Kaufman & Broad Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

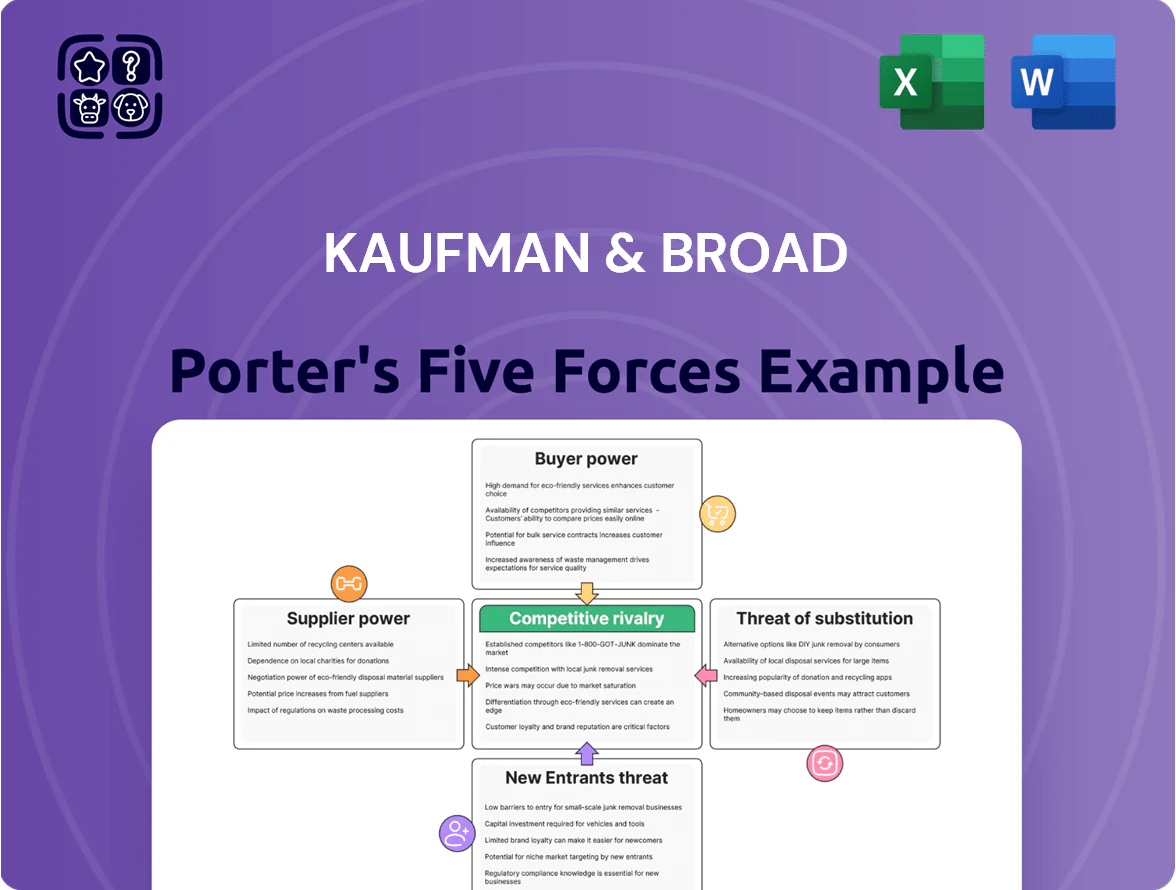

Suppliers Bargaining Power

Scarcity of developable land in strategic urban areas

The scarcity of developable land in strategic French urban areas is the key supplier power issue for Kaufman & Broad through 2025; municipalities and private owners control plots under tight zoning, limiting supply.

Competitive bidding has driven prices up—urban land in Paris region rose ~18% 2020–2024, pushing per-hectare values above €10m in some suburbs—squeezing developer margins.

Volatility in construction material and energy costs

Suppliers of concrete, steel and timber hold moderate bargaining power as global commodity swings persist—steel rose ~18% in 2023 and timber 12% in 2024—while supply chains eased since 2022.

Demand for low-carbon materials under French RE2020 boosts niche suppliers’ pricing power; low-carbon concrete premiums reached ~5–10% in 2024.

Kaufman & Broad should lock costs via 3–5 year contracts and bulk buys; a 10% volume discount can cut COGS materially.

Dependency on a specialized subcontracting workforce

The persistent shortage of skilled construction labor in France—unemployment in the sector fell to 4.2% in 2024—raises supplier power as specialized subcontractors gain leverage over builders like Kaufman & Broad. Kaufman & Broad depends on external crews for on-site execution across regions, so scarcity lets firms charge premium rates; average specialist subcontractor wage growth hit 6.8% in 2024. Demand for eco-friendly building skills (BREEAM/RE2020 compliance) further pushes up wages and contract concessions.

Tightening of environmental and technical regulations

As RE2020 and tightening EU regs push new builds to cut CO2 and boost insulation, suppliers of certified green tech gain leverage over Kaufman & Broad; mandatory high-performance insulation and heat pumps raise switching costs and limit use of cheaper alternatives.

In 2024 France required new residential ratings to reduce emissions ~30% vs 2020, creating a captive market where certified suppliers can command price premiums and influence delivery timelines.

- Mandatory RE2020 targets: ~30% emissions cut vs 2020

- Higher switching costs: certified components only

- Price premiums for certified suppliers

- Supply timing impacts project schedules

Concentration of financial lending institutions

Kaufman & Broad relies heavily on bank financing and guarantees for large residential projects; in France the top five banks held about 60% of corporate lending in 2024, so a few lenders largely set loan pricing and covenant terms.

When major banks tighten credit or raise development loan rates (EURIBOR-linked spreads rose 120–180 bps in 2023–24), project starts and margins for Kaufman & Broad fall quickly.

- High dependency on bank debt

- Top 5 banks ≈60% corporate lending (2024)

- EURIBOR spreads +120–180 bps (2023–24)

- Credit tightening = immediate project slowdown

Suppliers exert rising squeeze on Kaufman & Broad as land, banks and materials hike costs

Suppliers hold moderate-to-high power for Kaufman & Broad: scarce urban land (Paris-region values +18% 2020–24, >€10m/ha in suburbs) and concentrated bank lending (top 5 banks ~60% of corporate loans in 2024) squeeze margins; commodities and green-certified materials saw 2023–24 price premiums (steel +18%, timber +12%, low-carbon concrete +5–10%), while specialist subcontractor wages rose ~6.8% in 2024.

| Metric | Value |

|---|---|

| Paris-region land change 2020–24 | +18% |

| Suburban land | >€10m/ha |

| Steel 2023 | +18% |

| Timber 2024 | +12% |

| Low-carbon concrete premium 2024 | 5–10% |

| Specialist wage growth 2024 | 6.8% |

| Top-5 banks share (lending) 2024 | ~60% |

What is included in the product

Tailored exclusively for Kaufman & Broad, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary to inform pricing, profitability, and defensive growth strategies.

A concise, one-sheet Kaufman & Broad Porter’s Five Forces summary that highlights competitive pressures and relief points—ideal for quick strategy sessions or investor briefings.

Customers Bargaining Power

High sensitivity to mortgage interest rates

Individual homebuyers in France are highly sensitive to mortgage rates, which in 2025 averaged ~3.1% for a 20-year loan and directly cut purchasing power; a 0.5 percentage-point rise reduces buyer affordability by roughly 7–10% on a typical €300k mortgage. Even though rates stabilized by end-2025, small moves still shift demand from new builds to resales, so Kaufman & Broad often offers reduced-rate financing, price discounts or deferred payments to keep sales velocity among retail clients.

Influence of large scale institutional investors

A large share of Kaufman & Broad’s 2024 France housing sales—about 28% of units—go to institutional buyers like insurers and social housing agencies, giving these customers strong bargaining power. They buy whole blocks, demand volume discounts (often 5–12%) and bespoke layouts or warranties, and can drop deals worth tens of millions, so they extract better pricing and contract terms than retail buyers.

Availability of government housing incentives

The demand for new housing in France hinges on state tax breaks like Pinel and subsidized loans (PTZ); when Pinel changes in 2024 saw regional limits tightened, new-build sales dipped 6% in H1 2024, shifting buyers to the secondary market. Customers gain indirect leverage as fiscal shifts alter net prices, so Kaufman & Broad must reprice and reconfigure units—mixing smaller, eligible apartments and energy-efficient builds—to retain demand and benefit from current incentives.

Information transparency and digital comparison tools

Modern buyers use portals and comparison tools (SeLoger, MeilleursAgents) and energy labels (DPE) to see prices and developer ratings; 2024 searches for developer reviews rose ~28% in France, shrinking info gaps and boosting customer leverage.

This transparency lets buyers compare Kaufman & Broad offers with rivals on price, finish, and DPE scores, pressuring the firm to keep margins tight and quality high—new-build average price per m² in 2024: ~€4,100 in Île-de-France.

- More review searches: +28% (2024, France)

- Average new-build price: ~€4,100/m² (Île-de-France, 2024)

- Higher DPE visibility → stronger negotiation

Demand for ESG compliance and energy performance

By late 2025, 62% of French homebuyers say environmental credentials influence purchase decisions, pushing Kaufman & Broad to add high-efficiency heating, triple glazing, and 10–20% higher-spec insulation to remain competitive.

Buyers demand full Energy Performance Certificate (DPE) ratings B or better for new homes; refusal to accept lower ratings forces developers to absorb ~€3,000–€8,000 extra per unit in green build costs.

Customers now dictate technical specs—PV-ready roofs, heat-pump prep, low-VOC materials—shrinking the market for standard builds and raising project breakeven thresholds.

- 62% of buyers prioritize ESG (France, 2025)

- Target DPE B+ drives €3k–€8k/unit cost rise

- Spec demands: PV-ready, heat-pump prep, triple glazing

Buyers Gain Leverage: Mortgage, ESG & Online Search Squeeze Prices and Margins

Customers wield strong bargaining power: retail buyers react to mortgage moves (20y ~3.1% in 2025; +0.5pp → −7–10% affordability) while institutional buyers (≈28% of K&B 2024 sales) secure 5–12% volume discounts; 62% of buyers prioritize ESG (2025), pushing DPE B+ and €3k–€8k/unit green costs, and online search growth (+28% in 2024) tightens price/quality pressure.

| Metric | Value |

|---|---|

| 20y mortgage (2025) | ~3.1% |

| Affordability impact | +0.5pp → −7–10% |

| Institutional share (2024) | ≈28% |

| Volume discounts | 5–12% |

| ESG buyers (2025) | 62% |

| DPE upgrade cost | €3k–€8k/unit |

| Review searches growth (2024) | +28% |

Preview Before You Purchase

Kaufman & Broad Porter's Five Forces Analysis

This preview shows the exact Kaufman & Broad Porter's Five Forces analysis you'll receive—fully formatted, professional, and ready to download immediately after purchase with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Scarcity of developable land in strategic urban areas

The scarcity of developable land in strategic French urban areas is the key supplier power issue for Kaufman & Broad through 2025; municipalities and private owners control plots under tight zoning, limiting supply.

Competitive bidding has driven prices up—urban land in Paris region rose ~18% 2020–2024, pushing per-hectare values above €10m in some suburbs—squeezing developer margins.

Volatility in construction material and energy costs

Suppliers of concrete, steel and timber hold moderate bargaining power as global commodity swings persist—steel rose ~18% in 2023 and timber 12% in 2024—while supply chains eased since 2022.

Demand for low-carbon materials under French RE2020 boosts niche suppliers’ pricing power; low-carbon concrete premiums reached ~5–10% in 2024.

Kaufman & Broad should lock costs via 3–5 year contracts and bulk buys; a 10% volume discount can cut COGS materially.

Dependency on a specialized subcontracting workforce

The persistent shortage of skilled construction labor in France—unemployment in the sector fell to 4.2% in 2024—raises supplier power as specialized subcontractors gain leverage over builders like Kaufman & Broad. Kaufman & Broad depends on external crews for on-site execution across regions, so scarcity lets firms charge premium rates; average specialist subcontractor wage growth hit 6.8% in 2024. Demand for eco-friendly building skills (BREEAM/RE2020 compliance) further pushes up wages and contract concessions.

Tightening of environmental and technical regulations

As RE2020 and tightening EU regs push new builds to cut CO2 and boost insulation, suppliers of certified green tech gain leverage over Kaufman & Broad; mandatory high-performance insulation and heat pumps raise switching costs and limit use of cheaper alternatives.

In 2024 France required new residential ratings to reduce emissions ~30% vs 2020, creating a captive market where certified suppliers can command price premiums and influence delivery timelines.

- Mandatory RE2020 targets: ~30% emissions cut vs 2020

- Higher switching costs: certified components only

- Price premiums for certified suppliers

- Supply timing impacts project schedules

Concentration of financial lending institutions

Kaufman & Broad relies heavily on bank financing and guarantees for large residential projects; in France the top five banks held about 60% of corporate lending in 2024, so a few lenders largely set loan pricing and covenant terms.

When major banks tighten credit or raise development loan rates (EURIBOR-linked spreads rose 120–180 bps in 2023–24), project starts and margins for Kaufman & Broad fall quickly.

- High dependency on bank debt

- Top 5 banks ≈60% corporate lending (2024)

- EURIBOR spreads +120–180 bps (2023–24)

- Credit tightening = immediate project slowdown

Suppliers exert rising squeeze on Kaufman & Broad as land, banks and materials hike costs

Suppliers hold moderate-to-high power for Kaufman & Broad: scarce urban land (Paris-region values +18% 2020–24, >€10m/ha in suburbs) and concentrated bank lending (top 5 banks ~60% of corporate loans in 2024) squeeze margins; commodities and green-certified materials saw 2023–24 price premiums (steel +18%, timber +12%, low-carbon concrete +5–10%), while specialist subcontractor wages rose ~6.8% in 2024.

| Metric | Value |

|---|---|

| Paris-region land change 2020–24 | +18% |

| Suburban land | >€10m/ha |

| Steel 2023 | +18% |

| Timber 2024 | +12% |

| Low-carbon concrete premium 2024 | 5–10% |

| Specialist wage growth 2024 | 6.8% |

| Top-5 banks share (lending) 2024 | ~60% |

What is included in the product

Tailored exclusively for Kaufman & Broad, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary to inform pricing, profitability, and defensive growth strategies.

A concise, one-sheet Kaufman & Broad Porter’s Five Forces summary that highlights competitive pressures and relief points—ideal for quick strategy sessions or investor briefings.

Customers Bargaining Power

High sensitivity to mortgage interest rates

Individual homebuyers in France are highly sensitive to mortgage rates, which in 2025 averaged ~3.1% for a 20-year loan and directly cut purchasing power; a 0.5 percentage-point rise reduces buyer affordability by roughly 7–10% on a typical €300k mortgage. Even though rates stabilized by end-2025, small moves still shift demand from new builds to resales, so Kaufman & Broad often offers reduced-rate financing, price discounts or deferred payments to keep sales velocity among retail clients.

Influence of large scale institutional investors

A large share of Kaufman & Broad’s 2024 France housing sales—about 28% of units—go to institutional buyers like insurers and social housing agencies, giving these customers strong bargaining power. They buy whole blocks, demand volume discounts (often 5–12%) and bespoke layouts or warranties, and can drop deals worth tens of millions, so they extract better pricing and contract terms than retail buyers.

Availability of government housing incentives

The demand for new housing in France hinges on state tax breaks like Pinel and subsidized loans (PTZ); when Pinel changes in 2024 saw regional limits tightened, new-build sales dipped 6% in H1 2024, shifting buyers to the secondary market. Customers gain indirect leverage as fiscal shifts alter net prices, so Kaufman & Broad must reprice and reconfigure units—mixing smaller, eligible apartments and energy-efficient builds—to retain demand and benefit from current incentives.

Information transparency and digital comparison tools

Modern buyers use portals and comparison tools (SeLoger, MeilleursAgents) and energy labels (DPE) to see prices and developer ratings; 2024 searches for developer reviews rose ~28% in France, shrinking info gaps and boosting customer leverage.

This transparency lets buyers compare Kaufman & Broad offers with rivals on price, finish, and DPE scores, pressuring the firm to keep margins tight and quality high—new-build average price per m² in 2024: ~€4,100 in Île-de-France.

- More review searches: +28% (2024, France)

- Average new-build price: ~€4,100/m² (Île-de-France, 2024)

- Higher DPE visibility → stronger negotiation

Demand for ESG compliance and energy performance

By late 2025, 62% of French homebuyers say environmental credentials influence purchase decisions, pushing Kaufman & Broad to add high-efficiency heating, triple glazing, and 10–20% higher-spec insulation to remain competitive.

Buyers demand full Energy Performance Certificate (DPE) ratings B or better for new homes; refusal to accept lower ratings forces developers to absorb ~€3,000–€8,000 extra per unit in green build costs.

Customers now dictate technical specs—PV-ready roofs, heat-pump prep, low-VOC materials—shrinking the market for standard builds and raising project breakeven thresholds.

- 62% of buyers prioritize ESG (France, 2025)

- Target DPE B+ drives €3k–€8k/unit cost rise

- Spec demands: PV-ready, heat-pump prep, triple glazing

Buyers Gain Leverage: Mortgage, ESG & Online Search Squeeze Prices and Margins

Customers wield strong bargaining power: retail buyers react to mortgage moves (20y ~3.1% in 2025; +0.5pp → −7–10% affordability) while institutional buyers (≈28% of K&B 2024 sales) secure 5–12% volume discounts; 62% of buyers prioritize ESG (2025), pushing DPE B+ and €3k–€8k/unit green costs, and online search growth (+28% in 2024) tightens price/quality pressure.

| Metric | Value |

|---|---|

| 20y mortgage (2025) | ~3.1% |

| Affordability impact | +0.5pp → −7–10% |

| Institutional share (2024) | ≈28% |

| Volume discounts | 5–12% |

| ESG buyers (2025) | 62% |

| DPE upgrade cost | €3k–€8k/unit |

| Review searches growth (2024) | +28% |

Preview Before You Purchase

Kaufman & Broad Porter's Five Forces Analysis

This preview shows the exact Kaufman & Broad Porter's Five Forces analysis you'll receive—fully formatted, professional, and ready to download immediately after purchase with no placeholders or samples.