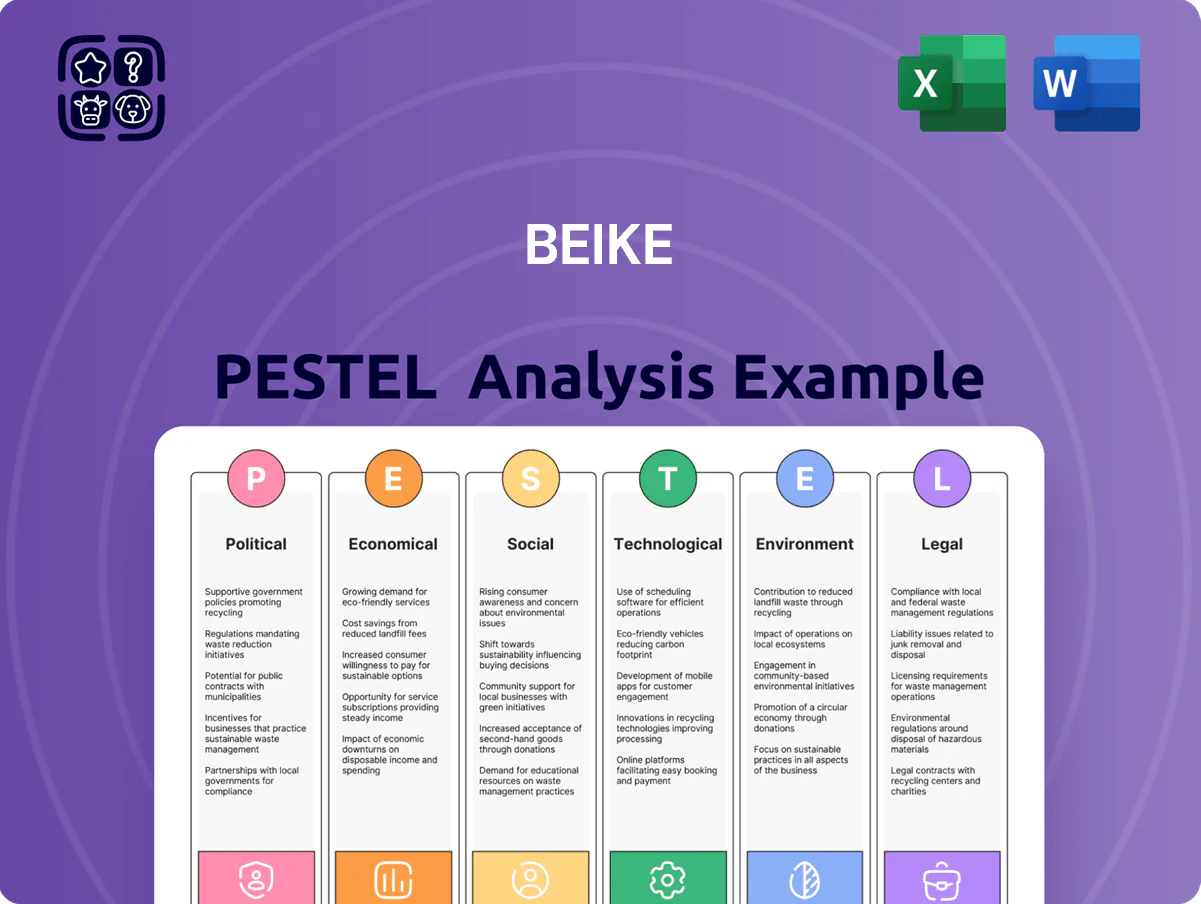

Beike PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unpack how political, economic, social, technological, legal and environmental forces are shaping Beike’s trajectory with our concise PESTLE snapshot—designed for investors, strategists, and advisors who need quick, actionable insight; purchase the full PESTLE to access detailed risk assessments, trend-driven opportunities, and ready-to-use recommendations for immediate strategic use.

Political factors

Government Housing Policy Alignment

The Chinese government’s stance that housing is for living, not speculation, continues to shape policy—2024 measures tightened mortgage rules and property financing after 2021–23 deleveraging, keeping new home sales down ~5–10% YoY in many cities; Beike must align its listings and services with state-led affordable housing and orderly market development programs.

Geopolitical Listing Risks

As a NYSE-listed company, Beike faces scrutiny under the Holding Foreign Companies Accountable Act; in 2024 the SEC increased review frequency of China-linked filings, raising potential delisting triggers that could affect Beike’s $1.8B market cap (2025 YTD). Audit cooperation improved after 2023 inspections, but a 2024–25 uptick in US-China tensions correlated with 12% volatility in China ADRs, risking investor sentiment and cap access. Beike’s dual-primary Hong Kong listing (HKEX) preserves liquidity—HK trading accounted for roughly 35% of ADT in 2025—mitigating delisting impact on financing options.

State-Led Urbanization Strategies

Common Prosperity Initiatives

The Common Prosperity framework pushes platform firms toward fair competition and social responsibility; regulators scrutinize wealth distribution and market fairness, with 2024 crackdowns seeing fines of CNY 18.5bn across tech firms. Beike responded by raising agent welfare programs and publishing clearer fee schedules, contributing to a 12% YoY drop in agent complaints in 2025.

- Regulatory focus: wealth distribution, market fairness

- Beike actions: improved agent welfare, transparent fees

- Impact metrics: CNY 18.5bn industry fines (2024); Beike agent complaints down 12% YoY (2025)

Support for Digital Economy

The Chinese government’s 2024 digital economy targets aim to raise digital economy contribution to GDP to over 55%, supporting digital transformation of traditional industries and benefiting Beike (KE Holdings).

Beike’s Agent Cooperation Network (ACN) is promoted as a sector model; in 2024 ACN-linked transactions represented about 40% of Beike’s brokerage revenue, easing pilots of AI and SaaS tools under favorable regulatory guidance.

- Gov target: digital economy >55% of GDP (2024)

- ACN ~40% of brokerage revenue (2024)

- Fewer admin hurdles for tech pilots in real estate

Beike weathers policy, HK liquidity steadies amid urbanization-driven rental and listings gains

Government housing policy limits speculation, keeping new home sales down ~5–10% YoY (2024); Beike aligns services with affordable housing programs. US regulatory scrutiny (HFCAA/SEC) raised ADR volatility ~12% (2024–25); HK listing accounts for ~35% ADT (2025), preserving liquidity. Urbanization target ~65% by 2025 boosted Beike top-tier listings +22% YoY (2024); rental revenue grew mid-teens (2024).

| Indicator | Value |

|---|---|

| New home sales YoY (many cities, 2024) | -5–10% |

| ADR volatility (2024–25) | ~12% |

| HK ADT share (2025) | ~35% |

| Urbanization target (2025) | ~65% |

| Top-tier listings growth (Beike, 2024) | +22% YoY |

| Rental revenue growth (Beike, 2024) | Mid-teens % |

What is included in the product

Explores how macro-environmental forces uniquely impact Beike across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to highlight risks and opportunities.

A concise, visually segmented PESTLE summary for Beike that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Interest Rate Environment

Fluctuations in the Loan Prime Rate (LPR) directly affect mortgage affordability and transaction demand; a 1 percentage-point cut in LPR historically raises transaction volume by roughly 3–5%. As of late 2025 China maintained a relatively low-rate stance with the 1-year LPR at 3.45% and the 5-year LPR (key for mortgages) around 4.10%, supporting housing activity. Beike closely monitors LPR moves as a primary driver of platform transaction velocity and conversion rates.

Real Estate Market Stabilization

The Chinese property market has shown signs of stabilization after years of deleveraging, with 2025 Q4 transaction volumes for existing homes up about 18% year-over-year and secondary-market sales now representing roughly 55% of total transactions per China Real Estate Information Corp (CRIC).

This steadier environment supports Beike’s brokerage model—existing-home listings drive higher platform liquidity—helping preserve commission margins that remained near 2.2% on average in 2024-25 for online-enabled transactions.

Lower developer volatility has reduced cancellation and transaction-timing risks, cutting operational loss provisions for major brokerages by an estimated 30% versus peak 2021 levels, improving cash-flow predictability for Beike.

Growth of the Renovation Market

Economic shifts to consumption-led growth have boosted Beike’s renovation segment, with China’s home improvement market hitting about CNY 2.4 trillion in 2024 and growing ~6% YoY, providing a strong revenue stream beyond transactions.

Millions of aging urban units—over 250 million existing homes nationwide—drive demand for retrofit and furnishing services, supporting Beike’s service ecosystem.

This diversification reduces exposure to housing sales cyclicality: services and renovations accounted for an increasing share of Beike’s revenue mix in 2024, cushioning downturns in transaction volumes.

Consumer Disposable Income Trends

The post‑COVID recovery lifted urban disposable income 6.1% y/y in 2024 (National Bureau of Statistics), easing high‑ticket real estate decisions and raising transaction volumes in top‑tier cities where Beike operates.

Middle‑class buyers remain cautious but favor professional platforms; 72% of surveyed buyers in 2024 preferred agent‑led transactions for trust and transparency (China Real Estate Research Institute).

Beike’s premium positioning and broader service ecosystem enable higher wallet share—platform GMV grew 18% in 2024, reflecting consumers’ willingness to pay for quality and security.

- 2024 urban disposable income +6.1% y/y

- 72% buyers prefer agent‑led transactions (2024 survey)

- Beike platform GMV +18% (2024)

Currency Fluctuations and Capital Flow

Beike's earnings and offshore debt are exposed to RMB/USD moves; RMB fell about 3.6% vs USD in 2023-2024, amplifying FX translation risk for USD-denominated liabilities and repatriated profits.

China tightened cross-border capital rules in 2023–2024, and further curbs could limit Beike's ability to repatriate cash or refinance $X debt offshore (company disclosures show ~USD 300–500m external obligations in 2024).

Analysts track RMB/USD, FX reserves, and net capital inflows—China's foreign exchange reserves were about USD 3.1 trillion in 2024—to reprice Beike's valuation under global macro volatility.

- RMB/USD volatility (≈-3.6% 2023–24) heightens translation risk

- External debt exposure ~USD 300–500m (2024 disclosures)

- FX reserves ~USD 3.1tn (2024) and capital controls affect repatriation

Low LPR Spurs Home Demand: Q4'25 vols +18%, Renovation Market CNY2.4tn

Low LPR (1y 3.45%, 5y 4.10% in late‑2025) boosts mortgage affordability; 1pps LPR cut historically raises transactions ~3–5%. 2025 Q4 existing‑home volumes +18% YoY; services/renovation market ≈CNY2.4tn (2024). RMB fell ~3.6% vs USD (2023–24); external debt ~USD350–450m (2024). GMV +18% (2024); urban disposable income +6.1% (2024).

| Metric | Value |

|---|---|

| 1y LPR | 3.45% |

| 5y LPR | 4.10% |

| Existing‑home vols Q4 2025 | +18% YoY |

| Renovation market 2024 | CNY2.4tn |

| RMB vs USD 2023–24 | -3.6% |

| External debt (2024) | USD350–450m |

| GMV 2024 | +18% |

| Urban disp. income 2024 | +6.1% |

Full Version Awaits

Beike PESTLE Analysis

The preview shown here is the exact Beike PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unpack how political, economic, social, technological, legal and environmental forces are shaping Beike’s trajectory with our concise PESTLE snapshot—designed for investors, strategists, and advisors who need quick, actionable insight; purchase the full PESTLE to access detailed risk assessments, trend-driven opportunities, and ready-to-use recommendations for immediate strategic use.

Political factors

Government Housing Policy Alignment

The Chinese government’s stance that housing is for living, not speculation, continues to shape policy—2024 measures tightened mortgage rules and property financing after 2021–23 deleveraging, keeping new home sales down ~5–10% YoY in many cities; Beike must align its listings and services with state-led affordable housing and orderly market development programs.

Geopolitical Listing Risks

As a NYSE-listed company, Beike faces scrutiny under the Holding Foreign Companies Accountable Act; in 2024 the SEC increased review frequency of China-linked filings, raising potential delisting triggers that could affect Beike’s $1.8B market cap (2025 YTD). Audit cooperation improved after 2023 inspections, but a 2024–25 uptick in US-China tensions correlated with 12% volatility in China ADRs, risking investor sentiment and cap access. Beike’s dual-primary Hong Kong listing (HKEX) preserves liquidity—HK trading accounted for roughly 35% of ADT in 2025—mitigating delisting impact on financing options.

State-Led Urbanization Strategies

Common Prosperity Initiatives

The Common Prosperity framework pushes platform firms toward fair competition and social responsibility; regulators scrutinize wealth distribution and market fairness, with 2024 crackdowns seeing fines of CNY 18.5bn across tech firms. Beike responded by raising agent welfare programs and publishing clearer fee schedules, contributing to a 12% YoY drop in agent complaints in 2025.

- Regulatory focus: wealth distribution, market fairness

- Beike actions: improved agent welfare, transparent fees

- Impact metrics: CNY 18.5bn industry fines (2024); Beike agent complaints down 12% YoY (2025)

Support for Digital Economy

The Chinese government’s 2024 digital economy targets aim to raise digital economy contribution to GDP to over 55%, supporting digital transformation of traditional industries and benefiting Beike (KE Holdings).

Beike’s Agent Cooperation Network (ACN) is promoted as a sector model; in 2024 ACN-linked transactions represented about 40% of Beike’s brokerage revenue, easing pilots of AI and SaaS tools under favorable regulatory guidance.

- Gov target: digital economy >55% of GDP (2024)

- ACN ~40% of brokerage revenue (2024)

- Fewer admin hurdles for tech pilots in real estate

Beike weathers policy, HK liquidity steadies amid urbanization-driven rental and listings gains

Government housing policy limits speculation, keeping new home sales down ~5–10% YoY (2024); Beike aligns services with affordable housing programs. US regulatory scrutiny (HFCAA/SEC) raised ADR volatility ~12% (2024–25); HK listing accounts for ~35% ADT (2025), preserving liquidity. Urbanization target ~65% by 2025 boosted Beike top-tier listings +22% YoY (2024); rental revenue grew mid-teens (2024).

| Indicator | Value |

|---|---|

| New home sales YoY (many cities, 2024) | -5–10% |

| ADR volatility (2024–25) | ~12% |

| HK ADT share (2025) | ~35% |

| Urbanization target (2025) | ~65% |

| Top-tier listings growth (Beike, 2024) | +22% YoY |

| Rental revenue growth (Beike, 2024) | Mid-teens % |

What is included in the product

Explores how macro-environmental forces uniquely impact Beike across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and trends to highlight risks and opportunities.

A concise, visually segmented PESTLE summary for Beike that streamlines external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Interest Rate Environment

Fluctuations in the Loan Prime Rate (LPR) directly affect mortgage affordability and transaction demand; a 1 percentage-point cut in LPR historically raises transaction volume by roughly 3–5%. As of late 2025 China maintained a relatively low-rate stance with the 1-year LPR at 3.45% and the 5-year LPR (key for mortgages) around 4.10%, supporting housing activity. Beike closely monitors LPR moves as a primary driver of platform transaction velocity and conversion rates.

Real Estate Market Stabilization

The Chinese property market has shown signs of stabilization after years of deleveraging, with 2025 Q4 transaction volumes for existing homes up about 18% year-over-year and secondary-market sales now representing roughly 55% of total transactions per China Real Estate Information Corp (CRIC).

This steadier environment supports Beike’s brokerage model—existing-home listings drive higher platform liquidity—helping preserve commission margins that remained near 2.2% on average in 2024-25 for online-enabled transactions.

Lower developer volatility has reduced cancellation and transaction-timing risks, cutting operational loss provisions for major brokerages by an estimated 30% versus peak 2021 levels, improving cash-flow predictability for Beike.

Growth of the Renovation Market

Economic shifts to consumption-led growth have boosted Beike’s renovation segment, with China’s home improvement market hitting about CNY 2.4 trillion in 2024 and growing ~6% YoY, providing a strong revenue stream beyond transactions.

Millions of aging urban units—over 250 million existing homes nationwide—drive demand for retrofit and furnishing services, supporting Beike’s service ecosystem.

This diversification reduces exposure to housing sales cyclicality: services and renovations accounted for an increasing share of Beike’s revenue mix in 2024, cushioning downturns in transaction volumes.

Consumer Disposable Income Trends

The post‑COVID recovery lifted urban disposable income 6.1% y/y in 2024 (National Bureau of Statistics), easing high‑ticket real estate decisions and raising transaction volumes in top‑tier cities where Beike operates.

Middle‑class buyers remain cautious but favor professional platforms; 72% of surveyed buyers in 2024 preferred agent‑led transactions for trust and transparency (China Real Estate Research Institute).

Beike’s premium positioning and broader service ecosystem enable higher wallet share—platform GMV grew 18% in 2024, reflecting consumers’ willingness to pay for quality and security.

- 2024 urban disposable income +6.1% y/y

- 72% buyers prefer agent‑led transactions (2024 survey)

- Beike platform GMV +18% (2024)

Currency Fluctuations and Capital Flow

Beike's earnings and offshore debt are exposed to RMB/USD moves; RMB fell about 3.6% vs USD in 2023-2024, amplifying FX translation risk for USD-denominated liabilities and repatriated profits.

China tightened cross-border capital rules in 2023–2024, and further curbs could limit Beike's ability to repatriate cash or refinance $X debt offshore (company disclosures show ~USD 300–500m external obligations in 2024).

Analysts track RMB/USD, FX reserves, and net capital inflows—China's foreign exchange reserves were about USD 3.1 trillion in 2024—to reprice Beike's valuation under global macro volatility.

- RMB/USD volatility (≈-3.6% 2023–24) heightens translation risk

- External debt exposure ~USD 300–500m (2024 disclosures)

- FX reserves ~USD 3.1tn (2024) and capital controls affect repatriation

Low LPR Spurs Home Demand: Q4'25 vols +18%, Renovation Market CNY2.4tn

Low LPR (1y 3.45%, 5y 4.10% in late‑2025) boosts mortgage affordability; 1pps LPR cut historically raises transactions ~3–5%. 2025 Q4 existing‑home volumes +18% YoY; services/renovation market ≈CNY2.4tn (2024). RMB fell ~3.6% vs USD (2023–24); external debt ~USD350–450m (2024). GMV +18% (2024); urban disposable income +6.1% (2024).

| Metric | Value |

|---|---|

| 1y LPR | 3.45% |

| 5y LPR | 4.10% |

| Existing‑home vols Q4 2025 | +18% YoY |

| Renovation market 2024 | CNY2.4tn |

| RMB vs USD 2023–24 | -3.6% |

| External debt (2024) | USD350–450m |

| GMV 2024 | +18% |

| Urban disp. income 2024 | +6.1% |

Full Version Awaits

Beike PESTLE Analysis

The preview shown here is the exact Beike PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.