SeaLink Travel Group Boston Consulting Group Matrix

Unlock Strategic Clarity

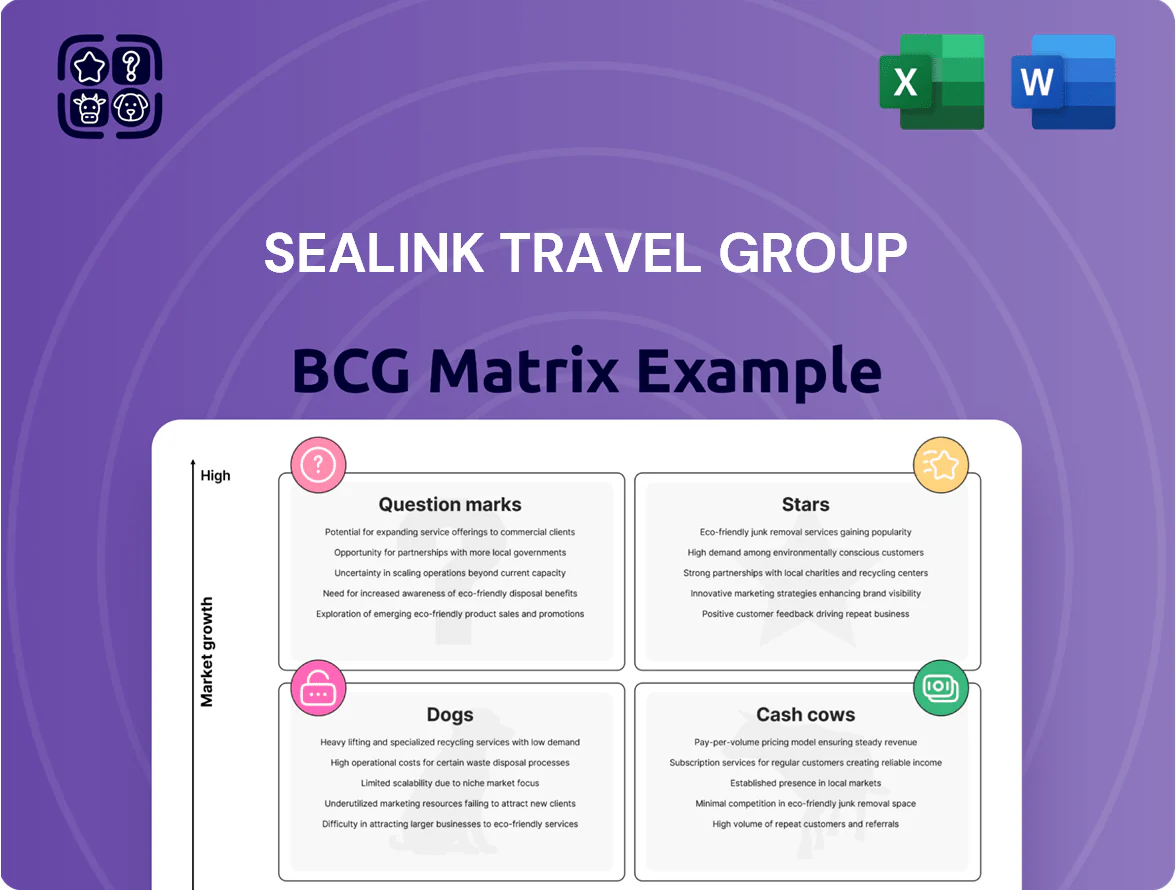

SeaLink Travel Group’s preliminary BCG Matrix signals a mixed portfolio—regional ferry services likely sit as Cash Cows, growing tourism ventures as potential Stars, niche charters as Question Marks, and legacy routes at risk of becoming Dogs; this snapshot highlights where cash generation and strategic reinvestment should focus. Dive deeper and purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and actionable strategies in ready-to-use Word and Excel formats.

Stars

Singapore Public Transport Expansion

Kelsian has secured and renewed major Singapore bus contracts, operating under high performance standards in a market growing ~3–4% annually; by H2 2025 these operations account for about 22% of Kelsian’s international revenue (~A$160m of A$730m international revenue, FY2024 pro forma).

Contracts demand ~A$120–180m capex for fleet and smart-ticketing rollouts but lock in predictable cash flows and position Kelsian as a dominant operator within a top-tier global public-transit market moving toward higher-frequency services.

USA Motorcoach and Charter Growth

Following the 2022 acquisition of All Aboard America! Holdings, Kelsian (SeaLink Travel Group subsidiary) gained top share in the fragmented US motorcoach market, estimated at ~5–7% national market share in 2024 and serving corporate shuttles and government contracts worth an estimated US$1.2–1.5bn annually.

Electric Vehicle Fleet Transition

Kelsian has shifted heavily into electric buses, converting about 900 vehicles across Australia and the UK by end-2024 and investing ~A$300m in chargers and batteries through 2025.

This aligns with federal and state zero-emission mandates (2035 for many metropolitan tenders), helping Kelsian win contracts where 30–40% of scoring favors emissions.

Upfront capex hit free cash flow—estimated A$120m in 2024—but builds a barrier: lower operating costs and tender access in a fast-growing regulated market.

Sydney Metropolitan Bus Contracts

SeaLink Travel Group's Sydney metropolitan bus contracts are Stars: they control multiple large regions under long-term NSW government contracts, driving strong, stable revenue—Sydney services generated about A$120–140m FY2024 revenue within SeaLink's NSW transport segment.

Rising Sydney population (5.4% growth 2016–2021; ABS projections to 5.8m by 2031) and higher urban transit ridership forecast (+2–3% p.a.) make these routes a high-growth engine, supporting margin expansion versus regional operators.

The scale enables optimized route scheduling, lower unit costs, and higher operating margin—SeaLink reports transport EBITDA margins roughly 12–15% in metro operations, versus ~6–9% in smaller regional contracts.

- Long-term govt contracts: stable cash flow

- FY2024 NSW transport rev ~A$120–140m

- Metro EBITDA margin ~12–15%

- Sydney pop ~5.3–5.4m; projected growth to 5.8m by 2031

- Ridership growth +2–3% p.a. supports scale

Integrated Transit Technology Solutions

Integrated Transit Technology Solutions is a Star for SeaLink (Kelsian Group) after Kelsian invested ~A$25m since 2021 in proprietary scheduling and passenger-data analytics, cutting dwell and turnaround delays by 12% and boosting on-time performance to 94% in FY2024, improving contract retention probability.

These digital tools are scaling across Australia, UK, and Singapore operations—deployed on 60% of fleet routes by end-2025—raising NPS and lowering operating cost per passenger km by ~4%, so continued capex is strategic.

The global market for transit analytics grew 18% Y/Y to US$6.2bn in 2024, driving high demand for data-driven transit management and making this area critical for future revenue and margin expansion.

- Kelsian capex ~A$25m (2021–2024)

- On-time performance 94% (FY2024)

- Dwell/turnaround delays down 12%

- Deployed to 60% of routes by 2025

- Transit analytics market US$6.2bn (2024), +18% Y/Y

- Opex per passenger km down ~4%

SeaLink’s Sydney Metro & Transit Tech Drive A$130m Revenue, 94% On‑Time, 12–15% EBITDA

SeaLink's Sydney metro buses and Integrated Transit Tech are Stars: metro revenue ~A$130m (FY2024), EBITDA margin 12–15%, ridership growth +2–3% p.a.; tech investment A$25m (2021–24) cut delays 12% and raised on-time to 94%, deployed to 60% routes by 2025.

| Metric | Value |

|---|---|

| Sydney rev (FY2024) | A$130m |

| Metro EBITDA | 12–15% |

| Ridership growth | +2–3% p.a. |

| Tech capex (2021–24) | A$25m |

| On-time (FY2024) | 94% |

| Routes with tech (2025) | 60% |

What is included in the product

Comprehensive BCG Matrix analysis of SeaLink Travel Group’s units with strategic recommendations for investment, retention, or divestment.

One-page BCG matrix placing SeaLink Travel Group units into quadrants for quick strategic decisions.

Cash Cows

Kangaroo Island SeaLink Ferry

The Kangaroo Island SeaLink ferry is the marine division’s flagship cash generator, holding an estimated 70–80% market share on the Penneshaw–Cape Jervis route and protected by high barriers to entry such as port access and vessel regulation.

By end-2025 the route is mature: annual passenger volumes stabilized near 250,000 and average fare yield rose 3.5% in 2024–25, sustaining pricing power and predictable revenue.

Low incremental marketing spend and existing terminal and vessel infrastructure cut incremental capex to under A$5m annually, letting SeaLink harvest roughly A$20–25m free cash flow in 2024–25 to fund global expansion.

South Australian Urban Bus Operations

Kelsian runs Adelaide urban buses under multi-year government contracts, delivering predictable, inflation-linked revenues; the 2024 contract roll contributed about A$85–95m in annual revenue to SeaLink Travel Group’s Australian operations, easing cash flow variability.

With Adelaide’s market mature and passenger growth near 1–2% annually, these services act as a stable cash cow, funding capital and dividend needs while lowering group-level earnings volatility.

Gladstone LNG Marine Transport

Gladstone LNG Marine Transport serves Queensland LNG projects in a mature, high-margin niche; FY2024 segment EBITDA margin was ~28% and average vessel utilization exceeded 92% across 2024 contracts.

Contracts are long-term—typical tenor 5–15 years—covering crew transfer and supply runs, securing steady cash flows and 2024 revenue around A$45m for the unit.

Existing berths and vessels limit capex needs to , enabling strong dividend flow to SeaLink, contributing roughly 12% of group free cash flow in 2024.

Western Australia Transit Services

Western Australia Transit Services under SeaLink Travel Group delivers steady EBITDA margins ~10–12% in Perth and regional WA, with contracts mature and low competitive risk, providing reliable cash flow.

Because routes are established, Kelsian focuses on operational excellence and cost control rather than market-share fights, trimming unit costs by ~3% year-over-year in 2024.

Cash generated is routinely redeployed to Question Mark international projects; FY24 free cash flow from WA operations ~A$25–30m funded expansion abroad.

- Steady EBITDA 10–12%

- Low competitive risk; mature contracts

- Opex focus; unit costs -3% YoY (2024)

- FY24 FCF A$25–30m funneled to international growth

North Stradbroke Island Ferry Services

North Stradbroke Island ferry services form a cash cow for SeaLink Travel Group, serving ~150,000 passengers annually (FY2024) with >60% route market share and stable yields tied to local residents and tourists.

Operating in a mature Queensland market where growth tracks population (Redland City +0.8% yr) and tourism (Moreton Bay region +2% yr), the route generates predictable EBITDA margins ~22% used to pay corporate debt and fund dividends.

- ~150,000 passengers/yr (FY2024)

- >60% market share on route

- EBITDA margin ~22%

- Supports debt service and dividends

Stable high‑margin transport assets deliver A$80–100m FCF to fuel growth & dividends

Kangaroo Island ferry, Adelaide buses, Gladstone LNG marine, WA transit and North Stradbroke ferry together generated stable, high-margin cash flows in 2024–25 (route market shares 60–80%; passenger volumes 150k–250k; segment EBITDA margins 10–28%), producing ~A$80–100m free cash flow to fund intl growth and dividends.

| Asset | Passengers/Revenue | Market share | EBITDA % | FCF 2024–25 (A$M) |

|---|---|---|---|---|

| Kangaroo Island ferry | 250,000 pax | 70–80% | ~24% | 20–25 |

| Adelaide buses (Kelsian) | A$85–95m rev | Contracted | 10–12% | 25–30 |

| Gladstone LNG marine | A$45m rev | Niche | ~28% | ~9 |

| WA transit | — | Mature | 10–12% | 25–30 |

| North Stradbroke ferry | 150,000 pax | >60% | ~22% | ~5 |

What You’re Viewing Is Included

SeaLink Travel Group BCG Matrix

The file you're previewing is the final SeaLink Travel Group BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

SeaLink Travel Group’s preliminary BCG Matrix signals a mixed portfolio—regional ferry services likely sit as Cash Cows, growing tourism ventures as potential Stars, niche charters as Question Marks, and legacy routes at risk of becoming Dogs; this snapshot highlights where cash generation and strategic reinvestment should focus. Dive deeper and purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and actionable strategies in ready-to-use Word and Excel formats.

Stars

Singapore Public Transport Expansion

Kelsian has secured and renewed major Singapore bus contracts, operating under high performance standards in a market growing ~3–4% annually; by H2 2025 these operations account for about 22% of Kelsian’s international revenue (~A$160m of A$730m international revenue, FY2024 pro forma).

Contracts demand ~A$120–180m capex for fleet and smart-ticketing rollouts but lock in predictable cash flows and position Kelsian as a dominant operator within a top-tier global public-transit market moving toward higher-frequency services.

USA Motorcoach and Charter Growth

Following the 2022 acquisition of All Aboard America! Holdings, Kelsian (SeaLink Travel Group subsidiary) gained top share in the fragmented US motorcoach market, estimated at ~5–7% national market share in 2024 and serving corporate shuttles and government contracts worth an estimated US$1.2–1.5bn annually.

Electric Vehicle Fleet Transition

Kelsian has shifted heavily into electric buses, converting about 900 vehicles across Australia and the UK by end-2024 and investing ~A$300m in chargers and batteries through 2025.

This aligns with federal and state zero-emission mandates (2035 for many metropolitan tenders), helping Kelsian win contracts where 30–40% of scoring favors emissions.

Upfront capex hit free cash flow—estimated A$120m in 2024—but builds a barrier: lower operating costs and tender access in a fast-growing regulated market.

Sydney Metropolitan Bus Contracts

SeaLink Travel Group's Sydney metropolitan bus contracts are Stars: they control multiple large regions under long-term NSW government contracts, driving strong, stable revenue—Sydney services generated about A$120–140m FY2024 revenue within SeaLink's NSW transport segment.

Rising Sydney population (5.4% growth 2016–2021; ABS projections to 5.8m by 2031) and higher urban transit ridership forecast (+2–3% p.a.) make these routes a high-growth engine, supporting margin expansion versus regional operators.

The scale enables optimized route scheduling, lower unit costs, and higher operating margin—SeaLink reports transport EBITDA margins roughly 12–15% in metro operations, versus ~6–9% in smaller regional contracts.

- Long-term govt contracts: stable cash flow

- FY2024 NSW transport rev ~A$120–140m

- Metro EBITDA margin ~12–15%

- Sydney pop ~5.3–5.4m; projected growth to 5.8m by 2031

- Ridership growth +2–3% p.a. supports scale

Integrated Transit Technology Solutions

Integrated Transit Technology Solutions is a Star for SeaLink (Kelsian Group) after Kelsian invested ~A$25m since 2021 in proprietary scheduling and passenger-data analytics, cutting dwell and turnaround delays by 12% and boosting on-time performance to 94% in FY2024, improving contract retention probability.

These digital tools are scaling across Australia, UK, and Singapore operations—deployed on 60% of fleet routes by end-2025—raising NPS and lowering operating cost per passenger km by ~4%, so continued capex is strategic.

The global market for transit analytics grew 18% Y/Y to US$6.2bn in 2024, driving high demand for data-driven transit management and making this area critical for future revenue and margin expansion.

- Kelsian capex ~A$25m (2021–2024)

- On-time performance 94% (FY2024)

- Dwell/turnaround delays down 12%

- Deployed to 60% of routes by 2025

- Transit analytics market US$6.2bn (2024), +18% Y/Y

- Opex per passenger km down ~4%

SeaLink’s Sydney Metro & Transit Tech Drive A$130m Revenue, 94% On‑Time, 12–15% EBITDA

SeaLink's Sydney metro buses and Integrated Transit Tech are Stars: metro revenue ~A$130m (FY2024), EBITDA margin 12–15%, ridership growth +2–3% p.a.; tech investment A$25m (2021–24) cut delays 12% and raised on-time to 94%, deployed to 60% routes by 2025.

| Metric | Value |

|---|---|

| Sydney rev (FY2024) | A$130m |

| Metro EBITDA | 12–15% |

| Ridership growth | +2–3% p.a. |

| Tech capex (2021–24) | A$25m |

| On-time (FY2024) | 94% |

| Routes with tech (2025) | 60% |

What is included in the product

Comprehensive BCG Matrix analysis of SeaLink Travel Group’s units with strategic recommendations for investment, retention, or divestment.

One-page BCG matrix placing SeaLink Travel Group units into quadrants for quick strategic decisions.

Cash Cows

Kangaroo Island SeaLink Ferry

The Kangaroo Island SeaLink ferry is the marine division’s flagship cash generator, holding an estimated 70–80% market share on the Penneshaw–Cape Jervis route and protected by high barriers to entry such as port access and vessel regulation.

By end-2025 the route is mature: annual passenger volumes stabilized near 250,000 and average fare yield rose 3.5% in 2024–25, sustaining pricing power and predictable revenue.

Low incremental marketing spend and existing terminal and vessel infrastructure cut incremental capex to under A$5m annually, letting SeaLink harvest roughly A$20–25m free cash flow in 2024–25 to fund global expansion.

South Australian Urban Bus Operations

Kelsian runs Adelaide urban buses under multi-year government contracts, delivering predictable, inflation-linked revenues; the 2024 contract roll contributed about A$85–95m in annual revenue to SeaLink Travel Group’s Australian operations, easing cash flow variability.

With Adelaide’s market mature and passenger growth near 1–2% annually, these services act as a stable cash cow, funding capital and dividend needs while lowering group-level earnings volatility.

Gladstone LNG Marine Transport

Gladstone LNG Marine Transport serves Queensland LNG projects in a mature, high-margin niche; FY2024 segment EBITDA margin was ~28% and average vessel utilization exceeded 92% across 2024 contracts.

Contracts are long-term—typical tenor 5–15 years—covering crew transfer and supply runs, securing steady cash flows and 2024 revenue around A$45m for the unit.

Existing berths and vessels limit capex needs to , enabling strong dividend flow to SeaLink, contributing roughly 12% of group free cash flow in 2024.

Western Australia Transit Services

Western Australia Transit Services under SeaLink Travel Group delivers steady EBITDA margins ~10–12% in Perth and regional WA, with contracts mature and low competitive risk, providing reliable cash flow.

Because routes are established, Kelsian focuses on operational excellence and cost control rather than market-share fights, trimming unit costs by ~3% year-over-year in 2024.

Cash generated is routinely redeployed to Question Mark international projects; FY24 free cash flow from WA operations ~A$25–30m funded expansion abroad.

- Steady EBITDA 10–12%

- Low competitive risk; mature contracts

- Opex focus; unit costs -3% YoY (2024)

- FY24 FCF A$25–30m funneled to international growth

North Stradbroke Island Ferry Services

North Stradbroke Island ferry services form a cash cow for SeaLink Travel Group, serving ~150,000 passengers annually (FY2024) with >60% route market share and stable yields tied to local residents and tourists.

Operating in a mature Queensland market where growth tracks population (Redland City +0.8% yr) and tourism (Moreton Bay region +2% yr), the route generates predictable EBITDA margins ~22% used to pay corporate debt and fund dividends.

- ~150,000 passengers/yr (FY2024)

- >60% market share on route

- EBITDA margin ~22%

- Supports debt service and dividends

Stable high‑margin transport assets deliver A$80–100m FCF to fuel growth & dividends

Kangaroo Island ferry, Adelaide buses, Gladstone LNG marine, WA transit and North Stradbroke ferry together generated stable, high-margin cash flows in 2024–25 (route market shares 60–80%; passenger volumes 150k–250k; segment EBITDA margins 10–28%), producing ~A$80–100m free cash flow to fund intl growth and dividends.

| Asset | Passengers/Revenue | Market share | EBITDA % | FCF 2024–25 (A$M) |

|---|---|---|---|---|

| Kangaroo Island ferry | 250,000 pax | 70–80% | ~24% | 20–25 |

| Adelaide buses (Kelsian) | A$85–95m rev | Contracted | 10–12% | 25–30 |

| Gladstone LNG marine | A$45m rev | Niche | ~28% | ~9 |

| WA transit | — | Mature | 10–12% | 25–30 |

| North Stradbroke ferry | 150,000 pax | >60% | ~22% | ~5 |

What You’re Viewing Is Included

SeaLink Travel Group BCG Matrix

The file you're previewing is the final SeaLink Travel Group BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report designed for strategic clarity and professional use.