl in 2024 after peaking near 120 USD/bbl in 2022; a 10% Brent decline can materially cut operating margins and free cash flow given Karoon's lift-cost structure.

Global demand swings—China and EU slowdowns in 2024 trimmed seaborne oil consumption growth to ~0.5 mb/d—force reassessment of marginal exploration and development projects with longer paybacks.

Karoon employs hedging and insurance instruments; firms in the sector increased hedge coverage to protect 2024–25 cash flows amid 2023–24 volatility, reducing downside price exposure.

Currency Exchange Rate Fluctuations

Karoon earns most revenue in USD while incurring substantial operating costs in BRL and some in AUD; in 2024 the BRL/USD moved from ~5.0 to ~5.3, amplifying local cost pressures and creating material FX translation effects on quarterly results.

Access to Capital Markets

As of late 2025 the global policy rate backdrop has tightened—US Fed funds around 5.25–5.50% and RBA cash rate near 4.35%—pushing corporate borrowing costs higher and raising Karoon’s cost of debt for expansionary offshore projects.

Tighter monetary settings elevate the hurdle rate for new developments and M&A, increasing discount rates used in Karoon valuation and project IRR targets.

Maintaining net cash or low gearing (target debt/EBITDA <1.5x) will be vital for Karoon to secure sub-investment-grade lenders’ terms and attract equity at competitive valuations.

Inflationary Pressure on OPEX

Inflation-driven rises in specialized labor, rig charters and subsea kit — with global rig dayrates up ~30% in 2024 and subsea equipment lead times extending 20–40% — threaten Baúna and Patola margins by increasing OPEX and unit costs.

Supply-chain bottlenecks pushed premium pricing for key services, contributing to sectoral OPEX inflation ~8–12% y/y in 2024; Karoon needs tight cost controls and operational efficiencies to preserve low-cost-producer status.

- Rig dayrates +30% (2024)

- Subsea lead times +20–40%

- Sector OPEX inflation 8–12% y/y (2024)

- Necessity: strict cost controls, efficiency gains

Global Economic Growth Forecasts

Global GDP growth forecast of 3.0–3.5% in 2025–2026 (IMF, Jan 2026) underpins stronger energy demand in emerging markets, supporting Karoon’s hydrocarbons and brownfield investment cases.

If a recession cuts global GDP to ~-0.5–0.0% scenario, lower oil/gas demand and ~20–30% capex deferral risk would push Karoon toward capital preservation and production optimization.

- IMF global growth 2025–26: 3.0–3.5%

- Emerging markets drive majority demand growth

- Recession scenario could trigger 20–30% capex cuts

Oil at $88, rising costs and FX squeeze margins—recession could cut capex 20–30%

Key economic risks: Brent averaged ~88 USD/bbl (2024); a 10% price drop materially compresses margins; rig dayrates +30% and sector OPEX inflation 8–12% (2024) raise unit costs; BRL/USD moved ~5.0→5.3 (2024) increasing local cost pressure; IMF global growth 2025–26 3.0–3.5% supports demand, while recession could force 20–30% capex cuts.

| Metric | Value (latest) |

|---|---|

| Brent (2024 avg) | ~88 USD/bbl |

| Rig dayrates | +30% (2024) |

| Sector OPEX inflation | 8–12% y/y (2024) |

| BRL/USD | ~5.0→5.3 (2024) |

| IMF global growth | 3.0–3.5% (2025–26) |

| Potential capex cut (recession) | 20–30% |

Full Version Awaits

Karoon PESTLE Analysis

The preview shown here is the exact Karoon PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making. The layout, content, and insights visible in this sample are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, finished document you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unpack the external forces shaping Karoon with our concise PESTLE snapshot—highlighting regulatory risks, commodity price exposure, technological shifts, and environmental pressures that matter to investors and strategists; purchase the full PESTLE to access detailed, actionable insights and downloadable formats for immediate use.

Political factors

Geopolitical Stability in Brazil

Brazil's political stability is pivotal for Karoon, which held 100% of its producing assets in Brazil until its 2024 takeover by Woodside; government shifts can alter Petrobras divestment timing and ANP regulatory enforcement—ANP issued 12 deepwater licensing decisions in 2023–2024 affecting Santos Basin activity. Contract sanctity remains vital for Karoon's planned Santos Basin CAPEX, which was estimated at ~US$150–200 million pre-takeover.

Australian Energy Policy Shifts

As an Australian-listed E&P, Karoon faces domestic policy shifts on offshore exploration and gas firming; federal debate in 2024 over a national gas trigger and state moratoriums (e.g., WA's tightened approvals) affects permit timing and project NPV—Karoon reported A$238m revenue in FY2024, so delays materially hit cash flow. Changes in leadership can reintroduce drilling moratoriums or fast-track permits, forcing trade-offs between domestic gas security and export price parity.

Global Trade and Energy Sanctions

Karoon must navigate a complex web of international trade relations that shape oil benchmarks and supply chain logistics; Brent averaged about 96 USD/bbl in 2024, shifting Karoon’s revenue sensitivity by roughly ±8% for every 10 USD move in price given its FY24 oil sales exposure.

Political tensions in the Middle East and Eastern Europe drove Brent volatility (+28% peak-to-trough in 2024), directly compressing Karoon’s margins through higher lift and transport costs and uneven offtake timing.

Strict adherence to international sanctions remains mandatory to preserve access to global financing and partners; in 2024, 70% of project funding and export routes for Australian oil firms relied on banks and insurers with sanctions compliance programs.

Fiscal Regime Stability

The company faces material fiscal regime risk in Brazil where effective royalties plus special participation can rise; Brazil’s 2024 average government take from deepwater fields has reached ~70% at peak prices, and proposed legislative drafts in 2024–25 signaled potential increases of 3–7 percentage points.

Political pressure to raise state revenue during the 2022–24 oil price upcycle (Brent averaging ~$87/bbl in 2024) increases this risk, making cash flow sensitive to royalty/surtax shifts.

Maintaining constructive engagement with Brazilian and Australian tax authorities is essential for predictable modeling; stress tests should include royalty hikes of 5–10% and special participation volatility of ±USD 50–100m annually.

- Brazil government take ~70% peak (2024)

- Potential royalty/surtax increases 3–7ppt (2024–25 drafts)

- Brent avg ~$87/bbl (2024) heightens pressure

- Model stress: royalty +5–10% or ±USD50–100m/yr

Resource Nationalism Trends

Resource nationalism is rising; in 2024 Argentina increased local content rules to 50% for oil services, pressuring foreign operators like Karoon which earned A$174m revenue in FY2024—Karoon must boost local employment and community spends to retain access.

Demonstrating local value via jobs and community investment reduces risk of protectionist measures; aligning projects with provincial governments and unions can shield operations from populist shifts.

- Local content rule example: Argentina 50% (2024)

- Karoon FY2024 revenue: A$174m

- Mitigation: hire locally, increase community investment, stakeholder alignment

Karoon outlook: Brazil take, ANP deepwater moves and rising local costs squeeze cash flow

Brazil political stability, ANP licensing (12 deepwater decisions 2023–24) and ~70% peak government take (2024) materially affect Karoon’s Santos Basin CAPEX (~US$150–200m pre-takeover) and cash flow; Australian gas policy debate and WA approvals impact permit timing; Brent avg ~$87–96/bbl in 2024 drove revenue sensitivity; sanctions/compliance and rising local content (Argentina 50% 2024) increase operational costs.

| Metric | 2024/24–25 |

|---|---|

| ANP deepwater decisions | 12 (2023–24) |

| Brazil gov't take | ~70% peak (2024) |

| Brent avg | $87–96/bbl (2024) |

| Santos CAPEX | US$150–200m (pre-takeover) |

| Local content (ARG) | 50% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Karoon across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed insights and forward-looking scenarios to pinpoint threats and opportunities for executives, investors, and strategists.

A concise, visually segmented Karoon PESTLE summary that’s easily dropped into presentations or shared across teams to streamline risk discussions and decision-making.

Economic factors

Crude Oil Price Volatility

Karoon's earnings are highly correlated with Brent crude, which averaged about 88 USD/bbl in 2024 after peaking near 120 USD/bbl in 2022; a 10% Brent decline can materially cut operating margins and free cash flow given Karoon's lift-cost structure.

Global demand swings—China and EU slowdowns in 2024 trimmed seaborne oil consumption growth to ~0.5 mb/d—force reassessment of marginal exploration and development projects with longer paybacks.

Karoon employs hedging and insurance instruments; firms in the sector increased hedge coverage to protect 2024–25 cash flows amid 2023–24 volatility, reducing downside price exposure.

Currency Exchange Rate Fluctuations

Karoon earns most revenue in USD while incurring substantial operating costs in BRL and some in AUD; in 2024 the BRL/USD moved from ~5.0 to ~5.3, amplifying local cost pressures and creating material FX translation effects on quarterly results.

Access to Capital Markets

As of late 2025 the global policy rate backdrop has tightened—US Fed funds around 5.25–5.50% and RBA cash rate near 4.35%—pushing corporate borrowing costs higher and raising Karoon’s cost of debt for expansionary offshore projects.

Tighter monetary settings elevate the hurdle rate for new developments and M&A, increasing discount rates used in Karoon valuation and project IRR targets.

Maintaining net cash or low gearing (target debt/EBITDA <1.5x) will be vital for Karoon to secure sub-investment-grade lenders’ terms and attract equity at competitive valuations.

Inflationary Pressure on OPEX

Inflation-driven rises in specialized labor, rig charters and subsea kit — with global rig dayrates up ~30% in 2024 and subsea equipment lead times extending 20–40% — threaten Baúna and Patola margins by increasing OPEX and unit costs.

Supply-chain bottlenecks pushed premium pricing for key services, contributing to sectoral OPEX inflation ~8–12% y/y in 2024; Karoon needs tight cost controls and operational efficiencies to preserve low-cost-producer status.

- Rig dayrates +30% (2024)

- Subsea lead times +20–40%

- Sector OPEX inflation 8–12% y/y (2024)

- Necessity: strict cost controls, efficiency gains

Global Economic Growth Forecasts

Global GDP growth forecast of 3.0–3.5% in 2025–2026 (IMF, Jan 2026) underpins stronger energy demand in emerging markets, supporting Karoon’s hydrocarbons and brownfield investment cases.

If a recession cuts global GDP to ~-0.5–0.0% scenario, lower oil/gas demand and ~20–30% capex deferral risk would push Karoon toward capital preservation and production optimization.

- IMF global growth 2025–26: 3.0–3.5%

- Emerging markets drive majority demand growth

- Recession scenario could trigger 20–30% capex cuts

Oil at $88, rising costs and FX squeeze margins—recession could cut capex 20–30%

Key economic risks: Brent averaged ~88 USD/bbl (2024); a 10% price drop materially compresses margins; rig dayrates +30% and sector OPEX inflation 8–12% (2024) raise unit costs; BRL/USD moved ~5.0→5.3 (2024) increasing local cost pressure; IMF global growth 2025–26 3.0–3.5% supports demand, while recession could force 20–30% capex cuts.

| Metric | Value (latest) |

|---|---|

| Brent (2024 avg) | ~88 USD/bbl |

| Rig dayrates | +30% (2024) |

| Sector OPEX inflation | 8–12% y/y (2024) |

| BRL/USD | ~5.0→5.3 (2024) |

| IMF global growth | 3.0–3.5% (2025–26) |

| Potential capex cut (recession) | 20–30% |

Full Version Awaits

Karoon PESTLE Analysis

The preview shown here is the exact Karoon PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making. The layout, content, and insights visible in this sample are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, finished document you’ll own upon checkout.