Kearny Bank Marketing Mix

Built for Strategy. Ready in Minutes.

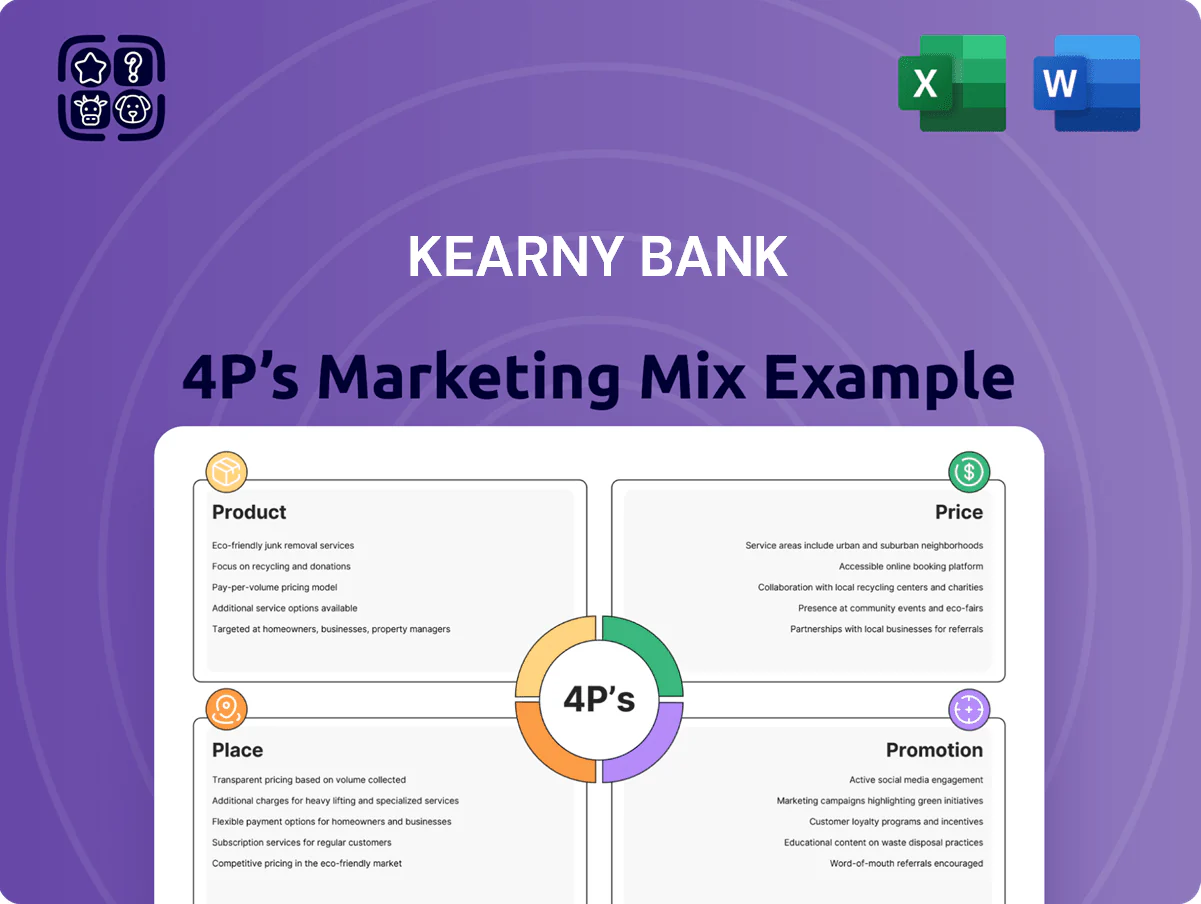

Discover how Kearny Bank’s product offerings, pricing structures, distribution channels, and promotional tactics combine to drive customer acquisition and retention—download the full 4P’s Marketing Mix Analysis for actionable insights and ready-to-use slides.

Product

Comprehensive Personal Banking Solutions

Kearny Bank’s personal banking suite covers checking, savings, and money market accounts tailored to life stages, with tiered APYs—up to 1.25% on high-balance money markets as of Dec 2025—to reward larger deposits. These accounts prioritize FDIC-backed security and 24/7 digital access, with 97% uptime reported in 2024. By end-2025 the bank rolled out enhanced fraud protection reducing unauthorized debit losses by 28% year-over-year and added API links to popular budgeting apps for seamless aggregation.

Strategic Commercial Real Estate Lending

Kearny Bank centers commercial real estate and multi-family lending as a core portfolio pillar, holding roughly 38% of its loan book in CRE/multi-family by YE 2024 (call report aggregated). The bank tailors loans for NJ and NY developers with flexible terms—interest-only options, 5–10 year amortizations—and local market underwriting. Average CRE loan size in 2024 was about $4.2M, supporting acquisitions and refinancings with seasoned local lenders and quick decision timelines.

Specialized Business Financial Services

Kearny Bank offers small and mid-sized businesses specialized credit lines, term loans, and advanced cash-management tools that helped clients reduce DSO (days sales outstanding) by an average 12% in 2024 and supported $1.2B in commercial lending that year.

The services target working-capital optimization and daily operations, with treasury solutions processing 35,000+ ACH transactions monthly to smooth cash flow for local entrepreneurs.

The bank emphasizes personalized plans: relationship managers create customized financial roadmaps, yielding a 9-point higher NPS for business clients versus branch-standard packages in 2024.

Integrated Wealth Management and Trust

Integrated Wealth Management and Trust at Kearny Bank delivers long-term planning, investment advisory, and estate management for high-net-worth clients, leveraging fiduciary expertise to grow and preserve assets across generations.

By late 2025 Kearny added ESG-focused funds and automated portfolio rebalancing; wealth AUM rose 18% year-over-year to $2.9 billion in 2024, improving retention and intergenerational transfer planning.

- High-net-worth focus: estate and trust services

- AUM: $2.9B in 2024 (+18% YoY)

- 2025: ESG options and auto-rebalancing

- Outcome: better preservation, lower drift risk

Advanced Digital Banking Infrastructure

The Advanced Digital Banking Infrastructure offers Kearny Bank customers a full mobile and online platform for remote finance management, including mobile check deposit, real-time alerts, and person-to-person payments; 72% of Kearny users engaged digitally in 2024, up from 58% in 2021.

The platform is updated continually for speed and security, meeting industry benchmarks like sub-2s app load times and PCI DSS compliance; digital transactions grew 24% YoY in 2024, reducing branch cash visits by 18%.

- 72% digital adoption (2024)

- 24% YoY rise in digital transactions (2024)

- Sub-2s app load target

- PCI DSS compliance

Kearny Bank: Diversified growth — CRE-heavy lending, $2.9B AUM, 1.25% top MMA

Kearny Bank’s product mix spans retail (checking/savings/money markets with APYs up to 1.25% on high-balance MMAs as of Dec 2025), commercial CRE/multi-family lending (38% of loan book, avg loan $4.2M in 2024), SMB credit and treasury (supported $1.2B lending; cut DSO 12% in 2024), and wealth AUM $2.9B (2024, +18% YoY) with ESG options and auto-rebalancing.

| Product | Key metric | 2024–2025 |

|---|---|---|

| Retail deposits | Top MMA APY | 1.25% (Dec 2025) |

| CRE/multi-family | % loan book / avg loan | 38% / $4.2M (2024) |

| SMB lending | Commercial loans | $1.2B (2024); DSO −12% |

| Wealth & trust | AUM / growth | $2.9B (+18% YoY, 2024) |

What is included in the product

Delivers a concise, company-specific deep dive into Kearny Bank’s Product, Price, Place, and Promotion strategies—grounded in real brand practices and competitive context for actionable benchmarking.

Condenses Kearny Bank’s 4P insights into a concise, at-a-glance summary that speeds leadership alignment and decision-making.

Place

Extensive New Jersey Branch Network

Kearny Bank maintains dozens of full-service branches—about 45 locations as of 2025—across northern and central New Jersey, keeping branch density near 1 per 20,000 residents in its core markets.

These branches act as community hubs offering personalized financial consulting and teller services; 60% of deposits in 2024 still originated from branch customers, per bank filings.

The footprint is optimized for visibility and access, with 85% of branches inside 5 miles of key residential clusters and commercial corridors.

Targeted New York Metropolitan Presence

Expansion into the New York metro—Brooklyn, Staten Island, and Westchester—has extended Kearny Bank’s footprint into markets representing roughly 7.5 million residents; these branches opened since 2019 target commercial lending and niche retail services to win urban share.

As of Q4 2025, the region contributes about 18% of the bank’s commercial loan pipeline and has increased core deposits by an estimated $320 million, diversifying revenue and lowering concentration risk.

24/7 Digital and Mobile Access

By 2025 Kearny Bank’s online portal and mobile app handle the majority of daily transactions, with digital logins up 42% since 2021 and 68% of retail deposits initiated remotely; the platform offers 24/7 account management, bill pay, and live chat support. This virtual storefront reduced branch transaction volume by 34% and lowered operating costs, while mobile active users reached 215,000 as of Dec 2024, making digital channels the core distribution point.

Strategic ATM and Network Partnerships

Strategic ATM and network partnerships give Kearny Bank customers wide cash access; as of 2025 the bank taps Into over 55,000 surcharge-free ATMs through networks like MoneyPass, reducing out-of-network fees and supporting daily withdrawals and deposits.

These partnerships extend liquidity and account access beyond Kearny’s 80+ branches in New Jersey and New York, keeping customers connected while traveling and lowering friction for retail deposits and cash-based transactions.

- 55,000+ surcharge-free ATMs (2025)

- 80+ branches in NJ/NY (2025)

- Reduces out-of-network fees, increases convenience

Relationship-Driven Commercial Loan Offices

- Operate in key economic zones

- Closed ~$420M (34%) of 2024 commercial loans

- On-site visits cut approval time ~18 days

- Focus on deals >$5M and complex syndications

Kearny Bank: 80+ Branches, 55k ATMs and Digital Reach Powering $420M Commercial Growth

Kearny Bank combines 80+ branches (NJ/NY) and 55,000+ surcharge-free ATMs with digital channels (215,000 mobile users; 68% remote-deposit share) and relationship-driven commercial teams (closed ~$420M, 34% of 2024 commercial loans) to balance local access, urban expansion, and lower-cost digital distribution.

| Metric | 2024–25 |

|---|---|

| Branches | 80+ |

| ATMs | 55,000+ |

| Mobile users | 215,000 |

| Remote deposits | 68% |

| Commercial loans closed | $420M (34%) |

Same Document Delivered

Kearny Bank 4P's Marketing Mix Analysis

The preview shown here is the actual document you’ll receive instantly after purchase—no surprises. This Marketing Mix analysis for Kearny Bank covers Product, Price, Place, and Promotion in a ready-made, editable format. You're viewing the exact, full version included with your order, fully complete and ready to use. Purchase with confidence knowing the file displayed is the final deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Built for Strategy. Ready in Minutes.

Discover how Kearny Bank’s product offerings, pricing structures, distribution channels, and promotional tactics combine to drive customer acquisition and retention—download the full 4P’s Marketing Mix Analysis for actionable insights and ready-to-use slides.

Product

Comprehensive Personal Banking Solutions

Kearny Bank’s personal banking suite covers checking, savings, and money market accounts tailored to life stages, with tiered APYs—up to 1.25% on high-balance money markets as of Dec 2025—to reward larger deposits. These accounts prioritize FDIC-backed security and 24/7 digital access, with 97% uptime reported in 2024. By end-2025 the bank rolled out enhanced fraud protection reducing unauthorized debit losses by 28% year-over-year and added API links to popular budgeting apps for seamless aggregation.

Strategic Commercial Real Estate Lending

Kearny Bank centers commercial real estate and multi-family lending as a core portfolio pillar, holding roughly 38% of its loan book in CRE/multi-family by YE 2024 (call report aggregated). The bank tailors loans for NJ and NY developers with flexible terms—interest-only options, 5–10 year amortizations—and local market underwriting. Average CRE loan size in 2024 was about $4.2M, supporting acquisitions and refinancings with seasoned local lenders and quick decision timelines.

Specialized Business Financial Services

Kearny Bank offers small and mid-sized businesses specialized credit lines, term loans, and advanced cash-management tools that helped clients reduce DSO (days sales outstanding) by an average 12% in 2024 and supported $1.2B in commercial lending that year.

The services target working-capital optimization and daily operations, with treasury solutions processing 35,000+ ACH transactions monthly to smooth cash flow for local entrepreneurs.

The bank emphasizes personalized plans: relationship managers create customized financial roadmaps, yielding a 9-point higher NPS for business clients versus branch-standard packages in 2024.

Integrated Wealth Management and Trust

Integrated Wealth Management and Trust at Kearny Bank delivers long-term planning, investment advisory, and estate management for high-net-worth clients, leveraging fiduciary expertise to grow and preserve assets across generations.

By late 2025 Kearny added ESG-focused funds and automated portfolio rebalancing; wealth AUM rose 18% year-over-year to $2.9 billion in 2024, improving retention and intergenerational transfer planning.

- High-net-worth focus: estate and trust services

- AUM: $2.9B in 2024 (+18% YoY)

- 2025: ESG options and auto-rebalancing

- Outcome: better preservation, lower drift risk

Advanced Digital Banking Infrastructure

The Advanced Digital Banking Infrastructure offers Kearny Bank customers a full mobile and online platform for remote finance management, including mobile check deposit, real-time alerts, and person-to-person payments; 72% of Kearny users engaged digitally in 2024, up from 58% in 2021.

The platform is updated continually for speed and security, meeting industry benchmarks like sub-2s app load times and PCI DSS compliance; digital transactions grew 24% YoY in 2024, reducing branch cash visits by 18%.

- 72% digital adoption (2024)

- 24% YoY rise in digital transactions (2024)

- Sub-2s app load target

- PCI DSS compliance

Kearny Bank: Diversified growth — CRE-heavy lending, $2.9B AUM, 1.25% top MMA

Kearny Bank’s product mix spans retail (checking/savings/money markets with APYs up to 1.25% on high-balance MMAs as of Dec 2025), commercial CRE/multi-family lending (38% of loan book, avg loan $4.2M in 2024), SMB credit and treasury (supported $1.2B lending; cut DSO 12% in 2024), and wealth AUM $2.9B (2024, +18% YoY) with ESG options and auto-rebalancing.

| Product | Key metric | 2024–2025 |

|---|---|---|

| Retail deposits | Top MMA APY | 1.25% (Dec 2025) |

| CRE/multi-family | % loan book / avg loan | 38% / $4.2M (2024) |

| SMB lending | Commercial loans | $1.2B (2024); DSO −12% |

| Wealth & trust | AUM / growth | $2.9B (+18% YoY, 2024) |

What is included in the product

Delivers a concise, company-specific deep dive into Kearny Bank’s Product, Price, Place, and Promotion strategies—grounded in real brand practices and competitive context for actionable benchmarking.

Condenses Kearny Bank’s 4P insights into a concise, at-a-glance summary that speeds leadership alignment and decision-making.

Place

Extensive New Jersey Branch Network

Kearny Bank maintains dozens of full-service branches—about 45 locations as of 2025—across northern and central New Jersey, keeping branch density near 1 per 20,000 residents in its core markets.

These branches act as community hubs offering personalized financial consulting and teller services; 60% of deposits in 2024 still originated from branch customers, per bank filings.

The footprint is optimized for visibility and access, with 85% of branches inside 5 miles of key residential clusters and commercial corridors.

Targeted New York Metropolitan Presence

Expansion into the New York metro—Brooklyn, Staten Island, and Westchester—has extended Kearny Bank’s footprint into markets representing roughly 7.5 million residents; these branches opened since 2019 target commercial lending and niche retail services to win urban share.

As of Q4 2025, the region contributes about 18% of the bank’s commercial loan pipeline and has increased core deposits by an estimated $320 million, diversifying revenue and lowering concentration risk.

24/7 Digital and Mobile Access

By 2025 Kearny Bank’s online portal and mobile app handle the majority of daily transactions, with digital logins up 42% since 2021 and 68% of retail deposits initiated remotely; the platform offers 24/7 account management, bill pay, and live chat support. This virtual storefront reduced branch transaction volume by 34% and lowered operating costs, while mobile active users reached 215,000 as of Dec 2024, making digital channels the core distribution point.

Strategic ATM and Network Partnerships

Strategic ATM and network partnerships give Kearny Bank customers wide cash access; as of 2025 the bank taps Into over 55,000 surcharge-free ATMs through networks like MoneyPass, reducing out-of-network fees and supporting daily withdrawals and deposits.

These partnerships extend liquidity and account access beyond Kearny’s 80+ branches in New Jersey and New York, keeping customers connected while traveling and lowering friction for retail deposits and cash-based transactions.

- 55,000+ surcharge-free ATMs (2025)

- 80+ branches in NJ/NY (2025)

- Reduces out-of-network fees, increases convenience

Relationship-Driven Commercial Loan Offices

- Operate in key economic zones

- Closed ~$420M (34%) of 2024 commercial loans

- On-site visits cut approval time ~18 days

- Focus on deals >$5M and complex syndications

Kearny Bank: 80+ Branches, 55k ATMs and Digital Reach Powering $420M Commercial Growth

Kearny Bank combines 80+ branches (NJ/NY) and 55,000+ surcharge-free ATMs with digital channels (215,000 mobile users; 68% remote-deposit share) and relationship-driven commercial teams (closed ~$420M, 34% of 2024 commercial loans) to balance local access, urban expansion, and lower-cost digital distribution.

| Metric | 2024–25 |

|---|---|

| Branches | 80+ |

| ATMs | 55,000+ |

| Mobile users | 215,000 |

| Remote deposits | 68% |

| Commercial loans closed | $420M (34%) |

Same Document Delivered

Kearny Bank 4P's Marketing Mix Analysis

The preview shown here is the actual document you’ll receive instantly after purchase—no surprises. This Marketing Mix analysis for Kearny Bank covers Product, Price, Place, and Promotion in a ready-made, editable format. You're viewing the exact, full version included with your order, fully complete and ready to use. Purchase with confidence knowing the file displayed is the final deliverable.