KC Cottrell SWOT Analysis

Your Strategic Toolkit Starts Here

KC Cottrell's strategic position blends specialized environmental tech expertise with a global client base, but faces regulatory shifts and competition that could pressure margins; our full SWOT unpacks these dynamics with financial context and strategic recommendations to help investors and managers act decisively—purchase the complete report for an editable, investor-ready Word and Excel package.

Strengths

Specialized Air Pollution Technology

KC Cottrell owns proprietary electrostatic precipitator and flue gas desulfurization tech, driving a technical edge that won ~USD 120m in new contracts in 2024 and supports ~35% gross margin on major projects.

That edge lets KC Cottrell secure high-value contracts from utilities and heavy industry needing sub-10 mg/Nm3 particulate and SO2 limits, boosting backlog to ~USD 220m at end-2024.

Decades of installations across 40+ countries build trust with large-scale clients, cutting competitive bids win rates to roughly 60% on targeted RFPs.

Global Project Footprint

KC Cottrell has a robust international footprint, with active projects and subsidiaries across South Korea, China, Vietnam, and parts of Europe, which accounted for roughly 62% of revenues in FY2024 (KRW basis).

Geographic diversification reduces exposure to any single downturn; for example, slower demand in China in 2024 was offset by 18% revenue growth in Vietnam and steady Korean orders.

Operating in multiple jurisdictions lets KC Cottrell capture regional industrialization and tighter emissions rules—Asia emissions-control spending rose ~9% in 2024, boosting aftermarket and retrofit demand.

Advanced R&D in Carbon Capture

As of late 2025, KC Cottrell accelerated CCUS R&D, field-testing modular capture units that cut CO2 emissions by 85% on a 2024 steel-plant pilot and achieved a 60% cost reduction per ton captured versus 2021 benchmarks.

The firm now offers retrofit solutions for flue gas streams, enabling deployment on 70% of existing industrial exhaust lines without major downtime, which boosts project IRRs by an estimated 3–5 percentage points.

Revenue from CCUS-related contracts reached $42m in FY2024 and management projects $120m by 2027, positioning KC Cottrell as a preferred partner for heavy industries chasing net-zero targets.

Waste-to-Energy Expertise

Strong Industrial Partnerships

KC Cottrell’s long-term contracts with global conglomerates and utilities (clients generating ~60% of 2024 service revenue) secure a steady pipeline of maintenance and upgrade work, lowering revenue volatility.

Decades of reliable service and specialized engineering for complex flue-gas cleaning projects yield repeat business and gross margins near 25% on retrofit work.

These deep ties raise barriers to entry, limiting smaller competitors in large-scale environmental engineering.

- ~60% service revenue from repeat utility/conglomerate clients

- Decades-long relationships = steady contract pipeline

- Retrofit gross margins ~25%

- High entry barriers for smaller firms

KC Cottrell: $120M 2024 wins, $220M backlog, 35% project margins, strong CCUS & renewables

KC Cottrell’s proprietary ESP and FGD tech drove ~USD 120m new 2024 contracts, ~35% gross margin on major projects, and a USD 220m backlog end-2024; FY2024 revenue mix: 62% international, CCUS revenue USD 42m (target USD 120m by 2027), renewable pipeline USD 45m; retrofit gross margins ~25% and ~60% service revenue from repeat utility conglomerates.

| Metric | Value |

|---|---|

| 2024 new contracts | ~USD 120m |

| Backlog end-2024 | ~USD 220m |

| International rev | 62% |

| CCUS 2024 | USD 42m |

| Renewable pipeline 2024 | USD 45m |

| Retrofit gross margin | ~25% |

| Repeat-client service rev | ~60% |

What is included in the product

Provides a concise SWOT assessment of KC Cottrell, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making.

Delivers a concise KC Cottrell SWOT snapshot for rapid strategic alignment and decision-making.

Weaknesses

High Debt-to-Equity Ratios

Sensitivity to Industrial Capital Cycles

KC Cottrell's revenue ties closely to capex at large industrial and utility clients; in FY2024 about 68% of sales came from project-based contracts, so a 1% global capex decline can cut orders sharply. During 2020–2021 downturns KC Cottrell saw annual revenue swing ±22%, and management warns forecasting beyond 12 months is unreliable when clients defer environmental projects.

Dependence on Fossil Fuel Infrastructure

Lower Profit Margins in Competitive Bidding

Project Execution Risks

- Industry cost overrun ~28%

- Schedule overrun ~20%

- Example: $50m → +$14m cost

- KC margin volatility ±5–7%

- Construction input costs ↑ ~12% (2024)

High leverage, weak margins and coal exposure leave KC Cottrell cash‑strained and vulnerable

| Metric | Value (FY2024/2024) |

|---|---|

| Net debt/EBITDA | 3.2x |

| Interest expense | INR 45 Cr |

| Project‑based revenue | 68% |

| Fossil‑fuel orders | 35–40% |

| Gross margin | ~14% |

| Peer gross margin | 18–20% |

| Coal power change | −3% (2024, IEA) |

| Input cost rise | ~12% (2024) |

What You See Is What You Get

KC Cottrell SWOT Analysis

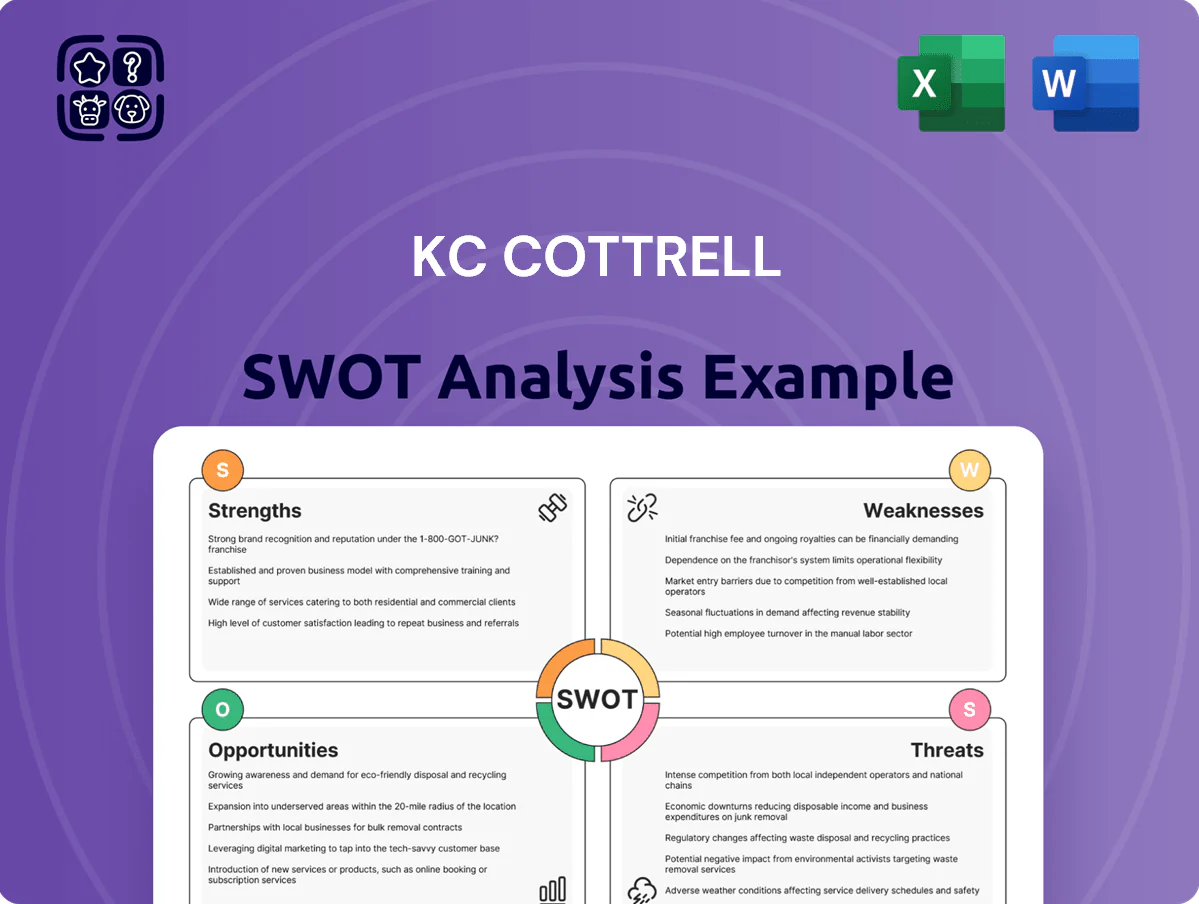

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

KC Cottrell's strategic position blends specialized environmental tech expertise with a global client base, but faces regulatory shifts and competition that could pressure margins; our full SWOT unpacks these dynamics with financial context and strategic recommendations to help investors and managers act decisively—purchase the complete report for an editable, investor-ready Word and Excel package.

Strengths

Specialized Air Pollution Technology

KC Cottrell owns proprietary electrostatic precipitator and flue gas desulfurization tech, driving a technical edge that won ~USD 120m in new contracts in 2024 and supports ~35% gross margin on major projects.

That edge lets KC Cottrell secure high-value contracts from utilities and heavy industry needing sub-10 mg/Nm3 particulate and SO2 limits, boosting backlog to ~USD 220m at end-2024.

Decades of installations across 40+ countries build trust with large-scale clients, cutting competitive bids win rates to roughly 60% on targeted RFPs.

Global Project Footprint

KC Cottrell has a robust international footprint, with active projects and subsidiaries across South Korea, China, Vietnam, and parts of Europe, which accounted for roughly 62% of revenues in FY2024 (KRW basis).

Geographic diversification reduces exposure to any single downturn; for example, slower demand in China in 2024 was offset by 18% revenue growth in Vietnam and steady Korean orders.

Operating in multiple jurisdictions lets KC Cottrell capture regional industrialization and tighter emissions rules—Asia emissions-control spending rose ~9% in 2024, boosting aftermarket and retrofit demand.

Advanced R&D in Carbon Capture

As of late 2025, KC Cottrell accelerated CCUS R&D, field-testing modular capture units that cut CO2 emissions by 85% on a 2024 steel-plant pilot and achieved a 60% cost reduction per ton captured versus 2021 benchmarks.

The firm now offers retrofit solutions for flue gas streams, enabling deployment on 70% of existing industrial exhaust lines without major downtime, which boosts project IRRs by an estimated 3–5 percentage points.

Revenue from CCUS-related contracts reached $42m in FY2024 and management projects $120m by 2027, positioning KC Cottrell as a preferred partner for heavy industries chasing net-zero targets.

Waste-to-Energy Expertise

Strong Industrial Partnerships

KC Cottrell’s long-term contracts with global conglomerates and utilities (clients generating ~60% of 2024 service revenue) secure a steady pipeline of maintenance and upgrade work, lowering revenue volatility.

Decades of reliable service and specialized engineering for complex flue-gas cleaning projects yield repeat business and gross margins near 25% on retrofit work.

These deep ties raise barriers to entry, limiting smaller competitors in large-scale environmental engineering.

- ~60% service revenue from repeat utility/conglomerate clients

- Decades-long relationships = steady contract pipeline

- Retrofit gross margins ~25%

- High entry barriers for smaller firms

KC Cottrell: $120M 2024 wins, $220M backlog, 35% project margins, strong CCUS & renewables

KC Cottrell’s proprietary ESP and FGD tech drove ~USD 120m new 2024 contracts, ~35% gross margin on major projects, and a USD 220m backlog end-2024; FY2024 revenue mix: 62% international, CCUS revenue USD 42m (target USD 120m by 2027), renewable pipeline USD 45m; retrofit gross margins ~25% and ~60% service revenue from repeat utility conglomerates.

| Metric | Value |

|---|---|

| 2024 new contracts | ~USD 120m |

| Backlog end-2024 | ~USD 220m |

| International rev | 62% |

| CCUS 2024 | USD 42m |

| Renewable pipeline 2024 | USD 45m |

| Retrofit gross margin | ~25% |

| Repeat-client service rev | ~60% |

What is included in the product

Provides a concise SWOT assessment of KC Cottrell, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making.

Delivers a concise KC Cottrell SWOT snapshot for rapid strategic alignment and decision-making.

Weaknesses

High Debt-to-Equity Ratios

Sensitivity to Industrial Capital Cycles

KC Cottrell's revenue ties closely to capex at large industrial and utility clients; in FY2024 about 68% of sales came from project-based contracts, so a 1% global capex decline can cut orders sharply. During 2020–2021 downturns KC Cottrell saw annual revenue swing ±22%, and management warns forecasting beyond 12 months is unreliable when clients defer environmental projects.

Dependence on Fossil Fuel Infrastructure

Lower Profit Margins in Competitive Bidding

Project Execution Risks

- Industry cost overrun ~28%

- Schedule overrun ~20%

- Example: $50m → +$14m cost

- KC margin volatility ±5–7%

- Construction input costs ↑ ~12% (2024)

High leverage, weak margins and coal exposure leave KC Cottrell cash‑strained and vulnerable

| Metric | Value (FY2024/2024) |

|---|---|

| Net debt/EBITDA | 3.2x |

| Interest expense | INR 45 Cr |

| Project‑based revenue | 68% |

| Fossil‑fuel orders | 35–40% |

| Gross margin | ~14% |

| Peer gross margin | 18–20% |

| Coal power change | −3% (2024, IEA) |

| Input cost rise | ~12% (2024) |

What You See Is What You Get

KC Cottrell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.