Kerry Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

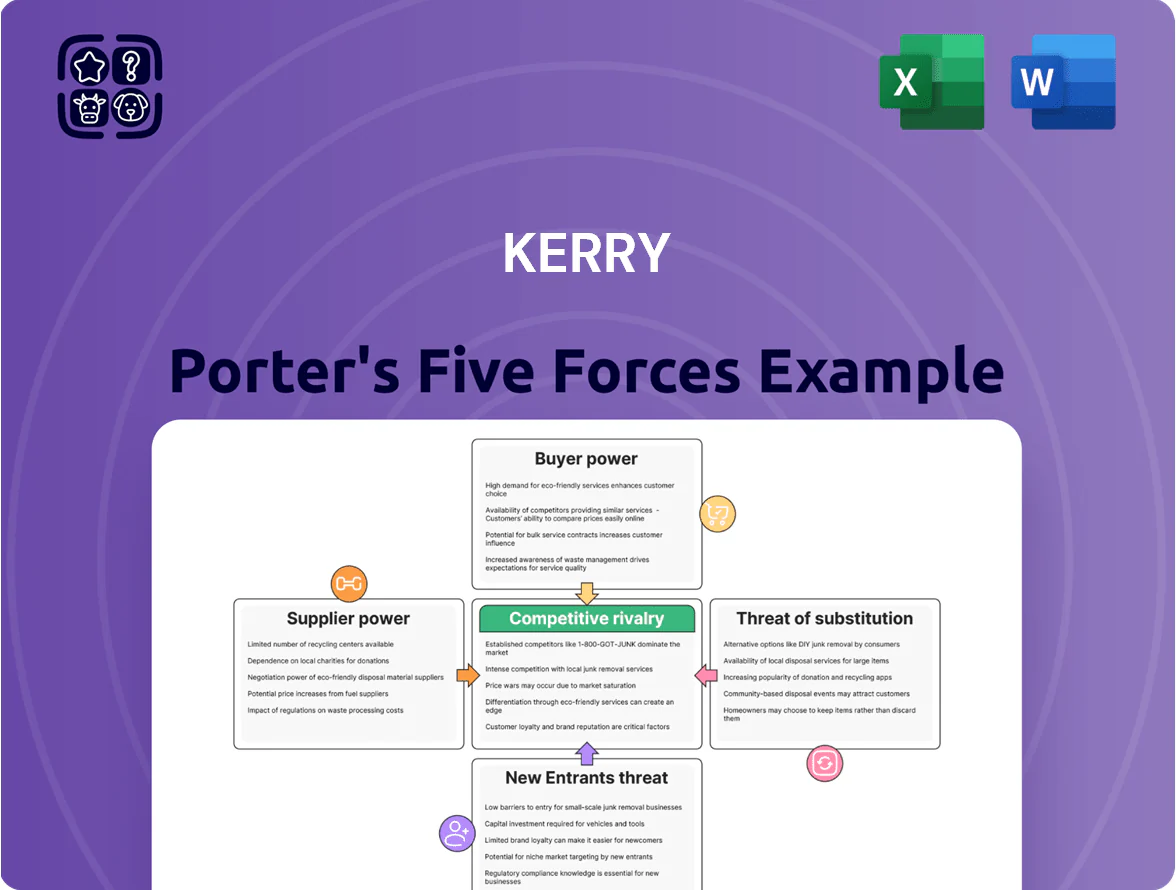

Kerry’s Five Forces snapshot highlights supplier bargaining, buyer sensitivity, competitive rivalry, threat of substitutes, and barriers to entry to show where margins and risks concentrate; it teases strategic levers but stops short of prescriptive conclusions.

This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Kerry’s market position.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Raw material commodity volatility: Kerry sources large volumes of dairy, grains and plant proteins, exposed to price swings—dairy powder rose 28% and soymeal 22% in 2023–24; climate shocks by end-2025 concentrated supply power in regional agricultural cooperatives (e.g., EU, Brazil), raising supplier bargaining power. Kerry counters with a diversified sourcing network across 30+ countries and long-term procurement contracts covering roughly 60% of key inputs, reducing spot-price exposure.

Dependency on Specialized Chemical Ingredients

The production of complex taste molecules needs specific chemical precursors made by a few specialized manufacturers, giving suppliers moderate bargaining power since Kerry PLC’s (ticker KRY) proprietary formulations depend on high-purity inputs; in 2024 Kerry reported 7–9% of COGS tied to specialty ingredients, so supplier constraints can move margins. Kerry is cutting reliance by expanding internal synthetic biology and fermentation capacity—R&D spend rose to €338m in FY2024—to secure supply and lower purchase volatility.

Sustainability and ESG Compliance Requirements

Suppliers certified to environmental and ethical standards hold growing leverage as Kerry Foods (part of Kerry Group plc) commits to a net-zero supply chain by 2050; by 2025 only ~18% of global palm oil and ~12% of cocoa derivatives are RSPO or equivalent certified, shrinking the supplier pool.

That scarcity lets compliant suppliers charge premiums of 5–20% and secure longer, more favorable contracts; Kerry reported paying a 7% sustainable premium on select oils in 2024, signaling willingness to absorb higher input costs to meet ESG goals.

Supplier Fragmentation in Local Markets

In many emerging markets Kerry sources from a fragmented base of small farmers, which lowers individual supplier leverage and lets Kerry enforce quality and delivery rules; Kerry reported over 120,000 direct smallholder relationships across Africa and Asia in 2024, diluting supplier bargaining power.

Still, managing those suppliers raises admin costs—Kerry disclosed supply-chain operating expenses of about EUR 320m in 2024, much tied to sourcing coordination, traceability, and training programs.

- 120,000+ smallholder relationships (2024)

- Lower per-supplier bargaining power

- Quality/delivery standards enforced by Kerry

- Supply-chain operating costs ~EUR 320m (2024)

Forward Integration Threats

While most raw-material producers lack Kerry Group’s advanced R&D and clinical capabilities, large dairy and grain processors (e.g., Arla, Ingredion-scale firms) are moving into basic ingredient blending, creating a minor forward-integration threat.

Kerry counters by investing in high-value, clinically supported nutritional tech—R&D spend ~€135m in 2024—keeping differentiation that commodity processors struggle to replicate.

- Minor threat: basic blending only

- Big suppliers: selective forward moves

- Kerry edge: €135m R&D (2024) + clinical data

- Risk: semi-processed uptake in value chains

Kerry's supplier power: scale, contracts & R&D curb risk but sustainable premiums pinch margins

Suppliers hold mixed power: commodity volatility and certified-supplier scarcity raise leverage, while Kerry’s 30+ country sourcing, 60% long-term contracts, 120,000+ smallholders (2024) and internal fermentation/R&D (€338m FY2024) reduce it; sustainable premiums (~7% paid in 2024) and specialty-ingredient concentration (7–9% of COGS) still pressure margins.

| Metric | Value (2024–25) |

|---|---|

| Long-term covers | ~60% |

| Smallholders | 120,000+ |

| R&D | €338m |

| Sustainable premium | ~7% |

What is included in the product

Concise Five Forces assessment for Kerry, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with actionable implications for pricing, profitability, and strategic positioning.

A concise, one-sheet Kerry Porter Five Forces snapshot that turns complex competitive analysis into immediate strategic choices—ideal for quick decisions and slide-ready summaries.

Customers Bargaining Power

Consolidation of Global Consumer Brand Owners

High Switching Costs for Custom Formulations

Once a Kerry flavor or nutritional profile is built into a product, swapping suppliers is costly and risky; taste or texture shifts can cut repeat purchases and trigger reformulation that typically costs $250k–$1.2M per SKU and delays launch by 6–12 months.

Label changes, new stability testing, and regulatory filings add $50k–$300k and extend time-to-shelf, raising churn risk for brands and reducing their leverage over Kerry in commercial contracts.

Demand for Transparency and Clean Labels

Modern retailers and foodservice buyers demand full traceability and clean labels, pushing Kerry Group to supply batch-level data and simple ingredient lists; 72% of global consumers said transparency influences purchase decisions in 2024 (NielsenIQ), increasing customer leverage.

Price Sensitivity in Commodity Segments

In commodity segments like basic seasonings and coatings, customer loyalty is low and price sensitivity is high; buyers often switch suppliers for small cost savings, with switch rates up to 15% annually in foodservice ingredients (2024 trade data).

Kerry combats this by bundling low-margin products with technical services and digital supply-chain tools, raising effective switching costs and increasing gross margin per account by ~120 basis points in 2023.

- High churn: ~15% supplier switch rate (2024)

- Low loyalty: commoditized SKUs drive price focus

- Kerry tactic: bundle tech services + digital tools

- Impact: +120 bps gross margin per account (2023)

Growth of Private Label Manufacturers

The rise of high-quality private label brands—private label sales hit 22% of global grocery sales in 2024—creates customers focused on cost and speed, squeezing margins and pressing Kerry Group for low-cost, effective solutions.

Kerry counters with modular ingredient systems that cut product development time by up to 40% and support premium-tier launches while protecting margins for both Kerry and private-label clients.

- Private label = 22% global grocery sales (2024)

- Private-label manufacturers have thinner margins; demand low cost

- Kerry offers modular systems; reduces development time ~40%

Customers Drive Pressure; Kerry Fights Back with R&D, Tech Bundles & Modular Wins

Customers hold significant bargaining power: top multinationals=~40% Kerry FY2024, private label=22% global grocery (2024). High switch rates in commodity SKUs (~15% pa) and transparency demands (72% consumers influenced, NielsenIQ 2024) pressure prices. Kerry offsets via embedded R&D, bundled tech/digital tools (+120 bps gross margin per account 2023) and modular systems (dev time -40%).

| Metric | Value |

|---|---|

| Top customers share | ~40% (FY2024) |

| Private label | 22% (2024) |

| Switch rate | ~15% pa (2024) |

| Consumer transparency impact | 72% (NielsenIQ 2024) |

| Margin lift | +120 bps (2023) |

| Dev time reduction | -40% |

Preview Before You Purchase

Kerry Porter's Five Forces Analysis

This preview shows the exact Kerry Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kerry’s Five Forces snapshot highlights supplier bargaining, buyer sensitivity, competitive rivalry, threat of substitutes, and barriers to entry to show where margins and risks concentrate; it teases strategic levers but stops short of prescriptive conclusions.

This brief overview only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Kerry’s market position.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Raw material commodity volatility: Kerry sources large volumes of dairy, grains and plant proteins, exposed to price swings—dairy powder rose 28% and soymeal 22% in 2023–24; climate shocks by end-2025 concentrated supply power in regional agricultural cooperatives (e.g., EU, Brazil), raising supplier bargaining power. Kerry counters with a diversified sourcing network across 30+ countries and long-term procurement contracts covering roughly 60% of key inputs, reducing spot-price exposure.

Dependency on Specialized Chemical Ingredients

The production of complex taste molecules needs specific chemical precursors made by a few specialized manufacturers, giving suppliers moderate bargaining power since Kerry PLC’s (ticker KRY) proprietary formulations depend on high-purity inputs; in 2024 Kerry reported 7–9% of COGS tied to specialty ingredients, so supplier constraints can move margins. Kerry is cutting reliance by expanding internal synthetic biology and fermentation capacity—R&D spend rose to €338m in FY2024—to secure supply and lower purchase volatility.

Sustainability and ESG Compliance Requirements

Suppliers certified to environmental and ethical standards hold growing leverage as Kerry Foods (part of Kerry Group plc) commits to a net-zero supply chain by 2050; by 2025 only ~18% of global palm oil and ~12% of cocoa derivatives are RSPO or equivalent certified, shrinking the supplier pool.

That scarcity lets compliant suppliers charge premiums of 5–20% and secure longer, more favorable contracts; Kerry reported paying a 7% sustainable premium on select oils in 2024, signaling willingness to absorb higher input costs to meet ESG goals.

Supplier Fragmentation in Local Markets

In many emerging markets Kerry sources from a fragmented base of small farmers, which lowers individual supplier leverage and lets Kerry enforce quality and delivery rules; Kerry reported over 120,000 direct smallholder relationships across Africa and Asia in 2024, diluting supplier bargaining power.

Still, managing those suppliers raises admin costs—Kerry disclosed supply-chain operating expenses of about EUR 320m in 2024, much tied to sourcing coordination, traceability, and training programs.

- 120,000+ smallholder relationships (2024)

- Lower per-supplier bargaining power

- Quality/delivery standards enforced by Kerry

- Supply-chain operating costs ~EUR 320m (2024)

Forward Integration Threats

While most raw-material producers lack Kerry Group’s advanced R&D and clinical capabilities, large dairy and grain processors (e.g., Arla, Ingredion-scale firms) are moving into basic ingredient blending, creating a minor forward-integration threat.

Kerry counters by investing in high-value, clinically supported nutritional tech—R&D spend ~€135m in 2024—keeping differentiation that commodity processors struggle to replicate.

- Minor threat: basic blending only

- Big suppliers: selective forward moves

- Kerry edge: €135m R&D (2024) + clinical data

- Risk: semi-processed uptake in value chains

Kerry's supplier power: scale, contracts & R&D curb risk but sustainable premiums pinch margins

Suppliers hold mixed power: commodity volatility and certified-supplier scarcity raise leverage, while Kerry’s 30+ country sourcing, 60% long-term contracts, 120,000+ smallholders (2024) and internal fermentation/R&D (€338m FY2024) reduce it; sustainable premiums (~7% paid in 2024) and specialty-ingredient concentration (7–9% of COGS) still pressure margins.

| Metric | Value (2024–25) |

|---|---|

| Long-term covers | ~60% |

| Smallholders | 120,000+ |

| R&D | €338m |

| Sustainable premium | ~7% |

What is included in the product

Concise Five Forces assessment for Kerry, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with actionable implications for pricing, profitability, and strategic positioning.

A concise, one-sheet Kerry Porter Five Forces snapshot that turns complex competitive analysis into immediate strategic choices—ideal for quick decisions and slide-ready summaries.

Customers Bargaining Power

Consolidation of Global Consumer Brand Owners

High Switching Costs for Custom Formulations

Once a Kerry flavor or nutritional profile is built into a product, swapping suppliers is costly and risky; taste or texture shifts can cut repeat purchases and trigger reformulation that typically costs $250k–$1.2M per SKU and delays launch by 6–12 months.

Label changes, new stability testing, and regulatory filings add $50k–$300k and extend time-to-shelf, raising churn risk for brands and reducing their leverage over Kerry in commercial contracts.

Demand for Transparency and Clean Labels

Modern retailers and foodservice buyers demand full traceability and clean labels, pushing Kerry Group to supply batch-level data and simple ingredient lists; 72% of global consumers said transparency influences purchase decisions in 2024 (NielsenIQ), increasing customer leverage.

Price Sensitivity in Commodity Segments

In commodity segments like basic seasonings and coatings, customer loyalty is low and price sensitivity is high; buyers often switch suppliers for small cost savings, with switch rates up to 15% annually in foodservice ingredients (2024 trade data).

Kerry combats this by bundling low-margin products with technical services and digital supply-chain tools, raising effective switching costs and increasing gross margin per account by ~120 basis points in 2023.

- High churn: ~15% supplier switch rate (2024)

- Low loyalty: commoditized SKUs drive price focus

- Kerry tactic: bundle tech services + digital tools

- Impact: +120 bps gross margin per account (2023)

Growth of Private Label Manufacturers

The rise of high-quality private label brands—private label sales hit 22% of global grocery sales in 2024—creates customers focused on cost and speed, squeezing margins and pressing Kerry Group for low-cost, effective solutions.

Kerry counters with modular ingredient systems that cut product development time by up to 40% and support premium-tier launches while protecting margins for both Kerry and private-label clients.

- Private label = 22% global grocery sales (2024)

- Private-label manufacturers have thinner margins; demand low cost

- Kerry offers modular systems; reduces development time ~40%

Customers Drive Pressure; Kerry Fights Back with R&D, Tech Bundles & Modular Wins

Customers hold significant bargaining power: top multinationals=~40% Kerry FY2024, private label=22% global grocery (2024). High switch rates in commodity SKUs (~15% pa) and transparency demands (72% consumers influenced, NielsenIQ 2024) pressure prices. Kerry offsets via embedded R&D, bundled tech/digital tools (+120 bps gross margin per account 2023) and modular systems (dev time -40%).

| Metric | Value |

|---|---|

| Top customers share | ~40% (FY2024) |

| Private label | 22% (2024) |

| Switch rate | ~15% pa (2024) |

| Consumer transparency impact | 72% (NielsenIQ 2024) |

| Margin lift | +120 bps (2023) |

| Dev time reduction | -40% |

Preview Before You Purchase

Kerry Porter's Five Forces Analysis

This preview shows the exact Kerry Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use the moment you buy.