Kearny Bank Porter's Five Forces Analysis

From Overview to Strategy Blueprint

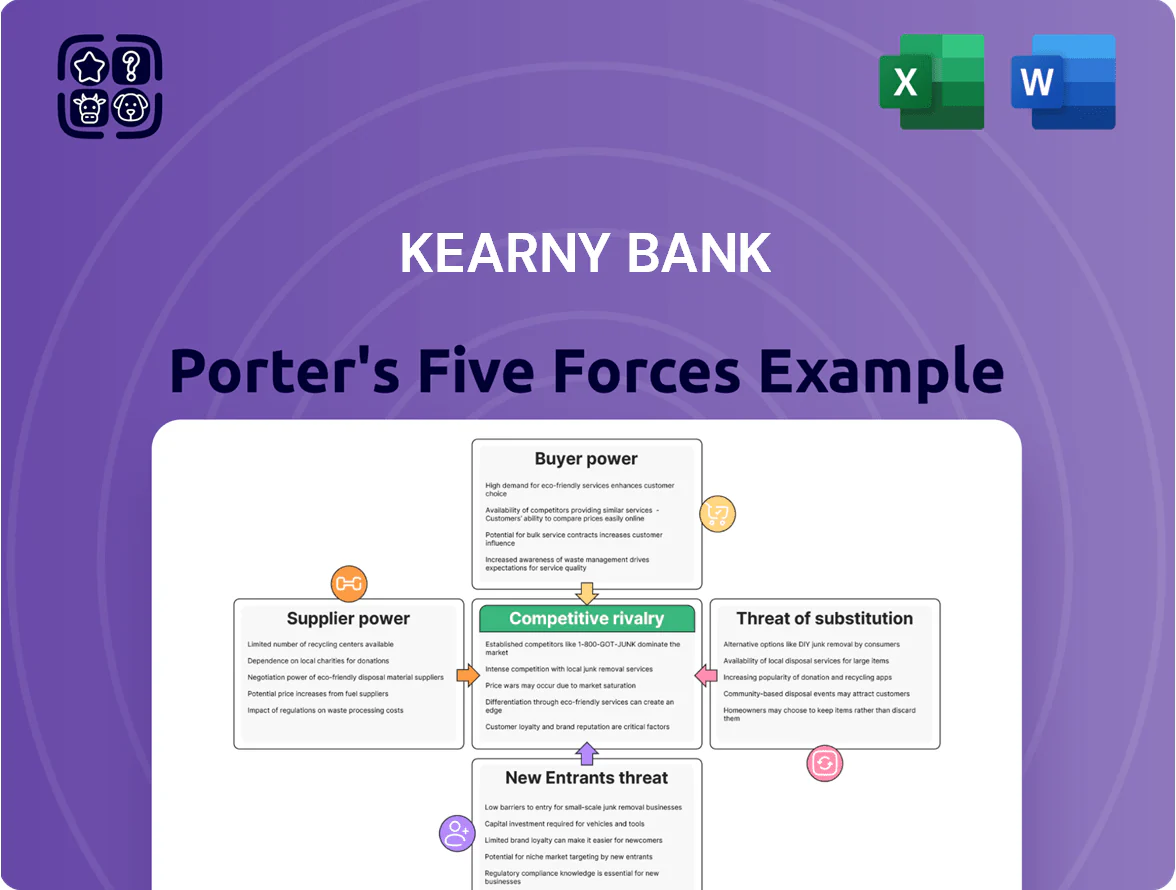

Kearny Bank faces moderate competitive intensity: strong local relationships and stable deposit bases counterbalanced by regional banks, fintechs, and evolving regulations that raise threat levels for margins and growth.

Suppliers Bargaining Power

Cost of Core Deposits

As of late 2025, individual and business depositors—Kearny Bank’s primary capital suppliers—are pushing for yields near 4.5–5.0% on retail deposits and 5.0–5.5% on business sweep accounts, giving them strong leverage to shift funds to banks or money market funds offering better returns.

Technology and Core Banking Vendors

The bank relies on a handful of specialized core banking and digital vendors—often 2–4 key suppliers—giving them high bargaining power since system replacement can take 18–36 months and cost $10–50m for a regional bank of Kearny’s scale.

Operational risk from migration and regulatory validation raises exit costs, so vendors can demand premium pricing for advanced cybersecurity and AI features, with enterprise fees rising 10–25% year-over-year in 2024–25.

Human Capital and Specialized Talent

The New York–New Jersey metro area commands top banking talent; average commercial-banking salaries rose 6.2% in 2024 to about $142,000, and compliance roles saw 8% wage growth, giving labor suppliers leverage to demand higher pay and hybrid schedules. Kearny Bank must compete with national banks and fintechs that spent $1.8B on tech hiring in 2024, pressuring retention and raising hiring costs by an estimated 10–15%.

Wholesale Funding Sources

Institutional lenders like the Federal Home Loan Bank (FHLB) act as key secondary liquidity suppliers for Kearny Bank; in 2024 FHLB advances nationwide totaled about $1.1 trillion, and their collateral and spread pricing directly affect Kearny’s funding costs and usable liquidity.

When markets tighten, higher advance rates or stricter collateral reduce Kearny’s capacity to fund loan growth; for example, a 50 bps rise in advance spreads can raise funding costs materially versus deposit funding.

- FHLB advances ≈ $1.1T (2024)

- Collateral rules limit usable assets

- +50 bps spread raises funding cost

Regulatory and Legal Services

Specialized legal and audit firms retain strong supplier power for Kearny Bank as post-2023 regulatory shifts and 2024–25 enforcement trends raise compliance complexity; top-tier counsel scarcity means the bank cannot cheaply replicate these services internally.

High stakes of non-compliance (fines averaged $220k per enforcement action for regional banks in 2024) make switching costly, so fees for these firms act as a fixed drag on non-interest expenses.

- 2024 enforcement fines avg $220,000 (regional banks)

- Top-tier legal rates $600–1,200/hr

- Compliance outsourcing ≈2–4% of non-interest expenses

High supplier power: deposit rates, costly vendors & FHLB drive Kearny’s elevated costs

Suppliers hold high bargaining power: depositors demand ~4.5–5.5% yields, core tech vendors charge premiums (replacement cost $10–50m, 18–36 months), FHLB advances ~$1.1T (2024) set liquidity costs, and legal/compliance fees (top rates $600–1,200/hr) raise non-interest expenses; switching costs and regulatory risk keep Kearny dependent.

| Supplier | Key Metric (2024–25) |

|---|---|

| Depositors | Retail 4.5–5.0%, Business 5.0–5.5% |

| Core vendors | Replacement $10–50m; 18–36 months |

| FHLB | Advances ≈ $1.1T; +50bps raises funding cost |

| Legal/compliance | Rates $600–1,200/hr; fines avg $220k |

What is included in the product

Tailored Porter’s Five Forces analysis for Kearny Bank uncovering competitive drivers, customer and supplier influence, entry barriers, substitute threats, and strategic levers shaping its pricing, profitability, and market defense.

Compact Porter's Five Forces snapshot for Kearny Bank—quickly assess competitive pressure and regulatory risk to guide strategic or investment decisions.

Customers Bargaining Power

Switching Costs for Retail Customers

The bargaining power of retail customers is high: digital onboarding cuts switching costs so moving personal accounts takes under 20 minutes and 42% of US consumers switched banks in 2023 for better rates or fees (2024 FDIC trend).

In Kearny Bank’s NJ/NY markets, easy online comparison of rates and fees means customers will jump for marginal gains; price sensitivity rose 7% in regional surveys through 2024.

Kearny must offset this by doubling down on high-touch service and community loyalty—branch events, local sponsorships, and relationship managers raised retention 3–5 ppt in comparable regional banks in 2024.

Price Sensitivity in Mortgage Lending

Borrowers seeking residential mortgages are highly price-sensitive and often use brokers to secure the lowest rates; in 2024 mortgage shopping reduced average lender spread by ~25 basis points, per industry data. Kearny Bank, focused on residential lending, faces competition from national banks with scale-driven cost edges and lower funding costs—large banks held 52% of mortgage originations in 2024. That scale forces Kearny to act as a price taker on many standard products, limiting spread expansion and pressuring net interest margins.

Concentration of Commercial Real Estate Clients

Information Transparency and Comparison Tools

By late 2025, real-time comparison platforms made CD rates and loan terms effectively transparent—customers see offers from top regional banks and fintechs instantly, cutting Kearny Bank’s information advantage.

This reduced asymmetry shifts bargaining power to customers, who now prioritize service and tailored advice over small rate differentials; 72% of consumers reported using comparison tools for deposit decisions in 2024 surveys.

Kearny must emphasize value-added services and personalized financial advice—relationship pricing, bundled planning, and advisor-led products—that comparison sites cannot price-match easily.

- Comparison platforms → near-perfect info on rates by 2025

- 72% of customers used tools for deposit choices (2024)

- Shift: price sensitivity down, service/personalization up

- Action: focus on advisor services, bundled value, relationship pricing

Demand for Digital and Mobile Excellence

Modern customers treat seamless digital banking as table stakes; 73% of US consumers (2024 EY Global Banking Survey) say they would switch banks for a better digital experience, giving customers high exit power.

If Kearny Bank's mobile app or portal lags neobanks — which average 4.6/5 app ratings and faster onboarding — primary deposits can migrate, hurting fee and deposit growth.

That risk forces continuous capex: regional banks spent ~0.9–1.2% of assets on tech in 2023, so Kearny likely needs similar ongoing investment to stay competitive.

- 73% willing to switch for better digital service

- Neobanks avg 4.6/5 app ratings

- Regional bank tech spend ~0.9–1.2% of assets (2023)

High customer power: 72% comparison use, 73% switch for digital — CRE pricing under pressure

Customer bargaining power is high: 72% use comparison tools (2024) and 73% would switch for better digital service, pushing Kearny toward relationship pricing and advisor-led bundles; top CRE borrowers (typical loans $20–150m) can secure 50–150 bps concessions, and top-5 loan exposure risks ~3–6% NII hit (2024).

| Metric | Value (year) |

|---|---|

| Comparison-tool users | 72% (2024) |

| Willing to switch for digital | 73% (2024) |

| Neobank app avg rating | 4.6/5 (2024) |

| Regional bank tech spend | 0.9–1.2% assets (2023) |

| Top-borrower concession | 50–150 bps (2024) |

| Top-5 loans NII sensitivity | ~3–6% (2024) |

What You See Is What You Get

Kearny Bank Porter's Five Forces Analysis

This preview shows the exact Kearny Bank Porter’s Five Forces analysis you'll receive after purchase—fully formatted, comprehensive, and ready to use with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Kearny Bank faces moderate competitive intensity: strong local relationships and stable deposit bases counterbalanced by regional banks, fintechs, and evolving regulations that raise threat levels for margins and growth.

Suppliers Bargaining Power

Cost of Core Deposits

As of late 2025, individual and business depositors—Kearny Bank’s primary capital suppliers—are pushing for yields near 4.5–5.0% on retail deposits and 5.0–5.5% on business sweep accounts, giving them strong leverage to shift funds to banks or money market funds offering better returns.

Technology and Core Banking Vendors

The bank relies on a handful of specialized core banking and digital vendors—often 2–4 key suppliers—giving them high bargaining power since system replacement can take 18–36 months and cost $10–50m for a regional bank of Kearny’s scale.

Operational risk from migration and regulatory validation raises exit costs, so vendors can demand premium pricing for advanced cybersecurity and AI features, with enterprise fees rising 10–25% year-over-year in 2024–25.

Human Capital and Specialized Talent

The New York–New Jersey metro area commands top banking talent; average commercial-banking salaries rose 6.2% in 2024 to about $142,000, and compliance roles saw 8% wage growth, giving labor suppliers leverage to demand higher pay and hybrid schedules. Kearny Bank must compete with national banks and fintechs that spent $1.8B on tech hiring in 2024, pressuring retention and raising hiring costs by an estimated 10–15%.

Wholesale Funding Sources

Institutional lenders like the Federal Home Loan Bank (FHLB) act as key secondary liquidity suppliers for Kearny Bank; in 2024 FHLB advances nationwide totaled about $1.1 trillion, and their collateral and spread pricing directly affect Kearny’s funding costs and usable liquidity.

When markets tighten, higher advance rates or stricter collateral reduce Kearny’s capacity to fund loan growth; for example, a 50 bps rise in advance spreads can raise funding costs materially versus deposit funding.

- FHLB advances ≈ $1.1T (2024)

- Collateral rules limit usable assets

- +50 bps spread raises funding cost

Regulatory and Legal Services

Specialized legal and audit firms retain strong supplier power for Kearny Bank as post-2023 regulatory shifts and 2024–25 enforcement trends raise compliance complexity; top-tier counsel scarcity means the bank cannot cheaply replicate these services internally.

High stakes of non-compliance (fines averaged $220k per enforcement action for regional banks in 2024) make switching costly, so fees for these firms act as a fixed drag on non-interest expenses.

- 2024 enforcement fines avg $220,000 (regional banks)

- Top-tier legal rates $600–1,200/hr

- Compliance outsourcing ≈2–4% of non-interest expenses

High supplier power: deposit rates, costly vendors & FHLB drive Kearny’s elevated costs

Suppliers hold high bargaining power: depositors demand ~4.5–5.5% yields, core tech vendors charge premiums (replacement cost $10–50m, 18–36 months), FHLB advances ~$1.1T (2024) set liquidity costs, and legal/compliance fees (top rates $600–1,200/hr) raise non-interest expenses; switching costs and regulatory risk keep Kearny dependent.

| Supplier | Key Metric (2024–25) |

|---|---|

| Depositors | Retail 4.5–5.0%, Business 5.0–5.5% |

| Core vendors | Replacement $10–50m; 18–36 months |

| FHLB | Advances ≈ $1.1T; +50bps raises funding cost |

| Legal/compliance | Rates $600–1,200/hr; fines avg $220k |

What is included in the product

Tailored Porter’s Five Forces analysis for Kearny Bank uncovering competitive drivers, customer and supplier influence, entry barriers, substitute threats, and strategic levers shaping its pricing, profitability, and market defense.

Compact Porter's Five Forces snapshot for Kearny Bank—quickly assess competitive pressure and regulatory risk to guide strategic or investment decisions.

Customers Bargaining Power

Switching Costs for Retail Customers

The bargaining power of retail customers is high: digital onboarding cuts switching costs so moving personal accounts takes under 20 minutes and 42% of US consumers switched banks in 2023 for better rates or fees (2024 FDIC trend).

In Kearny Bank’s NJ/NY markets, easy online comparison of rates and fees means customers will jump for marginal gains; price sensitivity rose 7% in regional surveys through 2024.

Kearny must offset this by doubling down on high-touch service and community loyalty—branch events, local sponsorships, and relationship managers raised retention 3–5 ppt in comparable regional banks in 2024.

Price Sensitivity in Mortgage Lending

Borrowers seeking residential mortgages are highly price-sensitive and often use brokers to secure the lowest rates; in 2024 mortgage shopping reduced average lender spread by ~25 basis points, per industry data. Kearny Bank, focused on residential lending, faces competition from national banks with scale-driven cost edges and lower funding costs—large banks held 52% of mortgage originations in 2024. That scale forces Kearny to act as a price taker on many standard products, limiting spread expansion and pressuring net interest margins.

Concentration of Commercial Real Estate Clients

Information Transparency and Comparison Tools

By late 2025, real-time comparison platforms made CD rates and loan terms effectively transparent—customers see offers from top regional banks and fintechs instantly, cutting Kearny Bank’s information advantage.

This reduced asymmetry shifts bargaining power to customers, who now prioritize service and tailored advice over small rate differentials; 72% of consumers reported using comparison tools for deposit decisions in 2024 surveys.

Kearny must emphasize value-added services and personalized financial advice—relationship pricing, bundled planning, and advisor-led products—that comparison sites cannot price-match easily.

- Comparison platforms → near-perfect info on rates by 2025

- 72% of customers used tools for deposit choices (2024)

- Shift: price sensitivity down, service/personalization up

- Action: focus on advisor services, bundled value, relationship pricing

Demand for Digital and Mobile Excellence

Modern customers treat seamless digital banking as table stakes; 73% of US consumers (2024 EY Global Banking Survey) say they would switch banks for a better digital experience, giving customers high exit power.

If Kearny Bank's mobile app or portal lags neobanks — which average 4.6/5 app ratings and faster onboarding — primary deposits can migrate, hurting fee and deposit growth.

That risk forces continuous capex: regional banks spent ~0.9–1.2% of assets on tech in 2023, so Kearny likely needs similar ongoing investment to stay competitive.

- 73% willing to switch for better digital service

- Neobanks avg 4.6/5 app ratings

- Regional bank tech spend ~0.9–1.2% of assets (2023)

High customer power: 72% comparison use, 73% switch for digital — CRE pricing under pressure

Customer bargaining power is high: 72% use comparison tools (2024) and 73% would switch for better digital service, pushing Kearny toward relationship pricing and advisor-led bundles; top CRE borrowers (typical loans $20–150m) can secure 50–150 bps concessions, and top-5 loan exposure risks ~3–6% NII hit (2024).

| Metric | Value (year) |

|---|---|

| Comparison-tool users | 72% (2024) |

| Willing to switch for digital | 73% (2024) |

| Neobank app avg rating | 4.6/5 (2024) |

| Regional bank tech spend | 0.9–1.2% assets (2023) |

| Top-borrower concession | 50–150 bps (2024) |

| Top-5 loans NII sensitivity | ~3–6% (2024) |

What You See Is What You Get

Kearny Bank Porter's Five Forces Analysis

This preview shows the exact Kearny Bank Porter’s Five Forces analysis you'll receive after purchase—fully formatted, comprehensive, and ready to use with no placeholders or samples.