Kesko SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Kesko’s robust retail network and strong market presence in the Nordics position it well for steady growth, yet shifting consumer habits and supply-chain pressures present clear challenges; uncover opportunities in digital expansion and sustainability by purchasing the full SWOT analysis for a professionally formatted, editable report and Excel matrix to support investment and strategic decisions.

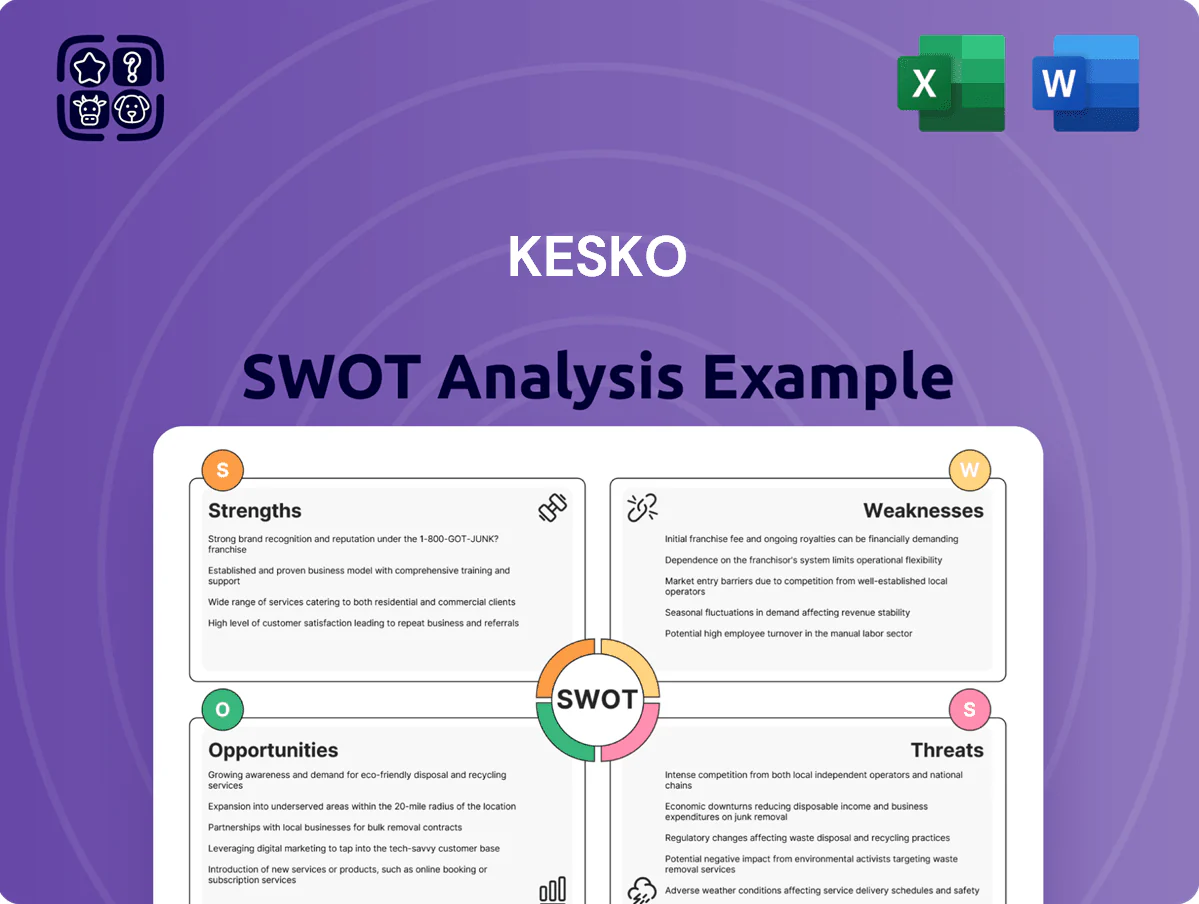

Strengths

Dominant Market Position in Finland

Kesko dominates Finnish grocery and building trades, holding about 33% market share in grocery retail and 40% in building supplies in 2024, giving a stable revenue base of €11.2bn group sales in Finland (2024).

The K-Group’s integrated franchise-and-own model drives high brand recognition and trust nationwide, with ~1,200 stores and 2.6m loyalty card users boosting repeat sales.

Scale yields strong supplier bargaining power and logistics: Kesko’s centralized procurement cut COGS by ~0.8ppt in 2023, a gap smaller rivals struggle to match.

Diversified Business Portfolio

Kesko’s diversified portfolio across grocery, building & technical trade, and car trade cushions sector-specific shocks; in 2024 groceries accounted for ~43% of group sales, balancing the more cyclical building trade. The building segment is interest-rate sensitive, yet the grocery segment delivered stable like-for-like sales growth of 2.1% in 2024, supporting cash flow. This mix helped Kesko sustain a dividend of EUR 0.95 per share in 2024 and a stable operating cash flow of EUR 540m, reducing reliance on any single market.

Advanced Data Analytics and Loyalty Program

Efficient Logistics and Supply Chain Network

Kesko has invested over EUR 300m since 2018 in automated logistics centers and digital supply-chain systems, cutting stockouts to under 2% and reducing waste by ~18% in 2024.

These systems cut operational costs—Kesko reported a 1.6 percentage-point improvement in gross margin contribution from logistics in 2024—and speed deliveries for stores and e-commerce, shortening lead times by ~24%.

A modern logistics backbone—12 automated centers in Finland and the Baltics as of 2025—creates a high entry barrier for international rivals.

- EUR 300m+ investment since 2018

- Stockouts <2% (2024)

- Waste −18% (2024)

- Lead times −24%

- 12 automated centers (2025)

Strong Sustainability and ESG Integration

- CDP A-list (2024)

- ~18% emissions cut (scope 1–3, 2019–2023)

- Net-zero target by 2030

- High Sustainalytics score (2024)

Kesko: Market-leading scale, resilient cash flow and net-zero-by-2030 momentum

Kesko’s market leadership (≈33% grocery, 40% building, 2024) plus €11.2bn Finnish sales, 1,200 stores, 3.6m K-Plussa members (2025) and scale-driven procurement savings (~0.8ppt COGS), EUR 300m+ logistics spend since 2018, stockouts <2% (2024), waste −18% (2024), 12 automated centers (2025), CDP A-list (2024) and net-zero by 2030 target underpin resilient cash flow and strong margins.

| Metric | Value |

|---|---|

| Grocery share | 33% (2024) |

| Sales Finland | €11.2bn (2024) |

| K-Plussa | 3.6m (2025) |

What is included in the product

Delivers a strategic overview of Kesko’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Offers a concise Kesko SWOT matrix for rapid strategic alignment and stakeholder-ready summaries, enabling quick edits to reflect changing market conditions.

Weaknesses

High Geographic Concentration

A vast majority of Kesko Oyj’s revenue comes from Finland—about 75% of 2024 net sales (EUR 9.6bn of EUR 12.8bn)—so the group is highly exposed to the Finnish economy and consumer spending.

Limited international diversification caps growth versus multinationals like Carrefour or Tesco, which generate revenues across many markets.

Any Finnish GDP drop or local regulatory change can disproportionately dent margins and cash flow, raising volatility for the whole group.

Vulnerability to Construction Industry Cycles

The building and technical trade segment is highly sensitive to interest rates and Finland’s housing market; in 2024 rising rates correlated with a 6% drop in Kesko’s building trade sales year-on-year, squeezing gross margins by ~120 basis points. During periods of high rates or low consumer confidence this division sees lower volumes and margin pressure, contributing to earnings volatility that can offset the grocery trade’s steadier results. This cyclicality drove K Group’s building trade operating profit variability of ±15% across 2021–2024.

Complex Merchant-Based Operating Model

Kesko’s merchant-based model, with roughly 1,200 independent K-retailers as of 2025, boosts local ties but causes uneven in-store execution and brand experience across Finland, Sweden, and the Baltics.

That decentralization complicates roll-out of corporate strategies and unified digital projects—Kesko reported IT and coordination costs rising 6% in 2024 to support merchant integration.

Managing relations with hundreds of retailers demands substantial management bandwidth and slows decision cycles, affecting agility versus centrally-run rivals.

Dependence on Third-Party Logistics Partners

Despite strong internal logistics, Kesko still uses third-party partners for last-mile delivery and international freight; in 2024 about 18% of its total goods movements were outsourced, raising exposure.

Global shipping disruptions and 2023–24 Nordic transport strikes showed how delays can cause stockouts and lost sales; Kesko reported logistics-related lost sales of roughly EUR 45m in 2023.

These external links create supply-chain vulnerabilities largely beyond Kesko’s direct control, increasing risk to margins and service levels.

- ~18% outsourced shipments (2024)

- EUR 45m lost sales from logistics issues (2023)

- High exposure to shipping lane disruption and strikes

Lower Profit Margins in Car Trade

The car trade unit posts notably lower gross margins than Kesko’s grocery and Rautakesko (hardware) chains; in 2024 auto gross margin averaged ~6–8% vs groceries' ~20% and hardware's ~25%.

EV transition and subscription pilots demand heavy capex—Kesko Car’s estimated fleet and charging investments exceeded €80m in 2024—raising depreciation and financing costs.

High inventory carrying costs and fierce price competition compress returns; automotive working capital tied-up days were ~45–60 in 2024, dragging consolidated ROIC.

- Auto gross margin ~6–8%

- Grocery ~20%, hardware ~25%

- Capex/EV programs >€80m (2024)

- Inventory days 45–60 (2024)

Kesko: Finland-reliant retailer faces margin pressure, logistics gaps and EV-driven strain

Kesko is highly Finland-concentrated (~75% of 2024 net sales: EUR 9.6bn/12.8bn), leaving it exposed to local GDP swings and regulation; building trade fell 6% y/y in 2024, cutting gross margin ~120bp and driving ±15% operating profit variability 2021–24. Merchant model (~1,200 retailers in 2025) creates uneven execution and rising IT costs (+6% in 2024). Logistics outsourcing ~18% (2024) led to ~EUR 45m lost sales in 2023; car unit margins low (~6–8% vs grocery ~20%, hardware ~25%) with >€80m EV capex in 2024 causing working capital strain.

| Metric | Value (Year) |

|---|---|

| Finland share of sales | 75% (2024) |

| Net sales | EUR 12.8bn (2024) |

| Building trade sales change | -6% (2024) |

| Merchant count | ~1,200 (2025) |

| Outsourced shipments | ~18% (2024) |

| Logistics lost sales | EUR 45m (2023) |

| Auto gross margin | 6–8% (2024) |

| Grocery/hardware margins | ~20% / ~25% (2024) |

| EV capex | >€80m (2024) |

What You See Is What You Get

Kesko SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kesko’s robust retail network and strong market presence in the Nordics position it well for steady growth, yet shifting consumer habits and supply-chain pressures present clear challenges; uncover opportunities in digital expansion and sustainability by purchasing the full SWOT analysis for a professionally formatted, editable report and Excel matrix to support investment and strategic decisions.

Strengths

Dominant Market Position in Finland

Kesko dominates Finnish grocery and building trades, holding about 33% market share in grocery retail and 40% in building supplies in 2024, giving a stable revenue base of €11.2bn group sales in Finland (2024).

The K-Group’s integrated franchise-and-own model drives high brand recognition and trust nationwide, with ~1,200 stores and 2.6m loyalty card users boosting repeat sales.

Scale yields strong supplier bargaining power and logistics: Kesko’s centralized procurement cut COGS by ~0.8ppt in 2023, a gap smaller rivals struggle to match.

Diversified Business Portfolio

Kesko’s diversified portfolio across grocery, building & technical trade, and car trade cushions sector-specific shocks; in 2024 groceries accounted for ~43% of group sales, balancing the more cyclical building trade. The building segment is interest-rate sensitive, yet the grocery segment delivered stable like-for-like sales growth of 2.1% in 2024, supporting cash flow. This mix helped Kesko sustain a dividend of EUR 0.95 per share in 2024 and a stable operating cash flow of EUR 540m, reducing reliance on any single market.

Advanced Data Analytics and Loyalty Program

Efficient Logistics and Supply Chain Network

Kesko has invested over EUR 300m since 2018 in automated logistics centers and digital supply-chain systems, cutting stockouts to under 2% and reducing waste by ~18% in 2024.

These systems cut operational costs—Kesko reported a 1.6 percentage-point improvement in gross margin contribution from logistics in 2024—and speed deliveries for stores and e-commerce, shortening lead times by ~24%.

A modern logistics backbone—12 automated centers in Finland and the Baltics as of 2025—creates a high entry barrier for international rivals.

- EUR 300m+ investment since 2018

- Stockouts <2% (2024)

- Waste −18% (2024)

- Lead times −24%

- 12 automated centers (2025)

Strong Sustainability and ESG Integration

- CDP A-list (2024)

- ~18% emissions cut (scope 1–3, 2019–2023)

- Net-zero target by 2030

- High Sustainalytics score (2024)

Kesko: Market-leading scale, resilient cash flow and net-zero-by-2030 momentum

Kesko’s market leadership (≈33% grocery, 40% building, 2024) plus €11.2bn Finnish sales, 1,200 stores, 3.6m K-Plussa members (2025) and scale-driven procurement savings (~0.8ppt COGS), EUR 300m+ logistics spend since 2018, stockouts <2% (2024), waste −18% (2024), 12 automated centers (2025), CDP A-list (2024) and net-zero by 2030 target underpin resilient cash flow and strong margins.

| Metric | Value |

|---|---|

| Grocery share | 33% (2024) |

| Sales Finland | €11.2bn (2024) |

| K-Plussa | 3.6m (2025) |

What is included in the product

Delivers a strategic overview of Kesko’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Offers a concise Kesko SWOT matrix for rapid strategic alignment and stakeholder-ready summaries, enabling quick edits to reflect changing market conditions.

Weaknesses

High Geographic Concentration

A vast majority of Kesko Oyj’s revenue comes from Finland—about 75% of 2024 net sales (EUR 9.6bn of EUR 12.8bn)—so the group is highly exposed to the Finnish economy and consumer spending.

Limited international diversification caps growth versus multinationals like Carrefour or Tesco, which generate revenues across many markets.

Any Finnish GDP drop or local regulatory change can disproportionately dent margins and cash flow, raising volatility for the whole group.

Vulnerability to Construction Industry Cycles

The building and technical trade segment is highly sensitive to interest rates and Finland’s housing market; in 2024 rising rates correlated with a 6% drop in Kesko’s building trade sales year-on-year, squeezing gross margins by ~120 basis points. During periods of high rates or low consumer confidence this division sees lower volumes and margin pressure, contributing to earnings volatility that can offset the grocery trade’s steadier results. This cyclicality drove K Group’s building trade operating profit variability of ±15% across 2021–2024.

Complex Merchant-Based Operating Model

Kesko’s merchant-based model, with roughly 1,200 independent K-retailers as of 2025, boosts local ties but causes uneven in-store execution and brand experience across Finland, Sweden, and the Baltics.

That decentralization complicates roll-out of corporate strategies and unified digital projects—Kesko reported IT and coordination costs rising 6% in 2024 to support merchant integration.

Managing relations with hundreds of retailers demands substantial management bandwidth and slows decision cycles, affecting agility versus centrally-run rivals.

Dependence on Third-Party Logistics Partners

Despite strong internal logistics, Kesko still uses third-party partners for last-mile delivery and international freight; in 2024 about 18% of its total goods movements were outsourced, raising exposure.

Global shipping disruptions and 2023–24 Nordic transport strikes showed how delays can cause stockouts and lost sales; Kesko reported logistics-related lost sales of roughly EUR 45m in 2023.

These external links create supply-chain vulnerabilities largely beyond Kesko’s direct control, increasing risk to margins and service levels.

- ~18% outsourced shipments (2024)

- EUR 45m lost sales from logistics issues (2023)

- High exposure to shipping lane disruption and strikes

Lower Profit Margins in Car Trade

The car trade unit posts notably lower gross margins than Kesko’s grocery and Rautakesko (hardware) chains; in 2024 auto gross margin averaged ~6–8% vs groceries' ~20% and hardware's ~25%.

EV transition and subscription pilots demand heavy capex—Kesko Car’s estimated fleet and charging investments exceeded €80m in 2024—raising depreciation and financing costs.

High inventory carrying costs and fierce price competition compress returns; automotive working capital tied-up days were ~45–60 in 2024, dragging consolidated ROIC.

- Auto gross margin ~6–8%

- Grocery ~20%, hardware ~25%

- Capex/EV programs >€80m (2024)

- Inventory days 45–60 (2024)

Kesko: Finland-reliant retailer faces margin pressure, logistics gaps and EV-driven strain

Kesko is highly Finland-concentrated (~75% of 2024 net sales: EUR 9.6bn/12.8bn), leaving it exposed to local GDP swings and regulation; building trade fell 6% y/y in 2024, cutting gross margin ~120bp and driving ±15% operating profit variability 2021–24. Merchant model (~1,200 retailers in 2025) creates uneven execution and rising IT costs (+6% in 2024). Logistics outsourcing ~18% (2024) led to ~EUR 45m lost sales in 2023; car unit margins low (~6–8% vs grocery ~20%, hardware ~25%) with >€80m EV capex in 2024 causing working capital strain.

| Metric | Value (Year) |

|---|---|

| Finland share of sales | 75% (2024) |

| Net sales | EUR 12.8bn (2024) |

| Building trade sales change | -6% (2024) |

| Merchant count | ~1,200 (2025) |

| Outsourced shipments | ~18% (2024) |

| Logistics lost sales | EUR 45m (2023) |

| Auto gross margin | 6–8% (2024) |

| Grocery/hardware margins | ~20% / ~25% (2024) |

| EV capex | >€80m (2024) |

What You See Is What You Get

Kesko SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.