Beike Boston Consulting Group Matrix

Download Your Competitive Advantage

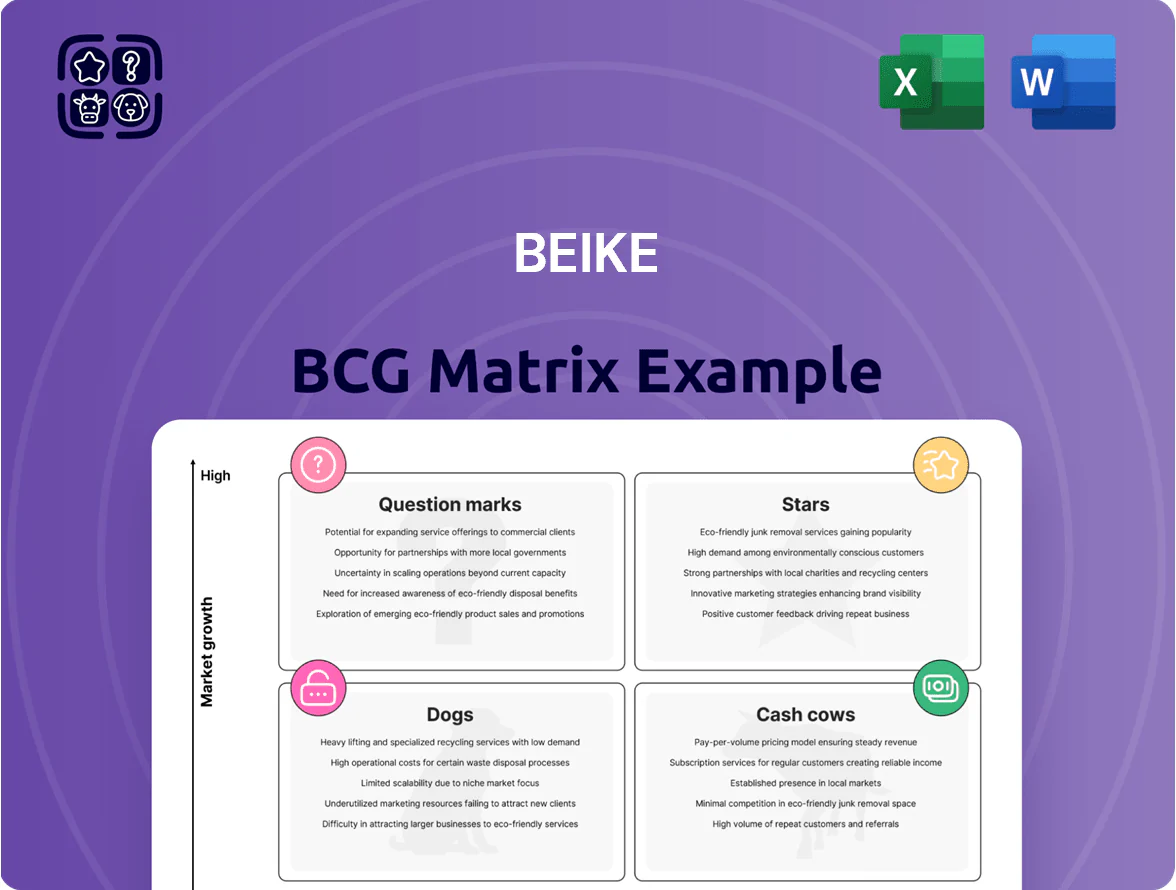

Beike's BCG Matrix snapshot shows where its offerings fall in growth and market-share dynamics—revealing potential Stars in fast-growing segments and Cash Cows funding core operations. This preview highlights strategic tensions and opportunities but stops short of the granular data and quadrant-level rationale you need to act. Purchase the full BCG Matrix for detailed placements, data-backed recommendations, and ready-to-use Word and Excel deliverables that guide investment and product decisions with confidence.

Stars

Home Renovation and Furnishing Services

As of late 2025, Home Renovation and Furnishing is Beike’s most aggressive growth engine, driving 28% revenue CAGR since 2023 and capturing ~22% share of China’s fragmented home services market (iResearch 2025).

After integrating Shengdu and Galabio in 2024–25, the segment scaled rapidly across tier‑1 and tier‑2 cities, adding 320 service centers and a 45% increase in GMV to RMB 18.6 billion in 2025.

It requires heavy capital: Beike invested RMB 3.2 billion in supply‑chain build‑out in 2025, pushing segment EBITDA negative but boosting consolidated EV/Revenue from 2.1x to 3.4x year‑over‑year.

Home Rental Management Services (Carefree Rent)

Beike’s Home Rental Management (Carefree Rent) sits in Stars: market for professionalized rentals in China grew ~18% CAGR 2018–2024, with long-term rentals market >RMB 1.2 trillion in 2024 due to demographic shifts and 2021–24 supportive policies for institutional leasing.

Carefree Rent’s decentralized manager model grew ~3x faster than legacy brokerage in 2023–24, reaching ~1.1 million managed units by end-2024, but needs continual tech CAPEX and ~RMB 200–300 per-unit monthly tenant-acq spend.

Ongoing investment in platform AI, IoT, and branding is required; with current unit economics trending positive, Carefree Rent can scale to lead China’s institutional rental market within 3–5 years.

Non-Real Estate Financial Services

Beike uses transaction data from 2024 (over 12M listings viewed monthly) to sell homeowner insurance and mortgage-adjacent credit, a high-growth fintech niche reporting 45% year-over-year revenue growth in Q3 2025.

Advanced ACN Technology Licensing

Advanced ACN Technology Licensing packages Beike's Agent Cooperation Network as a SaaS-like product for international and domestic partners, targeting a market where proptech spending reached about $12.5B globally in 2024; this vertical drove 28% year-on-year revenue growth for Beike's tech services in FY2024.

The ACN sets industry standards for transparency and efficiency—reducing transaction time by up to 35% in pilot deployments—and positions Beike as a first-to-market infrastructure provider despite significant R&D spend (R&D rose to 14% of revenue in 2024).

- Market: $12.5B proptech spend (2024)

- Revenue growth: 28% YoY tech services (FY2024)

- R&D: 14% of revenue (2024)

- Efficiency gain: up to 35% faster transactions (pilots)

Smart Home Integration and IoT

By embedding smart home tech into renovation and new-home packages, Beike enters a residential IoT market growing at ~18% CAGR (2020–25) and valued at $150B globally in 2025, tapping demand for energy-efficient, connected living.

This segment benefits from consumer preference—67% of homebuyers in 2024 preferred smart-ready homes—and regulatory pushes for efficiency that can raise selling prices by ~3–5%.

Beike currently leads in bridging physical real estate and digital homes via platform integrations with 120+ device OEMs and a pilot installing smart systems in 12,000 units in 2025.

What this estimate hides: integration costs and recurring service churn; gross margins depend on hardware mix and subscription uptake.

- Market size: $150B (2025)

- CAGR: ~18% (2020–25)

- Buyer preference: 67% (2024)

- Pilot units: 12,000 (2025)

- Price uplift: 3–5%

Beike’s high‑growth proptech & IoT arms: RMB18.6B GMV, 1.1M units, 28% CAGR

Stars: Beike’s Home Renovation, Carefree Rent, ACN tech, and smart‑home bundles are high‑growth, market‑leading units; 2023–25 CAGR ~28% (renovation) and 18% (rentals/IoT), 2025 GMV RMB18.6B, managed units 1.1M, R&D 14% rev, proptech market $12.5B (2024), IoT $150B (2025).

| Metric | Value |

|---|---|

| GMV 2025 | RMB18.6B |

| Managed units | 1.1M |

| R&D | 14% rev |

| Proptech market | $12.5B (2024) |

| IoT market | $150B (2025) |

What is included in the product

Comprehensive BCG Matrix review of Beike’s units with strategic advice on Stars, Cash Cows, Question Marks, and Dogs.

One-page Beike BCG Matrix placing each business unit in a quadrant for instant strategic clarity

Cash Cows

Existing Home Transaction Services

Existing home transaction services form Beike’s cash cow, holding roughly 45% share of China’s secondary housing listings as of Q4 2025 and driving stable GMV near RMB 1.2 trillion annually.

This mature segment delivers predictable operating cash flow—about RMB 12.5 billion EBITDA in FY 2024—while requiring low incremental capex to maintain network effects and agent platforms.

Profits here fund expansion: dividends support R&D and new verticals, contributing ~60% of capital deployed into mid-2025 growth initiatives.

New Home Sales Brokerage

Beike’s New Home Sales Brokerage remains a Cash Cow: in 2024 it handled ~1.2 million listings and generated ~RMB 18.5 billion in revenues, making it the preferred distribution channel for developers needing quick liquidity despite market dips.

High efficiency and margins stem from Beike’s 300,000-agent network and tech stack; brokerage gross margin exceeded 32% in FY2024, funding debt service and R&D programs like 2025 AI agent tools.

Lianjia Branded Stores

The self-operated Lianjia brand is the gold standard for service in premium urban districts, holding a stable ~18–22% market share in Beijing/Shanghai core areas as of 2025 and commanding higher ASPs. Physical stores are fully optimized, producing ~60–70% gross margin contribution to offline revenue while requiring minimal promotional spend versus franchised channels. These outlets generate steady free cash flow, funding platform ops and bolstering Beike’s credibility and cash reserves.

Transaction Support and Closing Services

Beike’s transaction support and closing services now operate at scale, delivering gross margins above 60% in 2025 as administrative and legal fees are embedded in every platform transfer, creating a toll-booth revenue stream that produced ~RMB 2.4bn in recurring income in 2024.

Established workflows and shared tech mean low incremental capex and high efficiency—average processing time fell to 3.2 days in 2024, cutting variable costs and locking in steady cash flows.

- High gross margin: >60% (2025)

- Recurring revenue: ~RMB 2.4bn (2024)

- Avg processing time: 3.2 days (2024)

- Minimal incremental capex; mature infrastructure

Platform Access and Membership Fees

Fees from third-party brokerages for accessing Beike's platform generated recurring revenue of about RMB 1.2 billion in 2024, offering stable cash flow with EBITDA margins above 60% since onboarding costs are sunk.

Growth is low—most major brokerages joined by 2023—so this segment is a high-share, low-growth BCG Cash Cow that mainly needs server maintenance and basic support.

- 2024 revenue ~RMB 1.2B

- EBITDA margin >60%

- Low CAGR prospect after 2023

- Minimal incremental capex: servers + support

Beike: RMB1.2T GMV, RMB12.5B EBITDA—high-margin, low-capex cash cows

Beike’s cash cows—existing-home transactions, new-home brokerage, Lianjia stores, and transaction services—generate steady cash: ~RMB 1.2T GMV (annual), ~RMB 12.5B EBITDA (2024), ~RMB 18.5B new-home revenue (2024), recurring fees RMB 2.4B + RMB 1.2B (2024); gross margins >60% (2025); low capex, high efficiency (3.2-day processing).

| Metric | Value |

|---|---|

| GMV | RMB 1.2T |

| EBITDA (2024) | RMB 12.5B |

| New-home rev (2024) | RMB 18.5B |

| Recurring fees (2024) | RMB 3.6B |

| Gross margin (2025) | >60% |

| Proc. time (2024) | 3.2 days |

Preview = Final Product

Beike BCG Matrix

The file you're previewing on this page is the exact Beike BCG Matrix report you'll receive after purchase; no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Beike's BCG Matrix snapshot shows where its offerings fall in growth and market-share dynamics—revealing potential Stars in fast-growing segments and Cash Cows funding core operations. This preview highlights strategic tensions and opportunities but stops short of the granular data and quadrant-level rationale you need to act. Purchase the full BCG Matrix for detailed placements, data-backed recommendations, and ready-to-use Word and Excel deliverables that guide investment and product decisions with confidence.

Stars

Home Renovation and Furnishing Services

As of late 2025, Home Renovation and Furnishing is Beike’s most aggressive growth engine, driving 28% revenue CAGR since 2023 and capturing ~22% share of China’s fragmented home services market (iResearch 2025).

After integrating Shengdu and Galabio in 2024–25, the segment scaled rapidly across tier‑1 and tier‑2 cities, adding 320 service centers and a 45% increase in GMV to RMB 18.6 billion in 2025.

It requires heavy capital: Beike invested RMB 3.2 billion in supply‑chain build‑out in 2025, pushing segment EBITDA negative but boosting consolidated EV/Revenue from 2.1x to 3.4x year‑over‑year.

Home Rental Management Services (Carefree Rent)

Beike’s Home Rental Management (Carefree Rent) sits in Stars: market for professionalized rentals in China grew ~18% CAGR 2018–2024, with long-term rentals market >RMB 1.2 trillion in 2024 due to demographic shifts and 2021–24 supportive policies for institutional leasing.

Carefree Rent’s decentralized manager model grew ~3x faster than legacy brokerage in 2023–24, reaching ~1.1 million managed units by end-2024, but needs continual tech CAPEX and ~RMB 200–300 per-unit monthly tenant-acq spend.

Ongoing investment in platform AI, IoT, and branding is required; with current unit economics trending positive, Carefree Rent can scale to lead China’s institutional rental market within 3–5 years.

Non-Real Estate Financial Services

Beike uses transaction data from 2024 (over 12M listings viewed monthly) to sell homeowner insurance and mortgage-adjacent credit, a high-growth fintech niche reporting 45% year-over-year revenue growth in Q3 2025.

Advanced ACN Technology Licensing

Advanced ACN Technology Licensing packages Beike's Agent Cooperation Network as a SaaS-like product for international and domestic partners, targeting a market where proptech spending reached about $12.5B globally in 2024; this vertical drove 28% year-on-year revenue growth for Beike's tech services in FY2024.

The ACN sets industry standards for transparency and efficiency—reducing transaction time by up to 35% in pilot deployments—and positions Beike as a first-to-market infrastructure provider despite significant R&D spend (R&D rose to 14% of revenue in 2024).

- Market: $12.5B proptech spend (2024)

- Revenue growth: 28% YoY tech services (FY2024)

- R&D: 14% of revenue (2024)

- Efficiency gain: up to 35% faster transactions (pilots)

Smart Home Integration and IoT

By embedding smart home tech into renovation and new-home packages, Beike enters a residential IoT market growing at ~18% CAGR (2020–25) and valued at $150B globally in 2025, tapping demand for energy-efficient, connected living.

This segment benefits from consumer preference—67% of homebuyers in 2024 preferred smart-ready homes—and regulatory pushes for efficiency that can raise selling prices by ~3–5%.

Beike currently leads in bridging physical real estate and digital homes via platform integrations with 120+ device OEMs and a pilot installing smart systems in 12,000 units in 2025.

What this estimate hides: integration costs and recurring service churn; gross margins depend on hardware mix and subscription uptake.

- Market size: $150B (2025)

- CAGR: ~18% (2020–25)

- Buyer preference: 67% (2024)

- Pilot units: 12,000 (2025)

- Price uplift: 3–5%

Beike’s high‑growth proptech & IoT arms: RMB18.6B GMV, 1.1M units, 28% CAGR

Stars: Beike’s Home Renovation, Carefree Rent, ACN tech, and smart‑home bundles are high‑growth, market‑leading units; 2023–25 CAGR ~28% (renovation) and 18% (rentals/IoT), 2025 GMV RMB18.6B, managed units 1.1M, R&D 14% rev, proptech market $12.5B (2024), IoT $150B (2025).

| Metric | Value |

|---|---|

| GMV 2025 | RMB18.6B |

| Managed units | 1.1M |

| R&D | 14% rev |

| Proptech market | $12.5B (2024) |

| IoT market | $150B (2025) |

What is included in the product

Comprehensive BCG Matrix review of Beike’s units with strategic advice on Stars, Cash Cows, Question Marks, and Dogs.

One-page Beike BCG Matrix placing each business unit in a quadrant for instant strategic clarity

Cash Cows

Existing Home Transaction Services

Existing home transaction services form Beike’s cash cow, holding roughly 45% share of China’s secondary housing listings as of Q4 2025 and driving stable GMV near RMB 1.2 trillion annually.

This mature segment delivers predictable operating cash flow—about RMB 12.5 billion EBITDA in FY 2024—while requiring low incremental capex to maintain network effects and agent platforms.

Profits here fund expansion: dividends support R&D and new verticals, contributing ~60% of capital deployed into mid-2025 growth initiatives.

New Home Sales Brokerage

Beike’s New Home Sales Brokerage remains a Cash Cow: in 2024 it handled ~1.2 million listings and generated ~RMB 18.5 billion in revenues, making it the preferred distribution channel for developers needing quick liquidity despite market dips.

High efficiency and margins stem from Beike’s 300,000-agent network and tech stack; brokerage gross margin exceeded 32% in FY2024, funding debt service and R&D programs like 2025 AI agent tools.

Lianjia Branded Stores

The self-operated Lianjia brand is the gold standard for service in premium urban districts, holding a stable ~18–22% market share in Beijing/Shanghai core areas as of 2025 and commanding higher ASPs. Physical stores are fully optimized, producing ~60–70% gross margin contribution to offline revenue while requiring minimal promotional spend versus franchised channels. These outlets generate steady free cash flow, funding platform ops and bolstering Beike’s credibility and cash reserves.

Transaction Support and Closing Services

Beike’s transaction support and closing services now operate at scale, delivering gross margins above 60% in 2025 as administrative and legal fees are embedded in every platform transfer, creating a toll-booth revenue stream that produced ~RMB 2.4bn in recurring income in 2024.

Established workflows and shared tech mean low incremental capex and high efficiency—average processing time fell to 3.2 days in 2024, cutting variable costs and locking in steady cash flows.

- High gross margin: >60% (2025)

- Recurring revenue: ~RMB 2.4bn (2024)

- Avg processing time: 3.2 days (2024)

- Minimal incremental capex; mature infrastructure

Platform Access and Membership Fees

Fees from third-party brokerages for accessing Beike's platform generated recurring revenue of about RMB 1.2 billion in 2024, offering stable cash flow with EBITDA margins above 60% since onboarding costs are sunk.

Growth is low—most major brokerages joined by 2023—so this segment is a high-share, low-growth BCG Cash Cow that mainly needs server maintenance and basic support.

- 2024 revenue ~RMB 1.2B

- EBITDA margin >60%

- Low CAGR prospect after 2023

- Minimal incremental capex: servers + support

Beike: RMB1.2T GMV, RMB12.5B EBITDA—high-margin, low-capex cash cows

Beike’s cash cows—existing-home transactions, new-home brokerage, Lianjia stores, and transaction services—generate steady cash: ~RMB 1.2T GMV (annual), ~RMB 12.5B EBITDA (2024), ~RMB 18.5B new-home revenue (2024), recurring fees RMB 2.4B + RMB 1.2B (2024); gross margins >60% (2025); low capex, high efficiency (3.2-day processing).

| Metric | Value |

|---|---|

| GMV | RMB 1.2T |

| EBITDA (2024) | RMB 12.5B |

| New-home rev (2024) | RMB 18.5B |

| Recurring fees (2024) | RMB 3.6B |

| Gross margin (2025) | >60% |

| Proc. time (2024) | 3.2 days |

Preview = Final Product

Beike BCG Matrix

The file you're previewing on this page is the exact Beike BCG Matrix report you'll receive after purchase; no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional use.