KC Cottrell Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

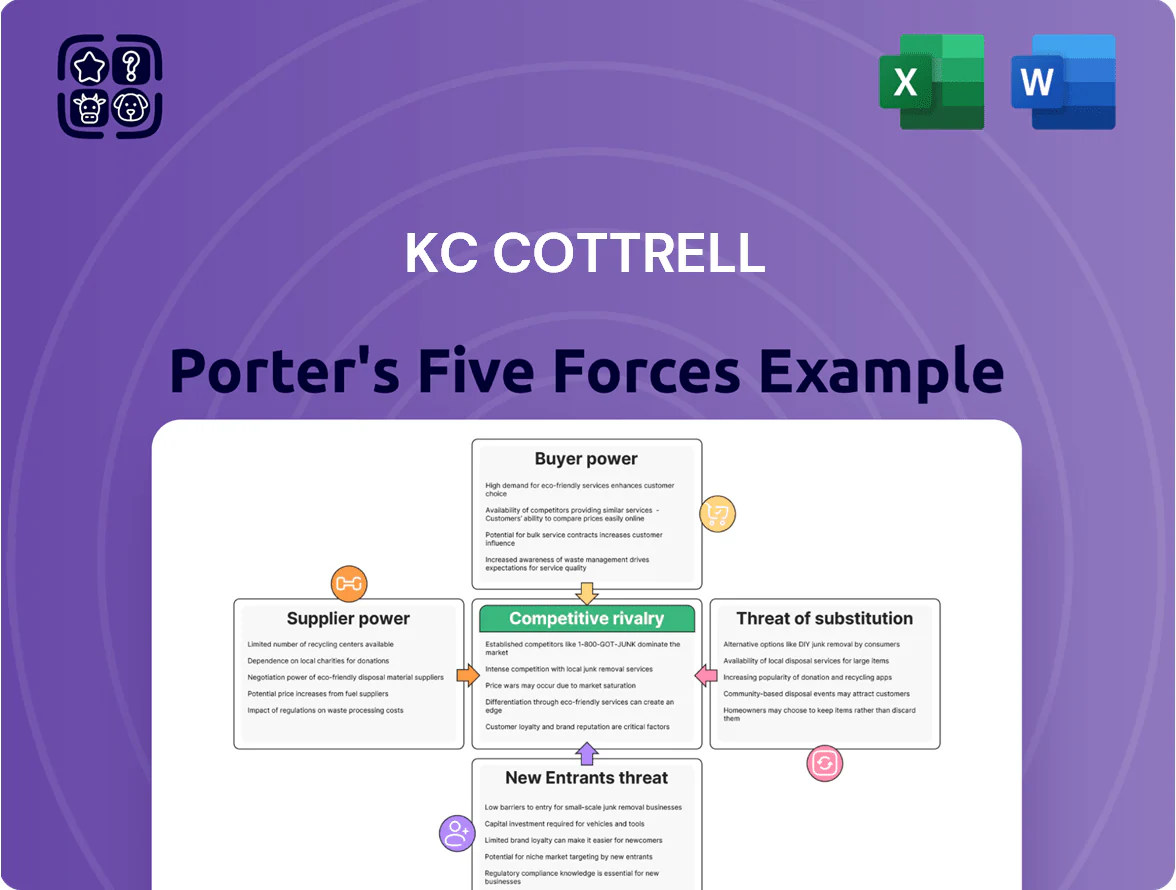

KC Cottrell faces moderate supplier power, niche customer segments, and evolving substitute technologies that together shape its competitive edge in air pollution control systems.

Barriers to entry and rivalry among specialized incumbents keep margins pressured, while regulatory trends create both risks and opportunities for growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KC Cottrell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

KC Cottrell depends on a few global makers for high-voltage transformers and precision sensors used in its electrostatic precipitators, giving suppliers strong bargaining power; supplier concentration means price hikes of 8–12% in 2024 hit margins directly.

Raw Material Price Volatility

The construction of large-scale air pollution control systems uses tons of steel and nickel alloys; global steel plate prices rose ~18% in 2021–2023 and averaged $780/ton in 2024, directly lifting project costs KC Cottrell faces.

Commodity swings are volatile—iron ore spot jumped 40% in 2021–22—and EPC contracts limit immediate price recovery, squeezing margins until change orders are approved.

Major raw-material suppliers set market-driven prices; KC Cottrell often must absorb costs to keep schedules, raising working capital needs and contract risk.

Scarcity of Specialized Engineering Talent

The human capital to design KC Cottrell’s waste-to-energy and air-quality systems is scarce; UN Environment Programme data show demand for environmental engineers rose ~18% globally from 2020–2024 while supply grew ~6%.

That gap lets niche engineering firms and consultants push rates up; industry reports in 2025 record 12–20% higher bill rates for specialized emissions engineers versus general engineers.

Higher labor costs compress project EBITDA margins—KC Cottrell’s typical EPC margin of ~8–12% can be cut by 1–3 percentage points on projects needing heavy specialist input.

Logistics and Global Supply Chain Constraints

Suppliers of logistical services are critical for transporting KC Cottrell’s heavy pollution-control units; 2025 data show ocean freight rates rose 18% year-over-year, and port congestion added average demurrage of $1,200 per container in Q1 2025, raising project overhead and delaying site commissioning.

Consolidation among major carriers—top 5 lines control ~80% of Asia-Europe capacity in 2025—gives them leverage to set schedules and premium surcharges, increasing supplier bargaining power and forcing KC Cottrell to absorb or renegotiate higher logistics costs.

- Freight rates +18% YoY (2025)

- Average demurrage ~$1,200/container (Q1 2025)

- Top 5 carriers ≈80% Asia-Europe capacity (2025)

- Higher logistics costs raise project CAPEX and lead times

Proprietary Technology Licensing

When KC Cottrell must license third-party patents to meet client specs, suppliers gain strong leverage because that IP can be necessary for regulatory approval in markets like the EU and China.

License holders can impose high royalties—often 3–8% of project revenue—or restrictive terms, creating cost pressure and schedule risk for KC Cottrell; a single patent bottleneck can delay projects by months.

- IP needed for compliance gives suppliers leverage

- Royalties typically 3–8% of project revenue

- Restrictive terms raise cost and schedule risk

- One-patent bottleneck can delay projects by months

KC Cottrell squeezed: rising steel, freight, scarce engineers and 3–8% IP drag

KC Cottrell faces high supplier power from concentrated transformers/sensor makers, volatile steel and alloy prices (steel ~$780/ton in 2024; +18% 2021–23), scarce specialist engineers (+18% demand vs +6% supply 2020–24) and tight logistics (freight +18% YoY, demurrage ~$1,200/container Q1 2025), plus IP royalties 3–8% of project revenue that can delay projects.

| Factor | Key metric |

|---|---|

| Steel price (2024) | $780/ton |

| Freight change (2025) | +18% YoY |

| Demurrage (Q1 2025) | $1,200/container |

| Engineer demand vs supply (2020–24) | +18% vs +6% |

| IP royalties | 3–8% rev |

What is included in the product

Tailored exclusively for KC Cottrell, this Porter's Five Forces analysis uncovers competitive pressures, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers shaping the company's profitability.

A concise Porter's Five Forces one-sheet tailored to KC Cottrell—instantly clarifies competitive pressures and helps prioritize strategic moves.

Customers Bargaining Power

Concentration of Industrial Giants

The primary buyers for KC Cottrell—large power plants, steel mills, and cement firms—are a small set of high-value customers holding outsized leverage; by 2025 the top 20 accounts likely account for ~55% of revenues, so they can demand tougher terms. These giants increasingly push for longer warranties and extended payment terms—average receivable days rising from 60 in 2023 to about 85 by end-2025—pressuring margins and cash flow.

Rigorous Competitive Bidding Processes

Most environmental engineering projects go to transparent public or private tenders; in India and globally over 60% of contracts use competitive bidding, letting buyers pit firms against each other to cut prices.

For KC Cottrell this means sustaining extreme cost efficiency—its FY2024 gross margin 18.3% must hold while meeting buyers’ technical specs and often matching lowest bids.

High Performance and Compliance Risks

Customers demand strict performance guarantees because missing emission limits can trigger fines up to $50k–$100k per day or plant shutdowns; that risk pushes buyers to insist on indemnities and performance bonds.

Those clauses and bonds shift operational risk and capital cost to KC Cottrell, which in 2025 faces bond/guarantee costs typically 1–3% of contract value, squeezing margins on $5M+ projects.

Availability of Information and Alternatives

Modern industrial buyers are highly informed and often use in‑house engineering teams to test air pollution control systems, cutting information asymmetry that would favor KC Cottrell.

Transparent tech specs and published pricing let buyers compare KC Cottrell with global peers like Ducon, Thermax, and Babcock; procurement data shows over 60% of large EPCs request multi-vendor technical bids in 2024.

That visibility increases customer bargaining power, pressuring margins and contract terms for KC Cottrell.

- In‑house engineering raises technical scrutiny

- Published specs/pricing lower info gap

- 60%+ of large EPCs seek multi‑vendor bids (2024)

- Stronger buyer leverage reduces pricing power

Demand for Integrated Life-Cycle Services

Buyers now seek long-term partners offering construction plus maintenance and digital monitoring, pushing KC Cottrell to sell integrated life-cycle services rather than one-off systems.

This solution-as-a-service trend lets customers demand bundled hardware-software packages at lower total cost, boosting negotiating leverage and compressing margins on upfront sales.

By late 2025, customer-driven service-level agreements became market standard: 60–70% of new contracts in flue-gas-cleaning and emission-control sectors include multi-year maintenance and remote-monitoring clauses.

- Customers demand end-to-end service

- Bundled SaaS+hardware lowers TCO

- SLA terms standard by late 2025 (60–70% adoption)

- Increases buyer bargaining power, pressure on margins

Top buyers squeeze margins: longer DSOs, higher bond costs hit KC Cottrell

Major buyers (top 20 ≈55% revenue by 2025) wield high leverage, pushing longer payment terms (DSO 85 days in 2025 vs 60 in 2023) and tougher warranties, raising bond costs (1–3% of contract value) and squeezing KC Cottrell’s FY2024 gross margin (18.3%). Competitive tenders (≥60% contracts), multi-vendor bids (2024), in‑house engineering, and 60–70% SLA adoption by late 2025 amplify buyer bargaining power.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Top-20 revenue% | — | — | ≈55% |

| DSO (days) | 60 | — | 85 |

| Gross margin | — | 18.3% (FY2024) | — |

| Contracts via tender | — | ≥60% | — |

| SLA adoption | — | — | 60–70% |

| Bond/guarantee cost | — | — | 1–3% |

Preview Before You Purchase

KC Cottrell Porter's Five Forces Analysis

This preview shows the exact KC Cottrell Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

KC Cottrell faces moderate supplier power, niche customer segments, and evolving substitute technologies that together shape its competitive edge in air pollution control systems.

Barriers to entry and rivalry among specialized incumbents keep margins pressured, while regulatory trends create both risks and opportunities for growth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KC Cottrell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

KC Cottrell depends on a few global makers for high-voltage transformers and precision sensors used in its electrostatic precipitators, giving suppliers strong bargaining power; supplier concentration means price hikes of 8–12% in 2024 hit margins directly.

Raw Material Price Volatility

The construction of large-scale air pollution control systems uses tons of steel and nickel alloys; global steel plate prices rose ~18% in 2021–2023 and averaged $780/ton in 2024, directly lifting project costs KC Cottrell faces.

Commodity swings are volatile—iron ore spot jumped 40% in 2021–22—and EPC contracts limit immediate price recovery, squeezing margins until change orders are approved.

Major raw-material suppliers set market-driven prices; KC Cottrell often must absorb costs to keep schedules, raising working capital needs and contract risk.

Scarcity of Specialized Engineering Talent

The human capital to design KC Cottrell’s waste-to-energy and air-quality systems is scarce; UN Environment Programme data show demand for environmental engineers rose ~18% globally from 2020–2024 while supply grew ~6%.

That gap lets niche engineering firms and consultants push rates up; industry reports in 2025 record 12–20% higher bill rates for specialized emissions engineers versus general engineers.

Higher labor costs compress project EBITDA margins—KC Cottrell’s typical EPC margin of ~8–12% can be cut by 1–3 percentage points on projects needing heavy specialist input.

Logistics and Global Supply Chain Constraints

Suppliers of logistical services are critical for transporting KC Cottrell’s heavy pollution-control units; 2025 data show ocean freight rates rose 18% year-over-year, and port congestion added average demurrage of $1,200 per container in Q1 2025, raising project overhead and delaying site commissioning.

Consolidation among major carriers—top 5 lines control ~80% of Asia-Europe capacity in 2025—gives them leverage to set schedules and premium surcharges, increasing supplier bargaining power and forcing KC Cottrell to absorb or renegotiate higher logistics costs.

- Freight rates +18% YoY (2025)

- Average demurrage ~$1,200/container (Q1 2025)

- Top 5 carriers ≈80% Asia-Europe capacity (2025)

- Higher logistics costs raise project CAPEX and lead times

Proprietary Technology Licensing

When KC Cottrell must license third-party patents to meet client specs, suppliers gain strong leverage because that IP can be necessary for regulatory approval in markets like the EU and China.

License holders can impose high royalties—often 3–8% of project revenue—or restrictive terms, creating cost pressure and schedule risk for KC Cottrell; a single patent bottleneck can delay projects by months.

- IP needed for compliance gives suppliers leverage

- Royalties typically 3–8% of project revenue

- Restrictive terms raise cost and schedule risk

- One-patent bottleneck can delay projects by months

KC Cottrell squeezed: rising steel, freight, scarce engineers and 3–8% IP drag

KC Cottrell faces high supplier power from concentrated transformers/sensor makers, volatile steel and alloy prices (steel ~$780/ton in 2024; +18% 2021–23), scarce specialist engineers (+18% demand vs +6% supply 2020–24) and tight logistics (freight +18% YoY, demurrage ~$1,200/container Q1 2025), plus IP royalties 3–8% of project revenue that can delay projects.

| Factor | Key metric |

|---|---|

| Steel price (2024) | $780/ton |

| Freight change (2025) | +18% YoY |

| Demurrage (Q1 2025) | $1,200/container |

| Engineer demand vs supply (2020–24) | +18% vs +6% |

| IP royalties | 3–8% rev |

What is included in the product

Tailored exclusively for KC Cottrell, this Porter's Five Forces analysis uncovers competitive pressures, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers shaping the company's profitability.

A concise Porter's Five Forces one-sheet tailored to KC Cottrell—instantly clarifies competitive pressures and helps prioritize strategic moves.

Customers Bargaining Power

Concentration of Industrial Giants

The primary buyers for KC Cottrell—large power plants, steel mills, and cement firms—are a small set of high-value customers holding outsized leverage; by 2025 the top 20 accounts likely account for ~55% of revenues, so they can demand tougher terms. These giants increasingly push for longer warranties and extended payment terms—average receivable days rising from 60 in 2023 to about 85 by end-2025—pressuring margins and cash flow.

Rigorous Competitive Bidding Processes

Most environmental engineering projects go to transparent public or private tenders; in India and globally over 60% of contracts use competitive bidding, letting buyers pit firms against each other to cut prices.

For KC Cottrell this means sustaining extreme cost efficiency—its FY2024 gross margin 18.3% must hold while meeting buyers’ technical specs and often matching lowest bids.

High Performance and Compliance Risks

Customers demand strict performance guarantees because missing emission limits can trigger fines up to $50k–$100k per day or plant shutdowns; that risk pushes buyers to insist on indemnities and performance bonds.

Those clauses and bonds shift operational risk and capital cost to KC Cottrell, which in 2025 faces bond/guarantee costs typically 1–3% of contract value, squeezing margins on $5M+ projects.

Availability of Information and Alternatives

Modern industrial buyers are highly informed and often use in‑house engineering teams to test air pollution control systems, cutting information asymmetry that would favor KC Cottrell.

Transparent tech specs and published pricing let buyers compare KC Cottrell with global peers like Ducon, Thermax, and Babcock; procurement data shows over 60% of large EPCs request multi-vendor technical bids in 2024.

That visibility increases customer bargaining power, pressuring margins and contract terms for KC Cottrell.

- In‑house engineering raises technical scrutiny

- Published specs/pricing lower info gap

- 60%+ of large EPCs seek multi‑vendor bids (2024)

- Stronger buyer leverage reduces pricing power

Demand for Integrated Life-Cycle Services

Buyers now seek long-term partners offering construction plus maintenance and digital monitoring, pushing KC Cottrell to sell integrated life-cycle services rather than one-off systems.

This solution-as-a-service trend lets customers demand bundled hardware-software packages at lower total cost, boosting negotiating leverage and compressing margins on upfront sales.

By late 2025, customer-driven service-level agreements became market standard: 60–70% of new contracts in flue-gas-cleaning and emission-control sectors include multi-year maintenance and remote-monitoring clauses.

- Customers demand end-to-end service

- Bundled SaaS+hardware lowers TCO

- SLA terms standard by late 2025 (60–70% adoption)

- Increases buyer bargaining power, pressure on margins

Top buyers squeeze margins: longer DSOs, higher bond costs hit KC Cottrell

Major buyers (top 20 ≈55% revenue by 2025) wield high leverage, pushing longer payment terms (DSO 85 days in 2025 vs 60 in 2023) and tougher warranties, raising bond costs (1–3% of contract value) and squeezing KC Cottrell’s FY2024 gross margin (18.3%). Competitive tenders (≥60% contracts), multi-vendor bids (2024), in‑house engineering, and 60–70% SLA adoption by late 2025 amplify buyer bargaining power.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Top-20 revenue% | — | — | ≈55% |

| DSO (days) | 60 | — | 85 |

| Gross margin | — | 18.3% (FY2024) | — |

| Contracts via tender | — | ≥60% | — |

| SLA adoption | — | — | 60–70% |

| Bond/guarantee cost | — | — | 1–3% |

Preview Before You Purchase

KC Cottrell Porter's Five Forces Analysis

This preview shows the exact KC Cottrell Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.