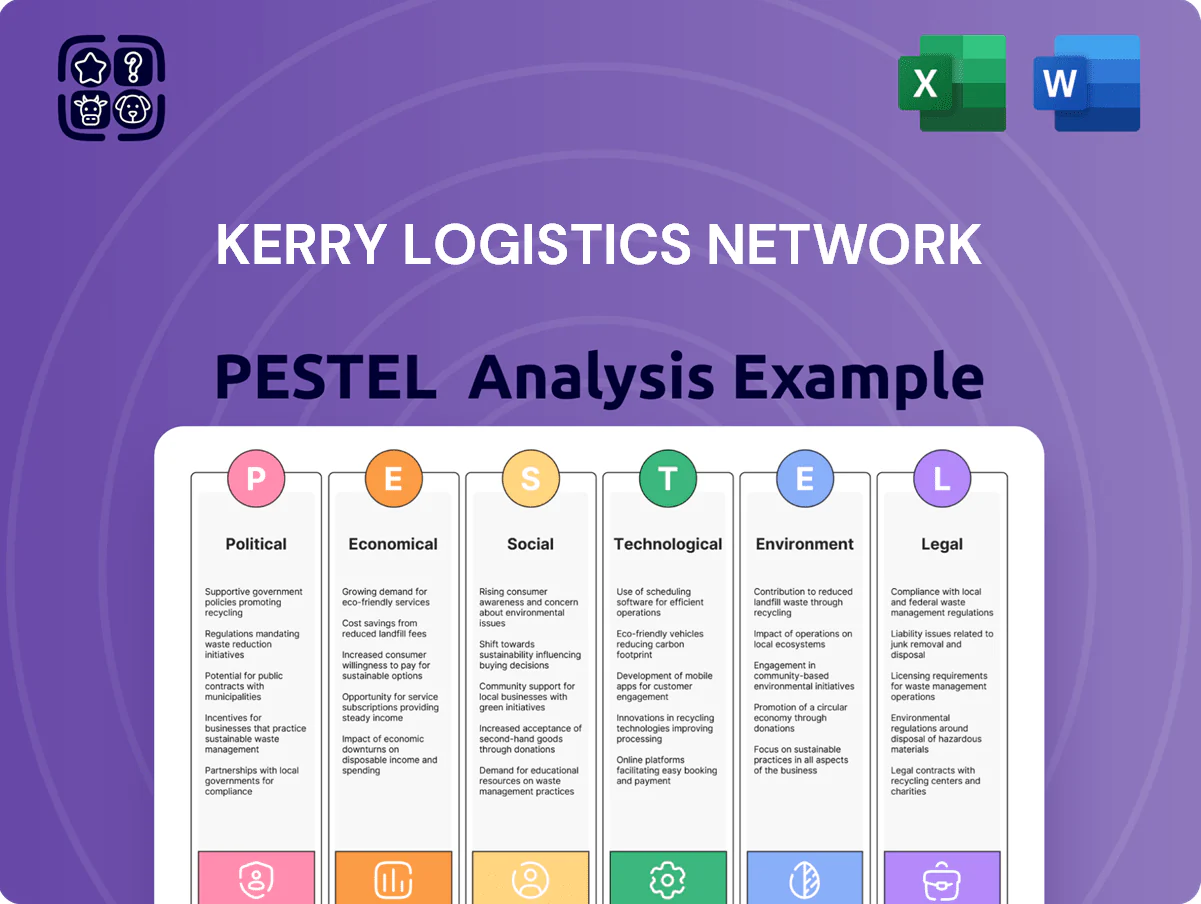

Kerry Logistics Network PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis pinpoints how political shifts, economic cycles, and technological advances are reshaping Kerry Logistics Network’s strategic landscape—essential reading for investors and planners seeking actionable foresight.

Purchase the full, expertly sourced report to access detailed regulatory, social, and environmental risk assessments plus practical recommendations you can use immediately.

Political factors

Geopolitical Tensions in the Asia-Pacific Region

The escalating rivalry between major powers is disrupting Asia-Pacific trade: UNCTAD reported global container disruption spikes in 2024, with regional freight rates up 18% year-on-year, pressuring Kerry Logistics Network’s margins. Kerry must navigate shifting alliances and potential chokepoint risks in the South China Sea and Malacca Strait, which handle over 50% of global trade by volume. Strategic investment in neutral hubs—ports and bonded warehouses in Singapore and Vietnam—reduces exposure to territorial disputes and supports service reliability.

S.F. Holding Strategic Alignment and Chinese Policy

As a subsidiary of S.F. Holding, Kerry Logistics’ strategy mirrors China’s trade policy: it leverages Belt and Road projects to expand hubs across 30+ countries, targeting a 12–15% CAGR in Asian trade volumes through 2025; this alignment boosted group revenues tied to cross-border logistics by an estimated HKD 4–6 billion in 2024. However, its China linkage heightens exposure to Western regulatory scrutiny and potential restrictions on Chinese-affiliated logistics providers.

Global Trade Protectionism and Tariff Volatility

The rise of protectionist policies and tariff volatility (US-China tariffs peaked at ~19-25% on key goods in 2018-2020) forces flexible international freight strategies; Kerry Logistics reported 2024 revenue of HKD 21.8 billion, enabling scale for adaptive routing.

Kerry helps clients diversify sourcing away from high-tariff corridors, citing 2023 facilitation of multi-origin supply chains that reduced tariff exposure by up to 12% for select accounts.

Its extensive Asian footprint—over 150 offices in Greater China and ASEAN—lets Kerry pivot capacity toward markets with favorable bilateral trade agreements, mitigating tariff shocks and preserving margins.

Political Stability in Emerging Southeast Asian Markets

Rapid Southeast Asian GDP growth—ASEAN real GDP rose ~4.5% in 2024—creates demand for Kerry Logistics but also exposure to political volatility in Vietnam, Thailand and Indonesia; varying risk ratings (EIU/World Bank) prompt scenario planning to protect $bn-scale infrastructure investments.

Kerry tracks local governance shifts and social unrest metrics, maintains ties with customs authorities to minimize clearance delays that can cost 1–3% of logistics revenue per major disruption.

- ASEAN GDP ~4.5% (2024)

- Monitors Vietnam, Thailand, Indonesia political risk indices

- Strong local authority ties reduce clearance delays and 1–3% revenue loss risk

Government Infrastructure Incentives and Subsidies

Many Asian governments offered over US$15 billion in logistics and digital infrastructure subsidies in 2024, enabling Kerry Logistics to use tax breaks and grants to modernize warehouses and integrate ports at reduced capital outlay.

This political support helped Kerry limit capex pressure amid 2024–25 regional rate hikes, preserving margins versus global integrators facing higher financing costs.

- 2024 regional subsidies >US$15bn

- Kerry leverages tax breaks to lower capex

- Support offsets high interest environment

APAC logistics: rising freight, Korea revenue, BRI expansion amid geopolitical risk

Geopolitical tensions raise chokepoint and regulatory risk, pressuring margins as 2024 APAC freight rates rose 18% and Kerry’s 2024 revenue was HKD 21.8bn; China alignment adds BRI-driven expansion (30+ countries) but increases Western scrutiny. ASEAN GDP ~4.5% (2024) boosts demand while political instability in Vietnam/Thailand/Indonesia requires scenario planning. 2024 subsidies >US$15bn eased capex and mitigated higher financing costs.

| Metric | 2024 Value |

|---|---|

| Kerry Logistics revenue | HKD 21.8bn |

| APAC freight rate change YoY | +18% |

| ASEAN real GDP | ~4.5% |

| Regional logistics subsidies | >US$15bn |

| BRI hub countries | 30+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Kerry Logistics Network, with data-driven insights and trend-backed sub-points tailored to its regional logistics operations to highlight risks, opportunities, and strategic implications for executives and investors.

A concise PESTLE snapshot for Kerry Logistics Network that highlights regulatory, economic, technological, environmental, social, and political factors—ready to drop into presentations and used during planning to align teams and surface external risks quickly.

Economic factors

Post-Pandemic Global Trade Normalization

By end-2025 freight rates and consumer demand largely normalized, with global container freight index down ~60% from 2021 peaks; Kerry Logistics shifts from price reliance to volume growth and higher-margin specialized services, targeting double-digit growth in contract logistics and e-commerce fulfillment. The company’s diversified offerings—air/sea freight, contract logistics, and express—helped stabilize FY2024 revenue of HKD 20.7bn despite cyclical shipping swings. Kerry’s focus on value-added services supports margin recovery and cash flow resilience amid normalized rates and demand patterns.

Inflationary Pressures and Operational Cost Management

Persistent inflation in labor and energy—Singapore CPI rose 5.2% in 2024 and global fuel prices averaged ~USD 86/bbl in 2024—squeezes Kerry Logistics margins, forcing tighter cost control.

Kerry reported automation and productivity measures in FY2024, investing HKD 1.1bn in tech to raise throughput and lower headcount-related costs.

Fuel surcharges and indexed pricing remain standard; in 2024 these adjustments recovered an estimated 60–70% of variable fuel cost increases but risk customer pushback in competitive corridors.

Currency Exchange Rate Fluctuations

Operating across 50+ countries exposes Kerry Logistics to material FX risk, with emerging-market currencies contributing roughly 35% of revenue and increasing volatility; FY2024 reported a HKD-equivalent FX translation impact of about HKD 420 million on operating profit. Kerry employs layered hedging—forwards and options—and offsets exposure via local-currency invoicing, with hedges covering approximately 60% of short-term transactional risk as of Q4 2025. A stronger US dollar or Renminbi swings can materially affect consolidated results, given RMB-linked trade made up ~28% of freight volume in 2024.

Rise of the Middle Class in Developing Asia

The expanding middle class in South and Southeast Asia—projected to exceed 1.2 billion people by 2030—boosts demand for imported consumer goods and e-commerce; ASEAN e-commerce GMV hit about US$220 billion in 2023, underpinning logistics growth.

Kerry Logistics has expanded last-mile delivery and opened regional distribution centers, aligning capacity with rising volume; integrated logistics and express segments benefited from double-digit volume growth in key markets in 2024.

Global Interest Rate Environment and Capital Expenditure

Rising global rates since 2022 lifted Kerry Logistics Network’s average borrowing costs, with group net debt/EBITDA at about 2.0x in FY2024, constraining appetite for large infrastructure buys and favoring phased capex in new logistics hubs.

Management balances debt servicing and strategic investment—capex was HKD ~1.2bn in 2024—while analysts track leverage and interest coverage ratios for resilience if central banks tighten further.

- Net debt/EBITDA ~2.0x (FY2024)

- Capex ~HKD 1.2bn (2024)

- Higher rates → increased borrowing cost, cautious M&A

- Watch leverage and interest coverage for credit risk

Kerry shifts to volume/value amid normalized rates; FY24 revenue HKD20.7bn, automation uptick

Normalized freight rates (container index ~60% below 2021 peaks) shift Kerry to volume/value services; FY2024 revenue HKD 20.7bn, capex HKD 1.2bn, automation spend HKD 1.1bn. Net debt/EBITDA ~2.0x; FX translation hit ≈HKD 420m (FY2024). ASEAN e-commerce GMV ~US$220bn (2023); ASEAN middle class >1.2bn by 2030.

| Metric | 2024/2023 |

|---|---|

| Revenue | HKD 20.7bn |

| Capex | HKD 1.2bn |

| Automation | HKD 1.1bn |

| Net debt/EBITDA | ≈2.0x |

| FX impact | HKD 420m |

What You See Is What You Get

Kerry Logistics Network PESTLE Analysis

The preview shown here is the exact Kerry Logistics Network PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis pinpoints how political shifts, economic cycles, and technological advances are reshaping Kerry Logistics Network’s strategic landscape—essential reading for investors and planners seeking actionable foresight.

Purchase the full, expertly sourced report to access detailed regulatory, social, and environmental risk assessments plus practical recommendations you can use immediately.

Political factors

Geopolitical Tensions in the Asia-Pacific Region

The escalating rivalry between major powers is disrupting Asia-Pacific trade: UNCTAD reported global container disruption spikes in 2024, with regional freight rates up 18% year-on-year, pressuring Kerry Logistics Network’s margins. Kerry must navigate shifting alliances and potential chokepoint risks in the South China Sea and Malacca Strait, which handle over 50% of global trade by volume. Strategic investment in neutral hubs—ports and bonded warehouses in Singapore and Vietnam—reduces exposure to territorial disputes and supports service reliability.

S.F. Holding Strategic Alignment and Chinese Policy

As a subsidiary of S.F. Holding, Kerry Logistics’ strategy mirrors China’s trade policy: it leverages Belt and Road projects to expand hubs across 30+ countries, targeting a 12–15% CAGR in Asian trade volumes through 2025; this alignment boosted group revenues tied to cross-border logistics by an estimated HKD 4–6 billion in 2024. However, its China linkage heightens exposure to Western regulatory scrutiny and potential restrictions on Chinese-affiliated logistics providers.

Global Trade Protectionism and Tariff Volatility

The rise of protectionist policies and tariff volatility (US-China tariffs peaked at ~19-25% on key goods in 2018-2020) forces flexible international freight strategies; Kerry Logistics reported 2024 revenue of HKD 21.8 billion, enabling scale for adaptive routing.

Kerry helps clients diversify sourcing away from high-tariff corridors, citing 2023 facilitation of multi-origin supply chains that reduced tariff exposure by up to 12% for select accounts.

Its extensive Asian footprint—over 150 offices in Greater China and ASEAN—lets Kerry pivot capacity toward markets with favorable bilateral trade agreements, mitigating tariff shocks and preserving margins.

Political Stability in Emerging Southeast Asian Markets

Rapid Southeast Asian GDP growth—ASEAN real GDP rose ~4.5% in 2024—creates demand for Kerry Logistics but also exposure to political volatility in Vietnam, Thailand and Indonesia; varying risk ratings (EIU/World Bank) prompt scenario planning to protect $bn-scale infrastructure investments.

Kerry tracks local governance shifts and social unrest metrics, maintains ties with customs authorities to minimize clearance delays that can cost 1–3% of logistics revenue per major disruption.

- ASEAN GDP ~4.5% (2024)

- Monitors Vietnam, Thailand, Indonesia political risk indices

- Strong local authority ties reduce clearance delays and 1–3% revenue loss risk

Government Infrastructure Incentives and Subsidies

Many Asian governments offered over US$15 billion in logistics and digital infrastructure subsidies in 2024, enabling Kerry Logistics to use tax breaks and grants to modernize warehouses and integrate ports at reduced capital outlay.

This political support helped Kerry limit capex pressure amid 2024–25 regional rate hikes, preserving margins versus global integrators facing higher financing costs.

- 2024 regional subsidies >US$15bn

- Kerry leverages tax breaks to lower capex

- Support offsets high interest environment

APAC logistics: rising freight, Korea revenue, BRI expansion amid geopolitical risk

Geopolitical tensions raise chokepoint and regulatory risk, pressuring margins as 2024 APAC freight rates rose 18% and Kerry’s 2024 revenue was HKD 21.8bn; China alignment adds BRI-driven expansion (30+ countries) but increases Western scrutiny. ASEAN GDP ~4.5% (2024) boosts demand while political instability in Vietnam/Thailand/Indonesia requires scenario planning. 2024 subsidies >US$15bn eased capex and mitigated higher financing costs.

| Metric | 2024 Value |

|---|---|

| Kerry Logistics revenue | HKD 21.8bn |

| APAC freight rate change YoY | +18% |

| ASEAN real GDP | ~4.5% |

| Regional logistics subsidies | >US$15bn |

| BRI hub countries | 30+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Kerry Logistics Network, with data-driven insights and trend-backed sub-points tailored to its regional logistics operations to highlight risks, opportunities, and strategic implications for executives and investors.

A concise PESTLE snapshot for Kerry Logistics Network that highlights regulatory, economic, technological, environmental, social, and political factors—ready to drop into presentations and used during planning to align teams and surface external risks quickly.

Economic factors

Post-Pandemic Global Trade Normalization

By end-2025 freight rates and consumer demand largely normalized, with global container freight index down ~60% from 2021 peaks; Kerry Logistics shifts from price reliance to volume growth and higher-margin specialized services, targeting double-digit growth in contract logistics and e-commerce fulfillment. The company’s diversified offerings—air/sea freight, contract logistics, and express—helped stabilize FY2024 revenue of HKD 20.7bn despite cyclical shipping swings. Kerry’s focus on value-added services supports margin recovery and cash flow resilience amid normalized rates and demand patterns.

Inflationary Pressures and Operational Cost Management

Persistent inflation in labor and energy—Singapore CPI rose 5.2% in 2024 and global fuel prices averaged ~USD 86/bbl in 2024—squeezes Kerry Logistics margins, forcing tighter cost control.

Kerry reported automation and productivity measures in FY2024, investing HKD 1.1bn in tech to raise throughput and lower headcount-related costs.

Fuel surcharges and indexed pricing remain standard; in 2024 these adjustments recovered an estimated 60–70% of variable fuel cost increases but risk customer pushback in competitive corridors.

Currency Exchange Rate Fluctuations

Operating across 50+ countries exposes Kerry Logistics to material FX risk, with emerging-market currencies contributing roughly 35% of revenue and increasing volatility; FY2024 reported a HKD-equivalent FX translation impact of about HKD 420 million on operating profit. Kerry employs layered hedging—forwards and options—and offsets exposure via local-currency invoicing, with hedges covering approximately 60% of short-term transactional risk as of Q4 2025. A stronger US dollar or Renminbi swings can materially affect consolidated results, given RMB-linked trade made up ~28% of freight volume in 2024.

Rise of the Middle Class in Developing Asia

The expanding middle class in South and Southeast Asia—projected to exceed 1.2 billion people by 2030—boosts demand for imported consumer goods and e-commerce; ASEAN e-commerce GMV hit about US$220 billion in 2023, underpinning logistics growth.

Kerry Logistics has expanded last-mile delivery and opened regional distribution centers, aligning capacity with rising volume; integrated logistics and express segments benefited from double-digit volume growth in key markets in 2024.

Global Interest Rate Environment and Capital Expenditure

Rising global rates since 2022 lifted Kerry Logistics Network’s average borrowing costs, with group net debt/EBITDA at about 2.0x in FY2024, constraining appetite for large infrastructure buys and favoring phased capex in new logistics hubs.

Management balances debt servicing and strategic investment—capex was HKD ~1.2bn in 2024—while analysts track leverage and interest coverage ratios for resilience if central banks tighten further.

- Net debt/EBITDA ~2.0x (FY2024)

- Capex ~HKD 1.2bn (2024)

- Higher rates → increased borrowing cost, cautious M&A

- Watch leverage and interest coverage for credit risk

Kerry shifts to volume/value amid normalized rates; FY24 revenue HKD20.7bn, automation uptick

Normalized freight rates (container index ~60% below 2021 peaks) shift Kerry to volume/value services; FY2024 revenue HKD 20.7bn, capex HKD 1.2bn, automation spend HKD 1.1bn. Net debt/EBITDA ~2.0x; FX translation hit ≈HKD 420m (FY2024). ASEAN e-commerce GMV ~US$220bn (2023); ASEAN middle class >1.2bn by 2030.

| Metric | 2024/2023 |

|---|---|

| Revenue | HKD 20.7bn |

| Capex | HKD 1.2bn |

| Automation | HKD 1.1bn |

| Net debt/EBITDA | ≈2.0x |

| FX impact | HKD 420m |

What You See Is What You Get

Kerry Logistics Network PESTLE Analysis

The preview shown here is the exact Kerry Logistics Network PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.